- Nutraceuticals & Functional Foods

- Millet Snacks Market

Millet Snacks Market Size, Share, and Growth Forecast 2026 - 2033

Millet Snacks Market by Product Type (Chips & Crisps, Puffed Snacks & Extruded Products, Bars & Bites, Bakery-Based Snacks, Others), Distribution Channel (Online, Offline), and Regional Analysis, 2026 - 2033

Millet Snacks Market Share and Trends Analysis

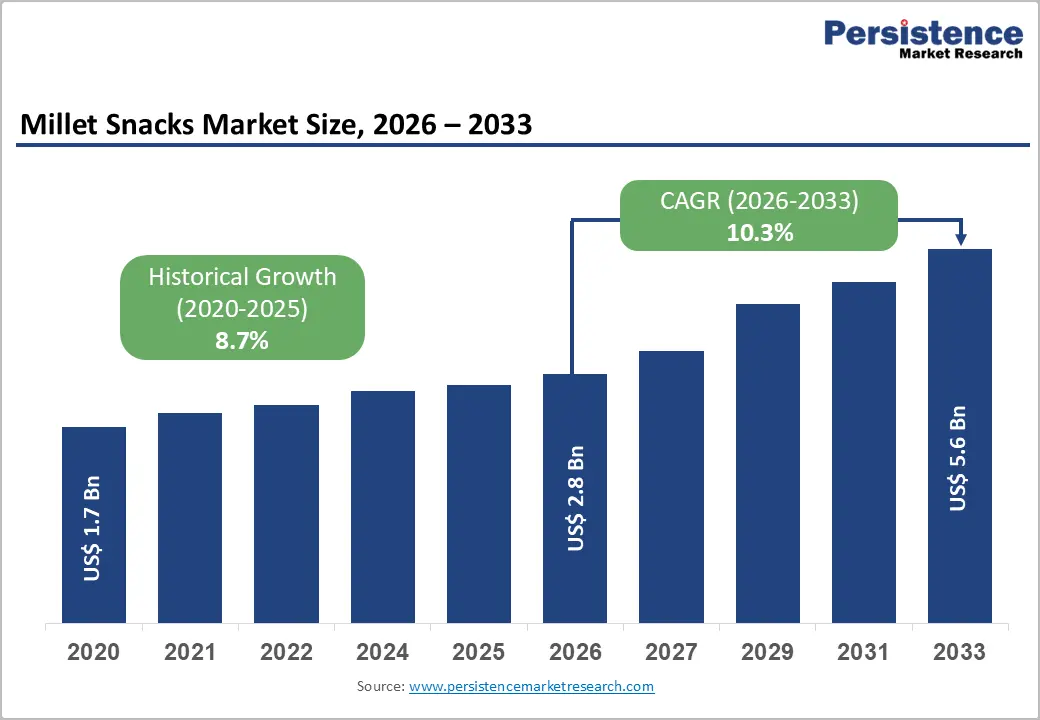

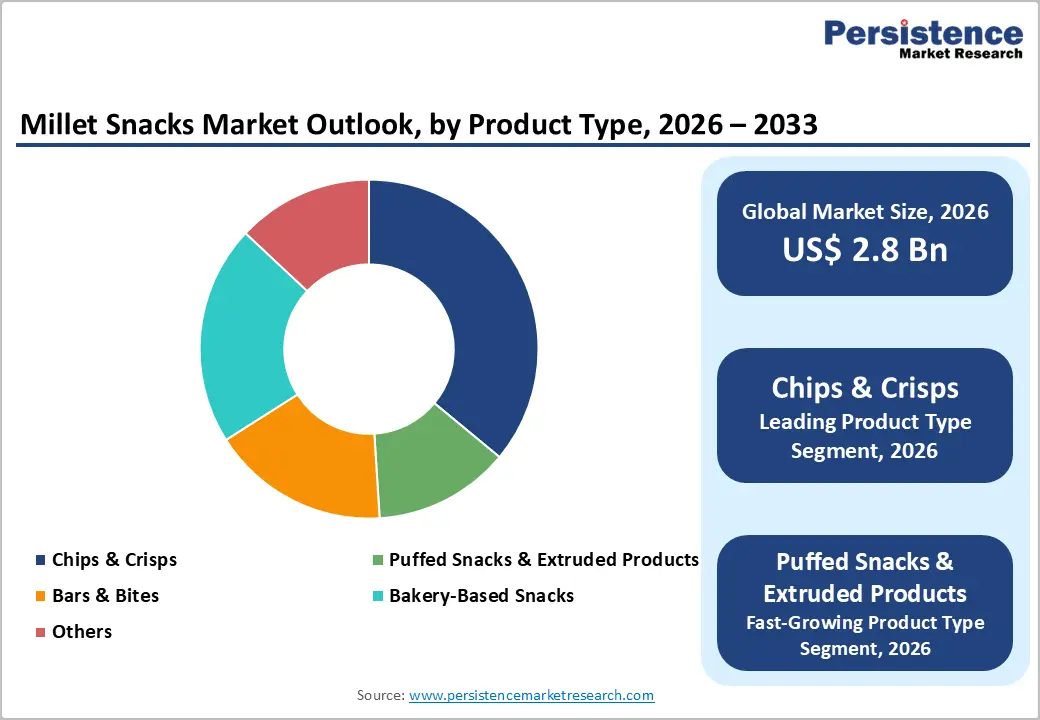

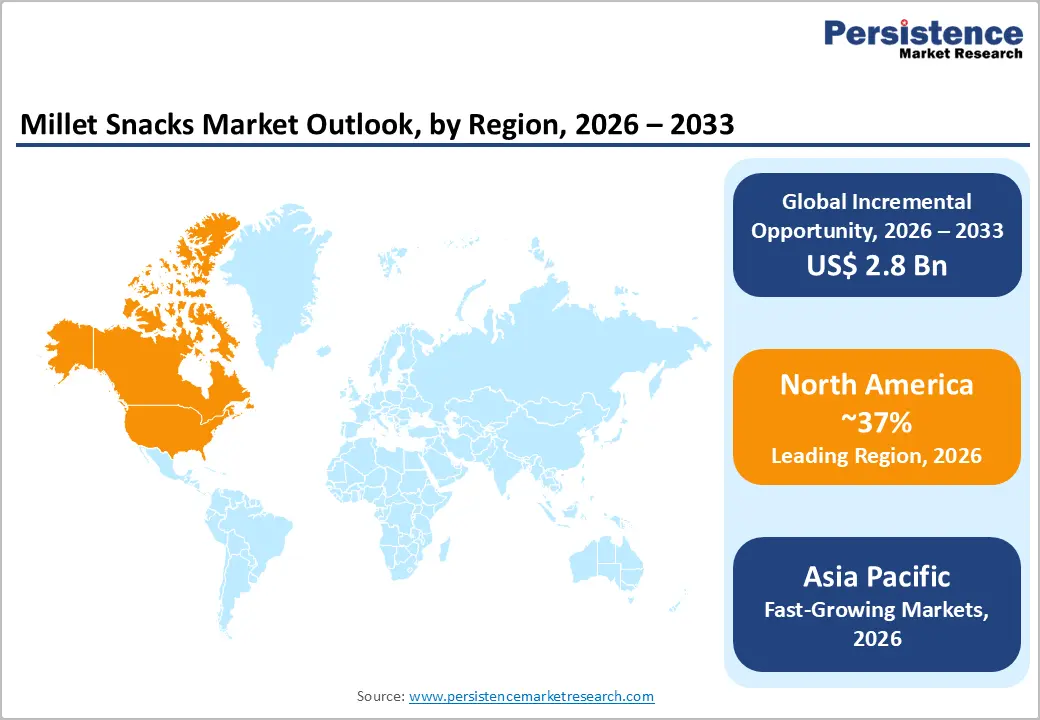

The global millet snacks market size is expected to reach US$ 2.8 billion in 2026 and US$ 5.6 billion by 2033, growing at a CAGR of 10.3% between 2026 and 2033.

The millet snacks market is on a high-growth trajectory underpinned by a powerful convergence of consumer health consciousness, global food security imperatives, and rising demand for gluten-free, high-fiber, and low-glycemic snack alternatives.

The United Nations Food and Agriculture Organization (FAO) designated 2023 as the International Year of Millets, catalyzing government-led promotional campaigns across Asia, Africa, and North America that have substantially elevated consumer awareness and retail shelf space for millet-based products. North America leads global consumption with approximately 37% revenue share in 2025, while Asia Pacific is the fastest-growing region, propelled by India's national millet promotion policy and expanding health-food retail penetration across China and Southeast Asia.

Key Industry Highlights:

- Regional Leadership: North America leads the global millet snacks market with approximately 37% revenue share in 2025, driven by premium health-food consumer spending, gluten-free diet adoption, and strong specialty retail infrastructure supporting ancient grain product development and distribution.

