- Power Generation, Transmission, & Distribution

- Pink Hydrogen Market

Pink Hydrogen Market Size, Share, and Growth Forecast, 2026 - 2033

Pink Hydrogen Market by Production Process (Electrolysis, Thermochemical Water Splitting, Others), End-user Industry (Energy Sector, Transport Sector, Other), Form & Distribution, and Regional Analysis for 2026 - 2033

Pink Hydrogen Market Size and Trends Analysis

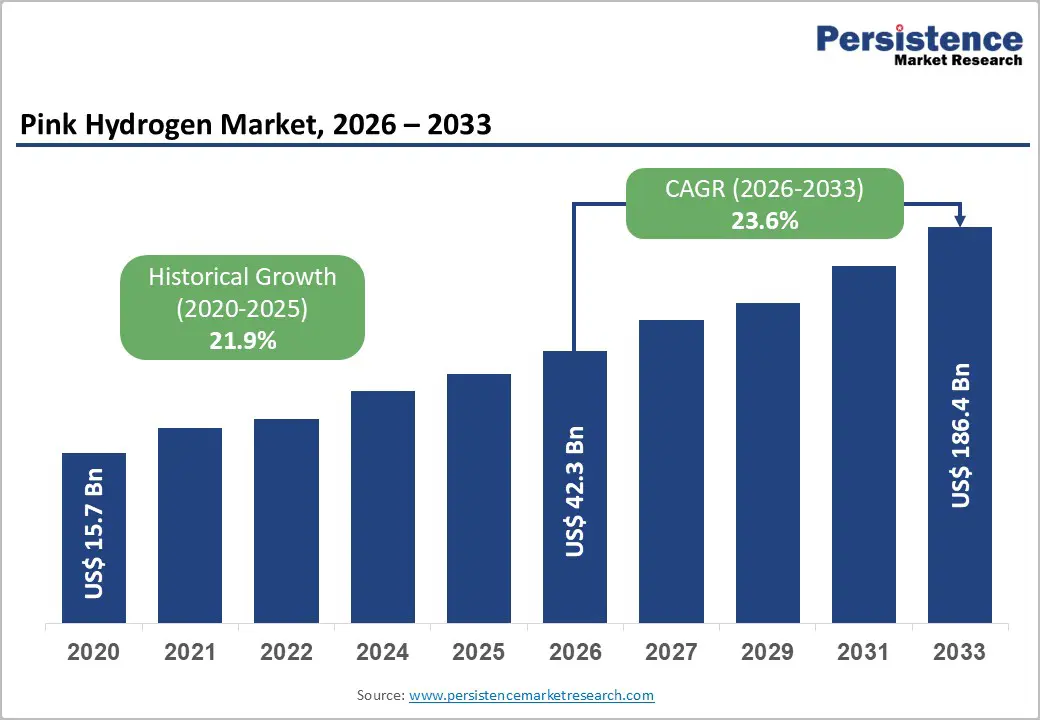

The global pink hydrogen market size is likely to be valued at US$42.3 billion in 2026 and is expected to reach US$186.4 billion by 2033, growing at a CAGR of 23.6% between 2026 and 2033, driven by supportive regulatory frameworks, efforts to optimize existing nuclear fleets, and increasing industrial demand across energy storage, mobility, and other hard-to-abate sectors.

Despite currently limited production volumes, the market’s expansion will be shaped by ongoing infrastructure development, the establishment of certification standards, and long-term offtake agreements that facilitate scalable deployment. Although still a niche segment, pink hydrogen plays a strategically important role within the broader hydrogen economy, supported by nuclear power’s ability to deliver continuous, low-carbon electricity along with high-temperature heat.

