- Metals & Minerals

- Nickel Alloy Market

Nickel Alloy Market Size, Share, and Growth Forecast 2026 - 2033

Nickel Alloy Market by Product Type (Heat-Resistant Nickel Alloys, Corrosion-Resistant Nickel Alloys, Electrical-Resistant Nickel Alloys, Low-Expansion Nickel Alloys, Other Type), by Composition (Ni-Cu, Ni-Cr-Fe, Ni-Cr-Mo, Ni-Mo, Misc.), by Industry (Aerospace & Defense, Chemical, Automotive, Oil & Gas, Power Generation, Electrical & Electronics, Misc.), by Regional Analysis, 2026 - 2033

Nickel Alloy Market Size and Trend Analysis

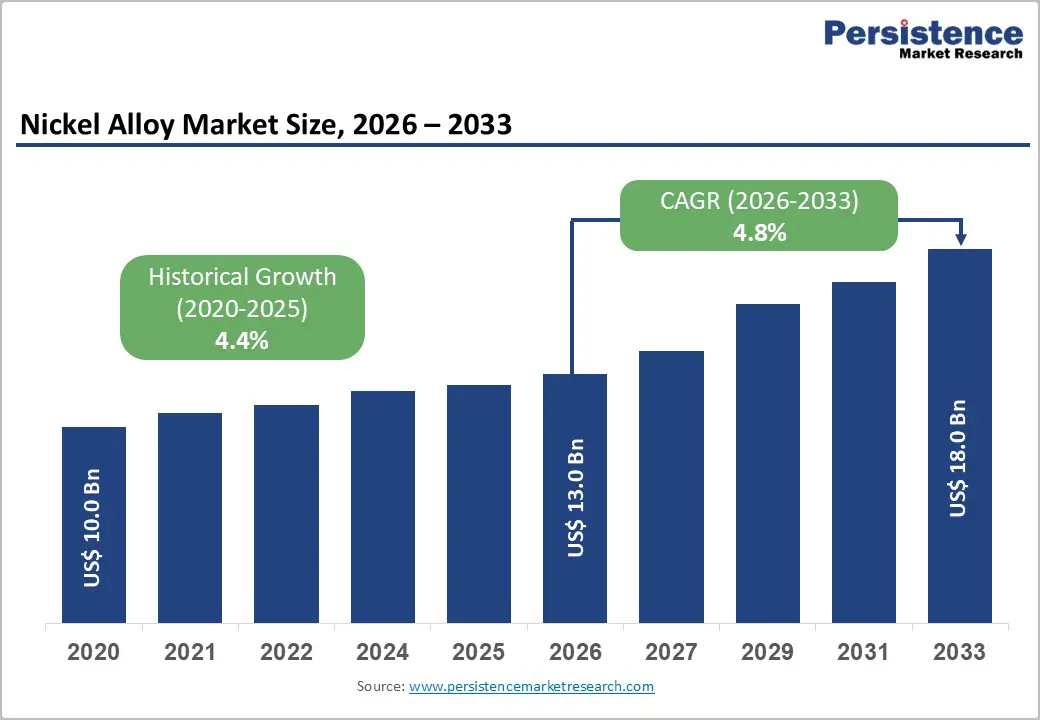

The global nickel alloy market size is expected to be valued at US$ 13.0 billion in 2026 and projected to reach US$ 18.0 billion by 2033, growing at a CAGR of 4.8% between 2026 and 2033.

This steady and resilient growth is underpinned by the irreplaceable role of nickel alloys in mission-critical, high-performance industrial applications, particularly in aerospace propulsion systems, gas turbine power generation, and corrosion-intensive chemical processing environments, where no cost-effective substitute material currently exists. The global resurgence of commercial aviation post-pandemic, accelerating investment in next-generation gas turbine technology, and expanding oil and gas exploration and production activity across deepwater and high-temperature well environments are collectively reinforcing durable end-use demand.

