ID: PMRREP34890| 180 Pages | 4 Nov 2024 | Format: PDF, Excel, PPT* | IT and Telecommunication

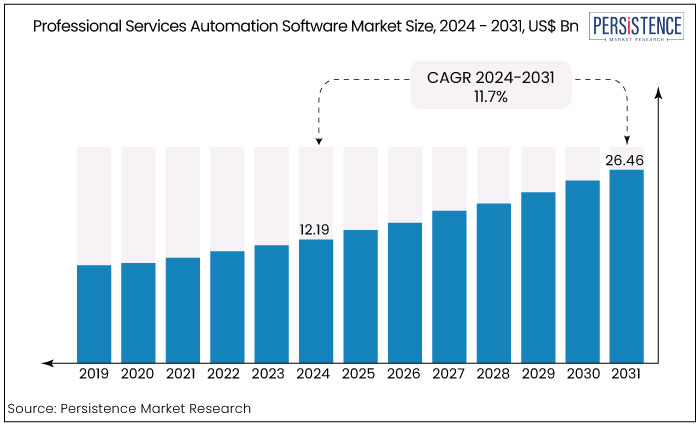

The professional services automation software market is estimated to increase from US$12.19 Bn in 2024 to US$26.46 Bn by 2031. The market is projected to record a CAGR of 11.7 % during the forecast period from 2024 to 2031.

The professional services automation (PSA) software market is expanding at a steady growth rate as organizations seek to improve operational efficiency, optimize resource utilization, and enhance project management capabilities.

PSA software is widely used in the IT & consulting services sector, which accounts for over 35% of the market share. Marketing & advertising sector holds around 15% of the PSA software market, as agencies manage large numbers of projects with distributed teams. Further, the legal and accounting firms contribute about 20 to 22% of the total market, leveraging PSA software for time and billing management.

Key Highlights of the Markets

|

Market Attributes |

Key Insights |

|

Professional Services Automation Software Market Size (2024E) |

US$ 12.19 Bn |

|

Projected Market Value (2031F) |

US$ 26.46 Bn |

|

Global Market Growth Rate (CAGR 2024 to 2031) |

11.7% |

|

Historical Market Growth Rate (CAGR 2019 to 2023) |

11% |

|

Region |

Market Share by 2024 |

|

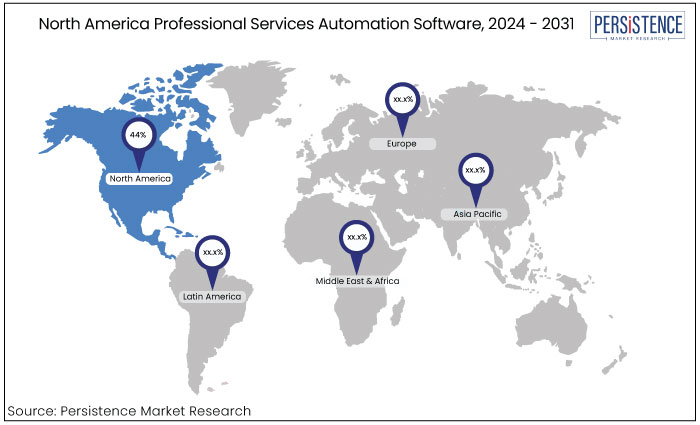

North America |

44% |

North America accumulated the largest market share and to account for 44% market share by 2024. The incorporation of modern technologies such as Artificial Intelligence (AI) and Machine Learning (ML), along with the launch of new solutions by market participants is generating favorable momentum for PSA solutions in North America.

The presence of established market participants, including Appirio, Inc., Salesforce, Inc., Oracle Corporation, Upland Software, and NetSuite OpenAir, Inc., propels market expansion in the region. Leading market participants are introducing new items to enhance profitability and expand their consumer base in this promising region.

|

Category |

Market Share by 2024 |

|

Application - Technology Companies |

54% |

Based on application, the market is sub segmented into consulting firms, marketing & communication firms, technology companies, architecture & construction firms, research firms, and accounting firms, Technology companies, especially those in the IT and software development sectors, form one of the largest segments using PSA software. These organizations have complex project management needs involving multiple teams, intricate timelines, and high resource allocation demands.

