- Power Generation, Transmission, & Distribution

- District Heating Market

District Heating Market Size, Share, and Growth Forecast 2026 - 2033

District Heating Market by Heat Source (Combined Heat and Power (CHP), Biomass, Geothermal, Solar Thermal, Waste Heat Recovery, Fossil Fuels, Others), Plant Type (Centralized, Decentralized), Technology (1st Generation, 2nd Generation, 3rd Generation, 4th Generation), Application (Space Heating, Water Heating, Industrial Heating), End-user (Residential, Commercial, Industrial), and Regional Analysis, 2026 - 2033

District Heating Market Size and Trend Analysis

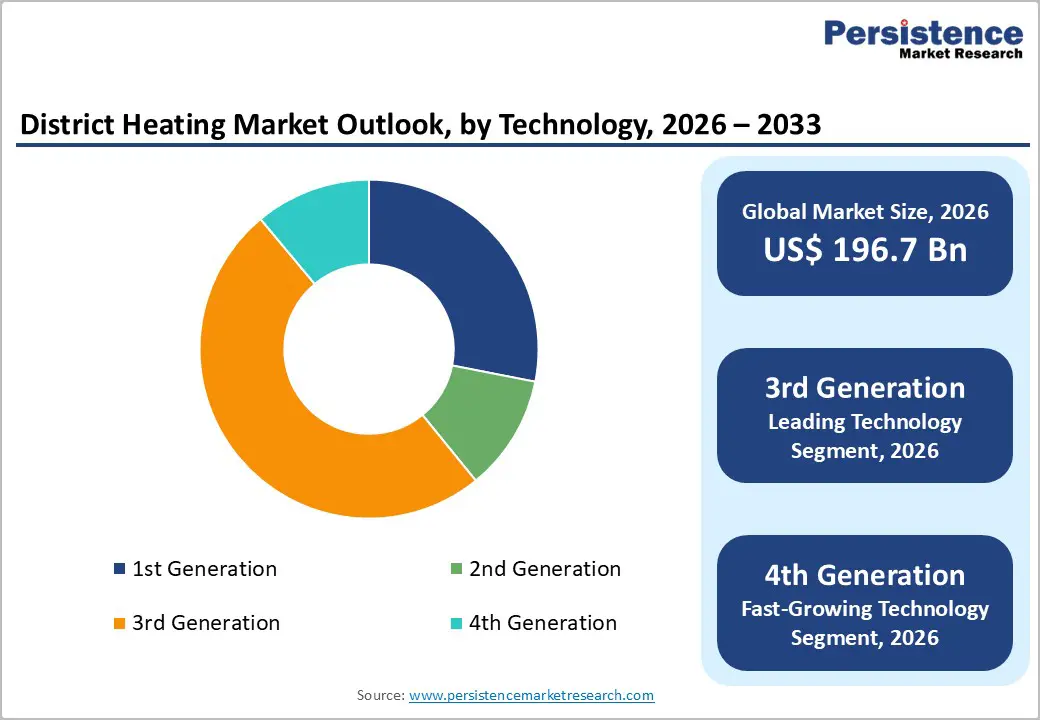

The global District Heating market size is expected to be valued at US$ 196.7 billion in 2026 and projected to reach US$ 232.2 billion by 2033, growing at a CAGR of 2.4% between 2026 and 2033.

The global market continues its steady expansion, underpinned by accelerating decarbonization mandates, rapid urbanization, and policy-driven investment in energy-efficient centralized heating infrastructure. The European Commission's Fit for 55 Package formally recognizes district heating as critical infrastructure for the EU energy transition, while the Revised Energy Efficiency Directive establishes a clear decarbonization pathway for heating networks to achieve CO2-neutrality by 2050. Simultaneously, technological advancements in 4th-generation low-temperature networks, waste heat recovery, and large-scale heat pumps are expanding the addressable market for district heating operators, making the technology increasingly viable across a broader range of climates, urban densities, and energy source configurations globally.