Key Industry Highlights

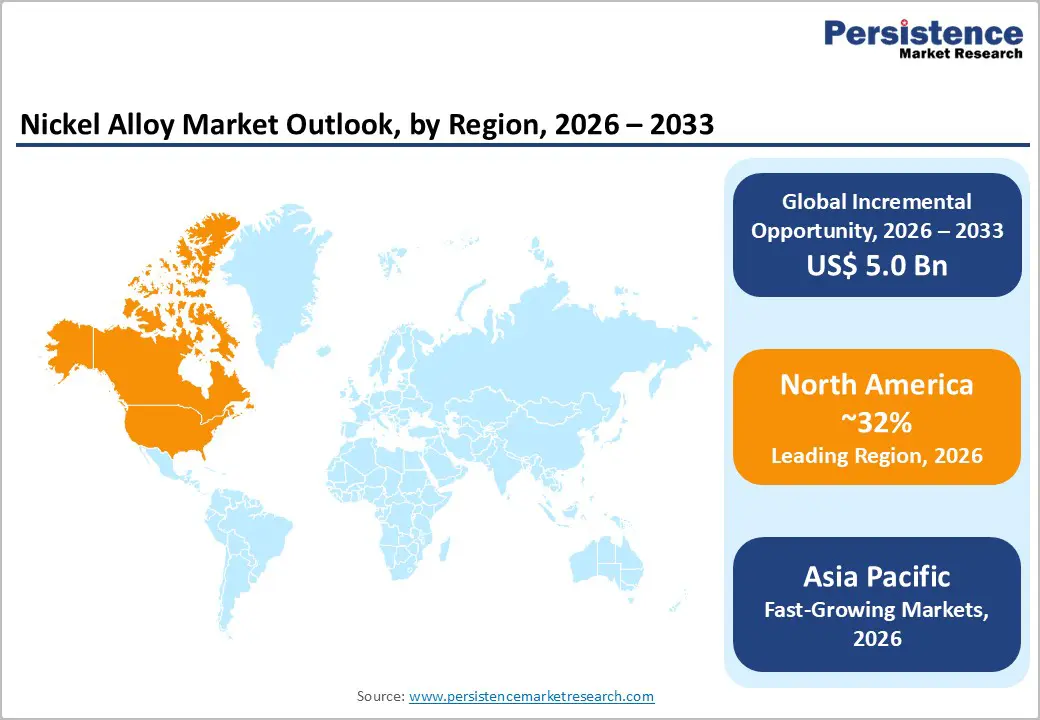

- Leading Region: North America leads the global Nickel Alloy Market with around 32% share in 2025, supported by the United States’ strong aerospace engine manufacturing base and focus on specialty alloy supply chain resilience.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, projected to expand at a CAGR of approximately 6.5% through 2033, driven by aviation expansion, defense modernization, and petrochemical investments.

- Dominant Segment: Aerospace & Defense dominates with about 35% share in 2025 due to the critical use of nickel superalloys in jet engines and strong commercial aircraft backlogs.

- Fastest Growing Segment: Power Generation is the fastest-growing end-use segment, supported by rising investments in gas turbines, SMR nuclear programs, and hydrogen infrastructure.

- Key Opportunity: Hydrogen economy infrastructure presents a major long-term opportunity, with expanding electrolyzer, compression, and reforming capacity expected to drive substantial nickel alloy demand.

| Key Insights | Details |

|---|---|

| Nickel Alloy Market Size (2026E) | US$ 13.0 Billion |

| Market Value Forecast (2033F) | US$ 18.0 Billion |

| Projected Growth CAGR (2026 - 2033) | 4.8% |

| Historical Market Growth (2020 - 2025) | 4.4% |

Market Dynamics

Drivers - Recovering Commercial Aviation and Next-Generation Aerospace Programs Driving Sustained Superalloy Demand

The global commercial aerospace sector’s strong recovery from the COVID-19 pandemic disruption is the most consequential near-term demand driver for nickel superalloys, the highest-value segment within the broader nickel alloy market. Nickel-based superalloys account for approximately 50% of the total weight of modern aircraft turbine engines, serving as the material of choice for turbine blades, vanes, disks, and combustion chamber components that must retain mechanical integrity at temperatures exceeding 1,000°C under extreme centrifugal stress. The International Air Transport Association (IATA) reported that global air passenger traffic fully recovered to pre-pandemic levels in 2023 and is forecast to nearly double by 2040, driving sustained demand for new aircraft deliveries across both narrowbody and widebody platforms. Boeing and Airbus reported combined order backlogs exceeding 13,000 aircraft as of 2024, representing approximately 10 years of production at current rates. This enormous manufacturing pipeline ensures a structurally durable, multi-year demand backlog for aerospace-grade nickel superalloy producers including Precision Castparts Corp, Carpenter Technology Corporation, and Haynes International, suppliers whose aerospace revenues are tightly correlated with jet engine production volumes from GE Aerospace, Pratt & Whitney, and Rolls-Royce.

