- Off-Road Equipment & Machinery

- Mobile Crushers and Screeners Market

Mobile Crushers and Screeners Market Size, Share, and Growth Forecast 2026 - 2033

Mobile Crushers and Screeners Market by Product Type (Mobile Crushers: Jaw Crushers, Cone Crushers, Impact Crushers, Others; Mobile Screeners: Scalping Screeners, Inclined Screeners, Trommel Screeners), Capacity (Below 200 TPH, 200-500 TPH, Above 500 TPH), Application (Mining, Quarrying, Waste Recycling, Road & Infrastructure), and Regional Analysis, 2026 - 2033

Mobile Crushers and Screeners Market Size and Trend Analysis

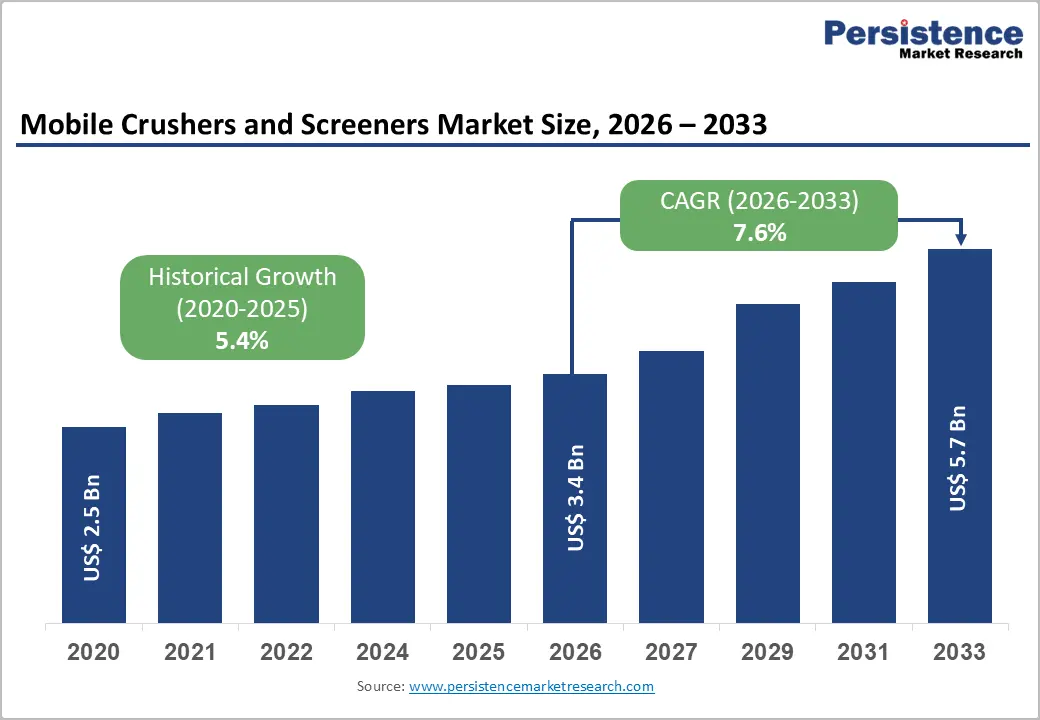

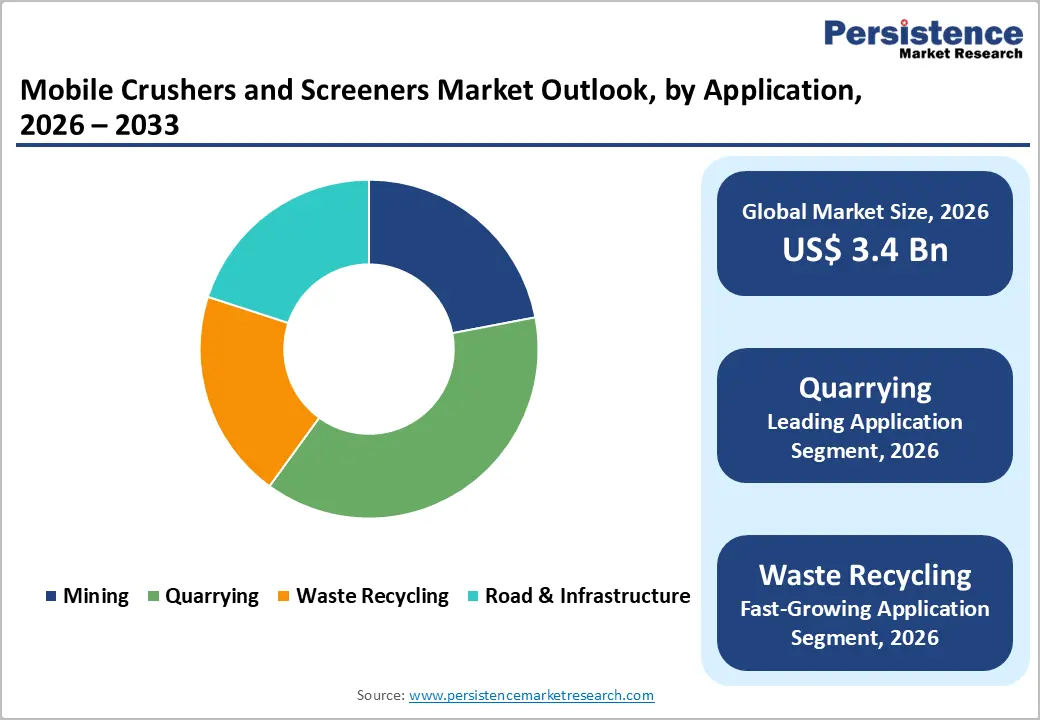

The global mobile crushers and screeners market size is expected to reach US$ 3.4 billion in 2026 and is projected to reach US$ 5.7 billion by 2033, growing at a CAGR of 7.6% between 2026 and 2033. This robust trajectory is driven by accelerating global infrastructure investment, a marked shift toward on-site material processing to reduce haulage costs and carbon footprints, and surging demand from waste recycling and road construction applications.

The market expanded from US$ 2.5 billion in 2020, with a historical CAGR of 5.4%, supported by large-scale mining activity in the Asia Pacific and sustained quarrying demand across North America and Europe.

