- Processed Food

- Low-Calorie Food Market

Low-Calorie Food Market Size, Share, and Growth Forecast 2026 - 2033

Low-Calorie Food Market by Product (Sucralose, Aspartame, Stevia, Saccharin, Cyclamate), by Application, Distribution Channel, and Regional Analysis, 2026 - 2033

Low-Calorie Food Market Size and Trend Analysis

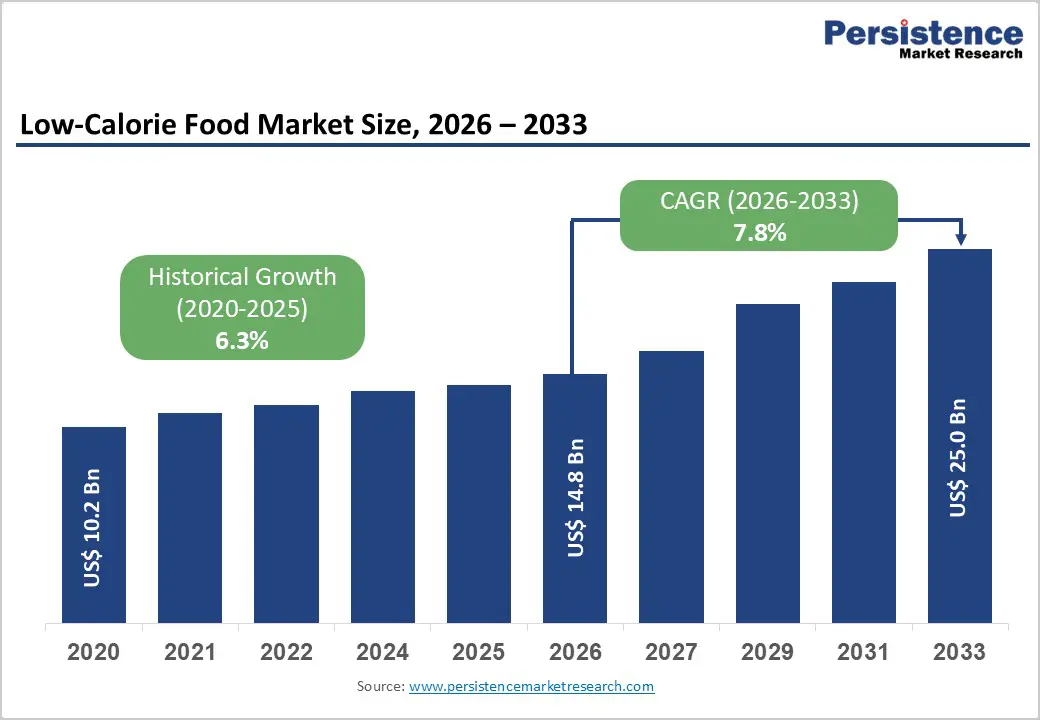

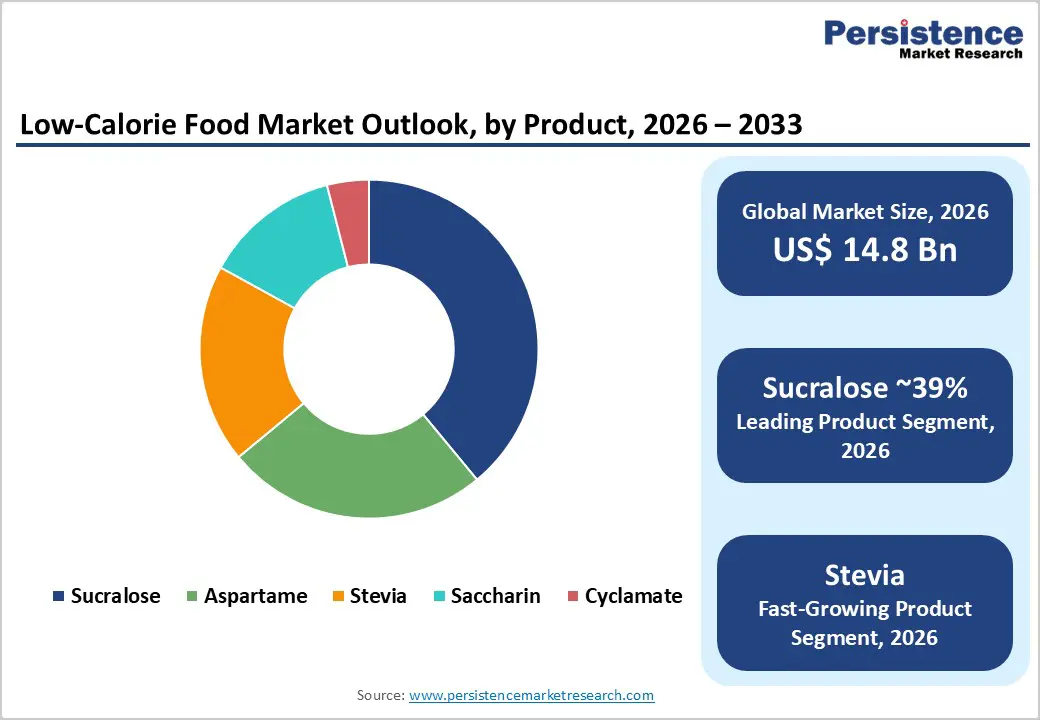

The global low-calorie food market size is expected to be valued at US$ 14.8 billion in 2026 and projected to reach US$ 25.0 billion by 2033, growing at a CAGR of 7.8% between 2026 and 2033. The market includes food and beverage products formulated with reduced sugar, fat, or calorie content to support healthier dietary choices.

These products often use alternative sweeteners such as aspartame, sucralose, stevia, and saccharin to maintain taste while lowering calorie intake. Rising global concerns over obesity, diabetes, and other lifestyle-related diseases are driving consumer demand for low-calorie options. Food manufacturers are increasingly reformulating products to meet regulatory guidelines and consumer preferences for healthier diets. In addition, growing awareness of nutrition, expanding fitness trends, and innovation in natural sweeteners and functional ingredients are further supporting the growth of the low-calorie food market worldwide.

Key Industry Highlights:

