- Executive Summary

- Global Nuclear Medicine Market Snapshot 2026 and 2033

- Market Opportunity Assessment, 2026-2033, US$ Bn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply-Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Market Dynamics

- Driver

- Restraint

- Opportunities

- Trends

- Macro-Economic Factors

- Global GDP Outlook

- Global Prison Growth Outlook

- Global Crime Rates by Country

- Global Prison Population by Country

- Global Private Prison Market Growth Outlook

- Forecast Factors – Relevance and Impact

- COVID-19 Impact Assessment

- Value Added Insights

- Value Chain analysis

- Key Market Players

- Product Adoption Analysis

- Key Promotional Strategies by key players

- PESTLE Analysis

- Porter's Five Forces Analysis

- Regulatory and Technology Landscape

- Global Nuclear Medicine Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Global Nuclear Medicine Market Outlook: Product

- Introduction/Key Findings

- Historical Market Size (US$ Bn) Analysis by Product, 2020-2025

- Current Market Size (US$ Bn) Forecast, by Product, 2026-2033

- Diagnosis

- SPECT

- PET

- Market Attractiveness Analysis: Product

- Global Nuclear Medicine Market Outlook: Application

- Introduction/Key Findings

- Historical Market Size (US$ Bn) Analysis by Application, 2020-2025

- Current Market Size (US$ Bn) Forecast, by Application, 2026-2033

- Urology

- Cardiology

- Neurology

- Market Attractiveness Analysis: Application

- Global Nuclear Medicine Market Outlook: End Use

- Introduction/Key Findings

- Historical Market Size (US$ Bn) Analysis by End Use, 2020-2025

- Current Market Size (US$ Bn) Forecast, by End Use, 2026-2033

- Hospitals

- Diagnostic Centres

- Market Attractiveness Analysis: End Use

- Global Nuclear Medicine Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) Analysis by Region, 2020-2025

- Current Market Size (US$ Bn) Forecast by Region, 2026-2033

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Nuclear Medicine Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- North America Market Size (US$ Bn) Forecast, by Country, 2026-2033

- U.S.

- Canada

- North America Market Size (US$ Bn) Forecast, by Product, 2026-2033

- Diagnosis

- SPECT

- PET

- North America Market Size (US$ Bn) Forecast, by Application, 2026-2033

- Urology

- Cardiology

- Neurology

- North America Market Size (US$ Bn) Forecast, by End Use, 2026-2033

- Hospitals

- Diagnostic Centres

- Europe Nuclear Medicine Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Europe Market Size (US$ Bn) Forecast, by Country, 2026-2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Europe Market Size (US$ Bn) Forecast, by Product, 2026-2033

- Diagnosis

- SPECT

- PET

- Europe Market Size (US$ Bn) Forecast, by Application, 2026-2033

- Urology

- Cardiology

- Neurology

- Europe Market Size (US$ Bn) Forecast, by End Use, 2026-2033

- Hospitals

- Diagnostic Centres

- East Asia Nuclear Medicine Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- East Asia Market Size (US$ Bn) Forecast, by Country, 2026-2033

- China

- Japan

- South Korea

- East Asia Market Size (US$ Bn) Forecast, by Product, 2026-2033

- Diagnosis

- SPECT

- PET

- East Asia Market Size (US$ Bn) Forecast, by Application, 2026-2033

- Urology

- Cardiology

- Neurology

- East Asia Market Size (US$ Bn) Forecast, by End Use, 2026-2033

- Hospitals

- Diagnostic Centres

- South Asia & Oceania Nuclear Medicine Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- South Asia & Oceania Market Size (US$ Bn) Forecast, by Country, 2026-2033

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Bn) Forecast, by Product, 2026-2033

- Diagnosis

- SPECT

- PET

- South Asia & Oceania Market Size (US$ Bn) Forecast, by Application, 2026-2033

- Urology

- Cardiology

- Neurology

- South Asia & Oceania Market Size (US$ Bn) Forecast, by End Use, 2026-2033

- Hospitals

- Diagnostic Centres

- Latin America Nuclear Medicine Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Latin America Market Size (US$ Bn) Forecast, by Country, 2026-2033

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Bn) Forecast, by Product, 2026-2033

- Diagnosis

- SPECT

- PET

- Latin America Market Size (US$ Bn) Forecast, by Application, 2026-2033

- Urology

- Cardiology

- Neurology

- Latin America Market Size (US$ Bn) Forecast, by End Use, 2026-2033

- Hospitals

- Diagnostic Centres

- Middle East & Africa Nuclear Medicine Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Middle East & Africa Market Size (US$ Bn) Forecast, by Country, 2026-2033

