- Advanced Materials

- Engineered Stone Market

Engineered Stone Market Size, Share, and Growth Forecast 2026 – 2033

Engineered Stone Market by Product Type (Quartz-Based Engineered Stone, Engineered Marble), Form (Slabs, Tiles), Application (Countertops, Flooring), and Regional Analysis, 2026 – 2033

Engineered Stone Market Size and Trends Analysis

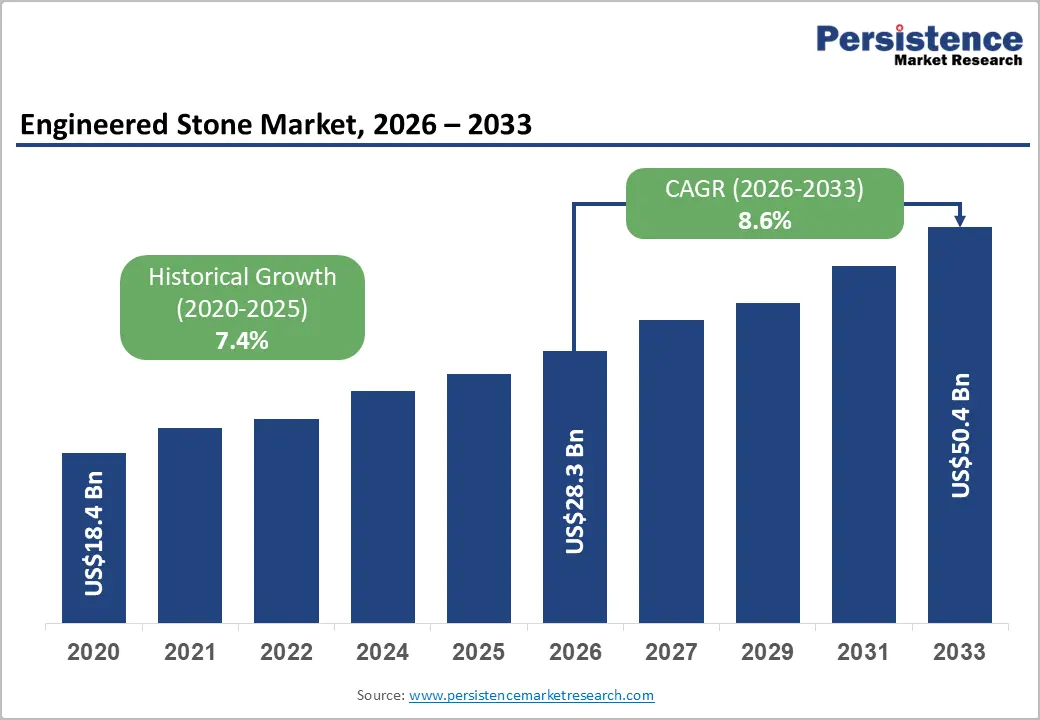

The global engineered stone market size is likely to be valued at US$28.3 billion in 2026 and is expected to reach US$50.4 billion by 2033, growing at a CAGR of 8.6% during the forecast period from 2026 to 2033, driven by increasing demand from residential renovation and modular kitchen installations across urban markets.

Rising preference for durable, low-maintenance, and non-porous surfaces is further spurring adoption in both residential and commercial spaces.

Key Industry Highlights:

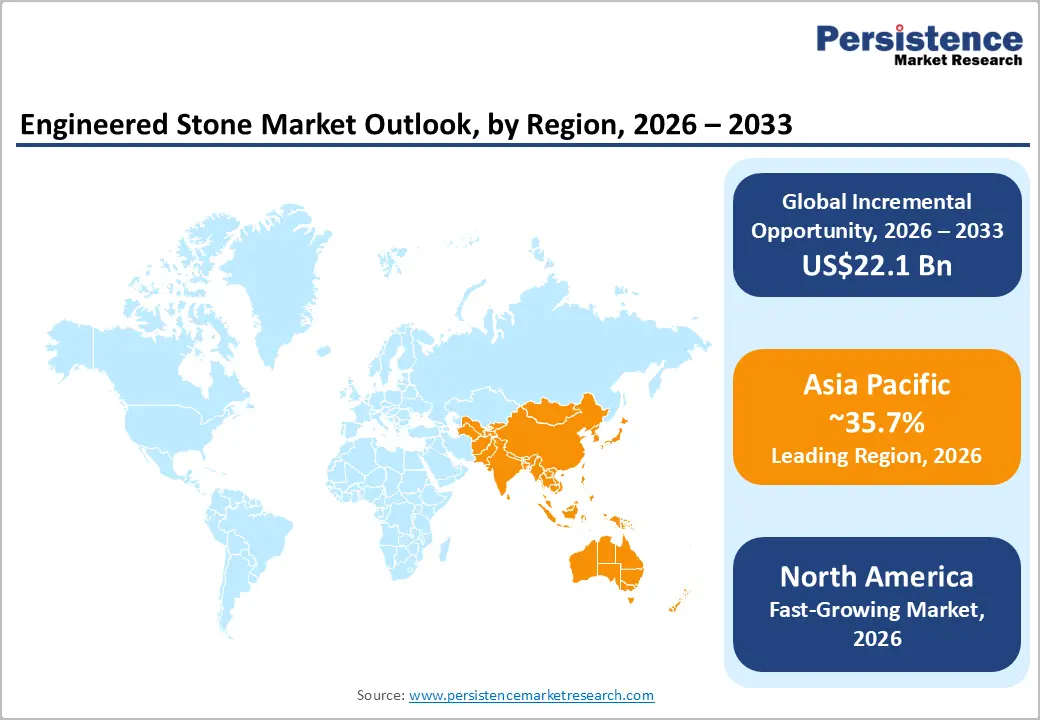

- Leading Region: Asia Pacific, with about a 35.7% share in 2026, backed by high construction demand and export dominance in low-cost engineered stone production.

- Fast-growing Region: North America, spurred by rising kitchen remodeling activity and strict silica regulations pushing safer material innovation.

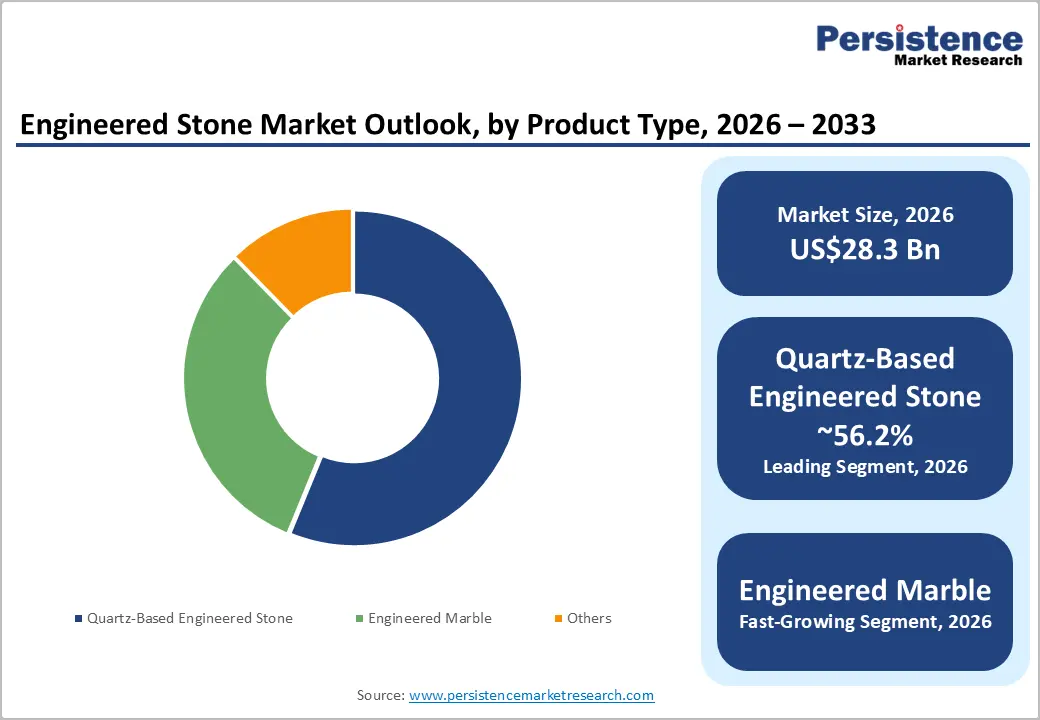

- Leading Product Type: Quartz-based engineered stone, approximately 56.2% share in 2026, as they combine high durability with non-porous and low-maintenance properties.

- Dominant Form: Slabs, nearly 58.7% in 2026, as large surfaces are preferred for countertops, islands, and wall cladding in modern residential and commercial designs.

- New Norm: In early 2026, California's Occupational Safety and Health Standards Board voted to advance a proposal to ban engineered stone with more than 1% crystalline silica, following testimony from dozens of physicians, job safety experts, and patients gravely ill with silicosis.

