- Smart Packaging

- Paper Bags Market

Paper Bags Market Size, Share, and Growth Forecast 2026 - 2033

Paper Bags Market by Product Type (Sewn Open Mouth, Pinched Bottom Open Mouth, Pasted Valve, Pasted Open Mouth, Flat Bottom, Others), Material Type (Kraft Paper, Recycled Paper, Coated Paper, Specialty Paper), Distribution Channel (B2B, B2C), Industry (Food and Beverages, Pharmaceutical, Retail & E-commerce, Construction, Industrial), and Regional Analysis, 2026 - 2033

Paper Bags Market Size and Trend Analysis

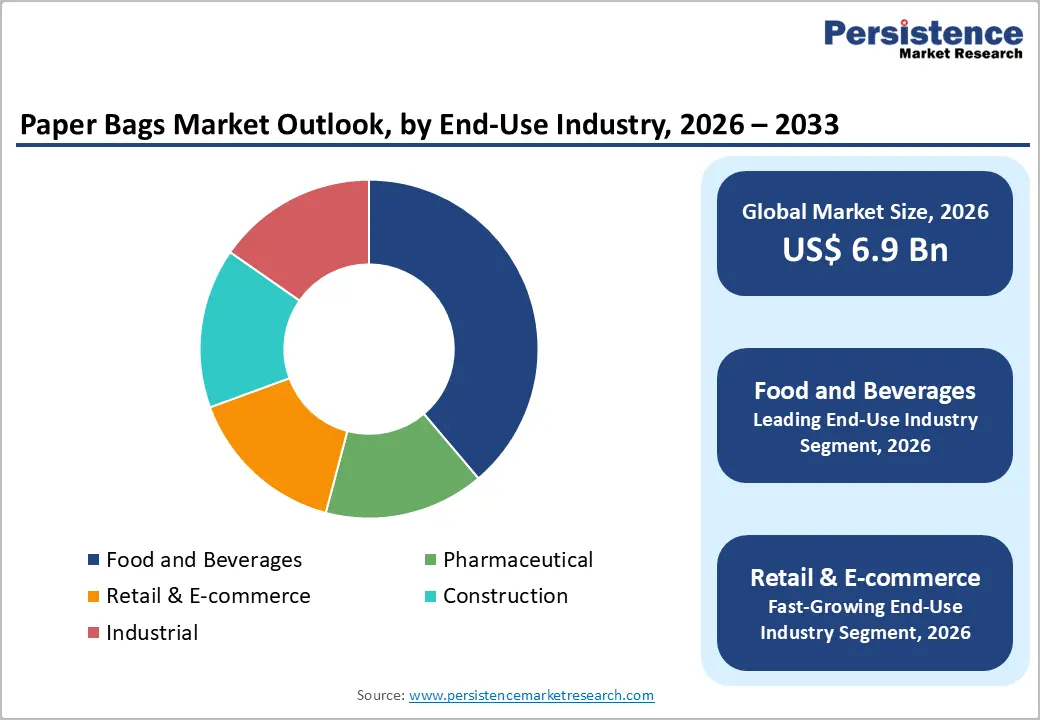

The global paper bags market size is expected to be valued at US$ 6.9 billion in 2026 and projected to reach US$ 10.3 billion by 2033, growing at a CAGR of 5.9% between 2026 and 2033. This sustained expansion is primarily driven by the accelerating global legislative shift from single-use plastic packaging toward paper-based alternatives, growing consumer and brand owner sustainability commitments, and the rapid expansion of organized retail and e-commerce packaging applications across Asia Pacific and Latin America.

The market grew from US$ 5.0 billion in 2020 at a historical CAGR of 5.4%, underpinned by landmark plastic bag bans across over 60 countries, the EU's Single-Use Plastics Directive, and growing food & beverage industry demand for kraft paper bags as a recyclable, food-safe, and premium-branded primary packaging solution.