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Bn) Forecast, by Product, 2026-2033

- Diagnosis

- SPECT

- PET

- Middle East & Africa Market Size (US$ Bn) Forecast, by Application, 2026-2033

- Urology

- Cardiology

- Neurology

- Middle East & Africa Market Size (US$ Bn) Forecast, by End Use, 2026-2033

- Hospitals

- Diagnostic Centres

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- GE Healthcare

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- Jubilant Life Sciences Ltd

- Nordion (Canada), Inc.

- Bracco Imaging S.P.A

- The institute for radioelements (IRE)

- NTP Radioisotopes SOC Ltd.

- The Australian Nuclear Science and Technology Organization

- Eczacıbaşı Monrol

- Lantheus Medical Imaging, Inc

- Eckert & Ziegler

- Mallinckrodt

- Cardinal Health

- Others

- GE Healthcare

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Medical Devices

- Nuclear Medicine Market

Nuclear Medicine Market Size, Share, and Growth Forecast 2026 - 2033

Nuclear Medicine Market by Product (Diagnosis, SPECT, PET), by Application (Urology, Cardiology, Neurology), by End Use (Hospitals, Diagnostic Centres), by Regional Analysis, 2026-2033

Nuclear Medicine Market Size and Trends Analysis

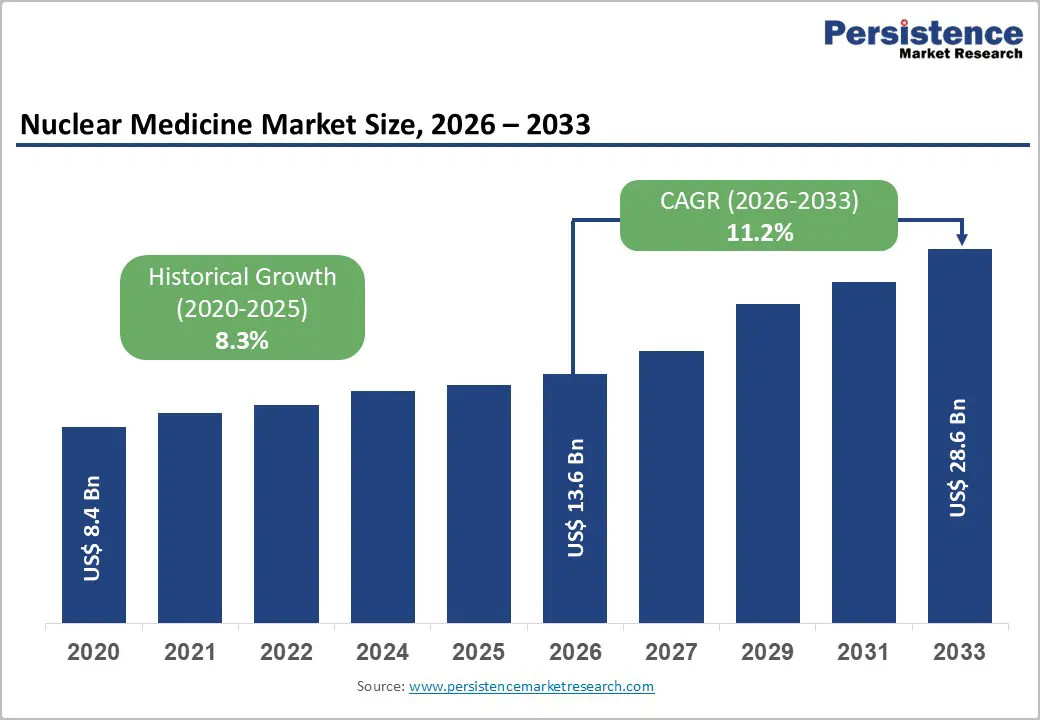

The global nuclear medicine market size is expected to be valued at US$ 13.6 billion in 2026 and projected to reach US$ 28.6 billion by 2033, growing at a CAGR of 11.2% between 2026 and 2033

The market is growing because more people are getting cancer and heart diseases, which require more advanced diagnostics and therapies. The market is experiencing significant growth, driven by rising incomes, increased spending on healthcare infrastructure and services, and the development of new radiopharmaceuticals and treatment methods.

