- Beverages

- NFC Juice Market

NFC Juice Market Size, Share, and Growth Forecast, 2026 - 2033

NFC Juice Market by Product Type (Fresh fruits, Fresh vegetables, Blends), Applications (Non-alcoholic, Alcoholic, Bakery & Confectionery, Dairy & Frozen Desserts), and Regional Analysis 2026 - 2033

NFC Juice Market Size and Trends Analysis

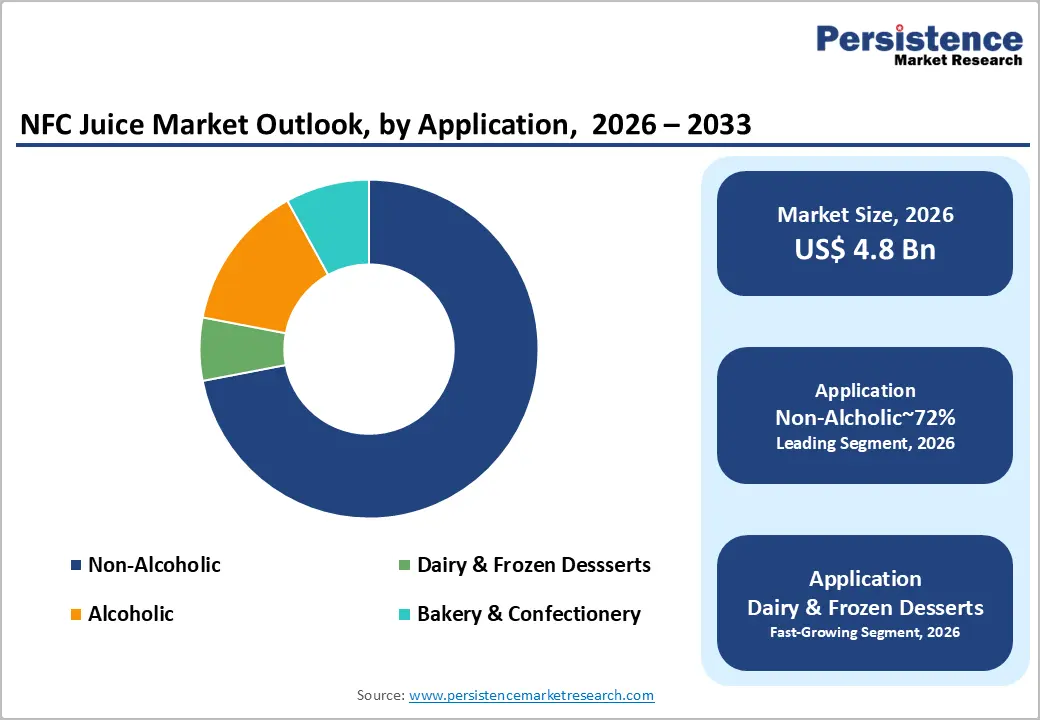

The global NFC juice market size is likely to be valued at US$4.8 billion in 2026 and is expected to reach US$7.4 billion by 2033, growing at a CAGR of 6.3% during the forecast period from 2026 to 2033, driven by increasing consumer preference for natural, minimally processed beverages, as health-conscious individuals shift away from pasteurized options.

This trend is strengthening demand for additive-free fruit and vegetable juices across retail channels. Improvements in cold-chain logistics are supporting product quality and freshness, while expanding distribution channels are enhancing accessibility among diverse consumer segments. Advancements in cold-pressing and high-pressure processing technologies are also extending shelf life while preserving nutritional integrity, positioning the market for steady growth across non-alcoholic applications and emerging blended juice categories.