Key Industry Highlights:

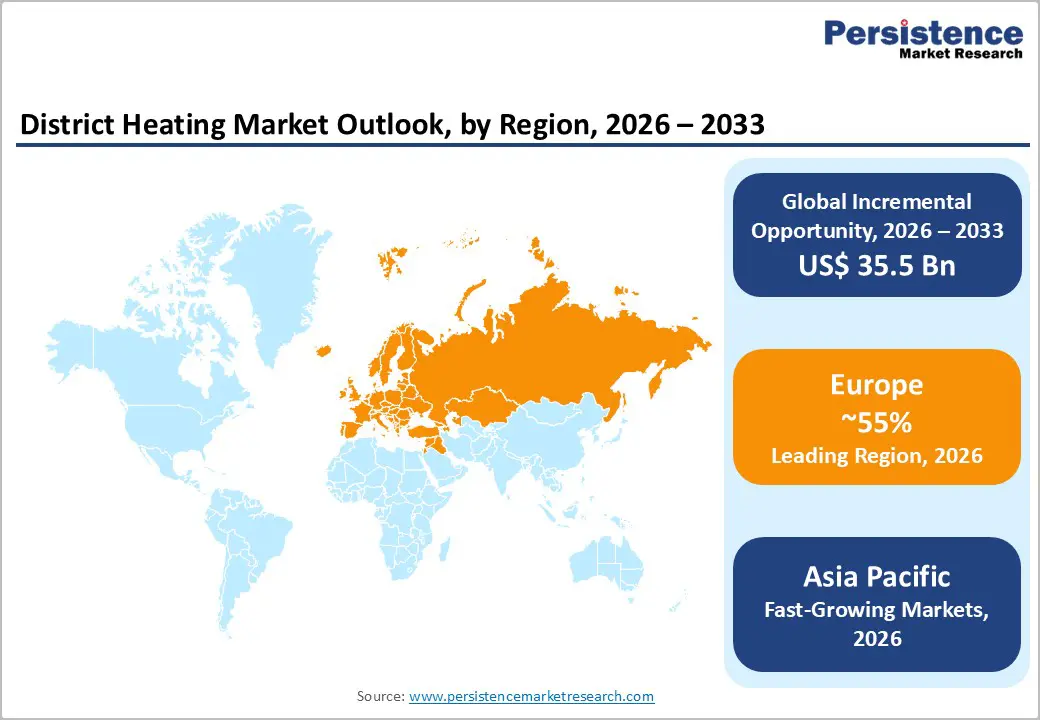

- Leading Region: Europe leads the global district heating market with approximately 55% share in 2025, underpinned by the EU's Fit for 55 Package, mature CHP and renewable heating infrastructure, and network decarbonization mandates requiring CO2-neutral heating networks by 2050 across all member states.

- Fastest Growing Region: Asia Pacific is the fastest-growing region in the district heating market, driven by China's mandatory centralized heating expansion under the NDRC, South Korea's KDHC serving over 1.6 million households, and India's Smart Cities Mission beginning to incorporate district energy into urban planning.

- Dominant Heat Source: Combined Heat and Power (CHP) is the dominant heat source segment with approximately 45% market share in 2025, led by its 80–85% overall energy efficiency advantage, strong policy support under the EU Energy Efficiency Directive, and proven scalability across both urban district heating and industrial cogeneration applications globally.

- Fastest Growing Technology: 4th Generation District Heating is the fastest-growing technology segment, operating at low supply temperatures of 50–70°C and enabling integration of solar thermal, heat pumps, and waste heat sources, with Copenhagen's HOFOR investing approximately US$ 418 million in heat pump capacity by 2033.