Expanding Oil & Gas Exploration and Chemical Processing Industries Reinforcing Corrosion-Resistant Alloy Demand

Global energy security imperatives and the sustained investment cycle in oil and gas upstream activities, particularly in deepwater, high-pressure, and high-temperature (HPHT) well environments, are generating consistent demand growth for corrosion-resistant nickel alloys. Nickel alloys such as Alloy 625 (Inconel 625) and Alloy C-276 (Hastelloy C-276) are the materials of choice for subsea pipeline components, wellhead equipment, downhole tubing, and heat exchangers in sour gas environments, where resistance to hydrogen sulfide (H2S) stress corrosion cracking and chloride pitting is critical. The U.S. Energy Information Administration (EIA) projects global oil demand to remain above 100 million barrels per day through the early 2030s, supporting continued upstream capital expenditure by major operators. In the chemical processing industry, corrosion-resistant nickel alloys are indispensable in reactors, pressure vessels, and piping systems handling aggressive acids, alkalis, and halogenated compounds, applications where material failure carries significant safety and economic consequences, reinforcing specification of premium nickel alloy grades over lower-cost alternatives.

Restraints - Nickel Price Volatility and Supply Chain Concentration Introducing Significant Market Uncertainty

Raw nickel price volatility represents one of the most persistent structural risks to the nickel alloy market. The London Metal Exchange (LME) nickel price experienced an extraordinary short-squeeze event in March 2022, briefly surpassing US$ 100,000 per metric ton before trading was suspended, highlighting the extreme price sensitivity and supply chain vulnerability inherent in the nickel market. Even under normalized trading conditions, nickel prices have historically exhibited high cyclicality driven by shifts in Indonesian ore export policy, stainless steel demand fluctuations, and EV battery material investment cycles. As nickel accounts for the largest cost component in most nickel alloy formulations, sustained price spikes directly compress margins for both alloy producers and downstream fabricators, constraining investment decisions and creating demand substitution pressure in cost-sensitive applications.

Emerging Material Substitution Threats from Advanced Ceramics and Titanium Alloys in Select Applications

Nickel alloys face growing material substitution pressure in certain high-temperature applications from advanced ceramic matrix composites (CMCs) and titanium aluminide (TiAl) intermetallic alloys, which offer superior temperature capability and substantially lower density. GE Aerospace and Safran have incorporated silicon carbide fiber-reinforced CMC components into the LEAP and GE9X engine hot sections, replacing nickel superalloy parts in turbine shrouds and combustor liners, enabling weight savings of up to 30% compared to equivalent nickel alloy components. While substitution currently affects a narrow range of hot-section components, the progressive maturation of CMC manufacturing technology and the aerospace sector’s relentless pursuit of fuel efficiency improvements could gradually erode nickel alloy volume demand in the highest-temperature turbine applications over the forecast period.

Opportunity - Hydrogen Economy Infrastructure Creating Transformational New Demand for High-Performance Nickel Alloys

The accelerating global transition toward hydrogen as a clean energy carrier is emerging as one of the most strategically significant long-term growth opportunities for the nickel alloy market. Nickel-based alloys, owing to their exceptional resistance to hydrogen embrittlement, high-temperature oxidation, and stress corrosion cracking, are uniquely positioned as the material of choice for critical hydrogen economy infrastructure components including electrolyzers, fuel cells, hydrogen compression and storage vessels, cryogenic hydrogen transport equipment, and high-temperature steam methane reforming (SMR) reactors. The International Energy Agency (IEA) projects that global clean hydrogen production capacity must expand to approximately 70 million metric tons per year by 2030 under net-zero scenarios, a trajectory requiring enormous capital investment in hydrogen production and distribution infrastructure. Haynes International’s HAYNES 230 and 282 alloys and VDM Metals’ nickel-based grades are already being specified for solid oxide electrolyzer and hydrogen compressor applications. As national hydrogen strategies gain momentum across the European Union, United States, Japan, and South Korea, nickel alloy demand from the hydrogen sector is expected to grow at a significantly above-average rate through 2033, creating a high-value incremental revenue opportunity for established alloy producers.

