- Processed Food

- Fish Fermentation Market

Fish Fermentation Market Size, Share, and Growth Forecast, 2026 – 2033

Fish Fermentation Market by Product Type (Traditional Fermented Fish, Fish Sauces, Others), Process Type (Natural Fermentation, Others), End-user (Foodservice Industry, Household Consumption, Retail Grocery Stores, Online Food Retailers), and Regional Analysis for 2026-2033

Fish Fermentation Market Share and Trends Analysis

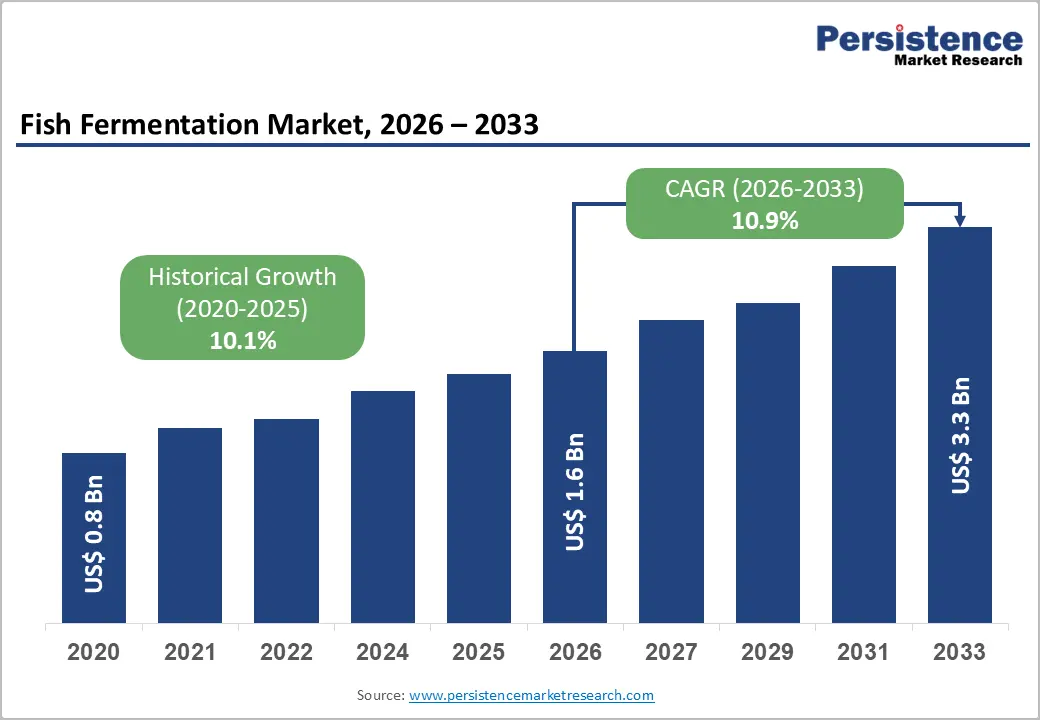

The global fish fermentation market size is likely to be valued at US$1.6 billion in 2026 and is estimated to reach US$3.3 billion by 2033, growing at a CAGR of 10.9% during the forecast period 2026−2033, driven by rising demand for natural preservation and functional foods, supported by increasing awareness of gut health and microbiome nutrition.

Urbanization and evolving diets boost consumption of fermented seafood with longer shelf life and enhanced flavor. Healthcare-led shifts toward probiotic-rich diets increase adoption. Technological advancements improve scalability and consistency. Guidelines from the Food and Agriculture Organization and World Health Organization (WHO) strengthen food safety, while retail expansion and cold chain investments enhance accessibility and global trade integration.