Nuclear medicine is a medical imaging modality that uses small amounts of radioactive material to identify, assess the severity of, or treat various conditions, including heart disease, many types of cancer, and disorders of the digestive, endocrine, and nervous systems. Nuclear medicine imaging provides substantially more information about the anatomy and physiology of organs and tissues than standard imaging methods, which only reveal the body's structure. Radiopharmaceuticals are used to achieve this. These chemicals emit gamma rays that can be detected by certain cameras.

When these cameras are connected to computers, they produce high-resolution images that show where and how much nuclear material is in the body. Nuclear medicine is beneficial for patients because it allows physicians to see how their bodies work at the molecular level. This facilitates early diagnosis and the selection of appropriate treatment.

Key Industry Highlights

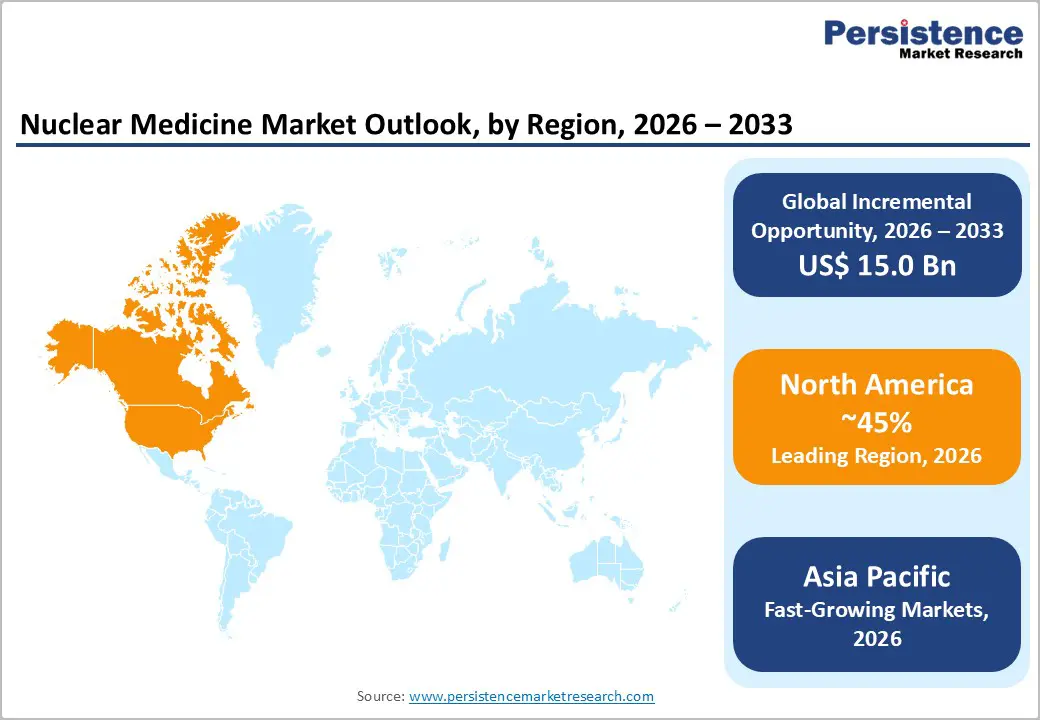

- Leading Region: North America leads the global nuclear medicine market, supported by advanced imaging infrastructure, high adoption of PET and SPECT systems, and favourable reimbursement policies.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, driven by rising cancer and cardiovascular disease prevalence, expanding hospital infrastructure, and increased healthcare investments.

- Dominant Segment: Diagnostic imaging dominates due to widespread use of PET and SPECT for early detection, treatment monitoring, and high procedure volumes globally.

- Fastest Growing Segment: PET imaging is growing fastest, fuelled by technological advancements, hybrid imaging systems, and increasing adoption in oncology and neurology applications.

