- Pharmaceuticals

- Long-Acting Drugs Market

Long-Acting Drugs Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Long-Acting Drugs Market by Delivery Technology (Liposome-Based Systems, Microsphere-Based Systems, Polymer-Based Depots, In-Situ Forming Gels, Nanoparticle-Based Systems), Route of Administration (Injectable, Implant, Oral), Therapeutic Area (Cancer, Central Nervous System (CNS) Disorders, Hormone Disorders, Infectious Diseases, Pain Management, Contraception), Material Used (Polymer, Non-Polymer), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies, Specialty Clinics), and Regional Analysis from 2026 to 2033

Long-Acting Drugs Market Size and Share Analysis

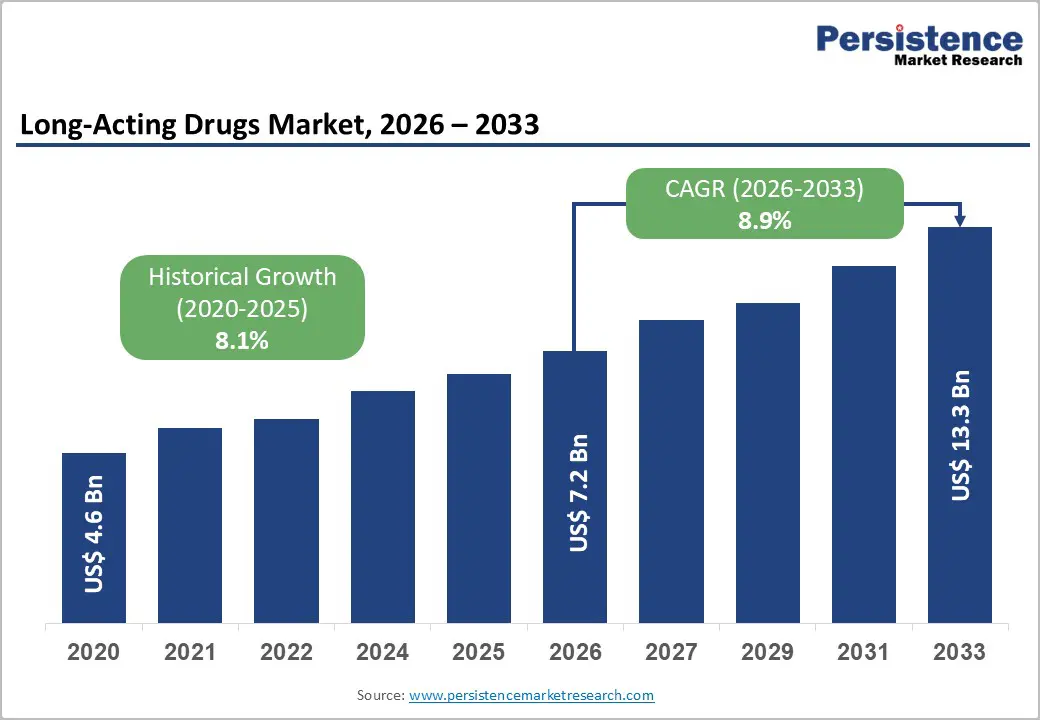

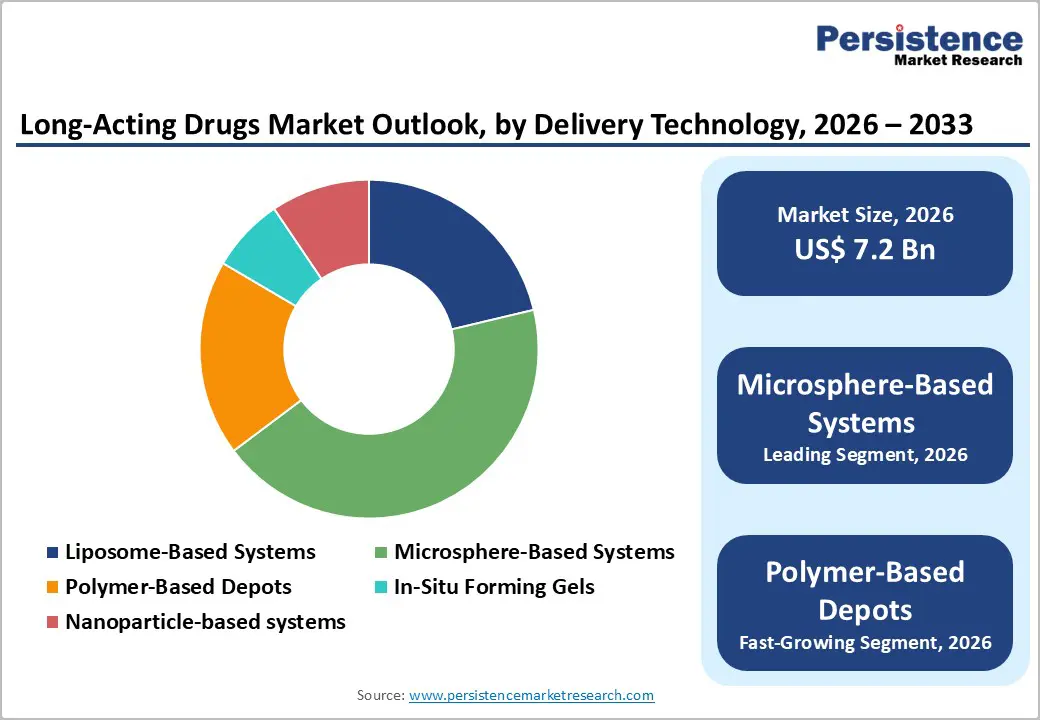

The global long-acting drugs market is estimated to grow from US$ 7.2 Bn in 2026 to US$ 13.3 Bn by 2033. The market is projected to record a CAGR of 8.9% during the forecast period from 2026 to 2033.