Advanced Nuclear Power Generation Programs Offering a High-Value, Long-Cycle Demand Opportunity

The global nuclear energy renaissance, driven by the recognition of nuclear power’s role as a dispatchable, low-carbon baseload energy source critical to net-zero electricity systems, is creating a compelling and long-duration demand opportunity for nickel alloys in advanced reactor component manufacturing. Both conventional large-scale light water reactors (LWRs) and next-generation small modular reactors (SMRs) require significant quantities of nickel alloys for reactor vessel internals, steam generators, heat exchangers, primary coolant piping, and control rod drive mechanisms, applications demanding exceptional resistance to radiation-induced embrittlement, high-temperature corrosion, and stress corrosion cracking. The World Nuclear Association (WNA) reports that over 60 nuclear reactors were under active construction globally as of 2024, with more than 100 additional units in advanced planning or licensing stages across China, India, South Korea, France, and the United States. The U.S. Department of Energy (DOE) has designated advanced nuclear, including SMR concepts from TerraPower, X-energy, and NuScale, as a national priority, with significant federal funding allocated under the Inflation Reduction Act and the ADVANCE Act of 2024. Each reactor unit represents a multi-decade demand commitment for high-performance nickel alloy components, providing alloy producers with long-cycle, high-margin revenue visibility through the forecast period and beyond.

Category-wise Analysis

Product Type Insights

Heat-Resistant Nickel Alloys, commonly referred to as nickel superalloys, dominated the global Nickel Alloy Market by product type, accounting for approximately 42% of total market share in 2025. This commanding leadership position reflects the irreplaceable role of nickel superalloys in the world’s most demanding high-temperature engineering environments, most critically, the hot sections of jet turbine engines and industrial gas turbines, where no competing material can match the combination of high-temperature strength, creep resistance, oxidation resistance, and fatigue performance that nickel superalloys deliver. Specific alloys such as Inconel 718, Inconel 625, Waspaloy, René 41, and Haynes 282 are extensively consumed by leading aerospace engine OEMs including GE Aerospace, Pratt & Whitney, and Rolls-Royce, as well as industrial gas turbine manufacturers including Siemens Energy and Mitsubishi Power. Corrosion-Resistant Nickel Alloys represent the fastest-growing product type segment, supported by expanding oil and gas upstream investment and growing hydrogen infrastructure development.

Composition Insights

The Ni-Cr-Fe (Nickel-Chromium-Iron) composition group led the global Nickel Alloy Market by alloy composition, capturing approximately 38% of total market share in 2025. Ni-Cr-Fe alloys, including the commercially dominant Inconel 600, Inconel 625, and Incoloy 800/825 series, occupy a uniquely broad application range spanning high-temperature heat exchangers, chemical processing equipment, nuclear steam generator tubing, and aerospace structural components. The chromium content in these alloys provides exceptional oxidation and corrosion resistance, while the iron component moderates raw material cost compared to higher-nickel-content grades, making Ni-Cr-Fe alloys the most commercially versatile and volume-significant composition class within the nickel alloy market. Their compatibility with a wide range of fabrication processes, including hot rolling, cold drawing, forging, and welding, further underpins their dominant specification preference across diverse industrial end-uses. The Ni-Cr-Mo composition group is the fastest-growing segment, driven by its critical role in corrosion-intensive chemical processing and offshore oil and gas applications.

Industry Analysis

Aerospace & Defense dominated the global Nickel Alloy Market by Industry, representing approximately 35% of total market share in 2025. The segment’s leadership is a direct function of the aerospace industry’s uncompromising material performance requirements and the unique fitness-for-purpose of nickel superalloys in jet propulsion systems. Each modern commercial turbofan engine, such as the CFM LEAP or Pratt & Whitney GTF, contains hundreds of individual nickel superalloy components that must maintain structural integrity for tens of thousands of flight hours under extreme temperature and mechanical loading conditions. The combined Boeing and Airbus aircraft order backlog exceeding 13,000 units ensures a structurally durable, decade-long demand pipeline for aerospace nickel alloy producers. In defense applications, nickel alloys are extensively used in military jet engines, gas turbine-powered naval vessels, and missile propulsion systems across NATO and allied nations that are collectively increasing defense budgets in response to evolving geopolitical dynamics. The Power Generation end-use segment is the fastest-growing, driven by global investment in gas turbine combined cycle power plants and next-generation nuclear reactor programs.

