- Medical Devices

- Immunoturbidimetric Kits Market

Immunoturbidimetric Kits Market Size, Share, and Growth Forecast, 2026 - 2033

Immunoturbidimetric Kits Market by Analyte Type (Cardiac Markers, Renal Markers, Others), Platform (Standalone Benchtop Analyzers, Others), End-user (Hospital Laboratories, Reference Labs, Others), and Regional Analysis for 2026 – 2033

Immunoturbidimetric Kits Market Size and Trends Analysis

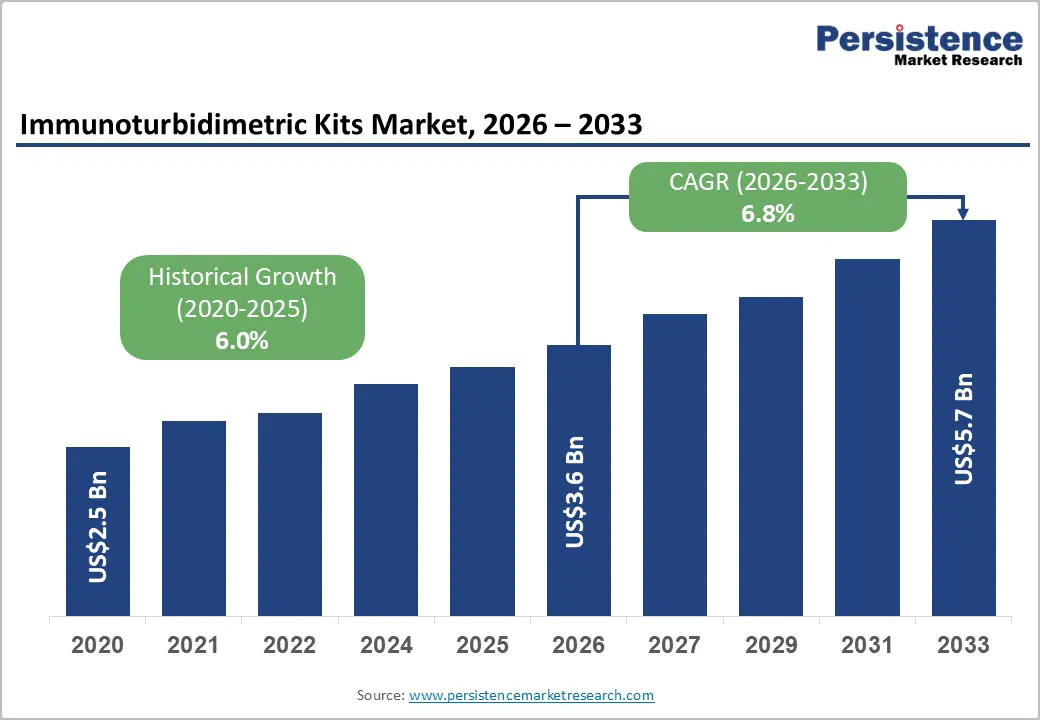

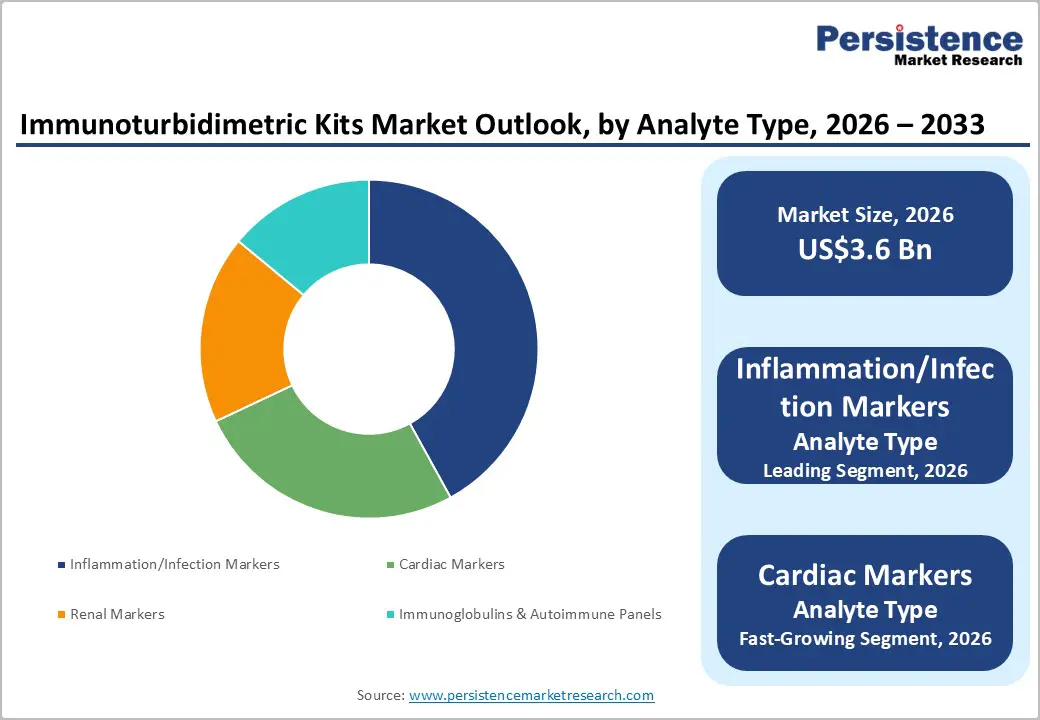

The global immunoturbidimetric kits market size is likely to be valued at US$3.6 billion in 2026, and is expected to reach US$5.7 billion by 2033, growing at a CAGR of 6.8% during the forecast period from 2026 to 2033, driven by the increasing prevalence of chronic and inflammatory diseases requiring routine protein biomarker monitoring, rising demand for high-throughput, cost-effective turbidimetric assays on automated analyzers, growing adoption of cardiac and renal marker panels in hospital and reference laboratories, and expanding point-of-care testing capabilities in physician offices and clinics. Increasing recognition of immunoturbidimetric kits as critical for accurate quantification of CRP, ferritin, immunoglobulins, and other acute-phase proteins in emerging chronic disease screening and infectious disease management markets remains a major driver of market growth.

Key Industry Highlights:

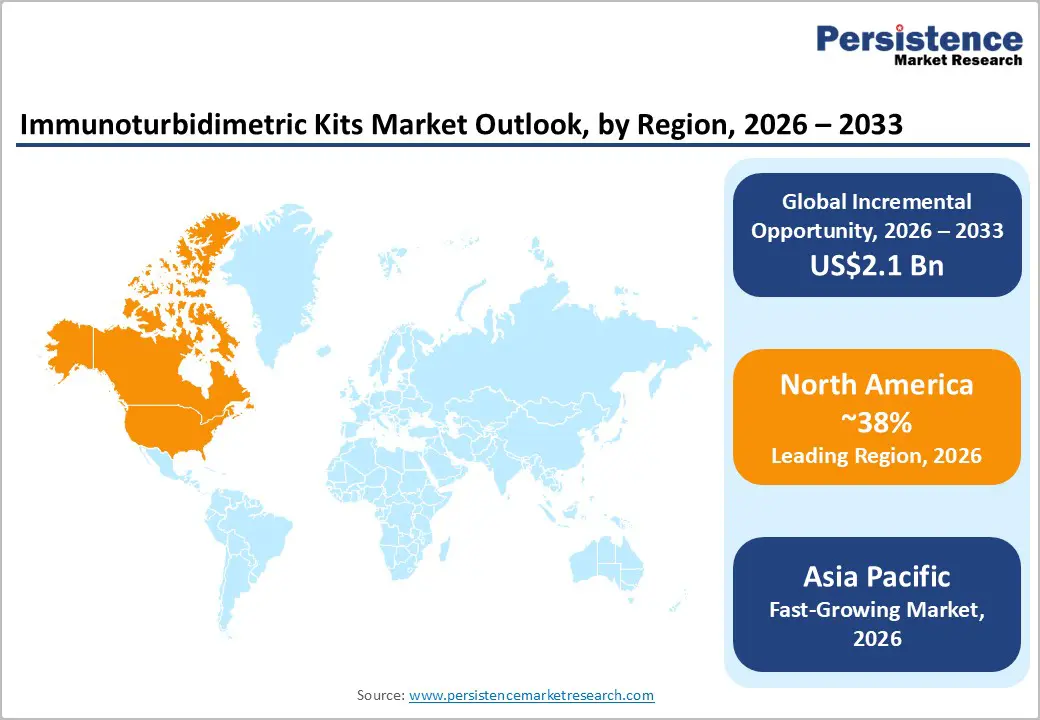

- Leading Region: North America, anticipated to account for a 38% market share in 2026, driven by high chronic disease burden, advanced lab infrastructure, and strong demand in the U.S.

- Fastest-growing Region: Asia Pacific, fueled by rising healthcare expenditure, expanding hospital networks, and increasing chronic disease screening in China and India.

- Dominant Analyte Type: Inflammation/Infection Markers, to hold approximately 42% of the market share, as CRP and procalcitonin remain the highest-volume assays.

- Leading Platform: Automated chemistry analyzers, contributing nearly 58% of the market revenue, due to the highest integration in high-throughput labs.

| Key Insights | Details |

|---|---|

|

Immunoturbidimetric Kits Market Size (2026E) |

US$3.6 Bn |

|

Market Value Forecast (2033F) |

US$5.7 Bn |

|

Projected Growth CAGR (2026-2033) |

6.8% |

|

Historical Market Growth (2020-2025) |

6.0% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Increasing Chronic Disease Burden and High-Throughput Lab Automation

The growing prevalence of chronic diseases has increased the need for reliable and routine clinical testing, which directly supports the adoption of immunoturbidimetric kits in diagnostic laboratories. Chronic conditions such as cardiovascular disorders, diabetes, and inflammatory diseases require continuous monitoring of biomarkers, including C-reactive protein, immunoglobulins, and specific proteins measured through immunoturbidimetric assays. These tests enable laboratories to provide rapid and quantitative results that support disease diagnosis, therapy monitoring, and risk assessment. According to the World Health Organization, noncommunicable diseases caused about 43 million deaths globally in 2021, representing around 75% of all non-pandemic deaths, highlighting the expanding patient pool that requires routine diagnostic testing.

Advancements in high-throughput laboratory automation further accelerate the adoption of immunoturbidimetric kits across modern clinical laboratories. Automated analyzers integrated with immunoturbidimetric assays enable laboratories to process large sample volumes with consistent quality, reduced manual intervention, and faster turnaround times. This efficiency is essential for healthcare systems managing large populations with chronic conditions that require frequent biochemical monitoring. Government health statistics indicate that noncommunicable diseases account for roughly 75% of deaths worldwide, demonstrating the scale of diagnostic testing required to support disease management programs.

Developing Point-of-Care and Physician Office Testing

The expansion of decentralized diagnostic services in physician offices and near-patient settings is increasing the demand for rapid and easy-to-use testing technologies. Immunoturbidimetric kits support this trend through their compatibility with compact analyzers and automated clinical chemistry systems used in outpatient clinics and physician office laboratories. These kits enable quantitative detection of proteins and biomarkers in a short turnaround time, supporting immediate clinical decision-making during patient visits. The growing acceptance of point-of-care diagnostics among primary healthcare providers also supports the expansion of immunoturbidimetric testing solutions.