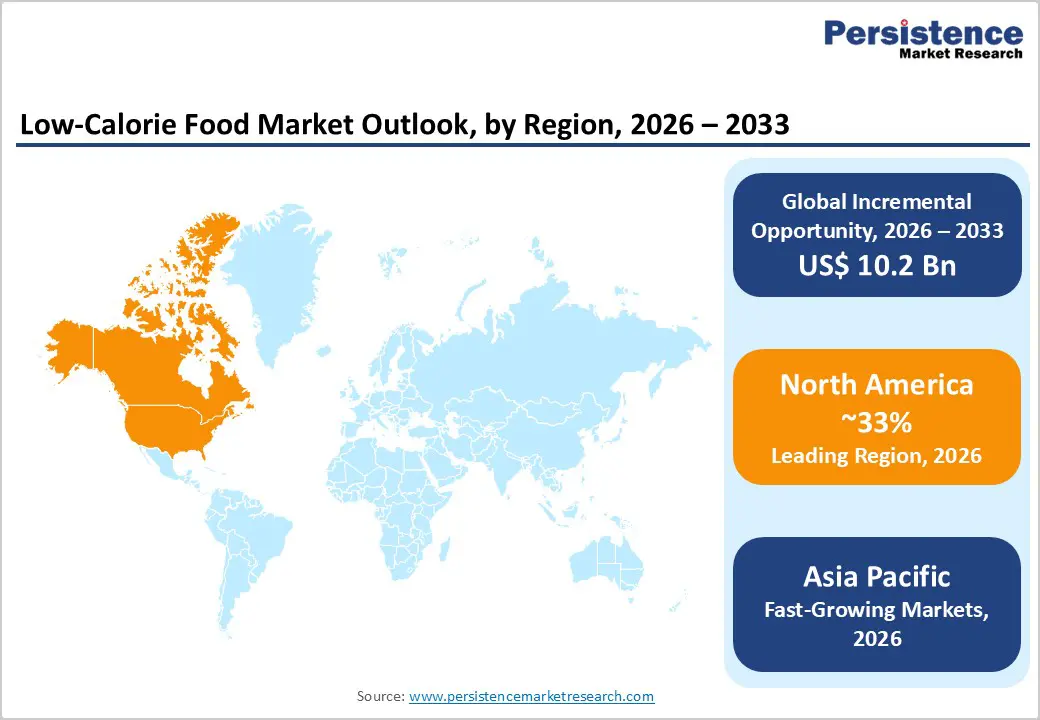

- North America leads the market with about 33% share in 2025, supported by high U.S. obesity prevalence, regulatory sweetener approvals, and large-scale reformulation by major food and beverage companies.

- Asia Pacific is the fastest-growing region, expanding at around 9% CAGR through 2032, driven by rising diabetes prevalence, rapid urbanization, and strong stevia production capacity.

- Sucralose dominates the product segment with nearly 39% market share in 2025, supported by high sweetness intensity, strong thermal stability, wide regulatory approvals, and increasing food industry adoption.

- Stevia is the fastest-growing segment, projected to grow above 12% CAGR due to rising clean-label demand, improved taste solutions like Reb M, and expanding global supply chains.

- Zero-calorie functional beverages present a major opportunity, combining sweeteners with vitamins and probiotics, attracting health-conscious consumers and driving strong repeat purchases in global beverage markets.

| Key Insights | Details |

|---|---|

| Low-Calorie Food Market Size (2026E) | US$ 14.8 billion |

| Market Value Forecast (2033F) | US$ 25.0 billion |

| Projected Growth CAGR (2026 - 2033) | 7.8% |

| Historical Market Growth (2020 - 2025) | 6.3% |

Market Dynamics

Drivers - Global obesity crisis and regulatory sugar reduction mandates

The rising global obesity crisis has become a major driver for the demand for low-calorie food products worldwide. According to the World Health Organization, more than 1 billion adults and around 39 million children under the age of five were living with obesity in 2022, reflecting a significant increase over the past decades. High sugar intake is widely recognized as a major contributor to obesity and related health conditions such as diabetes and cardiovascular diseases. As consumers become more aware of the health risks associated with excessive sugar consumption, demand for reduced-calorie and sugar-free foods and beverages has increased. Food manufacturers are responding by incorporating alternative sweeteners such as aspartame, sucralose, and stevia to maintain product taste while lowering calorie content.

Government regulations and sugar reduction policies are further accelerating the adoption of low-calorie ingredients across the food and beverage industry. Several countries have introduced sugar taxes, front-of-pack nutritional labeling, and reformulation targets to encourage healthier consumption patterns. For example, the United Kingdom’s Soft Drinks Industry Levy led to a significant reduction in sugar levels in beverages within a short period after implementation. Similar initiatives in countries such as Mexico, France, and South Africa are encouraging manufacturers to reformulate products using high-intensity sweeteners, creating sustained demand for low-calorie food solutions globally.

Restraints - Consumer Skepticism Toward Artificial Sweeteners

Consumer skepticism toward artificial sweeteners remains a major restraint for the low-calorie food market despite regulatory approvals and widespread industry use. Artificial sweeteners such as aspartame and saccharin have been approved by global regulators including the U.S. Food and Drug Administration and the European Food Safety Authority, which have repeatedly confirmed their safety within recommended intake levels. However, recurring media reports and debates linking certain artificial sweeteners to potential health risks, including cancer, continue to influence public perception. These discussions often create confusion among consumers, leading many to question the long-term safety of diet beverages, sugar-free snacks, and other low-calorie food products.

Recent consumer research indicates that a significant share of shoppers actively avoids products containing artificial sweeteners, preferring natural alternatives or products marketed with “no artificial ingredients” claims. This shift in consumer behavior particularly impacts diet sodas and sugar-free confectionery products, where taste concerns such as bitterness or aftertaste also influence purchasing decisions. As a result, food and beverage manufacturers are increasingly investing in new formulation strategies, flavor-masking technologies, and natural sweetener blends to maintain product taste while addressing consumer concerns, often increasing overall production and research costs.