Key Industry Highlights

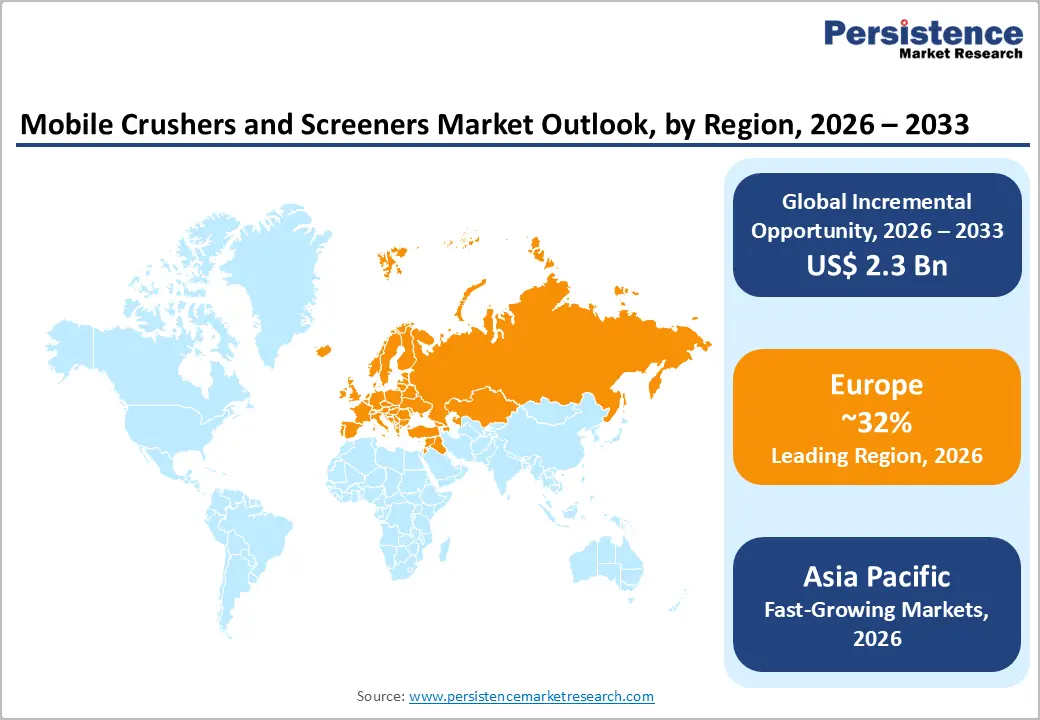

- Leading Region: Europe holds 32% of the global mobile crushers and screeners market share in 2025, driven by stringent C&D recycling mandates, active quarrying industries across the UK, Germany, and Scandinavia, and rapid adoption of electrified processing equipment.

- Fastest Growing Region: Asia Pacific is the fastest growing region at 9.2% CAGR (2026 - 2033), underpinned by India's US$ 1.4 trillion infrastructure pipeline, China's quarrying demand, and expanding mining activity in Australia and Southeast Asia.

- Dominant Product Type: Mobile crushers command 65% market share in 2025, with jaw crushers as the leading sub-type owing to their mechanical reliability, 4:1-9:1 reduction ratios, and versatility across primary crushing in quarrying, mining, and infrastructure applications.

- Fastest-Growing Application: Waste recycling is the fastest-growing application segment, driven by EU mandates requiring 70% C&D waste recovery rates and U.S. EPA estimates of over 600 million tonnes of annual demolition debris, fueling demand for mobile impactors and trommel screens.

- Key Opportunity: Electric and hybrid-powered mobile crushers present the highest growth opportunity, with European Commission zero-emission construction site targets by 2035 compelling fleet operators to upgrade to battery-electric and plug-in hybrid mobile processing solutions.

Market Dynamics

Drivers - Surge in Global Infrastructure Development and Road Construction Activity

Massive public infrastructure investment programs worldwide are directly fueling demand for mobile crushing and screening equipment. The U.S. Infrastructure Investment and Jobs Act allocated US$ 1.2 trillion to transportation, roads, and related infrastructure, while the European Union's Trans-European Transport Network (TEN-T) program continues channeling hundreds of billions of euros into road and rail expansion.

In Asia, India's National Infrastructure Pipeline (NIP), targeting US$ 1.4 trillion in infrastructure spending by 2025, has substantially increased aggregate and crushed stone demand. Mobile crushers and screeners, enabling on-site material processing at project locations, are ideally suited to the scale and geographic dispersion of modern road and infrastructure projects, reducing transportation costs and improving project economics across construction sites globally.

Growing Adoption of Mobile Equipment in Mining and Quarrying Operations

The global mining industry's transition toward in-pit crushing and conveying (IPCC) systems is substantially expanding the addressable market for mobile crushers. According to the World Mining Congress, mobile and semi-mobile crushing solutions reduce mine haulage truck fleets and associated diesel consumption by 20-40%, delivering significant operational cost savings.

Global mineral extraction volumes continue to rise; the U.S. Geological Survey (USGS) reports that world mine production of crushed stone, sand, and gravel exceeds 50 billion tonnes annually, driving relentless demand for high-capacity processing equipment. Mobile cone and jaw crushers designed for hard-rock applications in copper, iron ore, and aggregates mining are experiencing particularly strong order flows from operators seeking flexible, scalable processing solutions adaptable to variable ore body geometries and mine plan changes.

Restraints - High Capital Cost and Maintenance Requirements

Mobile crushers and screeners represent significant capital outlays, with mid-range units typically priced between US$ 250,000 and US$ 1.5 million depending on capacity and configuration. For small and medium quarry operators, who constitute a substantial portion of the buyer base, financing such investments can be prohibitive, particularly in developing markets with limited access to equipment finance. Maintenance costs, including replacement of jaw plates, cone liners, and screen media, can add 15-25% to capital costs annually, further constraining adoption among cost-sensitive operators. These economic barriers slow market penetration in price-sensitive regions, including Sub-Saharan Africa and parts of Southeast Asia.