| Global Market Attributes | Key Insights |

|---|---|

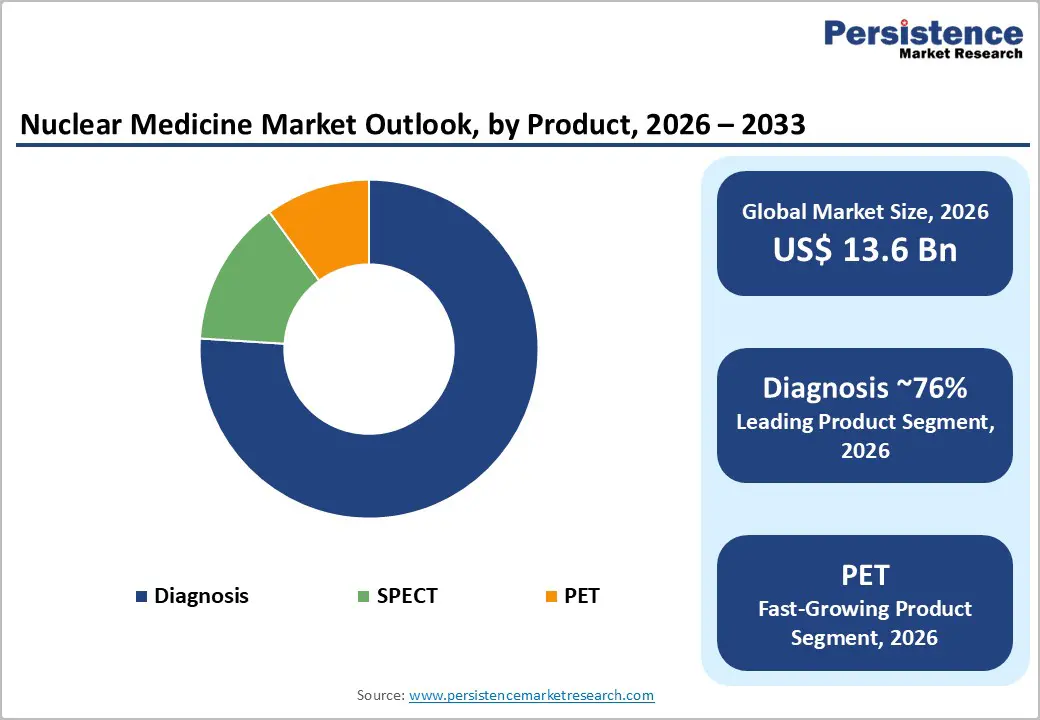

| Nuclear Medicine Market Size (2026E) | US$ 13.6 billion |

| Market Value Forecast (2033F) | US$ 28.6 billion |

| Projected Growth CAGR (2026-2033) | 11.2% |

| Historical Market Growth (2020-2025) | 8.3% |

Market Dynamics

Driver – Technological Innovation and Chronic Disease Burden Accelerating Global Nuclear Medicine Market Expansion

The high capital expenditure associated with PET and SPECT scanners remains a major barrier, particularly for hospitals in resource-limited settings. Acquisition costs, infrastructure requirements, shielding facilities, and regular maintenance significantly raise financial burdens, discouraging smaller centers from adopting nuclear medicine capabilities. Radiopharmaceutical production entails additional costs because synthesis processes require sophisticated equipment, regulatory compliance, and rigorous quality controls. Short half-lives also necessitate rapid logistics, cold-chain transportation, and regional cyclotron facilities, increasing operational risk and expenditure.

Operating nuclear medicine departments requires specialized physicians, radiopharmacists, physicists, and technologists, whose training and salaries increase recurring costs. Compliance with radiation safety standards requires monitoring systems, protective materials, and facility redesigns, further inflating budgets. Inconsistent reimbursement policies across countries compound these challenges, as inadequate procedural coverage limits providers' profitability. Such financial constraints restrict service expansion, slow technology uptake, and reduce patient access in developing and semi-urban markets.

Restraints – High Equipment Costs, Operational Complexity, Skilled Workforce Needs, and Reimbursement Gaps Restrain Adoption

The high capital expenditure associated with PET and SPECT scanners remains a major barrier, particularly for hospitals in resource-limited settings. Acquisition costs, infrastructure requirements, shielding facilities, and regular maintenance significantly raise financial burdens, discouraging smaller centers from adopting nuclear medicine capabilities. Radiopharmaceutical production entails additional costs because synthesis processes require sophisticated equipment, regulatory compliance, and rigorous quality controls. Short half-lives also necessitate rapid logistics, cold-chain transportation, and regional cyclotron facilities, increasing operational risk and expenditure.

Operating nuclear medicine departments requires specialized physicians, radiopharmacists, physicists, and technologists, whose training and salaries increase recurring costs. Compliance with radiation safety standards requires monitoring systems, protective materials, and facility redesigns, further inflating budgets. Inconsistent reimbursement policies across countries compound these challenges, as inadequate procedural coverage limits providers' profitability. Such financial constraints restrict service expansion, slow technology uptake, and reduce patient access in developing and semi-urban markets.