Opportunities - Natural Sweeteners Expansion Led by Stevia Innovation

The growing demand for natural and plant-based ingredients presents a significant opportunity for the low-calorie food market, particularly through the rapid expansion of stevia-based sweeteners. Consumers are increasingly seeking clean-label products with recognizable and natural ingredients, encouraging manufacturers to shift away from synthetic sweeteners toward plant-derived alternatives. Market studies show that many consumers prefer natural sweeteners, which has accelerated the adoption of stevia across beverages, dairy products, snacks, and confectionery categories. As health awareness continues to rise, stevia is becoming a preferred solution for reducing sugar content while maintaining sweetness in a wide range of food products.

Technological innovations are further strengthening the growth potential of stevia. Advances in fermentation-based production of steviol glycosides, particularly Reb M, have significantly improved taste profiles by reducing the bitterness often associated with earlier stevia extracts. These developments allow manufacturers to achieve high levels of sugar reduction without compromising flavor. At the same time, expanding cultivation and production in major agricultural regions such as China and India is improving supply stability and cost competitiveness. Large global food and beverage companies are increasingly investing in stevia-based product reformulation, supporting long-term growth across multiple low-calorie food segments.

Category-wise Analysis

Product Insights

Sucralose holds the leading position within the product segment of the low-calorie food market, accounting for an estimated 39% share in 2026. Its dominance is largely linked to strong functional advantages in food processing and beverage formulation. Sucralose provides approximately 600 times the sweetness of sugar while containing no calories, making it an effective substitute in reduced-sugar and sugar-free products. Regulatory approvals from major authorities, including the U.S. Food and Drug Administration, the European Food Safety Authority, and the Joint FAO/WHO Expert Committee on Food Additives have strengthened industry confidence in its safety and stability.

Another key advantage is its strong thermal and acid stability, allowing manufacturers to use it in baked goods, beverages, dairy products, and confectionery without significant degradation during processing. Global beverage brands frequently use sucralose in combination with other sweeteners to achieve a balanced taste profile in zero-sugar beverages. Over the past two decades, improvements in production technologies and expansion of manufacturing capacity in Asia have reduced production costs significantly, allowing the ingredient to be used across both premium and mass-market food products. As a result, sucralose continues to remain widely adopted across diverse low-calorie food and beverage categories worldwide.

Distribution Channel Insights

The Business-to-Consumer (B2C) retail segment, particularly hypermarkets and supermarkets, represents the leading distribution channel for low-calorie food products, accounting for roughly 45% of total sales. Large retail chains provide extensive shelf space and high product visibility, allowing consumers to easily access diet beverages, reduced-sugar snacks, and other low-calorie alternatives. In-store marketing strategies, product placement, and promotional discounts further influence purchasing decisions, especially for ready-to-drink beverages and packaged diet foods. Supermarkets also benefit from high customer traffic and broad product assortments, which support the rapid introduction of new low-calorie food innovations.

Online retail has emerged as the fastest-growing distribution channel as digital grocery platforms continue to expand. E-commerce platforms such as Amazon have strengthened the availability of specialty diet products, including stevia-sweetened beverages, keto-friendly snacks, and sugar-free confectionery. Consumers increasingly prefer online channels for convenience, product variety, and access to niche wellness brands. Meanwhile, Business-to-Business (B2B) supply channels remain important for the bulk distribution of sweeteners to food manufacturers, ensuring a steady supply of ingredients used in large-scale product reformulation and manufacturing.

Regional Insights

North America Low-Calorie Food Market Trends and Insights

North America represents the largest regional market for low-calorie food products, accounting for an estimated 33% share of global demand in 2025. The U.S. contributes much of this regional consumption due to strong consumer awareness of health and nutrition, along with a well-developed packaged food industry. According to the Centers for Disease Control and Prevention, approximately 42% of U.S. adults are affected by obesity, encouraging consumers to reduce sugar intake and shift toward low-calorie food and beverage options. Regulatory clarity also supports product development. The U.S. Food and Drug Administration has approved multiple high-intensity sweeteners and granted recognized safety status for several sugar alternatives used in reduced-calorie foods.