Key Industry Highlights:

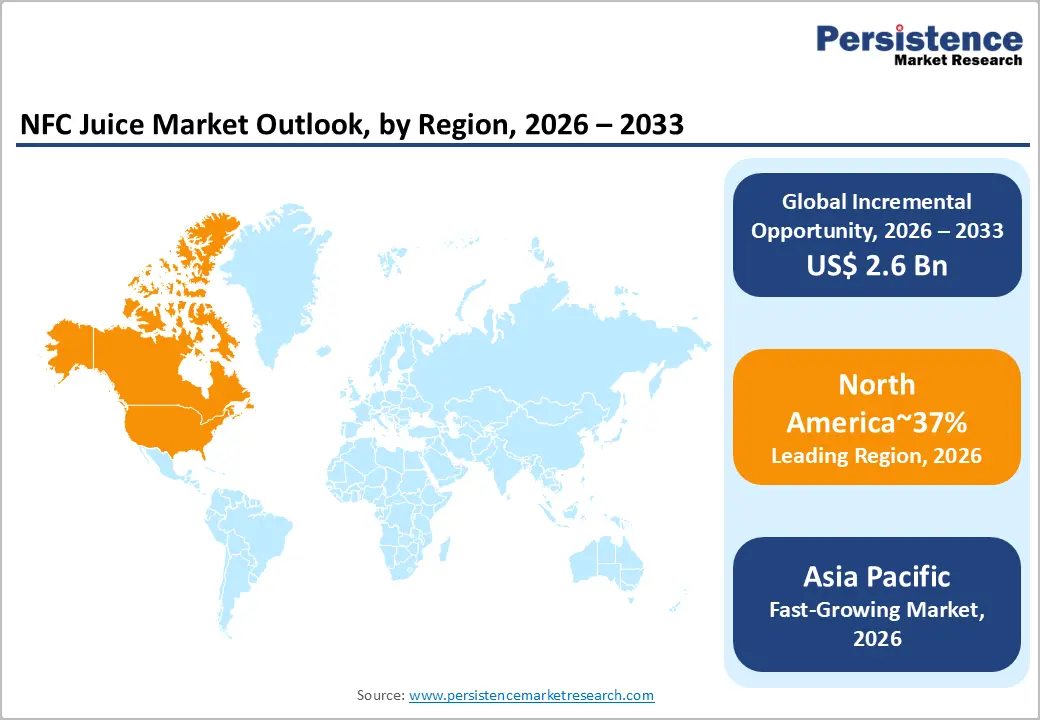

- Leading Region: North America is projected to lead, accounting for approximately 37% share in 2026, supported by mature retail networks, strong premium beverage distribution, and established cold-chain logistics.

- Fastest-growing Region: Asia Pacific is anticipated to grow fastest, driven by urbanization, rising disposable incomes, and expanding health food retail channels.

- Leading Product Type: Fresh fruit is expected to lead, accounting for approximately 64% share in 2026, anchored by strong consumer familiarity and traditional breakfast consumption habits.

- Leading Application: The non-alcoholic segment is anticipated to dominate, accounting for approximately 72% share in 2026, anchored by everyday hydration needs, retail shelf presence, and low-alcohol trend avoidance.

| Key Insights | Details |

|---|---|

| NFC Juice Market Size (2026E) | US$4.8 Bn |

| Market Value Forecast (2033F) | US$7.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.8% |

DRO Analysis

Driver Analysis - Evolution of Health-Conscious Consumption Patterns

Rising awareness of adverse effects from artificial additives increases demand for natural beverage formulations globally. Consumers prioritize transparent labeling and minimally processed ingredients across daily dietary consumption patterns. This behavioral shift compels manufacturers to expand premium juice portfolios aligned with clean-label expectations. Health-focused lifestyles accelerate transition from concentrate-based beverages toward pure liquid extraction alternatives. Perceived nutritional superiority of not-from-concentrate methods reinforces sustained consumer preference across retail channels. Regulatory emphasis on ingredient disclosure further strengthens adoption of natural beverage categories. These dynamics collectively support consistent procurement growth within premium, health-oriented beverage markets.

PepsiCo’s Tropicana Rise & Shine aligns with demand for pure juice offerings derived from minimally processed fruit sources. Advanced cold-pressed technologies preserve biological integrity and nutritional value within beverage formulations. Supply chain participants integrate such processing methods to maintain quality and extend product differentiation. Retail positioning emphasizes wellness attributes and ingredient transparency to attract health-conscious consumers. Distribution networks expand availability across urban markets with high demand for premium beverages. These interdependencies reinforce valuation growth within the clean-label beverage segment.