Key Industry Highlights:

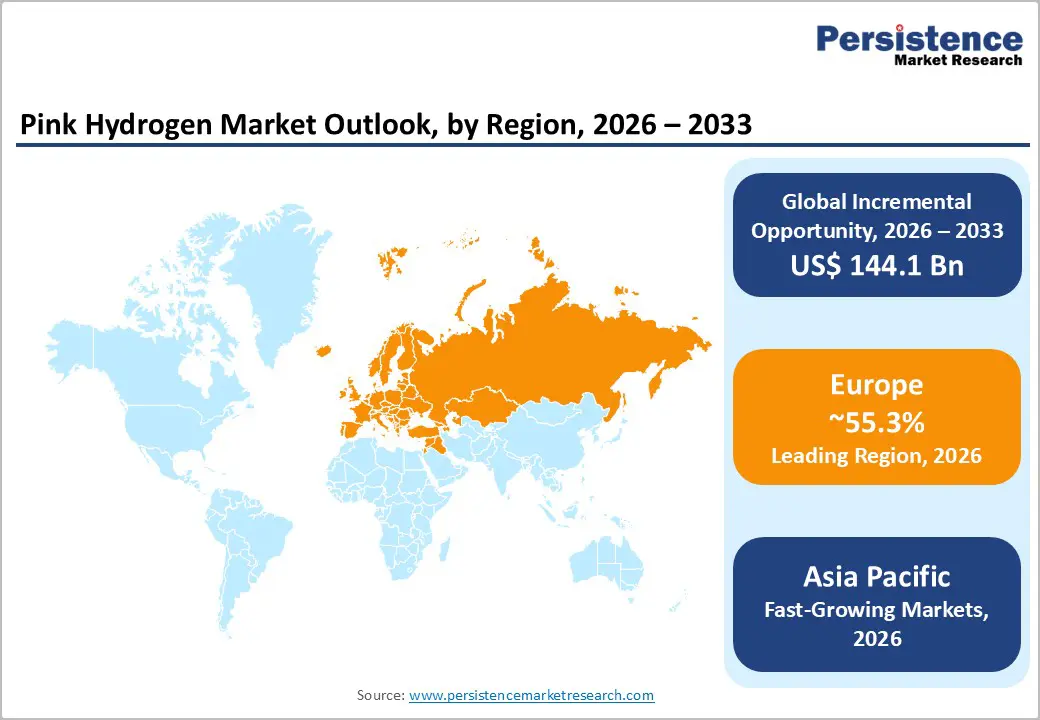

- Leading Region: Europe is projected to account for 55.3% of the market share, supported by strong regulatory frameworks, nuclear capacity, and large-scale investments in hydrogen.

- Fastest-growing Region: Asia Pacific is expected to be the fastest-growing region, driven by expanding nuclear infrastructure and hydrogen initiatives, with countries such as China, Japan, and India accelerating adoption at a high growth pace.

- Investment Plans: The market is seeing significant investments exceeding US$1 billion in large-scale electrolyzer and nuclear-integrated hydrogen projects, particularly in Europe and North America, with a focus on industrial clusters, hydrogen hubs, and infrastructure development.