The global long-acting drugs market is witnessing strong growth, driven by the rising need for improved patient compliance, reduced dosing frequency, and better treatment outcomes in chronic diseases. Increasing prevalence of conditions such as cancer, diabetes, cardiovascular disorders, and psychiatric illnesses is accelerating the adoption of long-acting formulations. Technological advancements in drug delivery systems, including liposomes, microspheres, implants, and polymer-based depots, are expanding the therapeutic potential of these drugs. North America dominates the market due to high healthcare expenditure, strong regulatory support, and the presence of leading pharmaceutical players, while Asia Pacific is rapidly emerging with growing healthcare access, expanding patient pool, and rising investments in innovative drug delivery research.

Key Industry Highlights

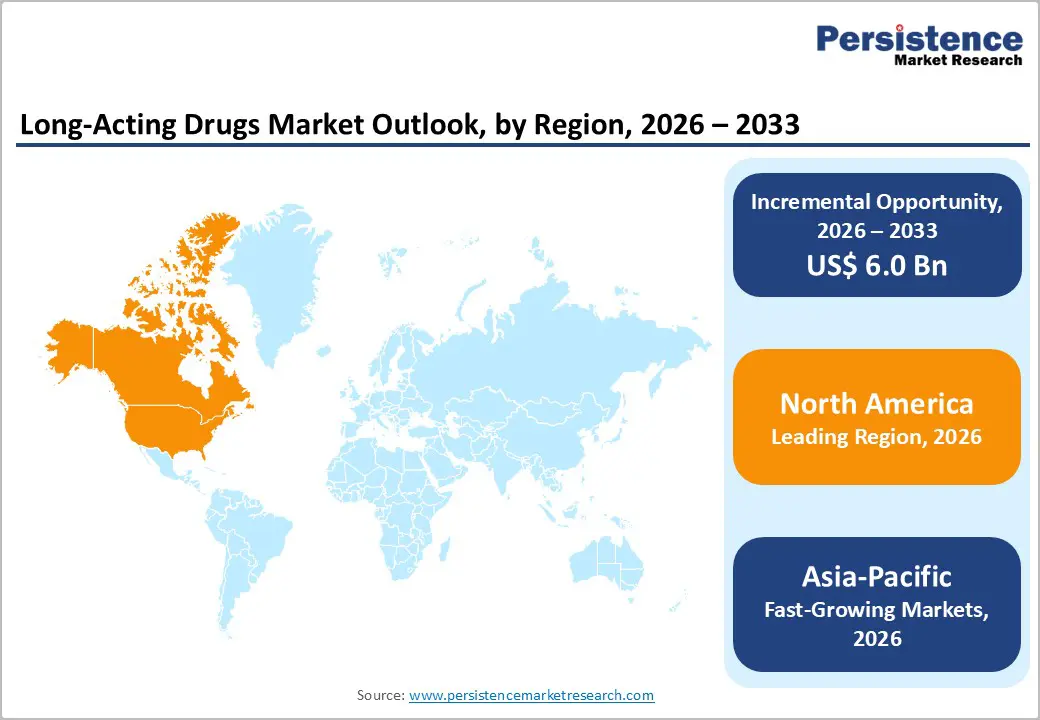

- Leading Region: North America, holding nearly 41.2% market share in 2025, supported by advanced drug delivery research, strong pharmaceutical pipelines, and favorable FDA approvals for extended-release formulations.