DRO Analysis

Driver - Booming Residential and Commercial Construction Sectors

Ongoing urbanization, especially in emerging economies, coupled with the expansion of residential sectors, is pushing significant demand for engineered stone. According to the World Bank, urban dwellers currently make up 56% of the global population, totaling 4.4 billion people. This demographic shift is constantly feeding construction pipelines across Asia Pacific, the Middle East, and South Asia.

In India alone, projects worth ?1.64 lakh crore (approximately US$17.2 billion) were completed under the Smart Cities Mission by 2025. Also, India's real estate market is projected to reach US$5.8 trillion by 2047, contributing 15.5% of total economic output, according to Invest India. This construction boom is creating high and sustained demand for affordable yet premium-looking surfacing materials, positioning engineered stone as a go-to choice for developers balancing aesthetics with budget.

Increasing Demand for Low Maintenance Products

Engineered stone is non-porous by construction. The manufacturing process binds crushed stone aggregate with polymer resin, filling all microscopic pores. This means no sealing is required at installation or at any point during the life of the countertop, which is one of its most significant practical advantages over granite and natural stone. In busy residential kitchens and commercial foodservice environments, this cuts down on maintenance costs and downtime.

For commercial kitchens, the non-porous nature simplifies compliance with hygienic cleaning protocols and reduces the frequency of maintenance required compared to natural stone. The result is a surface that remains hygienic and visually consistent with just routine cleaning. This is a meaningful differentiator for facility managers and homeowners alike.

Restraint - Vulnerability to Heat May Pose a Threat to Growth

Engineered stone is composed of natural quartz crystals bound together with polymer resins, which make up about 7% to 10% of the countertop material. These resins can begin to degrade when exposed to temperatures above 150°C (300°F), causing discoloration, warping, or cracking. This is a key functional limitation, especially in active kitchens where direct contact with hot cookware is common. Engineered stones are less heat-resistant than natural stones such as granite.

Their susceptibility to damage from sudden temperature shifts can be a limiting factor. Unlike granite, which can withstand much higher heat, engineered stone requires constant precaution, such as always using a trivet. Engineered stone also contains polymeric resins that are not UV stable, causing discoloration and breakdown of the resin binder over time, making it unfit for outdoor use as well. These combined vulnerabilities restrict application scope and can deter buyers who prioritize durability in high-heat environments.

Opportunity - Silica-Free and Low-Silica Formulations to Open New Markets

Strict occupational health regulations are changing the field of engineered stone at a product level. On 1 July 2024, all states and territories in Australia made it an offence to carry out or direct work involving the manufacture, supply, processing, or installation of engineered stone benchtops containing at least 1% crystalline silica, following a recommendation by Safe Work Australia in response to rising silicosis cases among fabricators. This ban has propelled a global product shift.

In response, Caesarstone launched Caesarstone ICON in July 2025. It is a crystalline silica-free surface with approximately 80% recycled materials. The company began a national U.S. rollout and transitioned 19 of its customer-favorite quartz products to the new formula. Similarly, Cosentino previewed its first zero-silica surface, Q0, at KBIS 2025, using its Inlayr Design Technology with up to 90% recycled content and crystalline silica content below 1%. These regulatory pressures are effectively creating a new product category and opening markets previously inaccessible due to health compliance concerns.

Eco-Friendly Materials to Gain Traction through Recycled and Bio-Based Inputs

Rising environmental mandates are pushing manufacturers to rethink material sourcing beyond just silica reduction. Cosentino's EARTHIC by Silestone XM collection, launched in April 2024, uses an advanced composition of up to 30% recycled materials, including recycled glass, PET, and post-consumer bio-resin derived from vegetable oil and recycled cooking oil. All Silestone products are now made using 100% renewable electric energy and 99% recycled and reused water, with a minimum of 20% recycled raw materials in their composition.

On the broad material front, bio-based epoxy resins replace petroleum-derived components with plant-based ingredients such as plant oils, maintaining high performance while significantly reducing the carbon footprint. These developments signal a clear industry direction: sustainable formulations are no longer a niche offering but are fast becoming a baseline expectation. These are further creating meaningful growth potential for brands that invest early in this transition.

Category-wise Analysis

Product Type Insights

Quartz-based engineered stones are predicted to lead with a share of approximately 56.2% in 2026, as they provide a combination of durability, low maintenance, and design consistency that natural stones struggle to match. Quartz is one of the hardest minerals found in nature, making engineered quartz surfaces highly resistant to scratches, stains, and daily wear. Unlike natural marble and granite, quartz surfaces are non-porous, which means they do not absorb liquids or require frequent sealing. This makes them particularly attractive for kitchens, healthcare facilities, restaurants, and commercial spaces.