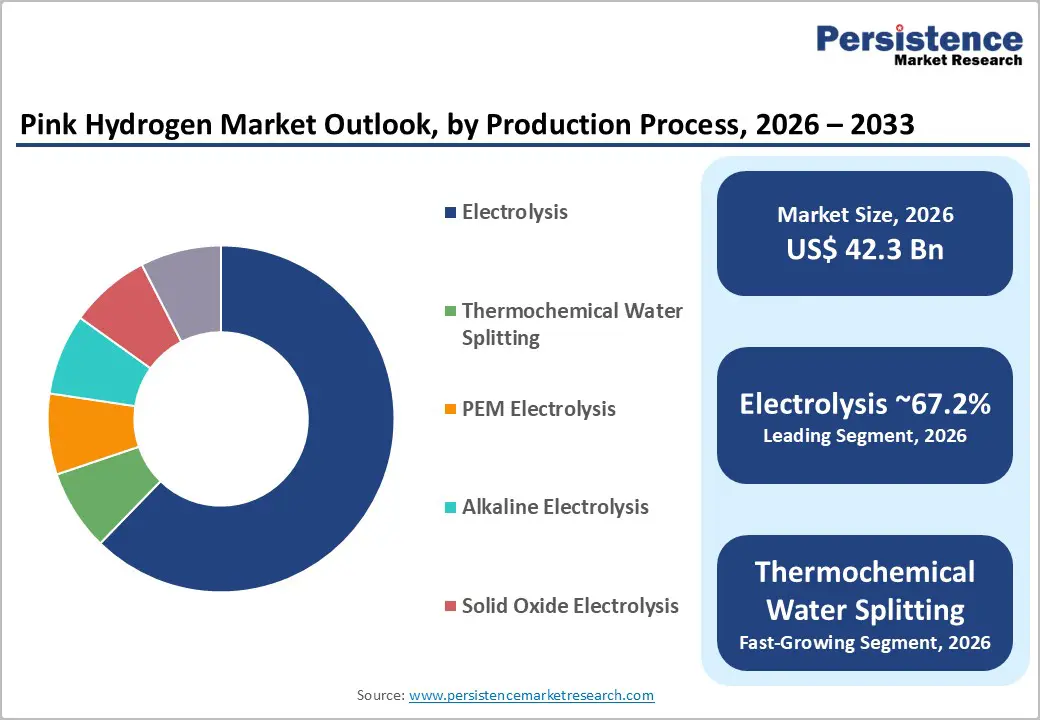

- Dominant Production Process: Electrolysis leads the production process segment, holding an anticipated 67.2% market share, due to its commercial maturity, scalability, and compatibility with nuclear power for continuous hydrogen production.

- Leading End-user: The energy sector is the largest end-user segment, accounting for an anticipated 43.9% market share, driven by increasing demand for energy storage, grid balancing, and low-carbon power generation.

| Key Insights | Details |

|---|---|

| Pink Hydrogen Market Size (2026E) | US$42.3 Bn |

| Market Value Forecast (2033F) | US$186.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 23.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 21.9% |

DRO Analysis

Driver Analysis - Policy Support Is Transforming Low-Carbon Hydrogen into a Bankable Asset Class

Governments across major economies are actively establishing regulatory frameworks, funding mechanisms, and incentive structures to accelerate hydrogen deployment. In Europe, the hydrogen and gas decarbonization framework has introduced dedicated rules for infrastructure, certification, and cross-border trade, while auction-based funding mechanisms are supporting early project development. In the U.S., clean hydrogen tax incentives and regulatory clarity have expanded the eligibility of nuclear-powered hydrogen within low-carbon classifications. These policy interventions reduce investment uncertainty and improve project bankability, enabling developers to secure financing and long-term contracts. As a result, pink hydrogen projects are increasingly integrated into national decarbonization strategies, particularly in regions with established nuclear capacity.

Nuclear Power Provides a Stable, High-Utilization Energy Source for Hydrogen Production

Pink hydrogen benefits from nuclear energy’s ability to deliver baseload, dispatchable, and low-carbon electricity, which is critical for efficient hydrogen production. Unlike intermittent renewables, nuclear power enables high utilization rates for electrolyzers and thermal systems, improving asset productivity and cost-efficiency. Advanced nuclear technologies, including small modular reactors (SMRs) and microreactors, further enhance this advantage by enabling flexible deployment and integration with hydrogen production systems. High-temperature reactors can also support thermochemical water splitting, increasing efficiency compared to conventional electrolysis. This compatibility between nuclear energy and hydrogen production strengthens the economic case for pink hydrogen, particularly for utilities seeking to diversify revenue streams and optimize existing nuclear assets.

Industrial Demand Is Expanding Across Energy, Transport, and Heavy Industry

Hydrogen demand is shifting from pilot applications to industrial-scale deployment, particularly in sectors requiring decarbonized fuels and feedstocks. In the energy sector, hydrogen is increasingly used for grid balancing, long-duration storage, and energy transport. In transportation, hydrogen fuel cells are gaining traction in heavy-duty vehicles, buses, and port logistics, where battery solutions face limitations in energy density and refueling time. Industrial applications, including refineries, chemicals, and steel production, are also emerging as key demand centers. The growing visibility of long-term offtake agreements signals a transition toward stable demand, which is essential for scaling pink hydrogen infrastructure and attracting institutional investment.

Restraint Analysis - High Capital Intensity and Cost Competitiveness Challenges

Pink hydrogen projects require significant upfront investment across nuclear power generation, hydrogen production systems, storage, and distribution infrastructure. These capital requirements create long payback periods and financing challenges, particularly in markets where hydrogen demand is still developing. Moreover, pink hydrogen must compete with conventional hydrogen produced from fossil fuels, which remains more cost-effective in many regions. The limited share of low-emissions hydrogen in global supply highlights the gap between announced projects and operational capacity. Until economies of scale and technological advancements reduce costs, financial viability will remain a key constraint for widespread adoption.

