- Advanced Materials

- Medical Grade Paper Market

Medical Grade Paper Market Size, Share, and Growth Forecast, 2026 - 2033

Medical Grade Paper Market by Product Type (Sterilization Paper, Wrapping Paper, Others), Sterilization Method (Steam Sterilization, Ethylene Oxide Sterilization, Others), Application (Sterilization Packaging, Others), and Regional Analysis for 2026 - 2033

Medical Grade Paper Market Share and Trends Analysis

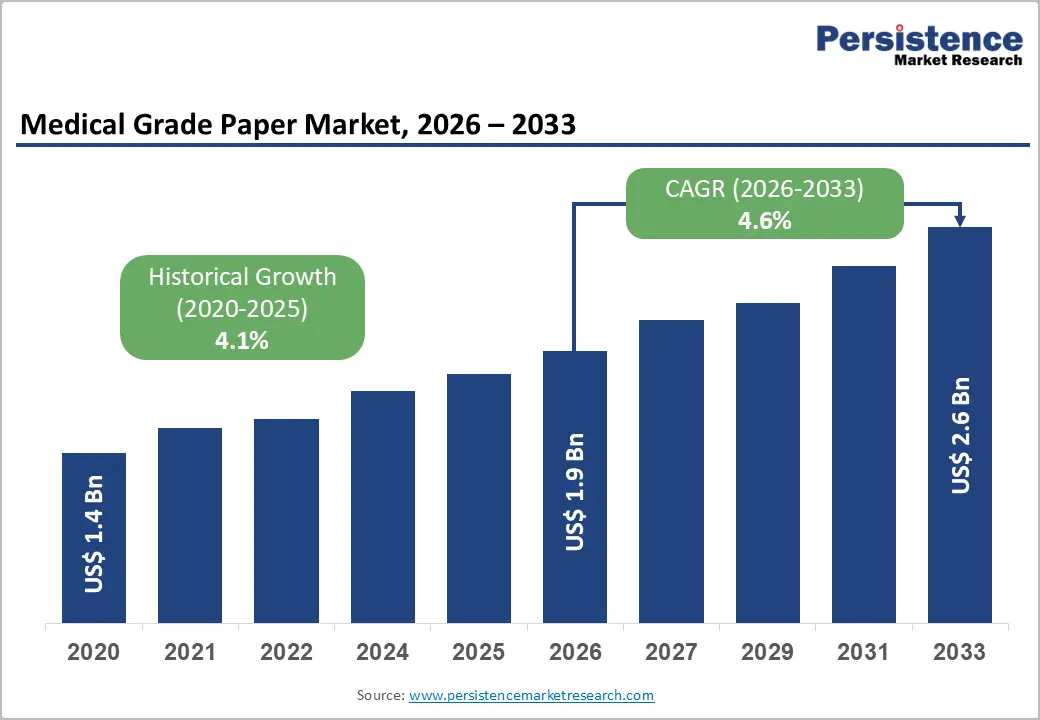

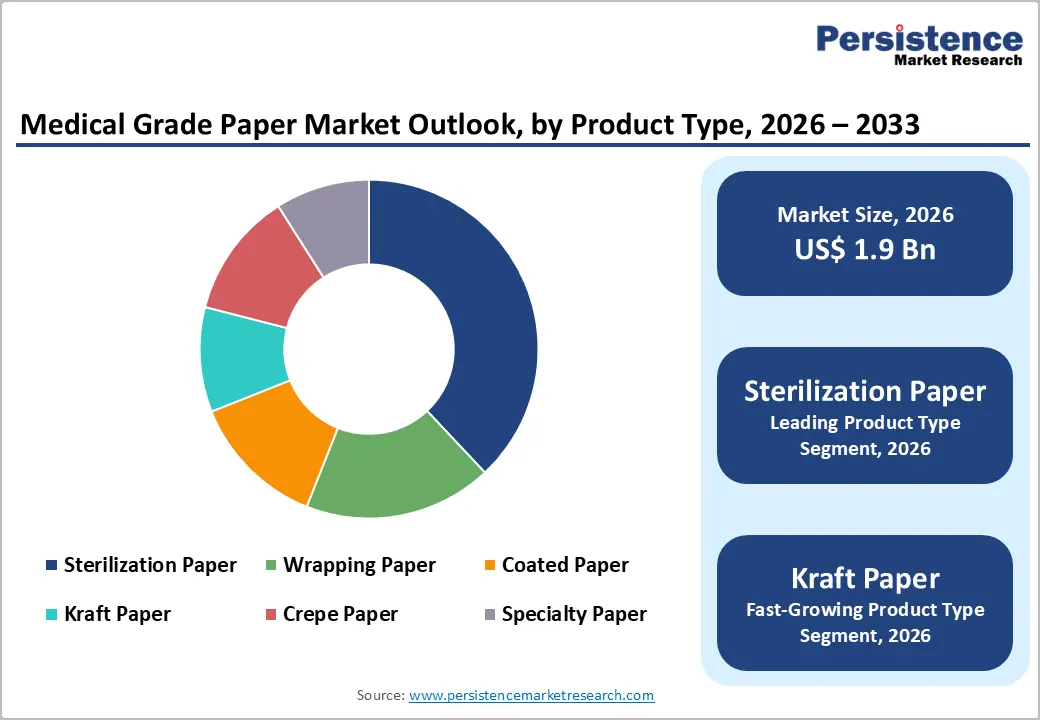

The global medical-grade paper market size is likely to be valued at US$1.9 billion in 2026 and is estimated to reach US$2.6 billion by 2033, growing at a CAGR of 4.6% during the forecast period 2026 - 2033, driven by increasing demand for sterile packaging solutions within the healthcare sector, which ensures sustained market expansion.

Demographic shifts, characterized by an aging global population, necessitate higher volumes of surgical procedures and chronic disease management. These clinical requirements dictate the use of high-barrier paper substrates to maintain instrument sterility. Strict regulatory frameworks regarding infection control drive the replacement of standard packaging with medical-grade alternatives.

Key Industry Highlights

- Leading Product Type: Sterilization paper is set to hold around 38% revenue share in 2026, driven by its extensive use in hospital-based autoclave processes.

- Fastest-growing Product Type: Kraft paper is projected to be the fastest-growing segment, supported by its increasing utilization in heavy-duty medical device pouches.

- Leading Application: Sterilization packaging is estimated to hold roughly 42% revenue share in 2026, due to constant demand for sterile barrier systems in surgical units.

- Fastest-Growing Application: Medical device packaging is forecast to grow the fastest, driven by expanding global production of specialized orthopedic implants.