- Fastest-growing Region: Asia Pacific, fueled by rising prevalence of chronic diseases, government initiatives for affordable therapies, and expanding clinical trials in countries such as China, India, and South Korea.

- Investment Plans: Europe, focusing on innovation in sustained-release technologies, with support from Horizon Europe funding, cross-border R&D collaborations, and multi-million-euro projects targeting oncology and CNS long-acting therapies.

- Dominant Delivery Technology: Microsphere-Based Systems, capturing nearly 43.5% share, due to their ability to provide controlled, sustained release for oncology, hormonal, and CNS therapies, improving patient compliance and treatment outcomes.

- Leading Therapeutic Area: Cancer treatment, accounting for over 37.7% of market revenue, driven by high demand for long-acting chemotherapeutics, targeted therapies, and supportive care drugs reducing treatment burden.

| Global Market Attributes | Key Insights |

|---|---|

| Global Long-Acting Drugs Market Size (2026E) | US$ 7.2 Bn |

| Market Value Forecast (2033F) | US$ 13.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.1% |

Market Dynamics

Driver – Polymer Depots Tackling CNS Disorders and HIV

Polymer depot systems represent a significant driver in the long-acting drugs market as they provide a reliable platform for sustained and controlled drug delivery. These formulations use biodegradable polymers, such as poly(lactic-co-glycolic acid) (PLGA), to encapsulate active pharmaceutical ingredients and release them steadily over weeks or months.

This technology is particularly impactful in central nervous system (CNS) disorders and infectious diseases like HIV, where treatment adherence is a persistent challenge. In conditions such as schizophrenia or bipolar disorder, polymer-based long-acting injectables help maintain stable plasma levels, reducing relapse risk and hospitalization caused by poor adherence to oral medication. Similarly, in HIV management, long-acting polymer depots are revolutionizing treatment by reducing the burden of daily pills.

A recent example is cabotegravir (Apretude, developed by ViiV Healthcare), which uses an injectable long-acting suspension that offers protection against HIV for two months per dose. Clinical trials have shown it significantly improves adherence and prevention outcomes compared to daily oral PrEP regimens.

As these depot technologies continue to expand into other therapeutic areas, they are driving the demand for long-acting drugs by enhancing patient convenience, reducing healthcare costs, and improving overall treatment outcomes. Moreover, ongoing innovations in polymer science are enabling customizable release profiles, expanding possibilities for precision medicine.

Restraints – Balancing Sterility Assurance with Suspension Stability in Complex LAI Systems

One of the most unique challenges in the development and commercialization of long-acting injectable (LAI) products lies in the delicate balance between ensuring sterility and maintaining suspension stability across the entire product lifecycle. Unlike conventional injectables, LAIs often contain micronized or crystalline drug particles dispersed in specialized vehicles, which are prone to sedimentation, agglomeration, Ostwald ripening, and caking during storage.

While terminal sterilization methods such as gamma irradiation or steam offer robust microbial inactivation, they can significantly compromise the physicochemical integrity of sensitive drug molecules and excipients, leading to altered particle size distribution, loss of suspension homogeneity, or even degradation.

To address this, manufacturers often resort to aseptic processing, which minimizes sterilization stress but heightens the risk of bioburden control failures and demands costly cleanroom operations with rigorous in-process controls. The introduction of stabilization strategies such as lyophilization into reconstitutable powders or the use of thixotropic excipients like PEG and PVP adds another layer of complexity: while they improve suspension stability and syringeability, they also impose challenges in scalability, excipient regulatory acceptance, and reproducibility of performance across batches.

This interplay of sterility assurance, suspension stability, and manufacturability makes the development of LAIs uniquely vulnerable to both technical failure and regulatory scrutiny, slowing market entry and increasing costs.

