- Smart Packaging

- Recyclable Packaging Market

Recyclable Packaging Market Size, Share, and Growth Forecast 2026 - 2033

Recyclable Packaging Market by Material Type (Paper & Paperboard, Plastic, Glass, Metal, Wood) Product Type (Bottles & Jars, Bags & Pouches, Boxes & Cartons, Trays & Containers, Drums & Cans, Wraps & Films, Protective Packaging), Packaging Format (Rigid Packaging, Flexible Packaging, Protective Packaging), Industry (Food & Beverages, Healthcare & Pharmaceuticals, Personal Care & Cosmetics, Household & Consumer Goods, Industrial & Chemicals, Retail & E-Commerce), and Regional Analysis, 2026 - 2033

Recyclable Packaging Market Size and Trend Analysis

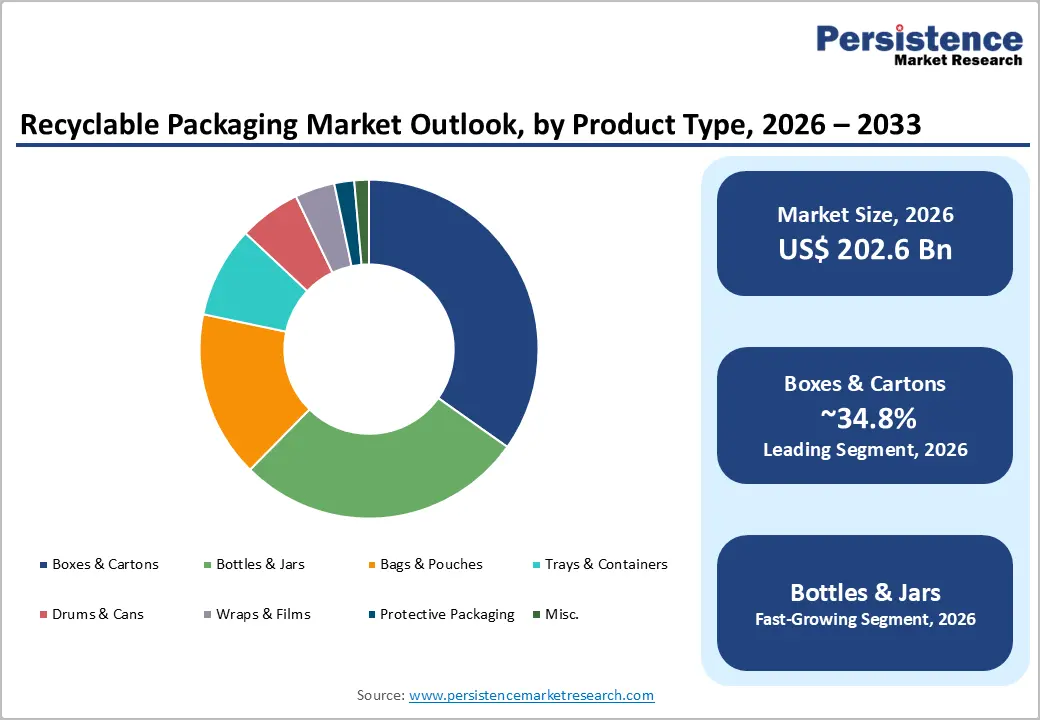

The global recyclable packaging market size is expected to be valued at US$ 202.6 billion in 2026 and projected to reach US$ 319.0 billion by 2033, growing at a CAGR of 6.7% between 2026 and 2033. The market's robust expansion is primarily underpinned by a convergence of tightening regulatory frameworks and a structural shift in consumer purchasing behavior toward sustainability-conscious products.

The European Union's Packaging and Packaging Waste Regulation (PPWR), which mandates that all packaging placed on the EU market be recyclable by 2030, is compelling manufacturers across sectors to reformulate their packaging strategies at scale. Simultaneously, the United Nations Environment Programme (UNEP) Global Plastics Treaty negotiations are driving multinational brands to commit to extended producer responsibility (EPR) and minimum recycled content thresholds, accelerating investment in recyclable material innovation across North America, the sAsia Pacific, and beyond.

Key Industry Highlights:

- Leading Region: Asia Pacific leads the global recyclable packaging market with a 36.8% share in 2025, driven by China's 14th Five-Year Plan recycling mandates, India's booming food processing and e-commerce sectors, and the region's dominance of global B2B eCommerce GMV at approximately 80% of worldwide volume.