Key Industry Highlights

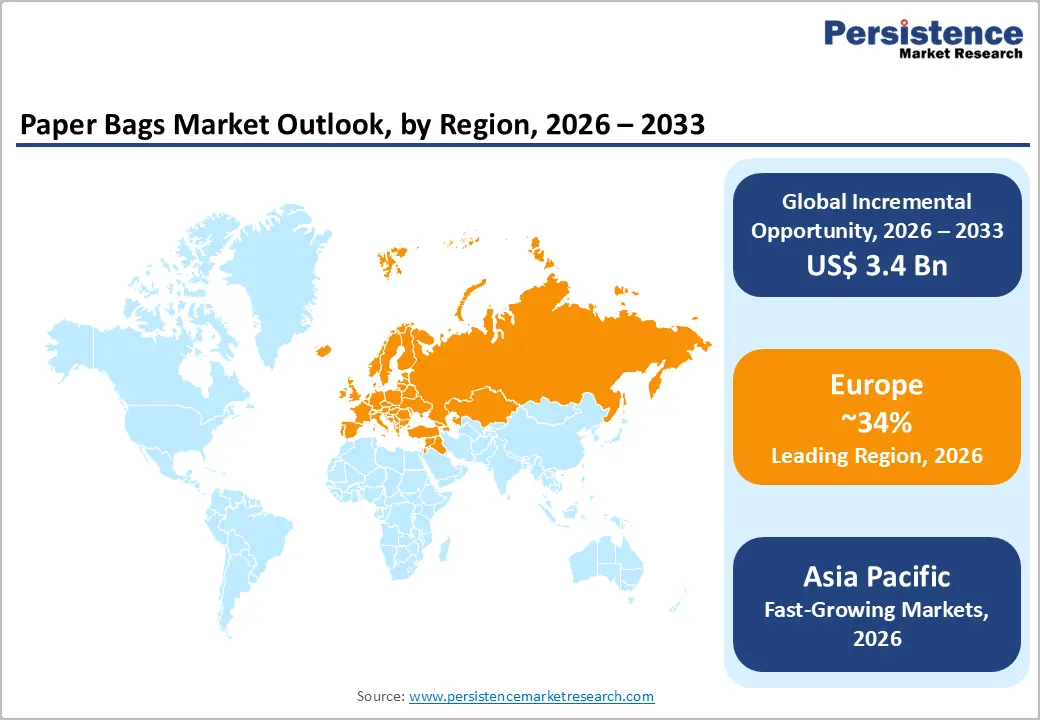

- Leading Region: Europe leads the global paper bags market with 34% market share in 2025, driven by EU Single-Use Plastics Directive mandates across 27 member states, strong paper manufacturing infrastructure from Mondi, Smurfit Westrock, and DS Smith, and retail sustainability commitments.

- Fastest Growing Region: Asia Pacific is the fastest growing region at 7.2% CAGR through 2033, driven by India's Single Use Plastic Phase-Out Rules 2022, China's expanding organized retail paper bag demand, and industrial multi-wall kraft bag demand from Southeast Asia's ADB-backed construction pipeline.

- Dominant Material Type: Kraft paper holds 58% material type market share in 2025, dominating through superior tensile strength, FSC/PEFC certification availability, natural sustainability aesthetic preferred by premium food and retail brands, and FDA/EU food contact compliance credentials for direct food packaging applications.

- Fastest Growing Industry: Retail & E-commerce is the fastest growing end-use segment, driven by major fashion and DTC brand transitions to 100% paper carry bags, Retail Industry Leaders Association sustainability commitments, and growing branded paper bag demand as a premium consumer-facing packaging touchpoint.

- Key Opportunity: Recyclable, moisture-barrier-coated kraft paper bags, replacing PE-lined plastic alternatives in fresh food and agricultural applications, represent the highest-margin innovation opportunity, combining Nestlé, Mondelez, and Unilever packaging transition commitments with growing regulatory restrictions on plastic-lined food packaging.