Key Industry Highlights:

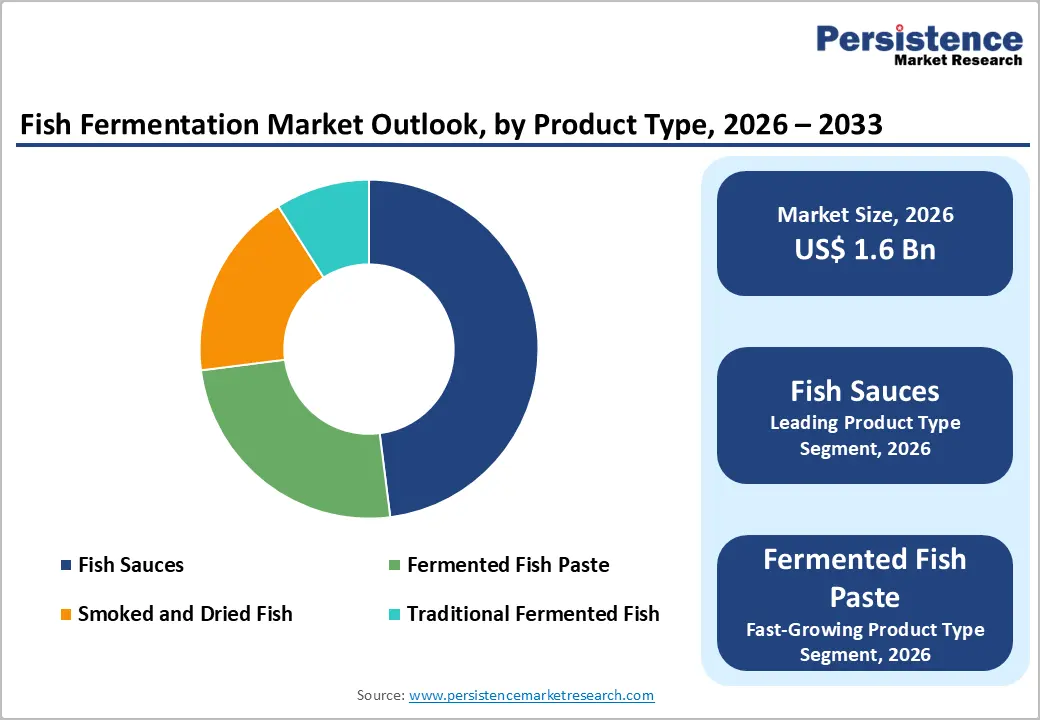

- Leading Product Type: Fish sauces are set to hold around 48% revenue share in 2026, driven by established culinary integration and consistent demand across foodservice and retail channels.

- Fastest-Growing Product Type: Fermented fish paste is projected as the fastest-growing segment, supported by expansion in functional condiment applications and innovation in flavor stabilization.

- Leading End-user: Household consumption is estimated to hold roughly 42% revenue share in 2026, due to strong integration within daily meal preparation and broad accessibility through grocery channels.

- Fastest-Growing End-user: Online food retailers are forecast to record the fastest growth, driven by rising digital commerce penetration and premium product discovery in urban markets.