- Fast-growing Market: Asia Pacific is the fastest-growing regional market through 2033, powered by India's Shree Anna Mission, China's functional food expansion, and rising millennial health consciousness across ASEAN markets, driving double-digit category growth rates.

- Leading Product: Chips & Crisps dominate the millet snacks market with 36% product type share in 2025, sustained by consumer familiarity with the chip format, regional flavor versatility, and broad retail distribution through established snack aisles in mass and health food channels.

- Fast-growing Product: Puffed Snacks & Extruded Products are the fastest-growing product type segment, as extrusion technology enables brands to overcome millet's taste barriers and deliver mainstream-appealing textures that drive trial and repeat purchase among conventional snack consumers.

- Leading Distribution Channel: E-commerce and DTC channels represent the highest-potential opportunity, enabling millet snack brands to achieve 13%+ CAGR channel growth through subscription models, personalized health positioning, and premium price realization without the shelf-space cost burden of physical retail.

Market Dynamics

Drivers - FAO's International Year of Millets and Government Policy Tailwinds

Governments and international agencies have provided the millet snacks category with an unprecedented volume of institutional support, directly translating into consumer education, retail expansion, and investment inflows that are structurally beneficial for market participants. The FAO's International Year of Millets 2023 initiative, endorsed by 72 countries, generated coordinated national campaigns spanning public procurement, school feeding programs, and retail promotion that significantly elevated millet visibility in mainstream grocery channels.

India's Ministry of Agriculture and Farmers Welfare launched the Shree Anna (Millets) Mission, allocating resources to expand millet production and processing, with direct downstream benefits for branded snack manufacturers. The Indian government's inclusion of millets in the Public Distribution System (PDS) and G20 advocacy for millet integration in global food systems have accelerated the grain's repositioning from subsistence crop to premium superfood ingredient, opening new product innovation and export pathways for snack brands globally.

Growing Consumer Demand for Gluten-Free, High-Nutrition Snack Alternatives

The structural shift away from conventional wheat- and corn-based snacks toward functional, nutrient-dense alternatives is creating durable demand for millet snacks across both health-motivated and medically-driven consumer segments. Millets are naturally gluten-free, rich in dietary fiber, magnesium, and antioxidants, and demonstrate a lower glycemic index compared to refined grain snack counterparts, attributes validated in peer-reviewed nutritional research published in journals such as the Journal of Food Science and Technology.

The Celiac Disease Foundation estimates that gluten intolerance and celiac disease affect approximately 1 in 100 people worldwide, representing a medically captive consumer segment for certified gluten-free millet snack products. Broader adoption of low-glycemic diets by consumers managing diabetes and metabolic health a population exceeding 537 million adults globally, according to the International Diabetes Federation (IDF) is further amplifying the health-motivated demand signal for millet-based snacks.

Market Restraints

Limited Consumer Awareness and Taste Familiarity in Western Markets

Despite growing institutional promotion, millet snacks continue to face a significant awareness and palatability gap among mainstream Western consumers who are unfamiliar with the grain's flavor profile and texture characteristics. Consumer research consistently identifies taste and sensory familiarity as the primary purchase drivers for snack foods, and millet's earthy, slightly bitter taste requires substantial product formulation investment to achieve broad appeal. This taste adaptation challenge increases product development costs and lead times for brands entering North American and European mass-market retail channels, constraining new entrant economics and slowing the category's transition from specialty to mainstream positioning.

Opportunities - Puffed and Extruded Millet Snack Innovation Targeting Mainstream Retail

The puffed snacks and extruded products segment represents the highest-growth innovation frontier in the millet snacks market, offering brands the most viable pathway to mainstream retail adoption by replicating the familiar texture and portability of conventional corn puffs and rice cakes. Extrusion technology enables manufacturers to mask millet's naturally bitter notes through controlled heat processing while achieving the light, crispy textures that mass-market snack consumers prefer, significantly lowering the taste barrier that suppresses category trial rates.

Brands such as Tata Soulfull and Slurrp Farm have pioneered flavored millet puffs in the Indian market, demonstrating robust repeat purchase rates. The global extruded snack market's scale and established retail infrastructure provide a ready distribution channel for millet-based entrants, and brands that invest in flavor innovation, including localized spice profiles for Asian markets and clean-label seasoning for North American health channels, are positioned to capture disproportionate share in this fast-growing segment.