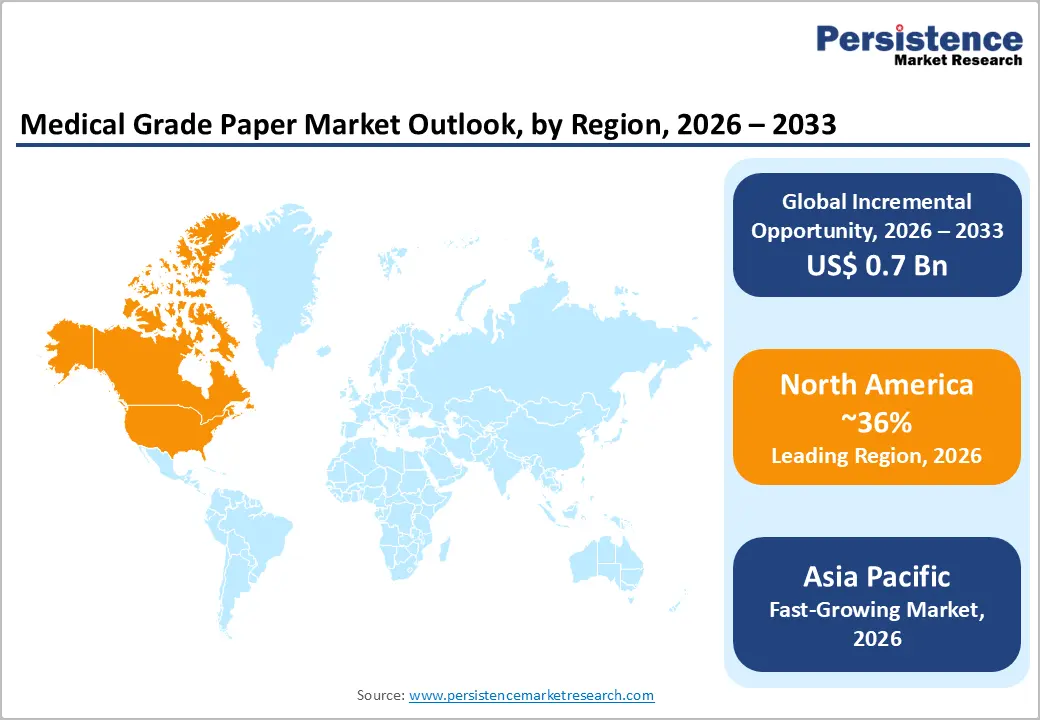

- Regional Leadership: North America is projected to capture roughly 36% of the market share by 2026, while Asia Pacific is forecast to record the fastest growth, driven by expanding healthcare infrastructure.

- Competitive Environment: The market is moderately fragmented, with key players such as Amcor and Billerud leveraging scale and specialized fiber technology to maintain leadership.

- Innovation Trends: Advancements in biodegradable coatings, enhanced microbial barrier properties, and smart packaging integration are shaping the long-term evolution of sterile paper substrates.

DRO Analysis

Driver - Stringent Regulatory Standards for Sterile Packaging

Global health authorities enforce rigorous standards for the sterilization and maintenance of medical devices to prevent healthcare-associated infections. Compliance with International Organization for Standardization (ISO) 11607 standards requires packaging materials to demonstrate validated microbial barrier properties and physical integrity during distribution. The U.S. Centers for Medicare & Medicaid Services reported that national health spending reached US$4.8 trillion in 2023, reflecting a continuous rise in clinical service utilization. This fiscal commitment to healthcare quality necessitates reliable sterile barriers.

Regulatory alignment across international borders promotes the adoption of standardized medical-grade paper. Manufacturers prioritize materials that facilitate effective gas sterilization while preventing recontamination after the process. Enhanced patient safety protocols lead to a direct increase in the consumption of specialized paper substrates. These materials provide a cost-effective yet high-performance solution for protecting single-use medical devices. Clinical settings increasingly rely on these validated barriers to mitigate the legal and health risks associated with surgical site infections.

Restraint - Competition from Advanced Synthetic Polymer Films

Synthetic materials such as Tyvek and various plastic laminates offer high puncture resistance and visual clarity for sterile packaging. These alternatives often provide superior moisture barriers compared to traditional paper-based solutions. In specialized applications involving heavy or sharp medical instruments, the mechanical limitations of paper may restrict its utilization and market share.

The shift toward transparent packaging allows for easier identification of contents in high-pressure clinical environments. As polymer technologies advance, the cost competitiveness between synthetics and medical paper narrows, impacting traditional market segments. Scalability in high-volume plastic production can outperform paper manufacturing in specific geographic regions. This competitive pressure necessitates continuous innovation in paper coatings to maintain functional relevance.

Opportunity - Advancements in Bio-Based and Sustainable Coating Technologies

Environmental regulations and corporate sustainability goals encourage the development of plastic-free medical packaging. Innovation in aqueous-based coatings allows paper to achieve high microbial barriers without the use of traditional synthetic laminates. These advancements enable manufacturers to offer fully recyclable and biodegradable sterile packaging solutions to healthcare providers. The shift toward circular-economy principles in hospital waste management creates a significant niche for eco-friendly medical paper.