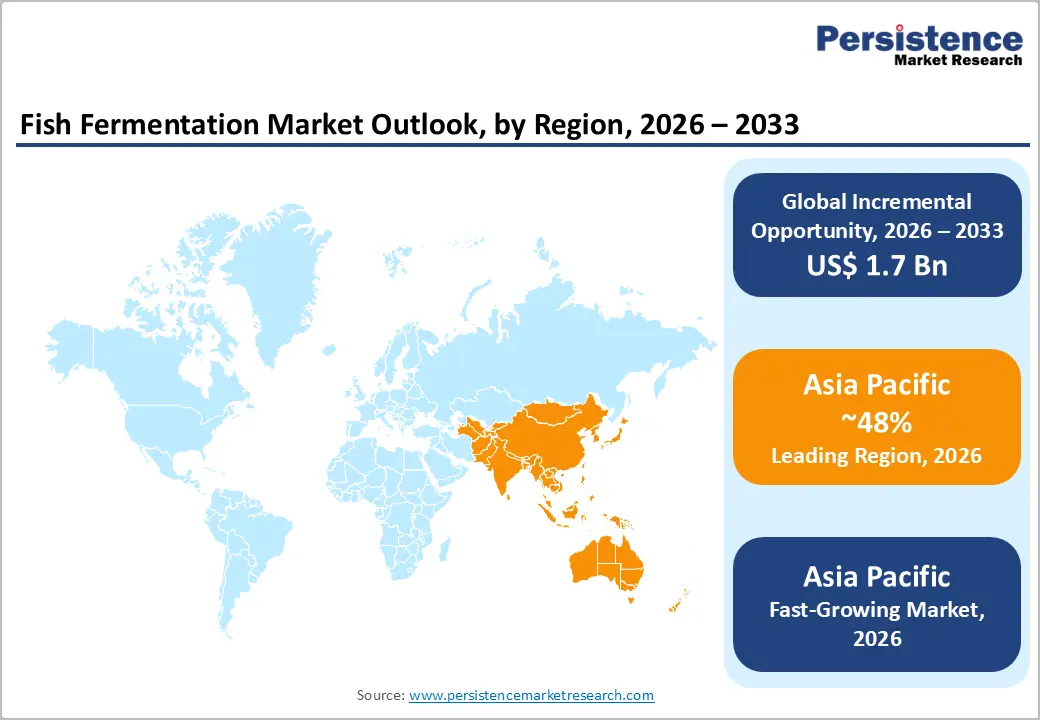

- Regional Leadership: Asia Pacific is projected to capture roughly 48% of the market share by 2026, while North America is forecasted to record the fastest growth due to demographic diversification and multicultural dietary trends.

- Competitive Environment: The market reflects a fragmented structure, with regional specialists leveraging authenticity, compliance, and supply-chain transparency to maintain competitive positioning.

- Innovation Trends: Precision fermentation techniques, sustainable sourcing initiatives, and digital distribution models are shaping long-term market evolution and investment direction.

DRO Analysis

Driver - Rising Global Demand for Functional and Probiotic Foods

Growing consumer focus on preventive nutrition elevates demand for fermented fish products rich in probiotics and bioactive compounds. Functional food positioning supports premium pricing and margin expansion across retail channels. Increasing awareness of gut microbiome balance strengthens preference for naturally fermented foods over synthetic supplements. This shift drives consistent consumption patterns and supports product diversification across urban food systems, reinforcing steady demand expansion and higher value realization for producers.

Industrial food processors respond through scaled fermentation systems that deliver standardized probiotic content and extended shelf stability. Efficiency gains reduce spoilage losses and improve inventory turnover across supply chains. Retailers prioritize high-value functional products, increasing shelf allocation and visibility. Expanding cold chain infrastructure supports wider geographic distribution. Investment in controlled cultures ensures consistent quality, enabling export growth and integration into global functional food segments with rising consumer spending on health-oriented dietary products.

Restraint - Stringent Food Safety and Regulatory Compliance Requirements

Strict safety frameworks impose high compliance costs across fermentation value chains. Standards defined by the Food and Agriculture Organization and the World Health Organization require validated microbial controls, traceability systems, and hygiene audits. Small producers face capital strain from certification, testing, and documentation processes. Limited technical capacity restricts adherence to standardized protocols. Delays in approvals slow product launches and restrict innovation cycles, reducing competitive flexibility in both domestic and export markets significantly.

Complex regulatory alignment across regions creates barriers for cross-border trade and scale expansion. Variations in permissible microbial strains, labeling rules, and storage standards disrupt supply chain uniformity. Producers allocate resources toward compliance management instead of process optimization. Informal sector participants struggle to transition into formal channels, limiting volume growth. Risk of recalls or penalties increases operational uncertainty, discouraging investment in new product development and advanced fermentation technologies across emerging economies.

Opportunity - Integration of Precision Fermentation Technologies

Precision fermentation technologies create a scalable pathway for high-value fermented seafood, improving yield consistency and reducing batch variability. Controlled microbial systems enable targeted flavor development and nutrient enrichment, supporting premium product positioning. Automation reduces labor intensity and waste levels, strengthening unit economics. According to the Food and Agriculture Organization 2022 data, global fish production reached about 223.2 million tonnes, expanding raw material availability for fermentation processing and industrial-scale applications across regional markets.

Market demand shifts toward functional and protein-rich foods support the adoption of precision-driven fermentation methods. Producers gain the capability to customize amino acid profiles and bioactive compounds, meeting health-oriented consumption patterns. Standardized processes improve regulatory compliance and traceability, enabling export readiness. Digital monitoring and bioreactor optimization increase throughput efficiency, lowering production costs per unit and supporting competitive pricing strategies in expanding urban retail and foodservice channels over time horizons.