Market Dynamics

Drivers - Global Plastic Bag Bans and Single-Use Plastic Regulations Mandating Paper Bag Substitution

The worldwide regulatory wave of banning or taxing single-use plastic bags, has created mandatory substitution demand for paper-based alternatives across retail, grocery, and foodservice applications. The United Nations Environment Programme (UNEP) reports that over 60 countries have enacted national plastic bag bans or levies, with the EU Single-Use Plastics Directive (2019/904) banning the most common single-use plastic products from 2021 across 27 member states.

In the U.S., over 12 states have enacted single-use plastic bag bans, with major retailers including Whole Foods Market, Trader Joe's, and Target proactively transitioning to paper bag alternatives. India's Single Use Plastic (SUP) Phase-Out Rules 2022 have accelerated paper bag adoption across the Indian retail sector, creating an enormous and rapidly growing demand base for kraft and specialty paper bags.

Growing Food & Beverage Sector Demand for Kraft Paper Bags as Sustainable Primary Packaging

The food and beverage industry's adoption of kraft paper bags as premium, food-safe, and recyclable primary packaging, for bakery goods, coffee, pet food, organic produce, and processed food, is creating a structurally growing, high-value demand category for paper bag manufacturers. The Food and Agriculture Organization (FAO) documents consistent growth in global packaged food consumption, with organic and premium food segments, which disproportionately adopt paper-based packaging for brand differentiation, growing at above-average rates.

Certified kraft paper bags meeting FDA food contact safety standards and EU Food Contact Materials Regulation (EC) No 1935/2004 are commanding specification preference from food manufacturers seeking both regulatory compliance and sustainable packaging credentials. Multinational food companies including Nestlé, Mondelez, and Unilever have publicly committed to transitioning packaging portfolios toward paper-based alternatives, sustaining premium kraft paper bag demand growth through 2033.

Restraints - Higher Cost Per Unit Relative to Plastic Bag Alternatives

Paper bags consistently carry a cost premium of 3-8 times the unit cost of equivalent-capacity plastic bags, driven by higher raw material (virgin or recycled kraft fiber), manufacturing energy, and transportation costs due to greater weight and volume per unit. For price-sensitive retailers and food service operators in developing markets, particularly in Sub-Saharan Africa and South Asia, this cost differential remains a significant barrier to rapid paper bag adoption, particularly where regulatory enforcement of plastic bans is inconsistent and cheaper plastic alternatives remain accessible.

Performance Limitations in Moisture-Exposed and Heavy-Load Applications

Paper bags face inherent performance limitations in applications involving moisture exposure, heavy loads, or rough handling. Standard kraft paper bags degrade significantly in humid conditions, a key constraint for fresh produce, cold chain, and certain industrial applications. While wet-strength treatments and moisture-barrier coatings partially address this limitation, they add cost and can compromise recyclability credentials, creating a performance-cost-sustainability trade-off that limits paper bag adoption in applications where these challenges are most acute. The Fibre Box Association (FBA) acknowledges these performance constraints as a persistent barrier to full substitution of plastic alternatives in demanding physical distribution environments.

Opportunities - E-commerce and Retail Packaging Shift Toward Sustainable Paper Bag Solutions

The explosive growth of e-commerce, particularly the direct-to-consumer segment, is creating a fast-growing, premium demand category for branded paper bags as both primary packaging and retail-experience elements. The U.S. Census Bureau reports consistent double-digit growth in U.S. e-commerce sales, with similar trajectories documented in Europe and Asia Pacific. Major fashion and luxury brands including H&M, Zara, Macy's, and Nordstrom have transitioned to 100% paper retail carry bags as centerpieces of their sustainability commitments, driving branded specialty paper bag procurement.

The Retail Industry Leaders Association (RILA) documents growing retailer commitments to plastic-free packaging programs, with paper bags serving as the primary substitute across apparel, accessories, and gift retail. This premium retail paper bag segment commands higher margins and more stable demand cycles than commodity grocery paper bags.