Major food and beverage companies continue to introduce reformulated products and low-sugar alternatives to meet changing consumer preferences. Retail chains across the U.S. and Canada are increasing shelf space for reduced-sugar beverages, diet snacks, and functional wellness products. At the same time, private-label brands are expanding their presence in supermarkets as retailers introduce competitively priced low-calorie options. Online grocery platforms such as Amazon are also playing a growing role by expanding digital access to specialty health products and enabling smaller brands to reach a wider consumer base across North America.

Asia Pacific Low-Calorie Food Market Trends and Insights

Asia Pacific is the fastest-growing regional market for low-calorie food products, supported by rapid urbanization, expanding middle-class populations, and increasing health awareness. Countries such as China, India, and Japan are experiencing rising rates of lifestyle-related diseases, including obesity and diabetes, which are encouraging consumers to reduce sugar intake. Government initiatives are also influencing market growth. In India, the Food Safety and Standards Authority of India has introduced front-of-pack labeling guidelines aimed at improving consumer awareness about sugar and calorie content in packaged foods. Such policies are encouraging manufacturers to introduce reduced-sugar beverages and reformulated food products.

China plays a major role in the regional market, particularly due to its strong agricultural and manufacturing capacity for natural sweeteners such as stevia. Expanding production capacity and large domestic demand are supporting the development of low-calorie beverage and dairy products across the country. In Southeast Asia, growing urban populations and increasing adoption of modern retail channels are accelerating demand for healthier packaged foods. Digital commerce platforms such as Alibaba and Flipkart are further strengthening product availability by enabling consumers to access a wide range of low-calorie beverages, snacks, and wellness-focused food products.

Competitive Landscape

The global low-calorie food market is dominated by many multinational corporations. Companies with a global presence account for 45-50% of the market. Manufacturers are focusing on the improvement of production lines and diversifying their offerings to cater to a wide consumer base. Maintaining conventional taste while reducing calorific content has gathered focus from consumers and producers alike. Mergers, acquisitions and joint ventures are steps taken by various companies to increase their global footprint.

Key Developments:

- In January 2026, Swiggy launched its EatRight category across more than 50 cities, offering health-focused food options with over 1.8 million dishes from more than 200,000 restaurants.

- In January 2025, Nestlé launched a new range of low-calorie ice cream products under its Häagen-Dazs brand, targeting consumers seeking indulgent desserts with reduced calorie content.

- In October 2024, PepsiCo acquired a stake in a plant-based snack brand offering low-calorie snack options, strengthening its portfolio of healthier food products for health-conscious consumers.

Companies Covered in Low-Calorie Food Market

- Cargill, Inc.

- Pepsi Co Inc.

- Ajinomoto Co, Inc.

- The Coca Cola Company

- Tate & Lyle PLC

- Stevia Biotech Pvt, Ltd.

- Vitasweet Co. Ltd.

- Bernard Food Industries Inc.

- Wisdom Natural Brands

- Beneo GmbH

- JK Sucralose Inc.

- Ingredion Inc.

- Zydus Wellness

- Others

Frequently Asked Questions

The Low-Calorie Food market is projected to reach US$ 14.8 billion in 2026.

Rising obesity prevalence and global sugar reduction policies drive demand for low-calorie foods, while consumers increasingly prefer reduced-sugar products and healthier beverage alternatives.

North America leads the Low-Calorie Food market due to high obesity prevalence, strong regulatory approvals for sweeteners, and large-scale distribution by major food companies.

Stevia presents a major growth opportunity due to strong clean-label demand, improving taste technologies, expanding supply chains, and increasing reformulation efforts by global food manufacturers.

Key market players include Cargill, PepsiCo, Coca-Cola, Tate & Lyle, Ingredion, JK Sucralose, Beneo, and Zydus, offering diverse low-calorie sweetener portfolios globally.