Regulatory Complexity and Public Perception of Nuclear Energy

Although regulatory frameworks are evolving, the lack of harmonized standards and certification mechanisms continues to create uncertainty for cross-border hydrogen trade. Differences in policy implementation across regions can delay project approvals and increase compliance costs. Public perception of nuclear energy also presents a structural challenge. In several countries, political and social resistance to nuclear power can limit the deployment of pink hydrogen projects, even when technically feasible. These regulatory and societal factors can slow market expansion, particularly in regions without strong nuclear policy support.

Opportunity Analysis - Advanced Production Technologies Will Enhance Efficiency and Scalability

Emerging technologies such as high-temperature electrolysis and thermochemical water splitting offer significant efficiency improvements over conventional methods. These processes utilize nuclear-generated heat, reducing electricity consumption and improving overall system performance. As advanced reactors and SMRs become commercially viable, they will enable integrated hydrogen production systems that combine electricity, heat, and hydrogen outputs. This technological convergence represents a major opportunity to improve cost competitiveness and accelerate commercialization, particularly in industrial clusters and energy hubs.

Distribution and Infrastructure Models are Enabling Market Expansion

The development of hydrogen transport and storage infrastructure is creating new opportunities for market growth. Pipeline networks, liquefaction facilities, and compressed hydrogen systems are enabling producers to reach a broader customer base beyond localized production sites. Flexible delivery models, including hub-and-spoke distribution systems, are particularly relevant for industrial zones, ports, and logistics corridors. This shift toward infrastructure-driven growth enhances market accessibility and supports large-scale deployment, making hydrogen more viable as a traded energy commodity.

Asia Pacific Presents Strong Growth Potential Driven By Nuclear Expansion

Asia Pacific is emerging as a key growth region due to increasing nuclear capacity, industrial demand, and government investment in hydrogen technologies. Countries such as Japan, India, and China are integrating hydrogen into their long-term energy strategies, with a focus on energy security and decarbonization. India’s investment in SMR development and hydrogen-focused nuclear technologies, along with China’s rapid nuclear capacity expansion, highlight the region’s commitment to scaling low-carbon hydrogen. The combination of manufacturing capabilities, policy support, and energy demand positions Asia Pacific as a major future market for pink hydrogen deployment.

Category-wise Analysis

Production Process Insights

The electrolysis segment is anticipated to lead, due to its scalability and commercial maturity, accounting for an anticipated 67.2% market share in 2026. Electrolysis dominates the production landscape as it is the most widely deployed and technologically established method for hydrogen generation. It is highly compatible with nuclear power, allowing continuous hydrogen production through low-temperature electrolysis systems such as alkaline and PEM technologies. These systems are already integrated into industrial operations and benefit from established supply chains and operational experience.

Real-world deployment examples include large-scale electrolyzer installations in Europe and North America, where nuclear and grid-connected electricity sources are used to produce low-carbon hydrogen for industrial clusters and refineries. Nuclear utilities are also exploring co-location of electrolyzers with existing reactors to utilize excess baseload capacity. This segment leads because it offers immediate scalability and lower technological risk, making it the preferred choice for early-stage pink hydrogen projects and near-term commercialization strategies.

Thermochemical water splitting is likely to be the fastest-growing segment, driven by efficiency gains. Thermochemical processes leverage high-temperature heat from advanced nuclear reactors, enabling more efficient hydrogen production compared to conventional electrolysis. Operating at elevated temperatures significantly reduces electricity requirements, improving overall system economics. Emerging pilot projects involving high-temperature gas-cooled reactors (HTGRs) and small modular reactors (SMRs) are demonstrating the feasibility of integrating thermochemical cycles for hydrogen production.

These systems are particularly relevant in regions investing in next-generation nuclear technologies, such as Japan and India. As next-generation reactors and high-temperature systems gain traction, this segment is expected to expand rapidly. Its growth is driven by the potential to deliver higher efficiency and deeper integration with nuclear systems, positioning it as a key technology for long-term market development and cost optimization.