- Key Opportunity: Integrating data center and industrial waste heat into district heating networks represents a transformative market opportunity, validated by Fortum-Microsoft's Helsinki project, which covers 40% of district heating for 250,000 users, signaling a replicable model for low-carbon urban heating globally.

| Key Insights | Details |

|---|---|

|

District Heating Market Size (2026E) |

US$ 196.7 Billion |

|

Market Value Forecast (2033F) |

US$ 232.2 Billion |

|

Projected Growth CAGR (2026–2033) |

2.4% |

|

Historical Market Growth (2020–2025) |

2.1% |

Market Dynamics

Drivers - Accelerating Global Decarbonization Policies and Renewable Energy Integration Mandates

Binding decarbonization targets from global and regional regulatory bodies are the most powerful structural driver of the district heating market. The European Commission's Fit for 55 Package and the Revised Energy Efficiency Directive (EED) mandate that EU member states develop roadmaps for the decarbonization of heating networks, requiring the integration of renewable and waste heat sources. According to Eurostat, district heating systems supplied approximately 12% of Europe's total heating demand in 2022, with regulatory ambition to expand this share substantially by 2030. The Danish Energy Agency highlights that renewables now account for over 60% of district heating energy in Denmark, while the Swedish Energy Agency reports that renewables supply over 70% of Sweden's district heating. The EU's investment in renewable-based systems is projected to reach €30 billion by 2030, reinforcing a sustained procurement cycle for district heating expansion and modernization across the region.

Rapid Urbanization and Growing Demand for Energy-Efficient Centralized Heating

Escalating urbanization is expanding the addressable market for district heating systems worldwide. According to the United Nations, the global urban population is projected to reach 68% of the total world population by 2050, adding approximately 2.5 billion people to urban areas. This concentration of population and industry in dense urban environments creates ideal conditions for centralized district heating networks, which deliver efficiencies of up to 85% compared to individual building heating systems. In January 2024, the United Kingdom's government allocated GBP 288 million through its Green Heat Network Fund to accelerate heat network development. The UK Climate Change Committee estimates that approximately 18% of the UK's heat consumption could be supplied through heat networks by 2050. In China, ongoing urbanization is driving investment in heating infrastructure, with district heating coverage in northern Chinese cities continuing to expand as part of national energy security and air quality improvement programs.

Restraints - High Capital Investment Requirements and Long Payback Periods

The development of district heating infrastructure requires substantial upfront capital investment in pipelines, heat generation plants, and distribution network equipment, with payback periods often extending 20–40 years. The cost of laying new insulated pipe networks in urban environments can reach EUR 1–3 million per kilometer, depending on soil conditions and urban density. This high capital intensity limits market expansion to jurisdictions with strong public financing mechanisms or regulatory guarantees, effectively slowing growth in regions without government-backed financing frameworks.

Stranded Asset Risk from Fossil Fuel Dependency and Regulatory Transition Challenges

A significant proportion of existing district heating networks globally, particularly in Eastern Europe, Russia, and parts of Asia, are built around fossil fuel-fired heat plants, including coal-fired CHP and natural gas boilers. As decarbonization mandates tighten, these fossil fuel assets face an increasing risk of becoming stranded prior to the end of their operational lives. Transitioning existing networks to renewable or waste heat sources requires capital-intensive retrofitting. Uniper SE's October 2024 announcement of the divestiture of its district heating operations in Germany's Ruhr region reflects the strategic burden of managing legacy fossil-fuel heating assets under evolving EU regulatory requirements.

Opportunities - Waste Heat Recovery from Data Centers and Industrial Facilities

The integration of waste heat from data centers and industrial facilities into district heating networks represents one of the most commercially compelling growth opportunities in the market. In March 2024, Fortum Corporation and Microsoft launched the world's largest data center heat recovery project in Helsinki, Finland, enabling Microsoft's data center waste heat to supply approximately 40% of the district heating needs of 250,000 customers in a CO2-free manner, replacing existing coal and fossil fuel-based heat sources. In August 2024, A2A, in collaboration with DBA Group and Retelit, launched Italy's first project to recover heat from data centers for district heating in Milan. In February 2024, Uniper SE and Evonik Industries AG launched the TORTE (Technical Options for Thermal Energy Recovery) project in Gelsenkirchen, supplying approximately 1,000 homes by integrating industrial waste heat into district heating. The global data center industry is projected to consume over 200 TWh of electricity annually by 2030, generating enormous recoverable waste heat volumes that district heating operators can strategically convert into network supply.