E-Commerce and Direct-to-Consumer Channels Enabling Premium Millet Snack Penetration

Online retail is emerging as the most structurally advantageous growth channel for millet snack brands, enabling premium pricing, targeted health-conscious consumer acquisition, and subscription-based recurring revenue without the shelf-space cost and promotional spend burden of physical retail. The India Brand Equity Foundation (IBEF) reported that India's e-commerce grocery segment exceeded US$ 26 billion in 2023, with health and wellness food among the highest-growth categories.

In the U.S., platforms including Amazon and specialty health retailers such as Thrive Market have become primary discovery channels for emerging millet snack brands. Companies including True Elements, Healthy Master, and 24 Mantra Organic have built significant brand equity through digital-first distribution strategies, demonstrating that online channels allow millet snack brands to build loyal consumer bases and generate data-driven product iteration cycles that brick-and-mortar retail cannot provide.

Category-wise Analysis

Product Type Insights

Chips & crisps command approximately 36% of the global millet snacks market by product type in 2025, establishing clear segment leadership through their alignment with the most universally familiar snacking format globally. The chip format reduces consumer trial barriers by delivering an expected crunch, portability, and flavor versatility that consumers apply directly from corn and potato chip habits, making millet chips the most accessible entry point into the category for first-time buyers.

Brands including ITC Limited's Bingo! and Britannia Industries have leveraged existing snack distribution infrastructure to place millet chip variants in mass retail channels across India. The segment benefits from broad flavoring potential, accommodating regional spice profiles from South Asia to North America, and is supported by the clean-label movement's demand for baked or air-popped chip formulations that eliminate trans fats and artificial additives.

Distribution Channel Insights

Offline distribution channels retain approximately 68% of the millet snack market sales in 2025, anchored by the dominance of hypermarkets, supermarkets, and specialty health stores in providing physical trial opportunities that are essential for driving first-purchase conversion in an emerging category.

Consumers unfamiliar with millet-based snacks are more likely to trial new products when they can physically inspect packaging, read nutritional claims, and access in-store tastings, a consumer journey that offline retail uniquely facilitates. Retailers, including Whole Foods Market, Nature's Basket, and large-format hypermarket chains in the Asia Pacific, have expanded dedicated health snack sections, providing millet brands with elevated shelf placement. Online retail is the fastest-growing channel with a projected CAGR above 13% through 2033, driven by health-conscious millennial and Gen Z digital-native shoppers.

Regional Insights

North America Millet Snacks Market Trends and Insights

North America leads the global millet snacks market with approximately 37% revenue share in 2025, driven by strong health and wellness consumer culture, premium snack spending power, and growing retailer commitment to ancient grain and gluten-free product segments. The region benefits from a well-developed specialty health retail infrastructure and a rapidly expanding online health food marketplace that is accelerating millet snack brand visibility and trial.

U.S. Millet Snacks Market Size

The United States accounts for approximately 85% of North America's millet snack revenues, underpinned by the US$ 650+ billion domestic snack food industry and growing consumer adoption of ancient grains. Specialty health retailers and e-commerce platforms are the primary growth channels, with brands including Bob's Red Mill and Nature's Path Foods leading category development.

Europe Millet Snacks Market Trends and Insights

Europe's millet snacks market is expanding steadily, shaped by rising consumer interest in sustainable, plant-based nutrition, and the EU Farm to Fork Strategy's push toward diverse grain consumption. Germany, the U.K., and France lead regional consumption, supported by robust organic and health food retail networks and growing awareness of millet's nutritional credentials among flexitarian and allergen-conscious consumers.

U.K. Millet Snacks Market Size

The United Kingdom accounts for approximately 19% of European market share, driven by the mainstream health food retail expansion of chains such as Holland & Barrett and a strong gluten-free product demand base. The UK's Coeliac Disease prevalence, estimated at 1 in 100 people, sustains consistent demand for certified gluten-free millet snack formats and is expected to grow steadily through 2033.

France Millet Snacks Market Size

France holds approximately 15% of Europe's millet snack market, with demand anchored by the country's growing bio (organic) food movement and the expansion of health-oriented snack ranges in retail chains including Biocoop and Carrefour Bio. Consumer interest in ancient grains as part of Mediterranean-influenced healthy eating habits is driving incremental millet snack adoption through 2033.