Opportunity – Oral Biologic & Peptide Delivery via Long-Acting Formulations

Developing oral long-acting biologic and peptide formulations particularly GLP-1 agonists and insulin analogs presents a transformative market opportunity. These products rely on protective coatings and absorption-enhancing excipients that safeguard peptide payloads from gastric degradation while boosting intestinal uptake.

Notable strategies include utilization of permeation enhancers like SNAC, which enabled oral semaglutide (Rybelsus) to reach meaningful bioavailability despite being a peptide a breakthrough that paved the way for oral biologics. The sustained-release profile can be optimized via controlled-release matrices or nanoparticle encapsulation, maintaining therapeutic levels over days and drastically improving convenience and compliance.

A recent concrete example is Eli Lilly’s orforglipron, a small-molecule (non-peptide) GLP-1 receptor agonist designed for oral daily dosing. In a pivotal Phase III trial involving over 1,600 overweight patients with type 2 diabetes, orforglipron delivered an average body-weight reduction of 10.5% over 72 weeks, plus improved A1C control offering efficacy close to injectables, but in pill form.

This highlights how long-acting technology coatings, enhancers, and molecular design can bridge the gap between injectable biologics and oral convenience. As the broader obesity and diabetes markets seek needle-free, long-lasting therapies, formulation innovations underpinning orforglipron and Rybelsus represent potent, scalable opportunities with significant commercial and adherence advantages.

Category-wise Analysis

By Delivery Technology, Microsphere-Based Systems dominates the Long-Acting Drugs Market

Microsphere-Based Systems lead the delivery technology category in the market because they offer controlled and sustained drug release, improving therapeutic efficacy and patient adherence. Their small, biodegradable polymer particles can encapsulate drugs and release them gradually over days, weeks, or months, reducing dosing frequency. This technology is highly versatile, applicable across oncology, hormonal therapies, CNS disorders, and infectious diseases, and compatible with injectable formulations. Additionally, microspheres enhance drug stability, bioavailability, and targeting, minimizing side effects. Regulatory familiarity and widespread clinical adoption further strengthen their dominance, making them the preferred choice for developers aiming to balance efficacy, safety, and patient convenience in long-acting therapies.

By Therapeutic Area, Cancer is gaining traction due to high prevalence, mortality, and sustained treatments

Cancer is the leading therapeutic area in the market due to its high global prevalence, significant mortality, and the need for effective, patient-friendly treatments. According to the World Health Organization, an estimated 20 million new cancer cases and 9.7 million deaths occurred globally in 2022, with lung, breast, and colorectal cancers being most common. In India, over 1.4 million new cases were reported in 2023, highlighting urgent treatment needs. Long-acting drug delivery systems, such as microsphere-based formulations, offer sustained release, improved bioavailability, and reduced dosing frequency, enhancing patient adherence. Government initiatives, including India’s Production Linked Incentive (PLI) Scheme for pharmaceuticals, further support accessibility. These factors collectively drive the dominance of cancer in the long-acting drugs market.

Regional Insights

North America Long-Acting Drugs Market Trends

North America region in the market with 41.2% share in 2025, particularly the U.S., leads the long-acting drugs market due to its advanced healthcare infrastructure, high healthcare expenditure, and strong regulatory support. The region faces a growing burden of chronic diseases, including diabetes, schizophrenia, and HIV, creating a critical need for sustained and effective treatments. According to the CDC, over 37 million Americans have diabetes, highlighting the demand for long-acting therapies that improve adherence and outcomes. FDA-approved long-acting injectables, such as aripiprazole and paliperidone, demonstrate the region’s adoption of innovative drug delivery systems, including microsphere-based technologies and in-situ forming gels. Favorable reimbursement policies and insurance coverage further support patient access, making North America the dominant market for long-acting drugs.

Europe Long-Acting Drugs Market Trends

Europe is a major region in the market with 27.5% share in 2025, driven by an aging population, increasing prevalence of chronic diseases, and advancements in drug delivery technologies. The European Medicines Agency (EMA) has approved several long-acting injectable medications, including treatments for conditions such as HIV and schizophrenia, reflecting a commitment to improving patient adherence and outcomes. For instance, the EMA's approval of injectable lenacapavir, administered twice yearly, has been highlighted as a significant advancement in HIV prevention. Additionally, the European Union's regulatory framework, including the Clinical Trials Regulation (CTR) introduced in January 2022, aims to streamline processes and enhance the development of innovative therapies. These initiatives underscore Europe's leadership in adopting long-acting drug delivery systems to address evolving healthcare needs.