4th Generation District Heating and Low-Temperature Networks Unlocking New Markets

The rapid development of 4th Generation District Heating (4GDH) systems is creating significant market expansion opportunities for network operators, technology suppliers, and engineering consultancies. Unlike legacy high-temperature systems, 4GDH operates at supply temperatures of 50–70°C, enabling the integration of low-grade heat sources, including solar thermal, heat pumps, geothermal, and industrial waste heat, that are incompatible with older network generations. Copenhagen's HOFOR utility is investing 3 billion Danish kroner (approximately US$ 418 million) to install 10 large heat pumps by 2033, electrifying its district heating network away from biomass and waste combustion. In March 2024, Ørsted agreed with VEKS and CTR to use surplus heat from the carbon capture process at Avedøre Power Station, which is set to capture 150,000 tonnes of CO2 annually from 2026, to supply district heating to households in the Greater Copenhagen area. These developments signal a systemic shift that will drive investment in 4GDH infrastructure globally through 2033.

Category-wise Analysis

Heat Source Insights

Combined Heat and Power (CHP) is the leading heat source segment, commanding approximately 45% of total market share in 2025. CHP's market leadership stems from its unmatched overall energy efficiency, which simultaneously generates electricity and usable heat from a single fuel source, achieving efficiencies of 80–85% compared to 35–45% for separate heat and power generation. The European Commission recognizes high-efficiency CHP as a key tool for meeting energy efficiency targets, and supports its adoption under the revised Energy Efficiency Directive (EED). In January 2025, E.ON and MM Neuss (Mayr-Melnhof Karton Group) activated Europe's first fully automated and market-driven CHP plant at the Neuss site in Germany using E.ON IQ Energy intelligent control. Solar Thermal is the fastest-growing heat source segment, growing at a CAGR of above 5.7%, driven by declining technology costs and improved seasonal thermal energy storage integration.

Plant Type Insights

Centralized plant type dominates the district heating market, representing approximately 70% of total market share in 2025. Centralized systems benefit from economies of scale in heat generation, lower per-unit fuel costs, easier integration of large-scale renewable heat sources, and a long history of infrastructure investment, particularly across Europe, Russia, and China, which collectively account for the vast majority of global district heating capacity. In Europe, centralized district heating networks boast a total installed capacity of approximately 300 GWth as of 2021, supplying approximately 500 TWh of heat annually across the surveyed European countries, according to Eurostat. The decentralized plant type is the fastest-growing segment, driven by the proliferation of small-scale and micro-CHP systems, urban heat pumps, and modular biomass units serving building clusters and new urban developments.

Technology Insights

3rd Generation technology leads the global market, accounting for approximately 50% of the total share in 2025. 3rd Generation systems, operating at supply temperatures of 80–130°C using pressurized hot water, represent the backbone of existing district heating infrastructure across Northern and Central Europe, Russia, and China. The majority of the world's active district heating networks were built under the 3rd Generation paradigm between the 1970s and early 2000s, and these networks continue to supply the bulk of connected heat demand. However, 4th Generation is the fastest-growing technology, operating at lower supply temperatures of 50–70°C and enabling the integration of renewable and low-grade waste heat sources, positioning it as the preferred framework for all new district heating network investments globally through 2033.