Engineered marbles are estimated to be the fastest-growing segment in the forecast period, as these provide the luxurious appearance of natural marble without many of the maintenance challenges. Growth is mainly being propelled by the luxury residential and hospitality sectors. Hotels, high-end apartments, and commercial developments increasingly want marble-inspired interiors but require materials that are easy to maintain over the long term. Engineered marble provides a practical alternative at a lower lifecycle cost than natural marble. This balance between appearance and functionality is attracting developers and architects.

Form Insights

Slabs are anticipated to dominate with a share of nearly 58.7% in 2026 as most high-value applications, especially countertops, kitchen islands, wall cladding, vanity tops, and commercial surfaces, require large continuous pieces rather than small formats. One of the biggest advantages of slabs is the ability to create smooth surfaces. Architects and homeowners increasingly prefer large islands, waterfall countertops, and full-height backsplashes with minimal joints. Large slabs reduce visible seams and provide a premium appearance that is difficult to achieve with tiles. This design trend has become particularly superior in luxury kitchens and modern commercial interiors.

Tiles are expected to remain in the second position in 2026, as they provide greater affordability and installation flexibility than slabs. While slabs dominate premium applications, tiles are increasingly used in renovations, commercial flooring, bathrooms, and wall applications where large-format surfaces may not be practical. Their low transportation and installation costs make them attractive for budget-conscious projects. Another prominent growth driver is the rising popularity of large-format tiles. These products provide a slab-like appearance while retaining the installation advantages of tiles.

Regional Insights

Asia Pacific Engineered Stone Market Trends

Asia Pacific is anticipated to dominate in 2026 with a share of nearly 35.7%, owing to the surging use of engineered stone for the construction and decoration of residential and non-residential interiors in rapidly expanding economies such as China, India, Japan, Malaysia, and Singapore. The region benefits from a rare combination, i.e., massive construction demand and a superior domestic supply base. The region is not just consuming engineered stone at scale, but it is also the world's workshop for it. Rising middle-class incomes and a shift toward premium home interiors are adding a further consumption layer on top of new construction, giving the region both volume and value-driven momentum.

China Engineered Stone Market Trends

China will likely lead Asia Pacific in 2026 with a share of around 32.7%. The country has over 100 quartz stone factories, with the Fujian Xiamen and Quanzhou-Shuitou area alone accounting for more than 60% of China’s total quartz production. On the demand side, state investment has been a key driver. Under China's 14th Five-Year Plan (2021 to 2025), the country completed 15.4 billion square meters of new building area between 2021 and 2024, and constructed over 11 million units of affordable housing.

As per the National Bureau of Statistics of China (NBS), the construction sector's total output reached 32.7 trillion yuan (US$4.6 trillion) in 2024, up 24% from 2020. This volume of housing output translates to sustained demand for interior surface materials such as engineered stone. Strategic initiatives, including Made in China 2025, further underline the country’s ambitions to extend high-value manufacturing output and global market presence.

India Engineered Stone Market Trends

In 2026, India is projected to account for a share of approximately 26.5%, and it is one of the most promising growth stories in engineered stone globally. Several real estate projects across metropolitan areas such as Mumbai, Delhi NCR, and Bengaluru incorporate engineered quartz surfaces for flooring, countertops, and wall cladding. Key developers such as DLF, Prestige Estates, and Sobha Ltd. have standardized the use of engineered quartz in premium residential and commercial projects. Government programs are strengthening this demand. The Smart Cities Mission has allocated around US$2.8 billion for sustainable building materials, thereby boosting quartz adoption in public infrastructure.

North America Engineered Stone Market Trends

North America is predicted to be the fastest-growing market in 2026 with a share of approximately 27.6%. Kitchen countertops hold the dominant share of the regional market, augmented by remodeling, durability demand, luxury housing growth, and increasing consumer preference for stylish surfaces. What makes North America dynamic is not just new construction, but a deeply embedded renovation culture. Commercial adoption is also adding to this momentum. Rising sustainability adoption and the expanding commercial hospitality sector seeking durable, hygienic, eco-friendly surfaces for kitchens, bathrooms, flooring, and wall applications are key factors fueling the market.

U.S. Engineered Stone Market Trends

A share of nearly 52.6% is expected to be held by the U.S. in 2026, augmented by surging residential remodeling activity and high adoption of premium kitchen and bathroom surfaces. The Joint Center for Housing Studies (JCHS) at Harvard University tracks this renovation wave closely. According to JCHS, total homeowner remodeling spending is anticipated to reach a record US$524 billion in early 2026, with year-over-year spending on home renovation projected to rise 2.4% in early 2026. Kitchens and bathrooms are the top renovation priorities for American homeowners. Quartz is the dominant material of choice in those spaces, creating a reliable and recurring demand cycle.