Stringent Emission Regulations and Transition to Tier 4/Stage V Compliance

Tightening engine emission standards are imposing significant compliance costs on mobile crushing and screening equipment manufacturers and end users. The U.S. EPA Tier 4 Final and EU Stage V non-road mobile machinery (NRMM) standards mandate substantial reductions in NOx and particulate matter emissions from diesel-powered equipment.

Retrofitting or replacing existing fleets to meet these standards requires considerable capital expenditure, and Stage V-compliant engines carry premiums of 10-20% over predecessor Tier 3/Stage IIIB equivalents. In markets where older equipment remains widely deployed, the cost of compliance transition acts as a near-term restraint on fleet renewal and new equipment procurement cycles.

Opportunities - Electrification and Hybrid-Powered Mobile Crushing Solutions

The electrification of mobile crushing and screening equipment represents the most transformative near-term commercial opportunity in the market. Several leading manufacturers have already introduced battery-electric and plug-in hybrid mobile crushers targeting zero-emission construction and quarrying sites. Kleemann GmbH (a Wirtgen Group / John Deere company) launched its MOBICAT MC 110(i) EVO2 electric-capable crusher, while Keestrack NV and RUBBLE MASTER HMH GMBH have introduced full hybrid product lines.

Urban construction and demolition recycling sites, where noise and emission restrictions are tightest, are a primary target market. The European Commission's push toward zero-emission construction sites by 2035 in several member states is compelling fleet operators to actively seek electric-capable alternatives, driving premium product category growth well above market averages through 2033.

Rapid Expansion of Construction and Demolition (C&D) Waste Recycling

Construction and demolition waste recycling is one of the fastest-growing application segments for mobile crushers and screeners globally, offering manufacturers a structurally expanding demand pool driven by circular economy mandates. The European Union's Construction Products Regulation and Waste Framework Directive mandate 70% recycling and recovery rates for non-hazardous C&D waste across member states.

In the U.S., the EPA estimates that C&D debris accounts for over 600 million tonnes of waste annually, more than twice the volume of municipal solid waste. Mobile impactors and trommel screeners capable of processing concrete rubble, asphalt, and mixed debris on-site are experiencing accelerating demand from demolition contractors and recycling operators, making this application one of the highest-growth verticals for mobile processing equipment suppliers through 2033.

Category-wise Analysis

Product Type Insights

Mobile crushers dominate the Product Type category, accounting for approximately 65% market share in 2025, with jaw crushers representing the largest sub-segment within this group. Jaw crushers' dominance stems from their mechanical simplicity, low operating cost, and proven capability to handle a wide range of material hardness, from soft limestone to hard granite, making them the workhorse of quarrying and primary crushing applications globally.

According to Sandvik AB's published technical literature, jaw crushers deliver reduction ratios of 4:1 to 9:1, making them ideal for primary reduction stages. Their robust reliability, low maintenance footprint, and broad compatibility with downstream screening plants ensure that jaw crushers in the mobile crusher category retain a majority of adoption across mining, quarrying, and infrastructure segments, reinforcing the dominance of mobile crushers overall.

Capacity Insights

The 200-500 TPH (tonnes per hour) capacity segment holds the leading position in the Capacity category, representing approximately 44% market share in 2025. This mid-range capacity tier optimally balances throughput performance with equipment mobility, footprint, and capital cost, making it the preferred choice for medium- to large-scale quarry operations, road base production, and recycling applications.

Operators in this segment benefit from the flexibility to service mid-size contracts without committing to the high capital and operational overhead of above-500 TPH mega-units. Major players, including Metso Corporation, Terex Corporation, and Sandvik AB, offer extensive product portfolios in this capacity range, with features such as remote monitoring, automatic setting adjustment, and modular conveyor configurations that enhance operational efficiency and uptime.