Opportunity – Hybrid Imaging Platforms and Expanding Radiopharmaceutical Pipelines Creating Significant Future Market Opportunities

Hybrid imaging systems such as PET/CT, SPECT/CT, and PET/MRI offer major growth opportunities by combining anatomical detail with functional assessment in a single scan. The integration of artificial intelligence into these platforms enhances image interpretation, accelerates reporting, and supports earlier diagnosis. Industry efforts toward compact and portable nuclear imaging devices could unlock new care settings, including outpatient centers, emergency departments, and remote clinics, improving access for underserved populations and enabling decentralized diagnostics.

Radiopharmaceutical innovation represents another high-potential opportunity area. Novel tracers for prostate cancer, neuroendocrine tumors, and inflammatory or neurodegenerative disorders expand clinical utility and patient pools. Theranostic approaches enable personalized treatment planning, aligning with value-based healthcare models. Extending nuclear medicine beyond oncology into cardiology, neurology, and infectious disease imaging broadens the addressable market, while collaborations among research institutes, isotope producers, and pharmaceutical companies can accelerate commercialization and geographic expansion.

Category-wise Analysis

By Product Analysis

By product type, the global nuclear medicine market is segmented into diagnostic imaging, SPECT, and PET, with diagnostic imaging accounting for the largest market share. This dominance is supported by the widespread use of nuclear imaging for disease detection, staging, and therapy monitoring across oncology, cardiology, and neurology. The increasing availability of advanced imaging modalities such as Single-Photon Emission Computed Tomography (SPECT) and Positron Emission Tomography (PET) has significantly improved diagnostic accuracy, workflow efficiency, and clinical confidence. Hospitals and diagnostic centers increasingly rely on these modalities because they provide functional insights that conventional imaging cannot, enabling earlier intervention and more informed treatment decisions.

Industry activity is further strengthened by rising procedure volumes worldwide and expanding radiotracer portfolios. According to the World Nuclear Association’s 2024 analysis, approximately 50 million nuclear medicine procedures are performed annually, alongside nearly 5% yearly growth in radioisotope demand. Continuous technological upgrades, hybrid imaging platforms, and development of novel tracers for tumor detection are accelerating market expansion. Together, increasing patient numbers, procedural growth, and innovation in diagnostic agents reinforce the global leadership of the diagnosis-focused product segment.

By Application Analysis

By application, the nuclear medicine market is categorized into urology, cardiology, and neurology, with urology representing the dominant segment. This leadership is driven largely by the expanding use of nuclear imaging and theranostic agents in prostate cancer diagnosis, staging, and targeted therapy. Radiopharmaceuticals such as PSMA-based tracers enable highly specific tumor visualization, supporting personalized treatment planning and monitoring. As a result, healthcare providers increasingly adopt nuclear techniques for managing urological diseases, positioning this application area as both the largest and fastest-growing segment during the forecast period.

Growth is reinforced by the rising global burden of prostate cancer, now recognized as the second most frequently diagnosed cancer among men. High incidence has been reported across major markets, including the United States, China, Japan, Brazil, Germany, France, the United Kingdom, Russia, Italy, and India. Contributing factors include aging male populations, lifestyle changes, and improved screening practices. These epidemiological trends, combined with expanding therapeutic options, continue to propel nuclear medicine utilization within urology worldwide.

Region-wise Insights

North America Nuclear Medicine Market Trends

In 2026, North America is expected to hold a 45% share of the global nuclear medicine market, maintaining its position as the leading regional market. This dominance is driven by the rapid adoption of advanced imaging technologies, including PET and SPECT, and the growing use of innovative therapeutic radiopharmaceuticals. Increasing prevalence of chronic diseases, particularly various cancers and cardiovascular conditions, further supports market expansion. Hospitals and diagnostic centers are investing heavily in cutting-edge nuclear medicine equipment to enhance diagnostic accuracy, treatment monitoring, and patient outcomes.

The U.S. remains the largest contributor to the regional market due to high incidences of heart disease and extensive utilization of PET and SPECT systems. However, market growth faces challenges from supply chain constraints, logistical complexities, and a shortage of skilled medical professionals. Despite these hurdles, ongoing investments in technology, infrastructure, and training are expected to sustain North America’s leading position and drive continuous growth throughout the forecast period.