End-user Industry Insights

The energy sector is expected to lead due to its role in storage and power system optimization, accounting for an anticipated 43.9% market share in 2026. The energy sector represents the largest end-user segment, as hydrogen is increasingly used for energy storage, grid balancing, and power generation. Pink hydrogen enables nuclear plants to convert excess electricity into a storable energy carrier, enhancing grid flexibility and reliability, particularly in systems with high renewable penetration.

Practical examples include hydrogen-based energy storage projects in Europe and North America, where utilities are integrating hydrogen production with nuclear and renewable assets to stabilize power supply and manage peak demand. Hydrogen is also being explored for reconversion into electricity via fuel cells or turbines during periods of high demand. This segment leads because it aligns directly with energy transition goals, allowing utilities to optimize asset utilization, improve grid resilience, and support renewable integration.

The transport sector is likely to be the fastest-growing due to fuel cell adoption. Transportation is emerging as a high-growth segment, particularly in heavy-duty vehicles, public transport, rail, and port logistics applications. Hydrogen fuel cells offer advantages in energy density, refueling time, and operational range compared to battery-electric solutions, especially for long-haul and high-utilization fleets.

Examples include hydrogen-powered buses in Europe, fuel cell truck deployments in North America, and pilot hydrogen rail projects in Asia. Increasing investment in hydrogen refueling infrastructure and government-backed mobility programs is accelerating adoption across these segments. Growth is driven by rising demand for zero-emission transport solutions and expanding infrastructure, positioning the transport sector as a key driver of incremental hydrogen demand over the forecast period.

Regional Insights

North America Pink Hydrogen Market Trends - Nuclear-Backed Hydrogen Hubs & Policy-Driven Commercialization

North America represents a high-potential market driven by strong policy support, nuclear infrastructure, and innovation ecosystems. The U.S. leads the region, supported by regulatory frameworks that recognize nuclear energy as a viable source for clean hydrogen production. Federal incentives, including clean hydrogen tax credits and funding for hydrogen hubs, have improved project economics and accelerated investment in nuclear-linked hydrogen systems.

A notable example is Constellation Energy, which has actively explored integrating hydrogen production with its nuclear fleet, demonstrating how existing reactors can be leveraged for clean hydrogen generation. Similarly, the U.S. Department of Energy has funded multiple hydrogen hub initiatives that include nuclear-powered hydrogen pathways, strengthening commercialization prospects. Canada complements this growth with a strong hydrogen strategy and established nuclear capabilities. Organizations such as Natural Resources Canada are promoting hydrogen production using off-peak nuclear electricity, particularly in Ontario’s nuclear-heavy grid.

Key growth drivers include policy incentives, advanced nuclear development (including SMRs), and rising industrial demand across manufacturing and energy sectors. Investment is increasingly directed toward hydrogen hubs, storage infrastructure, and cross-border supply chains, particularly between the U.S. and Canada. The region’s strong financing environment, regulatory clarity, and technological leadership position North America as a key player in pink hydrogen commercialization, especially in integrating nuclear energy with scalable hydrogen production.

Europe Pink Hydrogen Market Trends - Regulatory Leadership & Large-Scale Integrated Hydrogen Ecosystems

Europe is expected to lead, accounting for 55.3% of the market share in 2026, driven by a comprehensive regulatory framework and strong policy alignment. The region has established clear rules for hydrogen infrastructure, certification, and market integration, enabling large-scale and cross-border project development. Countries such as Germany, France, the U.K., and Spain are actively investing in hydrogen technologies, supported by funding mechanisms and national strategies. France plays a pivotal role due to its nuclear-dominated energy mix, which provides a stable foundation for pink hydrogen production.

For example, EDF is exploring hydrogen production linked to its nuclear assets, reinforcing the integration of nuclear and hydrogen value chains. Industrial gas leaders such as Air Liquide and energy majors like TotalEnergies have launched large-scale electrolyzer projects in Europe, including developments exceeding 200 MW capacity. These projects are designed to supply refineries, industrial clusters, and mobility applications, demonstrating how hydrogen ecosystems are being built around long-term offtake agreements and infrastructure networks.