- Emerging Region: Latin America and Asia Pacific's emerging markets are the fastest-growing regions, with India's industrial warehousing leasing hitting a record 39.5 million sq. ft. in 2024 and Brazil's healthcare market at US$ 135 billion, driving recyclable pharmaceutical packaging demand at accelerating rates.

- Leading Material Segment: Paper & Paperboard dominates the Material Type category with 38% market share in 2025, anchored by industry-leading recycling rates of 74% in Europe and 68% in the U.S., widespread regulatory acceptance, and structural demand from e-commerce corrugated and food carton applications.

- Fast-Growing Segment: Flexible recyclable plastic packaging is the fastest-growing segment at a projected 7% CAGR from 2026 to 2033, propelled by mono-material PE laminate innovations, CEFLEX design guidelines, and surging e-commerce mailer and DTC brand packaging demand globally.

- Key Opportunity: The highest-value strategic opportunity lies at the intersection of pharmaceutical and healthcare recyclable packaging. Europe's ageing population, nearly one-third over 65 by 2050, and India's Ayushman Bharat-driven healthcare expansion are creating premium, compliance-grade recyclable packaging demand that remains significantly underserved.

DRO Analysis

Drivers - Tightening Global Regulatory Mandates Compelling Packaging Redesign

A sweeping wave of legislative action is fundamentally restructuring material procurement and packaging design decisions across industries. The EU Packaging and Packaging Waste Regulation (PPWR), proposed by the European Commission in November 2022, mandates that all packaging be recyclable by 2030 and sets minimum recycled content thresholds ranging from 30% to 65% for various plastic packaging categories by 2040.

In the United States, California's SB 54 signed into law in 2022, requires 100% of plastic packaging to be recyclable or compostable by 2032 and mandates a 25% reduction in single-use plastic packaging. These legislative requirements are compelling brand owners, contract packagers, and raw material suppliers to prioritise recyclable substrates, driving sustained volume demand for paper, glass, metal, and next-generation recyclable plastic formats. Countries across Southeast Asia and Latin America are enacting analogous EPR frameworks, broadening the regulatory push beyond mature economies.

Surging Corporate Sustainability Commitments Across Consumer Goods and Food & Beverages Sectors

Global fast-moving consumer goods (FMCG) manufacturers are operationalising ambitious packaging sustainability pledges at a pace that directly fuels recyclable packaging procurement. Unilever has committed to making 100% of its plastic packaging reusable, recyclable, or compostable, while Nestlé has pledged that all its packaging will be recyclable or reusable by 2025. In the food and beverages space, which represents one of the largest end-use segments for recyclable packaging, the structural imperative is particularly pronounced.

The U.S. food and beverage manufacturing sector employed approximately 1.7 million workers in 2021 and accounted for 16.8% of total U.S. manufacturing sales, reflecting the enormous packaging consumption footprint. As processors in this industry reformulate packaging to meet retailer sustainability scorecards and end-consumer expectations, demand for certified recyclable formats in boxes & cartons, bottles & jars, and bags & pouches segments is supported.

Restraints - Infrastructure Deficiencies in Recycling Collection and Sortation Limiting Material Recovery Rates

Despite policy tailwinds, the physical infrastructure required to close the recyclable packaging loop remains critically underdeveloped in many geographies. According to the Ellen MacArthur Foundation, only 14% of plastic packaging is collected for recycling globally, with even lower rates in emerging economies.

The European Environment Agency (EEA) reports that paper and cardboard recycling rates across EU member states range from under 50% in some Eastern European nations to over 85% in Germany and the Netherlands. When packaging is collected but cannot be effectively sorted and reprocessed due to multi-material construction or contamination, it undermines the commercial viability of recyclable packaging claims, creating consumer skepticism and exposing companies to greenwashing risk, a significant commercial and reputational restraint for market participants.

Elevated Production Costs and Price Premiums of Recyclable Formats Versus Conventional Alternatives

The cost differential between recyclable packaging solutions and conventional non-recyclable counterparts remains a material commercial barrier, particularly for price-sensitive categories and small-to-medium enterprises. Packaging incorporating post-consumer recycled (PCR) content commands price premiums of 15% to 40% over virgin material equivalents, depending on substrate type and PCR content percentage, according to Packaging Digest and industry procurement benchmarks.