Policy initiatives favoring sustainable procurement practices in major healthcare systems accelerate the adoption of these innovations. Companies investing in research and development for bio-polymers find new pathways for product differentiation. Market expansion is secured by aligning product portfolios with global decarbonization trends. This strategic transition reduces the environmental footprint of sterile barrier systems. Enhanced performance characteristics of new coatings further expand the application range of paper-based medical containers.

Category-wise Analysis

Product Type Insights

Sterilization paper is anticipated to secure around 38% of the medical-grade paper market share in 2026, reflecting its fundamental role in steam and gas sterilization cycles. Hospital sterilization wraps for surgical instrument trays utilize this material to ensure long-term shelf-life sterility. This segment maintains dominance due to standardized clinical protocols.

Kraft paper is expected to be the fastest-growing segment, propelled by its high mechanical strength and cost-effectiveness in medical pouch applications. Manufacturers use unbleached kraft paper for heavy-duty medical device packaging where puncture resistance is critical. Rising demand for economical yet reliable sterile barriers drives this accelerated growth.

Sterilization Method Insights

The steam sterilization segment is poised to dominate with a forecast market share of over 45% in 2026, powered by its universal application in hospital environments. Autoclave procedures utilize porous medical paper to allow steam penetration while maintaining a microbial barrier upon cooling. This method remains the gold standard for reusable medical instrument processing.

Ethylene oxide sterilization is estimated to be the fastest-growing segment, fueled by the increasing production of heat-sensitive single-use medical devices. Specialty coated papers enable efficient gas diffusion for the sterilization of intricate catheters and electronic medical components. Growth in disposable medical equipment manufacturing sustains this segment's rapid expansion.

Application Insights

Sterilization packaging is likely to be the leading segment with a projected 42% of the medical-grade paper market share in 2026, due to the high turnover of sterile supplies in surgical settings. Pre-formed sterilization pouches provide a standardized solution for small-scale dental and clinical practices. Constant replenishment of these supplies ensures market stability.

Medical device packaging is anticipated to be the fastest-growing segment, fueled by the global expansion of original equipment manufacturers producing specialized surgical implants. Packaging for orthopedic joint replacements requires high-performance medical paper to withstand rigorous transit and storage conditions. Increasing surgical intervention rates globally drive the demand in this application area.

Regional Insights

North America Medical Grade Paper Market Trends

North America is expected to lead with an estimated 36% of the medical grade paper market share in 2026, supported by advanced healthcare infrastructure, strict regulatory frameworks, and high surgical volumes. Strong presence of medical device manufacturers and adherence to sterilization standards drive consistent demand. Technological innovation in packaging materials enhances product performance.

U.S. Medical Grade Paper Market Insights

The U.S. market is projected to maintain a strong position in 2026, driven by domestic production strength, technological adoption, or sector-specific demand patterns. Leading companies, including Steris and Oliver Healthcare Packaging, focus on strategic expansion and innovation. Recent developments involve 2024-2026 advancements aligned with relevant regulatory or industrial frameworks, supporting efficiency improvements and compliance requirements.

Canada Medical Grade Paper Market Insights

The Canadian market is expected to witness steady expansion, supported by industrial development and application-specific growth. Key participants, including Winpak and Amcor, strengthen market presence through product optimization and capacity expansion. Strategic initiatives include infrastructure development and regulatory alignment, improving operational efficiency, and supporting sustained demand.

Europe Medical Grade Paper Market Trends

Europe represents a mature and highly regulated market, characterized by evolving industrial frameworks, regulatory reforms, and increasing adoption of advanced solutions. Market expansion is supported by infrastructure modernization and supply chain improvements. Demand is influenced by sector diversification and rising investment in production capabilities, reinforcing the regional market importance in the medical grade paper landscape.