Application Insights

Quarrying is the leading application segment, accounting for approximately 38% of the market share in 2025. Quarrying operations require reliable, high-throughput crushing and screening of hard rock aggregates, crushed limestone, granite, and basalt, for use in road construction, concrete production, and railway ballast.

The consistent and recurring nature of quarry production, operating year-round at fixed or semi-fixed sites, generates predictable, high-volume equipment utilization that justifies investment in premium mobile processing units. According to the National Stone, Sand and Gravel Association (NSSGA), the U.S. alone produces approximately 1.5 billion tonnes of crushed stone annually, underscoring the enormous scale of aggregate demand that underpins quarrying's dominance in the mobile crushing and screening equipment market.

Regional Insights

Europe leads the global mobile crushers and screeners market with approximately 32% market share in 2025, supported by its mature quarrying industry, stringent C&D recycling mandates, and strong presence of leading manufacturers. Asia Pacific is the fastest-growing region, projected to record the highest CAGR of approximately 9.2% during 2026 - 2033, driven by infrastructure investment in India, Southeast Asia, and continued mining expansion in Australia and China.

North America Mobile Crushers and Screeners Market Trends and Insights

North America represents a mature but growing market for mobile crushers and screeners, supported by the U.S. Infrastructure Investment and Jobs Act, driving aggregate demand for road and highway construction. The region is witnessing a strong shift toward Tier 4 Final-compliant and hybrid-powered equipment as state-level construction procurement standards tighten. Rental and equipment-as-a-service models are gaining traction, lowering barriers for smaller operators.

U.S. Mobile Crushers and Screeners Market Size

The United States accounts for approximately 79% of the North American market revenue in 2025. Annual crushed stone production exceeding 1.5 billion tonnes per USGS data, combined with US$ 1.2 trillion in federal infrastructure spending commitments, sustains high and growing demand for both primary crushing and screening equipment across quarry, recycling, and infrastructure construction segments.

Europe Mobile Crushers and Screeners Market Trends and Insights

Europe is the leading regional market, driven by active quarrying across Scandinavia, the UK, Germany, and France, and by the world's most stringent C&D waste recycling targets under the EU Waste Framework Directive. Stage V emission compliance requirements are accelerating fleet renewal cycles. Electrification is most advanced in Europe, with multiple manufacturers headquartered in Germany, Austria, and Belgium pioneering hybrid and electric mobile processing equipment.

Germany Mobile Crushers and Screeners Market Size

Germany contributes approximately 20% of European market revenue in 2025, underpinned by its large construction sector and world-leading equipment manufacturing base. Companies, including Kleemann GmbH and Thyssenkrupp AG, drive domestic market activity on both supply and demand sides. Germany's Kreislaufwirtschaftsgesetz (Circular Economy Act) mandates aggressive recycling targets, sustaining strong demand for mobile C&D waste processing equipment.

U.K. Mobile Crushers and Screeners Market Size

The United Kingdom represents approximately 13% of the European market in 2025. The UK Aggregates Levy incentivizes the use of recycled concrete aggregates, directly benefiting mobile crusher and screener adoption in demolition and recycling. Post-Brexit infrastructure programs, including National Highways' road investment strategies, maintain robust aggregate demand, supporting equipment utilization across quarrying and construction applications.

France Mobile Crushers and Screeners Market Size

France accounts for approximately 11% of the European market revenue in 2025. The country's significant public works investment, including the Plan de Relance infrastructure recovery spending, alongside strong aggregate quarrying activity in the limestone-rich Massif Central region, supports consistent demand. France's RE2020 building standards, which encourage the circular use of construction materials, further stimulate the procurement of mobile recycling equipment among demolition and civil engineering contractors.

Asia Pacific Mobile Crushers and Screeners Market Trends and Insights

Asia Pacific is the fastest-growing regional market, supported by large-scale infrastructure construction across India, Southeast Asia, and continued mining output growth in Australia and Indonesia. China remains the largest single national market in the region, with domestic manufacturers Shanghai SANME Mining Machinery Corp. and China ZME Machinery serving extensive domestic quarrying and road construction demand. Government infrastructure programs across the region are generating sustained aggregate processing equipment demand.