For flexible plastic formats, the transition to mono-material recyclable structures requires capital investment in new tooling and line modifications. In food and beverage applications, recyclable packaging must also meet food-contact safety requirements, adding regulatory compliance costs. These combined cost pressures disproportionately impact mid-tier manufacturers, slowing the pace of adoption in segments outside large multinational brand portfolios.

Opportunities- Mono-Material Flexible Packaging Innovation: Unlocking Recyclability in High-Growth Pouches Segment

The flexible packaging segment encompassing bags & pouches and wraps & fFilms has historically faced structural recyclability challenges due to its multi-layer construction combining dissimilar materials such as PET, PE, aluminum, and paper. However, advances in mono-material flexible structures, particularly all-polyethene (PE) laminates with high-barrier coatings, are enabling flexible packaging to enter certified recyclable streams for the first time at a commercial scale. CEFLEX, the Circular Economy for Flexible Packaging initiative backed by over 180 European industry participants, has established guidelines for designing flexible packaging for recyclability that are gaining adoption across converters and brand owners.

The global B2B eCommerce market, projected to reach US$ 36,163 billion in GMV by 2026 at a CAGR of 14.5%, is a key demand driver for flexible packaging formats, as e-commerce fulfilment drives adoption of lightweight, protective, and recyclable mailers and pouches. Companies investing in mono-material flexible innovation are positioned to capture a disproportionate share of the fastest-growing product type segment.

Expanding Healthcare & Pharmaceutical End-Use Sector Creating Premium Recyclable Packaging Demand

The healthcare and pharmaceutical sector presents a structurally attractive and underserved opportunity for recyclable packaging providers. Europe's healthcare system faces an estimated shortfall of 1.2 million doctors, nurses, and midwives, according to Health at a Glance: Europe 2024, and with nearly one-third of the EU's population projected to be over 65 by 2050, sustained demand for pharmaceutical packaging across chronic disease management and long-term care categories is structurally secured.

In India, the healthcare industry, supported by government initiatives such as Ayushman Bharat and rising FDI inflows, is expanding rapidly, creating new demand for compliant, sustainable secondary and tertiary packaging. Brazil's healthcare market, valued at approximately US$ 135 billion (representing 9.7% of GDP), with its dual public-private structure serving 72% of the population through the Sistema Único de Saúde (SUS), presents a significant addressable base for recyclable pharmaceutical and medical device packaging formats.

Category-wise Analysis

Material Type Insights

Paper & paperboard dominate the global recyclable packaging market, commanding approximately 38% of total market share in 2026, reflecting its unmatched combination of recyclability credentials, regulatory compliance, and versatility across end-use applications. Paper and paperboard are among the most efficiently recycled materials globally. The Confederation of European Paper Industries (CEPI) reported a European paper recycling rate of 74% in 2022, among the highest of any packaging material.

In the United States, the American Forest & Paper Association (AF&PA) confirmed a paper recycling rate of 68% in 2021. The material's dominance is further reinforced by consumer trust: multiple consumer surveys consistently identify paper-based packaging as the most recognisable sustainable option. Boxes & Cartons for food and beverage applications, along with corrugated board for e-commerce secondary packaging, are the primary volume drivers within this segment.

Product Type Insights

Boxes & cartons represent the leading segment within the product type category, accounting for approximately 32% share in 2026. This leadership reflects the dominant role of corrugated and folding carton formats across the food & beverages, retail, and e-commerce end-use industries, the three largest demand verticals for recyclable packaging.

The growth of e-commerce has been a particular catalyst: global B2B eCommerce GMV is forecast to reach US$ 36,163 billion by 2026, while India's e-commerce market, worth approximately US$ 125 billion in 2024, is projected to reach US$ 345 billion by 2030, generating substantial corrugated box demand across fulfilment and last-mile delivery chains. Food and beverage applications further anchor this segment, as cereal cartons, beverage multipacks, and retail shelf-ready packaging are predominantly fibre-based and recyclable by design.

Industry Insights

Food & beverages represent the dominant end-use segment, accounting for approximately 34% of the global recyclable packaging market in 2026. The sector's primacy reflects both its sheer scale as a packaging consumer and its accelerating transition toward sustainable formats under retailer mandates and consumer pressure.