Category-wise Analysis

Product Type Insights

Fish sauces are anticipated to secure around 48% of the fish fermentation market share in 2026, reflecting sustained preference in flavor applications across multiple cuisines. Established distribution channels boost accessibility in foodservice settings such as Thai restaurants and Vietnamese pho kitchens, where umami enhancement proves essential. Fish sauce serves as a sodium-efficient alternative in controlled portions for low-sodium diets. Packaging innovations like squeeze bottles improve shelf presence and drive repeat household use in salads and stir-fries.

Fermented fish paste is expected to be the fastest-growing segment, propelled by alignment with functional food trends that emphasize concentrated nutrient delivery. Paste formats enable precise dosing in recipes such as Korean gochujang blends, improving adherence among health-focused consumers. Flavor stabilization extends usability beyond traditional markets into global fusion cuisines. Bioactive retention during processing supports wellness applications. Retail penetration grows in specialty aisles for versatile condiments.

Process Type Insights

Natural fermentation is poised to dominate with a forecasted market share of over 52% in 2026, powered by entrenched cultural acceptance that builds consumer trust through generational familiarity. Traditional methods require minimal capital outlay and preserve authentic profiles in Southeast Asian fish sauces like Thai nam pla or Filipino bagoong. Clean-label preferences favor perceived natural attributes in preventive healthcare. Digital commerce educates on benefits, reinforcing trust among new buyers in Korean markets.

Controlled fermentation is estimated to be the fastest-growing segment from 2026 to 2033, fueled by technological predictability that addresses safety concerns and supports scalability. Standardized outcomes reduce batch variability in products like Japanese fermented mackerel, encouraging trial. Methods retain traditional taste in modern sushi applications while meeting expectations. Reliable supply enables consistent merchandising in U.S. retail. Traceability enhances nutrient documentation for healthcare adoption.

End-user Insights

Household consumption is likely to be the leading segment with a projected 42% of the fish fermentation market share in 2026, due to direct accessibility through grocery channels and integration into daily meal preparation. Unit packaging aligns with small-quantity needs in home cooking, such as stir-fries or marinades. Recipe apps boost engagement and repeat purchases for Thai curries. Dietary guides endorse products for flavor without excess additives. Nutritionists support through general recommendations.

Online food retailers are anticipated to be the fastest-growing segment, fueled by digitalization that removes geographic barriers and enables curated assortments. Subscription models serve non-traditional markets such as U.S. urban consumers seeking Asian condiments. Reduced margins cut costs for competitive pricing on Amazon Fresh. Algorithms drive the discovery of fish sauce varieties. Platforms link products to wellness content on gut health benefits.

Regional Insights

North America Fish Fermentation Market Trends

North America is forecast to be the fastest-growing market for fish fermentation, stimulated by the rapid expansion of functional food portfolios and premium condiment positioning across retail chains. Product innovation by companies such as Red Boat Fish Sauce and Blue Dragon strengthens shelf differentiation through clean-label claims and origin transparency. Regulatory clarity from the U.S. Food and Drug Administration supports standardized labeling and safety compliance, improving consumer confidence and accelerating category penetration across mainstream grocery channels.

E-commerce infrastructure and data-driven merchandising reshape demand generation and product discovery. Platforms such as Amazon and Walmart deploy recommendation engines that elevate niche fermented products into high-visibility categories. Immigration-driven culinary diversity increases adoption across households and foodservice operators. Investment in cold chain logistics and specialty distribution networks enhances product stability and reach. Strategic collaborations between importers and local distributors strengthen supply continuity and expand access across urban and suburban consumption clusters.

Europe Fish Fermentation Market Trends

Europe demonstrates structured growth in fermented seafood through strict regulatory enforcement and advanced traceability frameworks. Standards defined by the European Food Safety Authority and the European Commission require microbial validation, origin labeling, and controlled processing environments. These measures strengthen product credibility and support premium pricing across retail chains. Import partnerships with Southeast Asian exporters ensure a consistent supply, while specialized distributors focus on high-value segments within urban consumption centers.