Application Analysis

Space Heating is the dominant application segment in the District Heating market, representing approximately 65% of the total market share in 2025. Space heating's leadership reflects the fundamental demand for building thermal comfort across cold-climate regions, which constitute the core markets for district heating globally. In Denmark, district heating accounts for approximately 60% of urban space heating needs, according to the Danish Energy Agency. In the Nordic countries, district heating is the primary space-heating solution for the majority of multi-family residential and commercial buildings. In China and Russia, space heating via district systems serves hundreds of millions of urban residents through state-mandated centralized heating infrastructure. Industrial Heating is the fastest-growing application segment, driven by decarbonization pressures on industrial operators seeking certified low-carbon heat supplies to meet process requirements.

End-user Insights

Residential is the leading end-user segment, accounting for approximately 55% of the total market share in 2025. The residential segment's dominance reflects the established role of district heating in providing affordable, reliable, and increasingly low-carbon space heating and hot water to apartment complexes, social housing estates, and individual residences across Europe and Asia. In Denmark, district heating connection rates in residential buildings exceed 65% in urban areas. In China, mandatory centralized heating provision for residential buildings in northern urban zones, mandated by the National Development and Reform Commission (NDRC), ensures sustained residential demand. Commercial is the fastest-growing end-user segment, driven by expanding smart city development, mixed-use urban projects, and hospitals, universities, and public institutions adopting district heating as part of their sustainability strategies.

Regional Insights

North America District Heating Market Trends and Insights

North America represents a growing and strategically important segment of the global District Heating market, with the United States and Canada increasingly recognizing centralized heat networks as a viable tool for urban decarbonization. The U.S. market includes established district heating systems in cities such as New York, Chicago, and Boston, operated by providers including Enwave Energy Corporation and NRG Energy Inc.

In January 2024, the U.S. Department of Energy (DOE) released the Industrial Decarbonization Roadmap, which specifically highlights waste heat recovery and district energy as priority pathways for reducing industrial thermal emissions, targeting 85% reduction in industrial carbon emissions by 2050.

Canada's Enwave Energy Corporation operates one of North America's most extensive deep-lake water-cooling and district-heating systems in Toronto, supplying over 100 connected buildings. The Inflation Reduction Act (IRA)'s clean energy investment tax credits are beginning to stimulate new district heating project development in the U.S., particularly for systems integrating geothermal and biomass heat sources. The integration of renewable energy sources, biomass, geothermal, and solar thermal, into district heating systems is gaining momentum, reducing carbon emissions and supporting sustainability commitments across both government-owned and private network operators in the region.

Europe District Heating Market Trends and Insights

Europe leads the global District Heating market with approximately 55% share in 2025, hosting the world's most mature and technologically advanced centralized heating networks. According to Eurostat, district heating supplies approximately 12% of Europe's total heating demand, with Denmark and Sweden exceeding 50% and 70% renewable heat penetration, respectively. The European Commission's Fit for 55 Package and Revised Energy Efficiency Directive are driving network modernization investments across Germany, France, the UK, and the Nordic countries.

In October 2024, Veolia announced the construction of a new district heating network in London, utilizing 75 GWh per year of low-carbon heat from the SELCHP Energy Recovery Facility to supply approximately 5,000 homes and public institutions.

Germany's Hamburg utility announced the installation of two large river heat pumps and supporting heat storage infrastructure in December 2024, as part of its coal-to-biomass conversion program. Denmark's parliament adopted regulation to support geothermal development in March 2024, exempting geothermal projects from existing price regulations, directly incentivizing new renewable heat capacity. In May 2025, ENGIE SA inaugurated a new renewable district heating network in Zamora, Spain, through DH Ecoenergías Zamora, marking a significant expansion of sustainable district heating infrastructure into Southern European markets that have historically been less penetrated by centralized heating systems.

Asia Pacific District Heating Market Trends and Insights

Asia Pacific is the fastest-growing region with the highest projected CAGR between 2026 and 2033, driven by China's enormous centralized heating infrastructure, India's emerging urban energy planning initiatives, and Japan and South Korea's growing adoption of low-carbon district energy. China remains the world's second-largest district heating market, with centralized heating mandatory in northern Chinese cities under NDRC regulations, serving hundreds of millions of urban residents. China's 14th Five-Year Plan (2021–2025) targets expansion of district heating coverage and integration of geothermal and waste heat sources to reduce coal dependency in heating, with new connections accelerating across Tier 2 and Tier 3 cities.