Key drivers include policy harmonization, funding programs such as hydrogen auctions, and aggressive industrial decarbonization targets. Investment trends highlight the expansion of cross-border hydrogen pipelines, port-based hydrogen hubs, and integrated energy systems. Europe’s structured regulatory environment, strong institutional backing, and early-mover advantage make it the most mature and commercially advanced market for pink hydrogen deployment.

Asia Pacific Pink Hydrogen Market Trends - Nuclear Expansion & Industrial-Scale Hydrogen Growth Engine

Asia Pacific is likely to be the fastest-growing region, driven by rapid industrialization, rising energy demand, and expanding nuclear capacity. Countries such as China, Japan, and India are leading regional growth through strategic investments in hydrogen and nuclear technologies. China’s large-scale nuclear expansion supports the development of hydrogen production at scale, with state-owned enterprises increasingly exploring nuclear-hydrogen integration. Japan, through companies such as IHI Corporation, is actively investing in hydrogen value chains, including production, storage, and transport, as part of its long-term energy security strategy.

India is also emerging as a key player, with initiatives supported by the Department of Atomic Energy focusing on SMR development and high-temperature reactors designed for hydrogen production. Additionally, JGC Holdings is involved in hydrogen infrastructure and project development across Asia, supporting regional deployment. Key drivers include strong manufacturing capabilities, government investment programs, and increasing demand for clean industrial energy solutions.

The region is witnessing rapid growth in hydrogen infrastructure, industrial applications, and export-oriented energy projects. Asia Pacific’s combination of scale, policy momentum, and industrial demand positions it as a critical growth engine, with the potential to become a major production and consumption hub for pink hydrogen over the forecast period.

Competitive Landscape

The global pink hydrogen market is fragmented, with no single player dominating the global market share. The ecosystem includes nuclear utilities, electrolyzer manufacturers, industrial gas companies, and technology providers, each contributing to different stages of the value chain. Competition is driven by technological capabilities, project execution, and strategic partnerships, rather than market concentration. Leading players are primarily based in Europe and North America, but Asia Pacific companies are rapidly gaining influence.

Key strategies include technology innovation, strategic partnerships, and market expansion. Companies are focusing on improving efficiency, reducing costs, and securing long-term offtake agreements. Collaboration across the value chain is emerging as a critical success factor, enabling faster deployment and reduced project risk.

Key Industry Developments:

- In February 2025, Air Liquide and TotalEnergies announced a joint investment of over €1 billion to develop two large-scale electrolyzer projects (200 MW and 250 MW) in the Netherlands, aimed at supplying low-carbon hydrogen to industrial sectors and significantly reducing emissions from refinery operations.

- In October 2025, Plug Power delivered the first of ten 10 MW GenEco electrolyzers to a refinery project, part of a broader 100 MW deployment expected to replace up to 20% of gray hydrogen and reduce approximately 110,000 tons of CO2 annually, reinforcing large-scale industrial hydrogen adoption.

Companies Covered in Pink Hydrogen Market

- EDF

- Constellation Energy

- Air Liquide

- TotalEnergies

- Siemens Energy

- Nel ASA

- Framatome

- NuScale Power

- Rolls-Royce SMR

- Next Hydrogen

- IHI Corporation

- JGC Holdings

- Korea Electric Power Corporation

- China National Nuclear Corporation

- Rosatom

- Westinghouse Electric Company

Frequently Asked Questions

The global pink hydrogen market is estimated to be valued at US$42.3 billion in 2026.

The pink hydrogen market is projected to reach US$186.4 billion by 2033, reflecting strong expansion driven by policy support and nuclear integration.

Key trends include the integration of nuclear power with hydrogen production, rising deployment of electrolyzer technologies, increasing investment in hydrogen infrastructure and hubs, and growing adoption in energy storage and heavy transport applications. The development of SMRs and high-temperature reactors is also shaping long-term market evolution.

Electrolysis is the leading production segment, accounting for an anticipated 67.2% market share in 2026, due to its scalability, commercial maturity, and compatibility with nuclear power.

The pink hydrogen market is expected to grow at a CAGR of 23.6% between 2026 and 2033.

Some of the major players include EDF, Air Liquide, Siemens Energy, NuScale Power, and Westinghouse Electric Company.