Health Wellness Integration in Natural Beverage Consumption

Dietary trends emphasizing natural hydration accelerate adoption of not-from-concentrate juices within daily consumption routines globally. Wellness programs integrate these beverages to support sugar reduction targets without compromising sensory appeal. Manufacturers adapt formulations to incorporate functional attributes such as immunity and digestive health support. This evolving demand strengthens positioning of premium juices within broader non-alcoholic beverage categories. Regulatory validation of health claims reinforces consumer confidence in functional beverage offerings. Cost structures shift toward fortified ingredient sourcing and advanced processing technologies ensuring product integrity. These dynamics collectively sustain rising procurement volumes across health-focused beverage segments.

Distribution strategies expand across fitness centers and digital retail platforms targeting active consumer demographics. Product portfolios emphasize verified health certifications to strengthen credibility within competitive beverage markets. E-commerce integration enables direct engagement and consistent supply access for repeat consumers. Manufacturers refine formulations to balance functionality with taste consistency across product lines. These interdependencies reinforce sustained demand within premium, wellness-integrated beverage ecosystems.

Restraint Analysis - Complexity and High Cost of Cold-Chain Logistics

Maintaining controlled temperature environments imposes substantial financial burdens across beverage production and distribution systems globally. Perishable liquid products require continuous refrigeration from extraction through storage and final retail consumption stages. Elevated energy consumption and equipment maintenance costs significantly increase overall product pricing structures. These logistical demands limit participation of smaller vendors lacking access to advanced cold-chain infrastructure. Entry barriers rise as capital requirements for refrigerated logistics and storage systems intensify across markets. Regulatory standards for food safety further mandate strict temperature compliance throughout supply chains. These factors collectively constrain scalability and profitability within premium beverage distribution ecosystems.

Florida's Natural Growers with Florida's Natural Orange Juice operates within complex cold-chain systems to preserve freshness and product integrity. Distribution inefficiencies in developing regions lead to higher spoilage rates and inconsistent quality outcomes. Limited cold-storage infrastructure restricts penetration into rural and lower-income markets globally. Logistics constraints increase operational complexity and extend delivery timelines across fragmented supply networks. Cost pressures influence pricing strategies, reducing accessibility for price-sensitive consumer segments. These interdependencies collectively limit broader adoption of fresh, premium juice products across diverse geographic regions.

Short Shelf Life Logistics in Fresh Juice Distribution

Perishable characteristics of unpasteurized juices impose stringent cold-chain requirements across complex distribution networks globally. Temperature fluctuations rapidly degrade product quality, limiting viable transport distances and retailer acceptance thresholds. Producers incur elevated logistics costs, compressing margins within highly competitive beverage pricing environments. This structural limitation restricts expansion into remote and infrastructure-constrained markets with inconsistent refrigeration capabilities. Inventory planning becomes challenging due to shortened shelf life and unpredictable demand fluctuations. Regulatory compliance on freshness and safety standards further intensifies operational constraints across supply chains. These factors collectively hinder scalability and consistent market penetration for fresh juice producers.

Odwalla’s Superfood Blends illustrates challenges associated with maintaining product integrity across extended distribution channels. Retailers increasingly prioritize longer shelf-life alternatives to reduce spoilage risks and inventory losses. Demand volatility emerges as seasonal shifts influence purchasing decisions and stocking strategies. Producers face commercial impacts including inventory write-offs and reduced order frequency from cautious distributors. Supply chain reliability concerns extend procurement cycles and disrupt consistent replenishment patterns. These interdependencies constrain growth potential within premium fresh juice segments.