Asia Pacific Long-Acting Drugs Market Trends

Asia Pacific is emerging as the fastest-growing region in the market, driven by increasing healthcare demands, expanding access to healthcare services, and supportive government policies. Countries like India and China are witnessing a rise in chronic diseases such as diabetes and hypertension, leading to a greater need for sustained-release medications. For instance, the Indian Council of Medical Research reported over 77 million adults with diabetes in India, highlighting the demand for effective long-term treatment options. Additionally, the Chinese government's initiatives to enhance healthcare infrastructure and promote innovation in drug delivery systems are fostering the development and adoption of long-acting therapies. These factors collectively contribute to the rapid growth of the long-acting drugs market in the Asia Pacific region.

Market Competitive Landscape

The global market is growing as players develop advanced delivery technologies like microsphere-based systems and polymer depots, expand therapeutic portfolios, and form strategic collaborations. Established firms focus on enhancing sustained-release performance and patient compliance, while emerging companies target niche indications and novel formulations. Partnerships, mergers, and regional expansion strengthen competitiveness, driving adoption across oncology, CNS disorders, hormone therapies, and infectious disease management.

Key Industry Developments:

- In February 2026, Novartis announced that it had broken ground on a new global biomedical research center in San Diego, marking a strategic expansion of its research and development footprint in the United States. The facility was designed to strengthen the company’s early-stage drug discovery capabilities and enhance collaboration across scientific disciplines.

- In December 2025, Tolmar announced that it had opened a new laboratory facility in Northern Illinois, located within Rosalind Franklin University’s Innovation and Research Park. The expansion was aimed at strengthening the company’s research and development capabilities and fostering closer collaboration with academic and scientific communities.

- In July 2025, Novartis received FDA approval for Leqvio® (inclisiran) as a first-line monotherapy option for LDL-C reduction, enabling use without statins. Its twice-yearly dosing cements its role as a pioneering long-acting siRNA therapy, addressing persistent gaps in cholesterol management.

- In July 2025, Pacira entered a strategic co-promotion partnership with Johnson & Johnson MedTech for ZILRETTA®, its extended-release corticosteroid injection for knee osteoarthritis. By leveraging J&J’s extensive “early intervention” sales force, the deal expands patient access and reinforces Pacira’s leadership in sustained-release, non-opioid pain therapies designed to reduce reliance on opioids.

- In April 2025, Johnson & Johnson received FDA approval for IMAAVY™, a human FcRn-blocking monoclonal antibody, for the treatment of generalized myasthenia gravis in adults and pediatric patients aged 12 and older.

- In February 2025, the FDA approved key updates to the SUBLOCADE® label, enabling rapid initiation patients can start therapy as soon as one hour after a single transmucosal buprenorphine dose and utilize multiple subcutaneous injection sites (abdomen, thigh, buttock, upper arm). This improves treatment timeliness and flexibility.

Companies Covered in Long-Acting Drugs Market

- Janssen Pharmaceutica NV (Johnson & Johnson)

- Novartis AG

- Teva Pharmaceutical Industries Ltd

- ViiV HEALTHCARE

- Alkermes

- Tolmar, Inc

- Pacira Pharmaceuticals, Inc.

- Indivior PLC

- AstraZeneca

- Jazz Pharmaceuticals plc

- Ipsen Pharma

- Gilead Sciences, Inc.

- Organon USA Inc.

- Endo, Inc.

- Bristol-Myers Squibb Company

- Verity Pharmaceuticals, Inc.

Frequently Asked Questions

The global Market is projected to be valued at US$ 7.2 Bn in 2026.

Rising chronic disease prevalence, patient compliance needs, and advancements in sustained-release drug delivery technologies.

The Global market is poised to witness a CAGR of 8.9% between 2026 and 2033.

Expansion in oncology, CNS, hormone therapies, emerging markets, and innovation in novel long-acting formulations.

Major players in the global are Janssen Pharmaceutica NV (Johnson & Johnson), Novartis AG, Teva Pharmaceutical Industries Ltd, ViiV Healthcare, Alkermes, Tolmar, Inc. and others