Asia Pacific Industrial and Agricultural Paper Bag Demand: Fastest Growing Regional Application

Asia Pacific's rapidly expanding industrial and agricultural sectors represent a high-volume, fast-growing demand opportunity for industrial-grade paper bags, particularly multi-wall kraft bags for cement, chemicals, fertilizers, and agricultural commodities. India's National Programme on Organic Production (NPOP) and growing organic agriculture sector are driving demand for food-grade kraft bags for certified organic commodity packaging.

China's National Sword policy transition, which redirected domestic paper manufacturing capacity toward value-added products including food-grade kraft paper, has strengthened domestic paper bag supply capabilities. The Asian Development Bank (ADB) reports consistent growth in construction and industrial activity across Southeast Asia, driving demand for multi-wall paper bags in cement and building materials applications, a segment where paper bags hold significant advantages over flexible plastics in terms of filling speed, printability, and end-of-life recyclability.

Category-wise Analysis

Product Type Insights

Pinched Bottom Open Mouth (PBOM) paper bags represent the leading Product Type segment, accounting for approximately 34% market share in 2025. PBOM bags are the dominant format in retail, grocery, and food service applications due to their flat-bottom gusset construction that enables stable standing on shelves and easy filling on automated packaging lines. Their compatibility with high-speed form-fill-seal packaging equipment makes them the preferred format for food & beverage manufacturers adopting paper primary packaging at scale.

Major brands including Mondi, Smurfit Westrock, and Novolex maintain the most extensive PBOM bag product portfolios, serving both retail grocery and branded specialty applications. The PBOM format's suitability for high-quality print decoration, enabling premium branded packaging aesthetics, further reinforces its dominant position across the food & beverage and retail end-use segments.

Material Type Insights

Kraft paper is the dominant material type, accounting for approximately 58% market share in 2025. Kraft paper, produced from the chemical kraft pulping process, delivers the highest tensile and tear strength among paper substrates, making it the preferred material for load-bearing paper bags across food, industrial, and retail applications. Its natural brown appearance has become associated with sustainability and premium product positioning, making it the specification choice for both functional industrial multi-wall bags and premium branded retail paper bags.

The American Forest & Paper Association (AF&PA) documents kraft paper as the largest segment of U.S. packaging paper production by volume. FSC-certified and PEFC-certified kraft paper grades are increasingly specified in brand owner sustainability programs that require chain-of-custody fiber sourcing credentials.

Distribution Channel Insights

B2B distribution dominates the paper bags market, accounting for approximately 72% market share in 2025. The paper bag market is fundamentally an industrial supply chain, with the vast majority of paper bags sold directly from manufacturers and distributors to end-user businesses including food manufacturers, retailers, construction companies, and chemical producers operating at scale.

Major paper bag producers including International Paper, Mondi, and Smurfit Westrock derive the overwhelming majority of their paper bag revenue through long-term B2B supply contracts with institutional buyers. The B2C channel, serving retail consumers purchasing branded paper bags directly, is smaller but growing faster, particularly in the premium specialty paper bag and branded retail carry bag segments where direct-to-consumer and e-commerce channel growth is most active.

Industry Insights

Food and Beverages is the dominant Industry segment, accounting for approximately 40% of the total paper bags market share in 2025. The food & beverage industry is the largest consumer of paper bags across multiple format types, from grocery carry bags and retail food service bags to multi-wall kraft bags for flour, sugar, coffee, pet food, and agricultural commodities.

FDA and EU food contact compliance requirements favor paper over plastic in direct food contact applications, and the food industry's outsized participation in corporate sustainability packaging commitments, such as the Ellen MacArthur Foundation's New Plastics Economy initiative, accelerates paper bag adoption. The premium organic and natural food segment's preference for kraft paper packaging as a brand signifier of clean-label, sustainable positioning further reinforces food & beverage's dominant and growing share.