Japan's Shinryo Corporation is a leading domestic operator of district heating and cooling systems, with operations in major urban developments across Tokyo and Osaka. South Korea's Korea District Heating Corporation (KDHC) serves approximately 1.6 million households and continues to invest in CHP modernization and renewable heat integration. In September 2025, Helen, a major Finnish energy firm, revealed plans to collaborate with data center operators establishing facilities in Helsinki, enabling their connection to the city's modern district heating and cooling network, a model increasingly being studied and replicated by Asian urban planners.

Competitive Landscape

The global District Heating market demonstrates a moderately consolidated structure at the strategic level but remains highly fragmented at the operational level due to the localized ownership of heating networks by municipalities and regional utilities. Large energy and infrastructure companies participate alongside numerous local operators that manage city-level heating grids. Market participants typically secure long-term supply agreements with municipal authorities and utility partners, creating stable revenue streams and high entry barriers for new competitors.

Competitive strategies increasingly focus on improving energy efficiency, diversifying heat sources, and integrating renewable and low-carbon technologies into district heating systems. Companies are investing in advanced digital platforms to optimize network performance, manage heat distribution, and reduce operational losses. Integration of waste heat from industrial facilities and data centers is emerging as an important competitive advantage, enabling operators to lower costs and improve sustainability profiles. In parallel, firms are exploring new investment models such as power-to-heat systems, large-scale heat pumps, and next-generation low-temperature heating networks designed to support decarbonized urban energy infrastructure.

Key Developments:

- November, 2025: Veolia launched its low-carbon “Ecothermal Grid” district heating offering in the UK, announcing a £1 billion pipeline of projects through 2030 to expand carbon-neutral heat networks across multiple cities using waste heat, geothermal energy, and digital energy management technologies.

- May, 2025: Telia increased the capacity of its district heating solution at the Pitäjänmäki data center in Helsinki, raising waste heat recovery to about 90% and enabling the system to potentially heat more than 28,000 apartments across the Finnish capital.

- March, 2025: Vattenfall AB announced it is assessing ownership options for its district heating operations in the UK, Sweden, and the Netherlands, including potential divestment, as part of a broader portfolio review to prioritize investments in fossil-free energy infrastructure.

Companies Covered in District Heating Market

- Vattenfall AB

- ENGIE SA

- Fortum Corporation

- Veolia Environnement S.A.

- Ramboll Group A/S

- Danfoss Group

- NRG Energy Inc.

- LOGSTOR A/S

- Keppel DHCS Pte Ltd

- Korea District Heating Corporation (KDHC)

- RWE AG

- STEAG GmbH

- Shinryo Corporation

- Cetetherm

- Enwave Energy Corporation

- E.ON SE

- Statkraft AS

- Helen Ltd.

- Alfa Laval AB

Frequently Asked Questions

The global District Heating market is estimated to reach US$ 196.7 billion in 2026, driven by expanding centralized heating networks and increasing integration of renewable and low-carbon heat sources.

Key demand drivers include decarbonization policies, rapid urbanization, government funding for heat network infrastructure, and growing integration of industrial and data-center waste heat.

Europe leads the District Heating market, supported by mature heating networks, strong decarbonization policies, and widespread adoption across Nordic and Central European countries.

A major growth opportunity lies in integrating data center and industrial waste heat into district heating networks alongside low-temperature renewable-based heating systems.

Key players include ENGIE SA, Vattenfall AB, Veolia Environnement S.A., Fortum Corporation, Danfoss Group, RWE AG, Korea District Heating Corporation, Enwave Energy Corporation, Keppel DHCS Pte Ltd, and Ramboll Group A/S.