Europe Engineered Stone Market Trends

Europe will likely see steady growth over the forecast period, with a share of nearly 16.9% in 2026, backed by rising emphasis on premium interior design, renovation activities, and increasing preference for durable and aesthetically appealing surfacing materials. According to a 2025 Eurobarometer survey, 68% of homeowners on the continent consider energy efficiency and material sustainability important when undertaking renovations. This complies well with engineered stone's low-maintenance and durable profile. According to Eurostat, the average annual building production in the EU and the euro region increased by 0.1% and 0.2%, respectively, in 2024 compared to 2022. The EU Renovation Wave and green building mandates continue to push refurbishment activity across member states, ensuring steady baseline demand.

Germany Engineered Stone Market Trends

Germany will likely register a substantial share of approximately 32.2% in 2026. Key growth drivers include rising residential renovations, expansion in commercial and hospitality projects, and increasing adoption of sustainable, eco-friendly engineered stone materials complying with environmental regulations. Germany's sustainability-first construction philosophy is a core tailwind. The nation's emphasis on green building practices, including passive house standards, boosts sales of sustainable and energy-efficient materials.

U.K. Engineered Stone Market Trends

A share of around 19.8% is predicted to be held by the U.K. in 2026, supported by surging residential renovations, luxury housing projects, and extensive commercial developments concentrated in London as well as surrounding metropolitan areas. On the regulatory front, the country has not banned engineered stone like Australia, but is tightening controls. The Health and Safety Executive (HSE) published new COSHH guidance requiring businesses to switch to low-silica engineered stone and use on-tool water suppression. This is backed by a nationwide inspection program, which is changing product specifications across the industry.

Competitive Landscape

The global engineered stone market is moderately fragmented, with the presence of international brands controlling the premium segment. Hundreds of regional manufacturers are competing on pricing, customization, and local distribution. Cosentino S.A., VICOSTONE, LX Hausys, and Cambria compete by delivering designer finishes, large-format slabs, and advanced surface technologies. They invest heavily in research and development activities to introduce features such as low-silica or silica-free surfaces, responding to tightening health regulations.

Beyond these leaders, the market becomes highly competitive and fragmented, especially in China and India, where hundreds of small and mid-sized manufacturers supply cost-effective quartz slabs. China alone accounts for a key share of global exports, with provinces such as Guangdong and Fujian acting as production hubs. These players often compete on price margins that are 20 to 40% lower than branded Western products, enabling them to penetrate markets in Southeast Asia, the Middle East, and Africa.

Key Industry Developments

- In May 2026, CRL Stone introduced its new 2026 CRL Quartz brochure, showcasing its complete collection of engineered quartz surfaces along with clearly identified Low Silica and Silica-Free options. CRL Quartz surfaces are non-porous, easy to clean, and designed to provide long-lasting durability, making them suitable for demanding residential and commercial environments.

- In April 2025, Construction Resources Company, LLC completed the acquisition of Opustone, L.L.C. from Mosaic Companies. Opustone is a stone slab and tile distributor with three showroom locations in South Florida. It provides premium surfaces for luxury residential and commercial design projects. Construction Resources, which was acquired by The Home Depot in December 2023, noted that Opustone would join UMI Stone and Cancos Tile & Stone under its surfaces portfolio.

- In February 2025, LX Hausys unveiled two new engineered stone technologies at KBIS in Las Vegas, namely, Splendor and Cloud Ridge. These feature luxurious, marble-like natural stone aesthetics, as part of the company's broad push to propel its presence in North America’s market.

Companies Covered in Engineered Stone Market

- LX Hausys

- Johnson Marble & Quartz

- Technistone A.S.

- Caesarstone Ltd.

- Belenco

- Quarella Group Ltd.

- Quartzforms

- Stone Italiana S.p.A.

- Cosentino S.A.

- VICOSTONE

- Others

Frequently Asked Questions

The global engineered stone market is projected to be valued at US$28.3 billion in 2026.

The engineered stone market is expected to reach US$50.4 billion by 2033.

Key market trends include the shift toward low- or zero-silica surfaces due to health regulations and high demand for large-format designs.

Slabs are expected to be the leading form segment with a share of nearly 58.7% in 2026, as manufacturers are producing jumbo sizes that reduce joints and improve aesthetics.

The engineered stone market is expected to grow at a CAGR of 8.6% from 2026 to 2033.

LX Hausys, Johnson Marble & Quartz, and Technistone A.S. are a few key market players.