Technology companies often manage large-scale, long-term projects that require detailed tracking of progress, budgets, and timelines. PSA software, a crucial tool helps them streamline processes and improve project delivery providing a sense of security in their project management.

Many tech firms have distributed teams working across the globe. PSA tools facilitate seamless collaboration, resource management, and communication among remote workers. PSA software helps these companies reduce project overruns and ensure that billing is accurate thus improving their profitability and operational efficiency.

|

Category |

Market Share in 2024 |

|

Deployment - On-Premise |

54% |

In terms of deployment, the market is segmented into cloud and on-premise. Among these, on-premise deployment segment dominates the market. On-premise PSA systems provide strong data protection and privacy, exhibiting less susceptibility to digital threats and propelling industry growth. On-premise PSA solutions may operate and ensure secure data access even during internet connectivity disruptions, owing to their local data storage system.

Market participants engage in multiple shows to promote their on-premise PSA solutions and enhance their brand identification. For instance, in October 2021, Plainview, Inc., a provider of work and portfolio management solutions presented its latest on-premise professional services automation software at Technology & Services World (TSW) 2021 in Las Vegas, Nevada, organized by the Technology & Services Industry Association (TSIA).

Professional services automation (PSA) is an automated software solution that assists professionals, such as IT and telecom consultants, lawyers, auditors, and others. PSA software includes essential tasks such as project and resource management, automated time and invoicing, invoice management, expenditure management, and resource allocation.

Automated software provides advantages, including increased project efficiency, higher customer satisfaction, decreased financial expenditure, and enhanced forecasting capacity.

The rising demand for automation services and the decrease in overall costs to improve operational productivity and income among professional service organizations are primary factors anticipated to propel the growth of the PSA software market during the forecast period.

The rising demand for sophisticated mobility services among consultants and the expanding necessity for scalable and adaptable professional services is anticipated to promote market expansion.

The professional services automation (PSA) software market has experienced robust growth, driven by increasing demand for efficient project management, resource optimization, and billing solutions across professional service industries.

The professional services automation software market expanded steadily during the period from 2019 to 2023 exhibiting a CAGR of 11%. This market growth fueled by the rising adoption of cloud-based PSA solutions, which provided flexibility and scalability to firms in the IT, consulting, and professional services sectors.

The shift toward digital transformation across industries increased the need for centralized management of resources and projects. North America held the largest market share, driven by widespread adoption in technology and consulting firms.

The PSA software market is expected to accelerate with a projected CAGR of 11.7% during the period from 2024 to 2031. The primary growth drivers include the increasing integration of AI and automation for predictive analytics, huge focus on remote work management tools, and the expansion of SME adoption of PSA software.

Cloud-based PSA solutions will continue to dominate, with notable growth in Asia Pacific region, driven by expanding IT sectors in India and China. Emerging trends like the use of AI for resource optimization and demand for real-time analytics will further propel market expansion.

Increasing Demand for Efficiency and Resource Optimization

One of the primary drivers for the professional services automation software market growth is the growing need for businesses to enhance operational efficiency and optimize resource utilization. As organizations, particularly in professional services like IT consulting, marketing, and legal services, handle multiple projects simultaneously, the complexity of resource allocation, time management, and project tracking increases.

PSA software is a game-changer providing an integrated platform that not only streamlines processes but also automates routine tasks such as time tracking, expense management, and resource allocation. By doing so, it reduces manual errors and administrative overhead, freeing up valuable time for high-level strategic activities.

PSA tools enable businesses to use their workforce better by ensuring that the right resources are assigned to the suitable projects, maximizing productivity. As companies seek to improve profitability by reducing project overruns and ensuring accurate billing, the demand for PSA solutions is expected to continue growing, especially among organizations.