Opportunity Analysis - Digital Transformation and E-commerce Subscription Models

Rapid expansion of online grocery platforms creates direct consumer access channels for premium fresh beverage products globally. Subscription-based delivery models ensure consistent supply while stabilizing demand patterns among time-constrained households. E-commerce ecosystems enable niche brands to scale reach without dependence on physical retail infrastructure networks. Direct-to-consumer strategies enhance data capture, supporting personalized marketing and targeted engagement initiatives. Advanced analytics optimize inventory planning and reduce perishable waste across distribution cycles. Integrated logistics frameworks support cold-chain compliance within last-mile delivery systems. These dynamics collectively accelerate adoption of premium juice products within digitally enabled consumption environments.

Evolution Fresh’s Evolution Fresh Cold-Pressed Juice leverages digital channels to strengthen customer retention and brand engagement. Data-driven insights refine product offerings aligned with consumer health and wellness preferences. Targeted advertising strategies improve conversion rates across defined demographic segments within online ecosystems. Cold-chain enabled home delivery overcomes traditional distribution constraints for perishable beverage categories. Platform integration enhances operational efficiency across order fulfillment and customer interaction workflows. These interdependencies reinforce sustained growth of subscription-based premium beverage consumption models.

Functional Beverage Formulations in Wellness Segments

Emerging demand for immunity-support beverages accelerates development of not-from-concentrate blends enriched with probiotics. Policy alignment toward natural fortification encourages innovation across vegetable and fruit-based beverage combinations. Advancements in stabilization technologies extend product viability while preserving nutritional integrity without thermal processing methods. This convergence enables premium pricing strategies within health-focused retail and wellness distribution channels. Regulatory validation of functional claims strengthens consumer confidence and supports differentiated product positioning. Cost structures evolve toward advanced processing and bioactive ingredient integration within beverage manufacturing systems. These factors collectively expand opportunities within premium functional beverage ecosystems.

Manufacturers leverage partnerships to introduce co-branded offerings aligned with wellness-focused consumer demand patterns. Product portfolios expand shelf presence across retail and digital channels emphasizing health-oriented positioning. Clinically supported claims enhance credibility and reinforce repeat purchasing behavior among targeted demographics. Distribution strategies integrate fitness and specialty health outlets to maximize consumer reach. These interdependencies strengthen market positioning and sustained growth within functional beverage categories.

Category-wise Analysis

Product Type Insights

Fresh fruit is expected to lead, accounting for approximately 64% share in 2026, underpinned by the widespread availability of citrus and pome varieties. Traditional consumption patterns prioritize pure fruit extracts during morning meal occasions across global households. This segment benefits from a deep-rooted consumer perception of fruit as a primary source of essential vitamins. Manufacturers focus on preserving the natural fiber and enzymatic content of fruits through cold extraction. PepsiCo with Tropicana Pure Premium and The Coca-Cola Company with Simply Orange reinforce this market leadership through extensive retail presence. Adoption remains anchored in the desire for authentic taste profiles that mimic fresh-squeezed fruit. Ongoing improvements in extraction efficiency help maintain competitive pricing for high-volume fruit juice lines. This convergence of consumer trust and established supply chains sustains the dominance of the fruit segment.

Blend is anticipated to be the fastest growing segment, driven by increasing consumer demand for diverse flavor profiles and enhanced nutritional density. Combining various fruit and vegetable extracts allows manufacturers to balance acidity and sweetness without using artificial additives. Suja Juice with Vibrant Probiotic Blend, Evolution Fresh with Organic Defense Blend, and Pressed Juicery with Wellness Blend demonstrate this shift through innovative layering techniques. This culinary innovation addresses the growing appetite for exotic and complex taste experiences among urban demographics. Integration of superfruits and nutrient-rich vegetables supports a broader range of health-focused product claims. As wellness-oriented buyers seek comprehensive nutritional support, blended juices are gaining traction across premium retail channels. These sophisticated formulations enable brands to target specific functional needs such as immunity and digestive health. This structural shift toward variety and functionality accelerates the expansion of the blended category.