Germany Medical Grade Paper Market Insights

The Germany market is forecast to maintain notable demand in 2026, supported by industrial expansion and targeted policy support. Key participants such as Billerud and Koehler Paper Group emphasize efficiency enhancement and production scaling. Recent developments include 2024-2026 advancements improving compliance alignment and strengthening manufacturing competitiveness.

France Medical Grade Paper Market Insights

The France market is projected to evolve through increasing technological integration and industrial investment. Leading companies, including Ahlstrom and Gascogne, focus on capacity expansion and innovation-driven strategies. Recent initiatives support infrastructure modernization and improved regulatory compliance across key application areas.

Asia Pacific Medical Grade Paper Market Trends

Asia Pacific is forecast to be the fastest-growing market for medical grade paper, stimulated by rapid healthcare infrastructure development, cost advantages, and increasing surgical procedures. Expanding manufacturing capabilities and government healthcare initiatives accelerate market penetration. Rising domestic demand and foreign investment strengthen supply chain localization, positioning the region as a major expansion hub.

China Medical Grade Paper Market Insights

The China market is expected to register rapid growth, supported by expanding industrial output and policy-driven incentives. Leading players such as Shanghai Jianzhong and Amcor focus on scaling production and improving operational efficiency. Recent developments include 2024-2026 investments in manufacturing capacity and infrastructure expansion.

India Medical Grade Paper Market Insights

The India market is anticipated to witness strong expansion due to rising demand across multiple application sectors. Key participants, including Billerud and various regional manufacturers, emphasize localization strategies and supply chain enhancement. Strategic investments and regulatory support strengthen production capabilities and market accessibility.

Competitive Landscape

The global medical grade paper market is moderately fragmented, with leading companies accounting for nearly 45% of total revenue shares. Competition is driven by sterilization compliance, sustainable packaging innovation, and healthcare packaging demand. High entry barriers persist due to regulatory certifications, cleanroom manufacturing requirements, and capital-intensive production infrastructure.

Amcor, Ahlstrom, Billerud, Oliver Healthcare Packaging, and Sterimed maintain strong market positions through advanced sterile barrier technologies and global distribution networks. Companies focus on recyclable medical packaging papers, product innovation, capacity expansion, and strategic partnerships to strengthen presence across medical device, pharmaceutical, and hospital packaging applications.

Key Industry Developments:

- In January 2026, ZSR Biomedical introduced a zero-ink, virgin-pulp-based eco-friendly packaging initiative that reduces paper usage by up to 20% while enhancing safety and sustainability.

- In June 2025, Covestro launched localized production of medical-grade Thermoplastic Polyurethane (TPU) in Asia Pacific to strengthen regional supply chains and support growing demand for high-performance sterile packaging materials, indirectly reinforcing innovation and supply reliability.

Companies Covered in Medical Grade Paper Market

- Amcor Plc

- Billerud AB

- Ahlstrom-Munksjö

- Steris Plc

- Oliver Healthcare Packaging

- Mondi Group

- Koehler Paper Group

- Winpak Ltd.

- Gascogne Group

- Shanghai Jianzhong Medical Packaging

- Westfield Medical Limited

- PMS Healthcare Technologies

- Bomark Packaging

- Arjowiggins

Frequently Asked Questions

The medical-grade paper market is projected to reach US$1.9 billion in 2026.

Rising surgical procedures and stringent sterilization regulations drive the medical-grade paper market.

The medical-grade paper market is poised to witness a CAGR of 4.6% from 2026 to 2033.

The development of sustainable biodegradable paper solutions and the expansion of healthcare infrastructure in emerging markets create key market opportunities.

Some of the key market players include Amcor Plc, Billerud AB, Ahlstrom-Munksjö, Steris Plc, Oliver Healthcare Packaging, and Mondi Group.