Regional Insights

North America Nickel Alloy Market Trends and Insights

North America leads the global Nickel Alloy Market, holding approximately 32% of total market share in 2025, driven by the region’s dominant aerospace manufacturing ecosystem, substantial defense industrial base, and growing energy sector investment. The United States is the primary regional demand hub, anchored by the concentration of world-class aerospace engine OEMs, including GE Aerospace (headquartered in Cincinnati, Ohio), Pratt & Whitney (a RTX Corporation subsidiary), and the Boeing commercial and defense supply chain, all of which depend on domestic and allied nickel alloy suppliers for critical engine and structural component materials. Key nickel alloy producers including Carpenter Technology Corporation, ATI Specialty Materials (now part of Allegheny Technologies Incorporated), Haynes International, and Precision Castparts Corp maintain significant manufacturing capacity in the United States, serving both domestic aerospace demand and global export markets.

The U.S. regulatory and policy environment is actively reinforcing domestic nickel alloy supply chain resilience. The U.S. Department of Defense (DoD) has identified specialty metals, including nickel superalloys, as critical materials under the Defense Production Act, with Title III programs funding domestic capacity expansion for aerospace-grade alloy production. The ADVANCE Act of 2024 and the DOE’s advanced nuclear deployment agenda are creating new long-term demand commitments for nickel alloys in SMR and advanced reactor construction programs. Canada contributes meaningful regional supply through its substantial nickel mining and primary production capacity, with Vale’s Canadian operations and Glencore’s Sudbury-area assets providing upstream raw material security for North American alloy producers.

Europe Nickel Alloy Market Trends and Insights

Europe represents the second-largest regional market for nickel alloys, sustained by the region’s world-class aerospace manufacturing and MRO ecosystems, sophisticated chemical processing industries, and significant oil and gas production and infrastructure assets in the North Sea and Mediterranean basins. Germany is the largest national market, home to major turbine manufacturers including Siemens Energy and MTU Aero Engines, as well as a deep precision manufacturing supply chain serving Airbus and its engine partners. France, through Airbus, Safran, and Thales, is a major consumer of aerospace-grade nickel superalloys, while the United Kingdom hosts Rolls-Royce, one of the world’s three leading commercial jet engine manufacturers, whose broad turbine alloy consumption spans advanced nickel superalloy grades. VDM Metals (a Acerinox Group subsidiary), headquartered in Germany, and Aperam SA are among the key European nickel alloy producers serving the region’s diversified industrial demand.

The European regulatory and policy environment is creating new structural demand vectors for nickel alloys through the EU Green Deal, REPowerEU energy security program, and national hydrogen strategies. France’s commitment to constructing 14 new EPR2 nuclear reactors, announced by President Macron in 2022 and progressing through regulatory approval, represents a significant long-cycle nickel alloy demand commitment for reactor vessel, steam generator, and primary loop piping components. The EU Critical Raw Materials Act, which classifies nickel as a strategic raw material, is stimulating investment in European supply chain resilience, supporting domestic production expansion by European alloy producers. Spain’s growing offshore wind and green hydrogen infrastructure investment is also creating incremental demand for corrosion-resistant nickel alloys in marine-environment equipment.

Asia Pacific Nickel Alloy Market Trends and Insights

Asia Pacific is the fastest-growing regional market for nickel alloys, expected to register a CAGR of approximately 6.5% through 2033, significantly above the global average, driven by China’s rapidly expanding commercial aviation fleet and aerospace manufacturing ambition, Japan’s advanced industrial base, India’s growing defense modernization program, and the broader region’s sustained economic growth supporting power generation and chemical processing investment. China is the dominant and fastest-growing national market, with the Commercial Aircraft Corporation of China (COMAC) advancing domestic narrow-body and wide-body aircraft development, including the C919 and CR929 programs, that will progressively create domestic demand for aerospace-grade nickel superalloys as production scales. China’s state-owned nickel alloy producers, including enterprises under the AECC (Aero Engine Corporation of China) umbrella, are investing heavily in superalloy manufacturing capability to serve domestic aviation and defense programs, reducing dependence on imported Western alloys.