The EU's accommodation and food services sector generated €280.7 billion in value added in 2022 and comprised nearly 2.0 million enterprises, underpinning massive packaging consumption across food processing, retail, and foodservice channels. In the United States, food and beverage manufacturing accounted for 16.8% of total manufacturing sales in 2021, with over 42,700 establishments nationally. India's food processing sector, valued at INR. 30.5 lakh crore (US$ 354.5 billion) in 2024 and projected to reach US$ 535 billion by FY26, is an emerging volume driver for recyclable packaging formats across processed, ready-to-eat, and dairy product categories.

Regional Insights

North America Recyclable Packaging Market Trends and Insights

North America holds a 24.9% share of the global recyclable packaging market in 2026, supported by a mature regulatory environment, high consumer sustainability awareness, and a well-developed recycling infrastructure, particularly in the United States and Canada. The region is characterised by strong adoption of paper-based and aluminium recyclable formats across food, beverage, and e-commerce channels, alongside accelerating legislative mandates at both federal and state levels, driving reformulation across rigid and flexible packaging categories.

U.S. Recyclable Packaging Market Size

The U.S. recyclable packaging market was valued at approximately US$ 40 billion in 2026. This scale is directly attributable to the U.S. food and beverage manufacturing sector's outsized packaging footprint, 16.8% of total U.S. manufacturing sales, combined with California's SB 54 mandate requiring 100% recyclable or compostable plastic packaging by 2032, which has compelled national brands to reformulate packaging portfolios. The proliferation of over 42,700 food manufacturing establishments nationwide, alongside surging e-commerce corrugated demand, anchors sustained recyclable packaging consumption at scale.

Europe Recyclable Packaging Market Trends and Insights

Europe is likely to register a 28.7% share of the global recyclable packaging market in 2026, making it the second-largest regional market and the world's most advanced from a regulatory standpoint. The EU Packaging and Packaging Waste Regulation (PPWR), mandatory recyclability targets by 2030, and harmonised EPR frameworks across member states are collectively creating the most stringent and commercially transformative packaging regulatory environment globally, accelerating substitution of non-recyclable formats across all end-use industries.

Germany Recyclable Packaging Market Size

Germany's recyclable packaging market is likely to be valued at approximately US$ 9.2 billion in 2026. Germany operates Europe's most sophisticated dual packaging take-back system, the Duales System Deutschland (DSD, or 'Green Dot' system), which has delivered paper recycling rates exceeding 85% and glass recycling rates above 80%, among the highest globally. This infrastructure maturity, combined with Germany's position as Europe's largest manufacturing economy and a key hub for automotive, chemical, and food processing industries, sustains high structural demand for certified recyclable packaging formats.

U.K. Recyclable Packaging Market Size

The U.K. recyclable packaging market reached approximately US$ 12.4 billion in 2025, reflecting the country's advanced retailer-led sustainability agenda and accelerating post-Brexit packaging regulations.

The UK Plastic Packaging Tax, effective from April 2022, imposes a charge of £217.85 per tonne on plastic packaging manufactured in or imported into the UK that contains less than 30% recycled plastic content, creating a direct financial incentive for manufacturers to shift to certified recyclable formats. Major retailers, including Tesco, Sainsbury's, and Marks & Spencer, have established packaging recyclability commitments tied to their 2025 and 2030 sustainability targets, driving upstream supply chain reformulation.

Asia Pacific Recyclable Packaging Market Trends and Insights

sAsia Pacific is the largest regional market for recyclable packaging, holding a 36.8% share in 2025, driven by the region's unparalleled manufacturing scale, rapid e-commerce growth, and tightening national regulations in China, Japan, South Korea, and India. China's 14th Five-Year Plan for Circular Economy Development and the National Sword policy have fundamentally restructured domestic recycling infrastructure investment.

The region's B2B eCommerce GMV, representing approximately 80% of global B2B eCommerce volume projected at US$ 36,163 billion by 2026, drives enormous corrugated and flexible recyclable packaging demand across China, India, Japan, and Southeast Asian manufacturing hubs.

China Recyclable Packaging Market Size

China's recyclable packaging market was valued at approximately US$ 30.5 billion in 2025, underpinned by the country's position as the world's largest manufacturing and export economy and the rapid scale-up of its domestic e-commerce ecosystem.

China's 14th Five-Year Plan explicitly targets a recycling rate of 60% for renewable resources by 2025, backed by mandatory producer take-back schemes and significant investment in sorting and reprocessing infrastructure. The dominance of Alibaba, JD.com, and Pinduoduo in generating billions of annual parcel shipments creates structural, non-cyclical demand for corrugated, paper-based, and recyclable flexible packaging at a scale unmatched by any other national market.