Regional Insights

Europe leads the global paper bags market with approximately 34% market share in 2025, while Asia Pacific is the fastest growing region, projected to record the highest CAGR of approximately 7.2% through 2026 - 2033.

North America Paper Bags Market Trends and Insights

North America is a mature, regulation-driven paper bags market characterized by progressive state-level plastic bag bans, strong brand owner sustainability commitments, and active grocery and retail paper bag consumption. The Sustainable Packaging Coalition documents growing retailer commitments to 100% paper carry bag policies across major U.S. chains, while foodservice and grocery segments drive consistent kraft bag volume. Premium branded paper bag demand is growing fastest among fashion, specialty retail, and DTC e-commerce channels.

U.S. Paper Bags Market Size

The United States accounts for approximately 79% of North American paper bags market revenue in 2025. Plastic bag bans across 12+ states including California, New York, and Hawaii, combined with major retailer transitions to paper, including Target, Trader Joe's, and Whole Foods, sustain growing retail paper bag demand. The U.S. food & beverage industry's kraft paper bag procurement, supported by FDA food contact compliance, represents the largest single demand category.

Europe Paper Bags Market Trends and Insights

Europe leads the global paper bags market, shaped by the EU Single-Use Plastics Directive, EU Packaging and Packaging Waste Regulation (PPWR), and national plastic bag levies creating consistent, policy-mandated paper bag demand across all 27 EU member states. The region's advanced paper bag manufacturing ecosystem, anchored by Mondi, Smurfit Westrock, and DS Smith, and premium retailer paper bag programs sustain market leadership.

Germany Paper Bags Market Size

Germany holds approximately 21% of European paper bags market revenue in 2025. Germany's Verpackungsgesetz (Packaging Act) mandating high packaging recyclability and the country's extensive retail network, including Edeka, Rewe, and dm-drogerie markt, drive large-scale paper bag procurement. Germany's world-class paper manufacturing base includes Papier-Mettler as a key specialized paper bag producer serving European retail and industrial markets.

U.K. Paper Bags Market Size

The United Kingdom represents approximately 16% of European paper bags market revenue in 2025. The UK's Single-Use Carrier Bag Charge (10 pence per bag, expanded to all retail businesses in 2021, has directly mandated the transition to reusable or paper alternatives. The UK's active fashion retail sector, including Marks & Spencer, Next, and John Lewis, sustains premium branded paper bag procurement.

France Paper Bags Market Size

France accounts for approximately 12% of European paper bags market revenue in 2025. France's Loi AGEC (Anti-Waste for a Circular Economy Law) mandates progressive elimination of plastic packaging, with paper bags benefiting from the transition across French grocery retail, specialty food, and fashion channels. France's active luxury retail sector, including flagship stores of leading fashion and cosmetics brands, drives premium specialty paper bag demand.

Asia Pacific Paper Bags Market Trends and Insights

Asia Pacific is the fastest growing paper bags market, driven by China's massive retail sector and food industry paper bag consumption, India's SUP phase-out rules driving rapid retail adoption, and industrial multi-wall paper bag demand across Southeast Asia's construction and chemical sectors. China accounts for approximately 43% of Asia Pacific demand, with domestic producers serving an expanding organized retail sector and growing food & beverage industry paper bag requirements as plastic restrictions tighten.

India Paper Bags Market Size

India represents approximately 16% of Asia Pacific paper bags market revenue in 2025. India's Single Use Plastic Phase-Out Rules 2022 banning plastic carry bags below 75 microns have created immediate, mandatory paper bag substitution demand across millions of Indian retail outlets. India's rapidly expanding organized retail sector and agricultural commodity packaging requirements are additional structural demand drivers for kraft paper bags.

Japan Paper Bags Market Size

Japan contributes approximately 12% of Asia Pacific paper bags market revenue in 2025. Japan's Plastic Resource Circulation Act (effective 2022) mandates that retailers charge for single-use plastic bags, accelerating paper bag adoption across Japanese retail. Japan's advanced food packaging culture and preference for high-quality, premium-printed paper bags in food retail and gift packaging sustain consistent above-average per-unit value demand.