India Mobile Crushers and Screeners Market Size

India represents approximately 18% of the Asia Pacific market revenue in 2025. The National Infrastructure Pipeline (NIP), targeting US$ 1.4 trillion in spending, and the Bharatmala Pariyojana highway development program are generating massive aggregate demand. India's rapid urbanization and mineral extraction growth, with iron ore and limestone production among the world's highest, position it as a priority growth market for mobile crushing and screening equipment manufacturers.

Japan Mobile Crushers and Screeners Market Size

Japan contributes approximately 10% of the Asia Pacific market revenue in 2025. Earthquake reconstruction programs, urban renewal projects, and ongoing construction of expressways and Shinkansen expansion corridors generate consistent aggregate demand. Japan's advanced adoption of Tier 4-equivalent emission regulations for non-road equipment encourages uptake of newer, efficient mobile crushing technology. Quarrying of andesite and limestone for domestic concrete production underpins equipment utilization.

Southeast Asia Mobile Crushers and Screeners Market Size

Southeast Asia collectively represents approximately 16% of the Asia Pacific market revenue in 2025. Indonesia, Vietnam, and the Philippines are experiencing rapid infrastructure-led aggregate demand growth. ASEAN's collective infrastructure investment pipeline, valued at over US$ 210 billion annually by the Asian Development Bank (ADB), is driving the adoption of both mid-range and high-capacity mobile processing equipment among domestic and international contractors operating regional construction projects.

Competitive Landscape

The global mobile crushers and screeners market is moderately consolidated, led by established OEMs with strong global footprints and extensive dealer networks. Competition is primarily driven by technology differentiation, product reliability, and the ability to provide integrated solutions, including telematics, remote monitoring, and compliance with evolving emission standards. Modular equipment design enabling flexibility across applications is also emerging as a key competitive factor.

Business strategies are increasingly focused on expanding aftermarket services, which generate stable recurring revenue through spare parts, maintenance, and lifecycle support. Companies are also adopting innovative models such as equipment-as-a-service, rental-based contracts, and digital platforms offering predictive maintenance through IoT integration. Price competition remains intense in emerging markets due to regional manufacturers, while advanced players are leveraging electrification, compact designs, and recycling-focused solutions to capture demand in urban infrastructure and sustainability-driven applications.

Key Developments:

- April 2025: Metso Corporation unveiled its next-generation Lokotrack Urban series of electric-hybrid mobile crushers designed for low-noise, zero-exhaust inner-city demolition and recycling applications, targeting tightening European urban emission zones.

- March 2025: Sandvik unveiled its latest electric crushers and screens, including the QH443E cone crusher, completing its fully electric tracked crushing train and delivering improved sustainability, fuel efficiency, and lower operating costs for mining and quarry applications.

- June 2024: Terex announced the launch of its new MAGNA brand, introducing high-capacity crushing and screening equipment designed for large-scale quarrying, mining, construction, and recycling applications, expanding its portfolio to address higher output and productivity demands.

Companies Covered in Mobile Crushers and Screeners Market

- Market Forecast and Trends

- Competitive Intelligence and Share Analysis

- Growth Factors and Challenges

- Strategic Growth Initiatives

- Pricing Analysis

- Future Opportunities and Revenue Pockets

- Market Analysis Tools

Frequently Asked Questions

The mobile crusher and screeners market is projected to reach US$ 3.4 billion in 2026 and grow to US$ 5.7 billion by 2033 at a CAGR of 7.6%.

Demand is driven by infrastructure investments, mining efficiency improvements, and increasing construction and demolition waste recycling.

Europe leads the market with around 32% share due to strong recycling regulations and a mature quarrying industry.

Key opportunities include electrification of equipment and rising adoption in construction and demolition waste recycling.

Leading players include Metso, Sandvik, Terex, and Astec Industries competing on innovation and aftermarket services.