Application Insights

Non-alcoholic is projected to dominate, accounting for approximately 72% share in 2026, reinforced by the universal demand for healthy hydration and meal accompaniments. This application remains the primary driver of high-volume procurement in both retail and foodservice sectors. The global movement toward reducing alcohol consumption further expands the addressable market for premium juice alternatives. Consumers increasingly utilize fresh juices as a base for smoothies and functional mocktails in home environments. Florida's Natural with Florida's Natural Orange Juice and Ocean Spray with Pure Cranberry are deeply embedded in these daily consumption rituals. Strategic placement in breakfast menus and health-focused cafes bolsters consistent utilization across diverse age groups. High penetration in school lunch programs and workplace cafeterias ensures stable demand throughout the year. This established alignment with daily lifestyle needs secures the segment's leading position.

Dairy & frozen desserts are anticipated to be the fastest-growing segment, driven by the expanding use of natural ingredients in artisanal food production. Manufacturers are shifting away from synthetic flavorings to meet the clean-label expectations of modern consumers. Incorporating pure juice extracts into ice creams and yogurts enhances the authentic fruit profile of these treats. Dohler with NFC Fruit Solutions and Louis Dreyfus Company with LDC NFC Juices provide high-quality ingredients for these specialized food applications. This trend is set to accelerate as premium dessert brands prioritize ingredient transparency and natural sourcing. The utilization of not-from-concentrate juices also serves as a natural coloring agent, eliminating the need for artificial dyes. Ongoing innovation in plant-based dairy alternatives further increases the demand for high-quality fruit bases. This growing integration into value-added food segments represents a significant momentum shift for the industry.

Regional Insights

North America NFC Juice Market Trends

North America is expected to remain the leading regional market, accounting for approximately 37% share in 2026, supported by high consumer awareness regarding minimally processed foods. The region's market dominance is anchored in a sophisticated retail landscape that prioritizes premium, clean-label beverage offerings. Established cold-chain infrastructure ensures the consistent delivery of perishable products from processing hubs to diverse urban centers. Health-conscious consumption patterns reinforce the transition away from high-sugar, concentrate-based alternatives. Subscription-based grocery services further expand the reach of fresh liquid products across suburban demographics. This regional environment is projected to maintain a stable demand for high-quality juice extracts.

The U.S. is anticipated to lead regional momentum through sustained consumer preference for transparently labeled and nutrient-dense hydration options. High per capita income levels support the premium pricing associated with not-from-concentrate extraction methods. The Coca-Cola Company with Simply Orange remains a dominant presence within the domestic retail sector. Regulatory focus on reducing added sugars in beverages encourages manufacturers to promote pure fruit and vegetable alternatives. Robust investment in high-pressure processing facilities strengthens the local production capacity for fresh juices. This alignment between health trends and industrial capability continues to drive market expansion.

Europe NFC Juice Market Trends

Europe is expected to remain a mature and structurally stable regional market, with demand primarily anchored in strict labeling regulations and premiumization. The region's market structure is characterized by a strong consumer preference for organic and ethically sourced beverage products. Stringent EU standards regarding food safety and ingredient transparency compel manufacturers to maintain high production quality. Adoption remains anchored in a well-developed network of specialty health stores and organic supermarkets. Premium juice brands utilize sustainable packaging to appeal to environmentally conscious demographics. This regulatory and cultural environment sustains a consistent valuation for the premium juice sector.

Germany is expected to anchor regional growth through increasing demand for functional and immunity-boosting beverage profiles. Consumers in this nation demonstrate a high willingness to invest in liquid products with certified health benefits. Eckes-Granini with Granini Selection addresses the local appetite for premium fruit juice experiences. The expansion of online grocery platforms facilitates the delivery of fresh, cold-pressed juices to busy urban households. Government initiatives promoting balanced diets further bolster the procurement of minimally processed fruit and vegetable extracts. This focus on wellness and convenience is set to drive the domestic market forward.

Asia Pacific NFC Juice Market Trends

Asia Pacific is expected to register the fastest growth trajectory, as rapid urbanization and increasing manufacturing scale accelerate market expansion. The region's growth is anchored in a rising middle class with an increasing appetite for health-conscious and premium lifestyle products. Modernization of traditional retail channels and the proliferation of e-commerce platforms provide new avenues for product distribution. Consumers are increasingly transitioning from carbonated drinks to natural, additive-free beverage alternatives. Ongoing investments in agricultural processing and cold-chain logistics are expected to reduce supply chain bottlenecks. This dynamic regional shift creates a fertile environment for the uptake of fresh juices.