Adoption of Cloud-Based Solutions Remains a Key Driver

The shift toward cloud-based PSA solutions is another significant driver for the market. Cloud technology offers numerous advantages over traditional on-premise systems including scalability, flexibility, and lower initial costs.

Businesses, particularly small and medium-sized enterprises (SMEs) are increasingly adopting cloud-based PSA tools due to their ability to scale as business needs grow and their ease of implementation.

Unlike on-premise solutions, which require significant upfront investment in hardware and infrastructure, cloud-based PSA software operates on a subscription model making it affordable and accessible to a wide range of organizations.

Cloud solutions provide real-time access to project and resource data from anywhere, which is essential for managing distributed teams and remote work environments. This capability has become even more critical with the rise of hybrid and remote work models post-pandemic.

As more organizations embrace digital transformation and seek greater operational agility, the demand for cloud-based PSA solutions will continue to expand, driving overall market growth.

High Implementation and Training Costs

One key restraint for the professional services automation software market is the high cost of implementation and training, which can deter small firms and new adopters. PSA software often requires substantial investment for licensing and system customization, integration with existing IT infrastructure, and deployment.

Training employees to use these advanced platforms can also incur further costs particularly for firms without dedicated IT support teams. For small and medium-sized enterprises (SMEs), these financial and resource constraints can be significant barriers to adoption.

The learning curve associated with PSA software is often steep, requiring time and commitment for employees to understand and effectively utilize its features thoroughly. This leads some businesses to delay or forego PSA adoptions, which can limit market growth, especially in the SME segment.

Growing Demand for Remote and Hybrid Work Management Capabilities

The rise of remote and hybrid work models presents a transformative opportunity for PSA software vendors to provide solutions tailored to distributed teams. With more companies adopting flexible work arrangements, the need for efficient collaboration and real-time project tracking across dispersed teams has become essential.

PSA software can enable seamless remote work management by offering cloud-based access to project schedules, task tracking, and resource allocation tools that team members can access from anywhere.

Enhanced features like real-time updates, collaboration tools, and centralized dashboards improve visibility and communication for teams working across various time zones. Such capability not only supports current remote work trends but also positions PSA software as a critical tool for future workforce models.

Vendors that innovate to address these unique needs for remote and hybrid teams can gain a competitive edge as firms increasingly prioritize agility and remote work flexibility.

The professional services automation (PSA) software market is highly competitive with key players continuously innovating to meet the evolving needs of service-based organizations. Leading vendors include Oracle NetSuite, FinancialForce, Mavenlink, Kimble Applications, Wrike, and Microsoft Dynamics 365. These companies dominate through comprehensive PSA solutions that offer cloud-based access, AI-driven automation, and integration with popular third-party tools like Slack and Microsoft Teams.

Oracle NetSuite and FinancialForce have strong positions in the enterprise market, while Mavenlink and Kimble target mid-sized organizations. Emerging players like BigTime and Replicon cater to niche segments, especially SMEs. The focus on AI, automation, and hybrid work capabilities has intensified competition driving product differentiation and consolidation in the market.

Recent Industry Developments in the Professional Services Automation Software Market

The market is estimated to be valued at US$26.46 Bn by 2031

The market is projected to exhibit a CAGR of 11.7% over the forecast period.

Some of the leading players in the market are Microsoft Corporation, Autotask Corporation, and BMC Software, Inc.

North America region dominates the market.

On-premise deployment type leads the market with major market share.

|

Attributes |

Details |

|

Forecast Period |

2024 to 2031 |

|

Historical Data Available for |

2019 to 2023 |

|

Market Analysis |

US$ Billion for Value |

|

Key Regions Covered |

|

|

Key Market Segments Covered |

|

|

Key Companies Profiled in the Report |

|

|

Report Coverage |

|

|

Customization & Pricing |

Available upon request |

By Application

By Deployment

By Region

Delivery Timelines

For more information on this report and its delivery timelines please get in touch with our sales team.

About Author