India Recyclable Packaging Market Size

India's recyclable packaging market reached approximately US$ 12.2 billion in 2025 and is among the fastest-growing country-level markets globally, propelled by the intersection of a booming food processing industry, surging e-commerce, and strengthening regulatory action on plastic waste. India's food processing sector, valued at US$ 354.5 billion in 2024 and projected to reach US$ 535 billion by FY26, is a principal driver of recyclable packaging consumption.

The country's e-commerce market, forecast to reach US$ 345 billion by 2030, is generating record warehousing demand. Industrial & warehousing leasing hit 39.5 million sq. ft. across eight major cities in 2024, creating cascading demand for corrugated and protective recyclable packaging across fulfilment networks.

Competitive Landscape

The global recyclable packaging market exhibits a moderately consolidated structure at the top tier, with multinational packaging conglomerates including Amcor plc, Sealed Air Corporation, Berry Global Group, Smurfit WestRock, and DS Smith commanding significant revenue shares through diversified product portfolios spanning paper, plastic, and flexible substrates. These leaders differentiate through investment in R&D for certified recyclable mono-material innovations, strategic acquisitions to bolster sustainable packaging capabilities, and co-development partnerships with FMCG brand owners.

The mid-tier and lower segments remain fragmented, populated by regional converters and speciality packaging manufacturers. An emerging trend is the formation of pre-competitive industry consortia such as CEFLEX and The Consumer Goods Forum's (CGF) Plastic Waste Coalition, where competitors collaborate on recyclability design standards to achieve systemic change that individual company action cannot deliver alone.

Key Developments:

- May 2026: UPM and BASF collaborated to accelerate the development of recyclable fibre-based packaging solutions by combining UPM’s barrier papers with BASF’s Joncryl® HPB barrier coating technology, enabling high-performance recyclable packaging alternatives for food and non-food applications aligned with circular economy and packaging waste reduction regulations.

- March 2026: Barilla announced that 99.8% of its product packaging is designed to be recyclable, while over 50% of packaging materials used globally are recycled materials, reinforcing the company’s commitment toward circular packaging solutions through sustainable paper-based packaging, recyclable design improvements, and packaging material reduction initiatives targeted through 2030.

Companies Covered in Recyclable Packaging Market

- Amcor plc

- Sealed Air

- Tetra Pak

- Mondi

- DS Smith

- WestRock Company

- Stora Enso

- Ball Corporation

- Crown Holdings, Inc.

- Gerresheimer AG

- Oji Holdings Corporation

- Ardagh Group S.A.

- Trivium Packaging

- Huhtamaki Oyj

- ProAmpac

- Constantia Flexibles

Frequently Asked Questions

The global recyclable packaging market is estimated to be valued at US$ 202.6 billion in 2026.

The primary demand drivers are the tightening regulatory mandates, including the EU Packaging and Packaging Waste Regulation (PPWR), requiring all packaging to be recyclable by 2030, and California's SB 54 mandating 100% recyclable or compostable plastic packaging by 2032 alongside structural shifts in consumer behavior toward sustainability. The exponential growth of global B2B eCommerce GMV, projected at US$ 36,163 billion by 2026 at a CAGR of 14.5%, further amplifies corrugated and flexible recyclable packaging demand.

Asia Pacific is the leading region with a 36.8% share in 2025, driven by China's manufacturing scale, India's booming food processing and e-commerce sectors, and the region's commanding approximately 80% share of global B2B eCommerce GMV.

The highest-value opportunity lies in mono-material flexible recyclable packaging and healthcare & pharmaceutical recyclable formats. Flexible packaging innovations enabled by CEFLEX design-for-recyclability guidelines and all-PE laminate structures are unlocking the fastest-growing product segment at a projected 7% CAGR (2026-2033). In parallel, Europe's ageing population, nearly one-third over 65 by 2050 and India's expanding healthcare sector under Ayushman Bharat are creating premium recyclable packaging demand that remains significantly underserved.

Leading companies in the global recyclable packaging market include Amcor plc, Smurfit WestRock plc, Berry Global Group, DS Smith plc, International Paper Company, Mondi Group, Sealed Air Corporation, Huhtamaki Oyj, Ball Corporation, Crown Holdings and Others.