Japan maintains a sophisticated nickel alloy production and consumption base, with Nippon Steel and downstream specialty alloy producers serving both domestic aerospace component manufacturing, including supply into IHI Corporation’s and Kawasaki Heavy Industries’ jet engine programs, and the country’s world-leading chemical and petrochemical industries. India is an emerging high-potential market, with the Indian Air Force’s fleet modernization program, the DRDO’s advanced propulsion development initiatives, and ISRO’s space launch vehicle programs generating growing demand for high-performance nickel superalloy components. The Make in India initiative and defense indigenization mandates are stimulating domestic nickel alloy processing investment. Across ASEAN, expanding petrochemical complex construction in Singapore, Malaysia, and Thailand is creating incremental demand for corrosion-resistant nickel alloy process equipment and piping systems.

Competitive Landscape

The global Nickel Alloy Market demonstrates moderate consolidation, with a concentrated group of vertically integrated specialty materials producers controlling the high-margin aerospace and superalloy segments, while a wider base of regional manufacturers competes in industrial and corrosion-resistant grades. Entry barriers are elevated due to stringent aerospace qualification cycles, metallurgical complexity, and capital-intensive melting and refining infrastructure. Long-term supply agreements with engine OEMs and aerospace primes create structural demand visibility and reinforce incumbent positioning.

Competitive strategies emphasize expansion of vacuum induction and vacuum arc remelting capacity, development of additive manufacturing-compatible powders, and qualification of next-generation alloys for hydrogen, advanced nuclear, and high-efficiency turbine applications. Producers are also strengthening backward integration into raw materials and enhancing process control to ensure traceability and performance consistency. Portfolio diversification across aerospace, energy, and chemical processing markets helps mitigate cyclicality, while technical collaboration with OEMs supports early-stage material specification and long-duration program alignment.

Key Developments:

- February 2025: Carpenter Technology Corporation announced a significant capacity expansion of its premium vacuum arc remelting (VAR) and electroslag remelting (ESR) facilities in Reading, Pennsylvania, targeting increased output of aerospace-grade nickel superalloy billet to address structural supply shortfalls driven by recovering jet engine production demand from GE Aerospace and Pratt & Whitney.

- September 2024: Haynes International reported successful qualification of its HAYNES 282 nickel superalloy for use in next-generation small modular reactor (SMR) high-temperature component applications, following extended testing in collaboration with a U.S. Department of Energy-funded advanced nuclear materials program, marking a key milestone in expanding the company’s presence in the emerging nuclear energy materials sector.

- March 2023: ATI (Allegheny Technologies Incorporated) completed the strategic divestiture of its stainless steel and specialty alloys flat-rolled products segment to focus exclusively on its high-value nickel superalloy, titanium, and advanced specialty materials businesses, sharpening its competitive positioning as a pure-play advanced materials supplier to the global aerospace, defense, and energy markets.

Companies Covered in Nickel Alloy Market

- PJSC Mining & Metallurgical Co. Norilsk Nickel

- Haynes International, Inc.

- Nippon Steel Corporation

- Aperam SA

- Carpenter Technology Corporation

- Thyssenkrupp AG

- VDM Metals GmbH (Acerinox Group)

- ATI Specialty Materials (Allegheny Technologies Incorporated)

- Precision Castparts Corp.

- Allegheny Technologies Incorporated (ATI)

- Special Metals Corporation (PCC Group)

- Rolled Alloys, Inc.

- Voestalpine High Performance Metals

- Proterial, Ltd.

- Doncasters Group

Frequently Asked Questions

The market is projected to reach US$ 13.0 billion in 2026, supported by aerospace recovery and steady oil and gas investment.

Demand is driven by commercial aircraft production growth and the need for corrosion-resistant alloys in oil, gas, and chemical processing.

North America leads with around 32% share, supported by strong aerospace manufacturing and advanced alloy production capacity.

Key opportunities include hydrogen infrastructure development and expanding advanced nuclear and SMR programs.

Major players include Haynes International, Carpenter Technology, ATI, Precision Castparts, VDM Metals, Aperam, Nippon Steel, and others.