Europe Nuclear Medicine Market Trends

Europe’s nuclear medicine market is recognized as highly lucrative, benefiting from the expansion of hospitals, clinics, and diagnostic centers. This expansion has increased demand for nuclear medicine products, driven by rising patient visits for disease diagnosis and treatment. Advanced imaging technologies, particularly PET and SPECT, are increasingly adopted across European countries to improve diagnostic precision, enhance workflow efficiency, and support early disease detection.

The UK nuclear medicine market is expected to witness significant growth during the forecast period, fueled by ongoing technological advancements in imaging systems. These innovations enable more accurate diagnosis and personalized treatment planning for oncology, cardiology, and neurology patients. Furthermore, favorable healthcare policies, increased healthcare spending, and investments in research and development support market expansion. Overall, Europe’s focus on technological integration, growing patient demand, and strategic healthcare investments positions the region as a key contributor to global growth in the nuclear medicine market.

Asia Pacific Nuclear Medicine Market Trends

The Asia-Pacific nuclear medicine market is experiencing rapid growth, driven by increasing healthcare investments, the rising prevalence of chronic diseases, and heightened awareness of advanced diagnostic and therapeutic solutions. Countries like China, Japan, and India are witnessing a surge in demand for PET and SPECT imaging systems due to expanding hospital infrastructure, rising patient volumes, and government initiatives supporting modern healthcare technologies. The region’s large population base and increasing incidence of cancers, cardiovascular, and neurological disorders further contribute to the adoption of nuclear medicine procedures.

Technological advancements, such as hybrid imaging systems and novel radiopharmaceuticals, are accelerating market growth in the Asia Pacific region. Efforts to improve healthcare access in tier-2 and tier-3 cities, along with collaborations between local and international healthcare providers, are expanding the reach of nuclear medicine services. Despite challenges such as high equipment costs and a limited number of skilled professionals, ongoing investments in infrastructure, training, and research are expected to strengthen the regional market and support sustained growth throughout the forecast period.

Market Competitive Landscape

The global nuclear medicine market is highly competitive, with major players assessed based on product portfolios, service offerings, financial performance, market positioning, and geographic presence. Companies are evaluated through SWOT analysis to understand their strengths, weaknesses, opportunities, and threats, providing insights into their strategic capabilities and operational efficiency. This analysis helps identify industry leaders and emerging challengers while highlighting areas of competitive advantage in technology adoption, product innovation, and market share.

To strengthen their market position, key competitors actively pursue strategic initiatives such as partnerships, mergers and acquisitions, and regional business expansions. These strategies allow companies to broaden service offerings, enter new markets, and enhance their global footprint. Continuous innovation and collaboration remain central to maintaining competitiveness and meeting evolving nuclear medicine demand worldwide.

Key Industry Developments:

- In December 2025, three nuclear medicine organizations jointly endorsed a standardized PET/CT and PET/MRI scanner accreditation framework to harmonize quantitative PET imaging globally.

- In November 2025, UCLA Health inaugurated its Department of Nuclear Medicine and Theranostics.

- In Mar 2024, the Ministry of Health of the Republic of Serbia and Rosatom State Corporation entered a Memorandum of Understanding (MoU) to collaborate on nuclear medicine. This collaboration is expected to accelerate market expansion over the forecast period.

- In Jan 2024, Lantheus Holdings, Inc. (Lantheus) strengthened its position in the US nuclear medicine industry by entering strategic partnerships with Perspective Therapeutics, Inc.

Companies Covered in Nuclear Medicine Market

- GE Healthcare

- Jubilant Life Sciences Ltd

- Nordion (Canada), Inc.

- Bracco Imaging S.P.A

- The institute for radioelements (IRE)

- NTP Radioisotopes SOC Ltd.

- The Australian Nuclear Science and Technology Organization

- Eczacıbaşı Monrol

- Lantheus Medical Imaging, Inc

- Eckert & Ziegler

- Mallinckrodt

- Cardinal Health

- Others

Frequently Asked Questions

The market is estimated to be valued at US$ 13.6 Bn in 2026.

Nuclear medicine is applied in various fields such as oncology, cardiology, and neurology for both diagnosis and treatment purposes.

The global market is expected to witness a CAGR of 11.2% between 2026 and 2033.

Some of the key players include GE Healthcare, Jubilant Life Sciences Ltd, Nordion (Canada), Inc., Bracco Imaging S.P.A, and The Institute for Radioelements (IRE).

North America is the leading region in the global nuclear medicine market.