Southeast Asia Paper Bags Market Size

Southeast Asia collectively accounts for approximately 14% of Asia Pacific paper bags market revenue in 2025. Progressive plastic bag bans in Thailand, Vietnam, Malaysia, and the Philippines are driving retail paper bag substitution. The region's active construction and industrial sectors generate substantial multi-wall kraft paper bag demand for cement, fertilizer, and chemical packaging, with the ADB's reported US$ 210 billion annual infrastructure investment pipeline sustaining this industrial demand.

Competitive Landscape

The global paper bags market exhibits a moderately consolidated structure at the upper end of the value chain, where a few large integrated packaging producers hold significant share, while a broad base of regional and niche manufacturers competes in price-sensitive segments. Large players benefit from backward integration into pulp production, scale efficiencies, and long-term contracts with FMCG, retail, and food service customers, whereas smaller firms focus on localized demand and customized offerings.

Competitive differentiation is increasingly driven by sustainability credentials such as FSC and PEFC certifications, compliance with global food safety standards, and the ability to deliver high-quality printed and branded packaging solutions. Companies are also investing in advanced barrier technologies to replace plastic coatings while maintaining recyclability. Supply chain reliability and cost control remain critical in winning large institutional contracts. Additionally, premiumization trends are supporting growth in branded paper packaging programs for retail and e-commerce clients, creating higher-margin opportunities across developed markets.

Key Developments

- April 2026: Mondi opened a new paper bags manufacturing facility in Pittsburgh, Pennsylvania, to expand its production capacity in the United States and support rising demand from e-commerce, food, and industrial packaging customers.

- July 2025: Evonik launched an eco-friendly 25-kg paper bag for its MetAMINO product by eliminating the plastic film layer, improving recyclability, reducing CO2 emissions by about 20%, and aligning packaging with EU PPWR sustainability regulations across production sites.

- June 2025: Mondi launched its re/cycle PaperPlus Bag Advanced, a high-performance paper bag designed for humidity-sensitive products, offering up to 60% reduced plastic use while maintaining strong moisture barrier performance and recyclability for industrial packaging applications.

Paper Bags Market - Key Insights

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 5.0 Billion |

| Current Market Value (2026) | US$ 6.9 Billion |

| Projected Market Value (2033) | US$ 10.3 Billion |

| CAGR (2026 - 2033) | 5.9% |

| Leading Region | Europe, 34% market share (2025) |

| Dominant Material Type | Kraft Paper, 58% market share (2025) |

| Top-Ranking Product Type | Pinched Bottom Open Mouth, 34% market share (2025) |

| Incremental Opportunity (2026 - 2033) | US$ 3.4 Billion |

Companies Covered in Paper Bags Market

- Mondi

- Smurfit Westrock

- International Paper

- Novolex

- Oji Holdings Corporation

- DS Smith (now part of International Paper)

- Amcor plc

- Papier-Mettler

- Welton Bibby & Baron

- ProAmpac

- Langston Bag

- York Paper Company Ltd

- Hood Packaging Corporation

- El Dorado Packaging

- Gelpac Inc.

Frequently Asked Questions

The global paper bags market is projected at US$ 6.9 billion in 2026, growing steadily toward US$ 10.3 billion by 2033.

Key drivers include global plastic bag bans, food industry shift to sustainable packaging, and rising use in retail and e-commerce.

Europe leads with about 34% share, supported by strict plastic regulations and strong adoption of sustainable packaging solutions.

Major opportunities lie in moisture-resistant recyclable paper bags and expanding demand from retail and e-commerce sectors.

Key players include Mondi, Smurfit Westrock, International Paper, Novolex, Oji Holdings Corporation, DS Smith, Amcor plc, ProAmpac, Papier-Mettler, Welton Bibby & Baron, Langston Bag, and York Paper Company Ltd.