Asia Pacific Millet Snacks Market Trends and Insights

Asia Pacific is the fastest-growing regional market for millet snacks, fueled by India's government-led millet promotion programs, China's expanding functional food consumer base, and the rapid rise of health-oriented snacking across ASEAN markets. China's growing middle class is actively seeking premium grain-based snack alternatives, with e-commerce platforms such as JD.com and Tmall amplifying brand reach for both domestic and imported millet snack products.

India Millet Snacks Market Size

India is the dominant sub-market within Asia Pacific, accounting for approximately 38% of the region's millet snack revenues. The government's Shree Anna Mission and the positioning of India as the global millet hub have directly boosted domestic branded snack development. Brands including Tata Soulfull, Slurrp Farm, and 24 Mantra Organic are scaling rapidly through e-commerce and modern trade channels.

Japan Millet Snacks Market Size

Japan accounts for approximately 14% of the Asia Pacific millet snack market, with demand driven by the country's long-established culture of whole grain and health-functional food consumption. Japanese consumers' preference for low-sugar, high-fiber snack formats aligns well with millet's nutritional profile, and specialty natural food retailers and convenience store health snack sections are the primary retail channels for the category.

Competitive Landscape

The millet snacks market is highly competitive, driven by rising consumer demand for healthy, gluten-free, and nutrient-rich snacking options. Competition is centered around product innovation, clean-label formulations, flavor diversification, and convenient packaging formats. Brands are focusing on baked, roasted, and extruded millet snacks to align with wellness trends and low-oil preferences. Premiumization and fortified offerings with added protein, fiber, and superfoods are strengthening market positioning. Strong retail presence across supermarkets and rapid growth in e-commerce are intensifying competition.

Key Developments

- In January 2026, WellBe Foods launched a new millet-based snacks category featuring Millet Nippatu, Millet Kodbale, Millet Chakli, Millet Tengolu, and Millet Chivda. The company reformulated traditional Indian snacks by replacing refined flour with a blend of rice flour and nutrient-rich, naturally gluten-free kodo millet to improve mainstream adoption of healthier grains.

- In November 2025, Kerala State Road Transport Corporation (KSRTC) launched a Children’s Day initiative to distribute gift packs to children travelling on long-distance buses and also introduced millet snacks for passengers on services passing through Thiruvalla.

- In September 2025, PepsiCo India expanded its millet-based snacking portfolio by launching Kurkure Jowar Puffs, marking the brand’s entry into the millet snacks category. The baked, not fried product combined jowar (sorghum) with Kurkure’s signature chatpata taste and was introduced in affordable INR 10 and INR 20 packs to ensure mass accessibility.

Millet Snacks Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 1.7 Billion |

| Current Market Value (2026) | US$ 2.8 Billion |

| Projected Market Value (2033) | US$ 5.6 Billion |

| CAGR (2026 - 2033) | 10.3% |

| Leading Region | North America, 37% market share (2025) |

| Dominant Category - Product Type | Chips & Crisps, 36% market share (2025) |

| Top-Ranking Category - Distribution Channel | Offline, 68% market share (2025) |

| Incremental Opportunity (2026 - 2033) | US$ 2.8 Billion |

Companies Covered in Millet Snacks Market

- Slurrp Farm

- Tata Soulfull

- ITC Limited

- 24 Mantra Organic

- True Elements

- Bagrry's India Ltd.

- Britannia Industries

- Healthy Master

- Pristine Organics

- Nature's Path Foods

- Kellogg's

- General Mills

- Bob's Red Mill Natural Foods

Frequently Asked Questions

The global millet snacks market is projected to reach US$ 2.8 billion in 2026.

The blend of consumer health consciousness and institutional policies support the FAO's International Year of Millets 2023 and India's Shree Anna Mission which have collecstively elevated millet's visibility as a nutritious, gluten-free, low-glycemic snack ingredient.

North America leads the global millet snacks market with approximately 37% revenue share in 2025, anchored by the U.S. market's premium health food spending, strong specialty retail infrastructure, and growing mainstream retailer adoption of ancient grain snack products.

The most significant growth opportunity lies in the puffed snacks and extruded products segment, where extrusion technology enables brands to overcome millet's taste familiarity barrier and deliver mainstream-appealing textures.

The global millet snacks market is led by Indian health food innovators including Tata Soulfull, Slurrp Farm, ITC Limited, 24 Mantra Organic, and True Elements in the Asia Pacific segment, alongside Western players including Nature's Path Foods, Kellogg's (Kellanova), General Mills Inc., and Bob's Red Mill Natural Foods in North America and Europe.