Demand expansion is shaped by increasing preference for artisanal and functional food products within metropolitan populations. Premium retailers integrate fermented fish items into curated assortments aligned with clean-label positioning. Companies such as Carrefour and Tesco expand offerings through private labels and imported brands. Foodservice operators incorporate fermented ingredients into fusion cuisine menus, strengthening visibility and supporting steady adoption across diverse consumer groups.

Asia Pacific Fish Fermentation Market Trends

Asia Pacific is expected to lead with an estimated 48% of the fish fermentation market share in 2026, supported by vertically integrated seafood ecosystems and strong institutional backing for fisheries modernization. Government programs in China and India strengthen aquaculture output and processing capacity, ensuring a stable raw material supply. In Japan and South Korea, advanced food processing systems and premium branding improve value capture. Leading companies such as Kikkoman Corporation and Masan Consumer scale production through standardized fermentation and export-focused strategies.

Industrial clustering across Southeast Asia creates cost-efficient production hubs with strong export orientation. Countries such as Vietnam and Thailand implement quality regulations and export incentives that improve global competitiveness and product standardization. Regulatory frameworks such as Vietnam’s national quality standards mandate microbial and chemical controls, strengthening international acceptance. Major producers, including Thai Fishsauce Factory and Red Boat Fish Sauce, leverage branding and traceability to access premium markets. High seafood availability and established consumption patterns sustain continuous production cycles and great domestic demand.

Competitive Landscape

The global fish fermentation market reflects a fragmented competitive structure, characterized by the coexistence of artisanal producers and organized food processing firms. Large companies such as Thai Union Group, Masan Group, and Nissui Corporation maintain moderate shares through scale efficiencies and export networks. Local producers sustain dominance in domestic markets through traditional methods, cost advantages, and strong consumer trust linked to heritage production practices and localized flavor profiles.

Mid-sized innovators, including Halcyon Proteins and Ocean’s Halo, focus on differentiated offerings and niche positioning. Competitive intensity is shaped by quality standardization, clean-label positioning, and packaging innovation. Distribution strength across retail and foodservice channels influences market reach and revenue stability. Companies invest in traceability, branding, and process control to improve consistency, strengthen consumer confidence, and support expansion into premium and international segments.

Key Industry Developments:

- In April 2026, DSM-Firmenich launched Veramaris® O3 Max Pure, a microalgae-based omega-3 ingredient produced through controlled fermentation, offering a sustainable alternative to fish oil and highlighting innovation pathways influencing the Fish Fermentation sector toward scalable, traceable, and consistent nutrient production.

- In February 2026, Mara Renewables advanced fish-free omega-3 production using precision fermentation of microalgae, scaling a reliable and sustainable nutrient supply that reduces dependence on wild fisheries and highlights innovation trends shaping the Fish Fermentation sector toward controlled, high-efficiency production systems.

Companies Covered in Fish Fermentation Market

- LactoSpore

- Danisco A/S

- Advanced Biotechnologies Inc.

- Kerry Group plc.

- Associated British Foods plc

- FMC Corporation

- Omega Protein Corporation

- TripleNine Group A/S

- Corpesca S.A.

- TASA

- Colpex International

Frequently Asked Questions

Various traditional methods include salt fermentation (e.g., fish sauce), acid fermentation (e.g., pickled herring), and fermentation with beneficial microorganisms (e.g., kimchi).

Fermentation promotes the breakdown of proteins and fats, enhancing digestibility and creating bioactive compounds while also inhibiting the growth of harmful bacteria, extending shelf-life.

Factors such as increasing consumer interest in fermented foods, demand for natural food preservation methods, and the growing popularity of ethnic cuisines drive market growth.

Compliance with food safety standards, such as Hazard Analysis and Critical Control Points (HACCP) and Good Manufacturing Practices (GMP), is crucial to ensure product safety and quality.

Trends include the development of novel flavor profiles, fermentation techniques using probiotic cultures, and the incorporation of sustainable sourcing practices in the production process.