India is expected to lead regional momentum through a burgeoning young population seeking convenient and nutritious hydration solutions. Increasing health consciousness among urban professionals drives the demand for minimally processed, high-quality juice brands. Parle Agro with Frooti continues to expand its reach through innovative packaging and extensive distribution networks. Rising disposable incomes allow for a shift toward more expensive, not-from-concentrate beverage categories. Local manufacturers are poised to integrate traditional regional flavors into modern juice formulations to attract diverse consumer segments. This convergence of demographic trends and retail evolution sustains rapid market acceleration.

Competitive Landscape

The global NFC juice market is moderately consolidated, with leadership concentrated among multinational beverage firms such as PepsiCo and The Coca-Cola Company. These companies exert influence through extensive distribution networks, strong brand equity, and advanced processing capabilities. Their investments in high-pressure processing and cold-chain logistics establish benchmarks for freshness, safety, and nutritional transparency. Global sourcing networks enable consistent raw material availability despite seasonal variability in fruit production. This structure coexists with regional producers addressing localized demand through specialized and fresh product offerings.

Competitive positioning reflects horizontal differentiation across flavors and functional formulations alongside vertical integration in sourcing and processing. Premium participants emphasize organic certifications, clean-label positioning, and sustainable packaging innovations. Companies such as Ocean Spray and Innocent Drinks advance specialized offerings targeting health-focused consumer segments. Industry dynamics include acquisitions of niche brands expanding organic and functional portfolios. Forward-looking strategies prioritize balancing premium quality with ethical sourcing and operational efficiency.

Key Industry Developments:

- In January 2026, The Coca-Cola Company announced a major digital transformation leadership shift to accelerate the adoption of AI across its global supply chain. This move is designed to optimize inventory management and real-time distribution of chilled juices, ensuring higher freshness levels and reducing cold-chain waste.

- In September 2025, Tropicana Products Inc. (Tropicana Brands Group) launched the "Tropicana Essentials" line, a value-positioned orange juice blend fortified with vitamins. By blending orange with apple and pear, the company offers a more affordable NFC entry point that addresses consumer concerns regarding high fruit prices and sugar content.

- In April 2025, Castillo Hermanos entered into a definitive agreement to acquire Harvest Hill Beverage Co. to strengthen its US chilled juice footprint. This acquisition allows the company to localize manufacturing, reducing the "cost-to-serve" in the competitive North American premium NFC juice market.

Companies Covered in NFC Juice Market

- PepsiCo

- The Coca-Cola Company

- Louis Dreyfus Company

- Eckes-Granini

- Dohler

- Ocean Spray

- Citrosuco

- Suntory

- Innocent Drinks

- Bolthouse Farms

- Florida's Natural

- Del Monte Foods

- Suja Juice

- Pressed Juicery

- Evolution Fresh

- Biotta

Frequently Asked Questions

The global NFC juice market is projected to be valued at US$4.8 billion in 2026 and is expected to reach US$7.4 billion by 2033, driven by rising consumer preference for natural, additive-free beverages and improvements in cold-chain logistics.

Increasing awareness of the adverse effects of artificial additives compels consumers to choose minimally processed, clean-label beverages, which encourages manufacturers to expand premium portfolios and adopt high-pressure and cold-press processing technologies.

The NFC juice market is forecast to grow at a CAGR of 6.3% from 2026 to 2033, reflecting increasing adoption across non-alcoholic applications and expanding distribution through retail and digital channels.

Asia Pacific is expected to register the fastest growth, driven by rapid urbanization, rising disposable incomes, modernization of retail networks, and growing consumer demand for health-oriented beverages.

The NFC juice market is moderately consolidated, with leading players including PepsiCo with Tropicana, The Coca-Cola Company with Simply Orange, Florida's Natural Orange Juice, Suja Juice, and Evolution Fresh, competing through advanced processing, cold-chain logistics, and premium product positioning.