Physician-office laboratories require diagnostic methods that integrate easily with small clinical chemistry platforms while maintaining analytical accuracy for routine biomarker assessment. Immunoturbidimetric assays meet this need through automated measurement of parameters such as C-reactive protein, immunoglobulins, and other protein markers used in chronic disease monitoring. A community-based survey across 45 districts in India reported that about 25% of primary healthcare providers already use point-of-care diagnostic tests, demonstrating the increasing role of decentralized testing in routine healthcare delivery.

Barrier Analysis – High Instrument Dependency and Reimbursement Pressures

Clinical laboratories rely on compatible automated chemistry analyzers to perform immunoturbidimetric testing, creating a strong dependency on specialized instrumentation. Many small and mid-sized diagnostic laboratories operate with limited capital budgets, which restricts the ability to procure or upgrade high-performance analyzers required for these assays. Instrument calibration, maintenance, and integration with laboratory information systems also add operational complexity.

Pricing pressure from reimbursement systems also constrains revenue growth for immunoturbidimetric testing. Diagnostic laboratories operate under strict reimbursement frameworks set by public health programs and insurance providers, which often limit payment for routine laboratory tests. When reimbursement levels remain low, laboratories prioritize high-volume tests with favorable margins and reduce spending on additional assay panels.

Competition from Alternative Technologies

Diagnostic laboratories are increasingly adopting advanced analytical technologies that offer higher sensitivity and broader testing capabilities, which limits the demand for immunoturbidimetric kits. Methods such as chemiluminescent immunoassays, enzyme-linked immunosorbent assays, and molecular diagnostic platforms provide enhanced detection performance for certain biomarkers and disease conditions. Large hospital laboratories often prefer these technologies for specialized testing, particularly in areas requiring ultra-low detection limits or multiplex biomarker analysis.

Technology advancement across clinical diagnostics also increases competitive pressure on traditional protein measurement methods. Many modern immunoassay platforms integrate automation, digital data management, and multi-analyte testing capabilities within a single system. These platforms allow laboratories to consolidate multiple assays on one instrument, improving operational efficiency and workflow management.

Opportunity Analysis – Advancements in Inflammation and Infection Marker Panels

Advances in biomarker research and panel-based diagnostic testing are expanding the clinical use of inflammation and infection markers, creating strong opportunities for immunoturbidimetric kits. Healthcare providers increasingly rely on panels that measure proteins such as C-reactive protein (CRP), immunoglobulins, and complement proteins to support early diagnosis and disease monitoring. Immunoturbidimetric assays are widely used in clinical laboratories to quantify these proteins with rapid turnaround and high analytical precision. CRP is one of the most used markers of systemic inflammation and infection in clinical practice, and its measurement is routinely performed in hospital laboratories to evaluate inflammatory responses and disease severity.

Growing clinical focus on infection severity assessment and patient monitoring further increases demand for multi-marker inflammatory panels. Research evidence shows that systemic inflammation identified through CRP testing is strongly associated with infection outcomes, with elevated CRP levels indicating a higher risk of infection-related mortality. Inflammatory biomarkers such as CRP, interleukin-6, and tumor necrosis factor are also used together to assess disease severity in infectious conditions, strengthening the clinical importance of panel-based testing strategies.

Category-wise Analysis

Analyte Type Insights

Inflammation/Infection Markers are anticipated to dominate the market, accounting for 42% of the market share in 2026. Their dominance is driven by their extensive use in routine clinical diagnostics. Biomarkers such as C-reactive protein (CRP), immunoglobulins, and complement proteins are frequently measured to detect infections, evaluate inflammatory conditions, and monitor treatment response. Hospitals and diagnostic laboratories rely on these tests for rapid clinical assessment in conditions such as sepsis, autoimmune disorders, and respiratory infections. High-sensitivity C-reactive protein (CRP) immunoturbidimetric assay developed by Roche Diagnostics. The company introduced a CRP (Latex) high-sensitivity immunoturbidimetric test system designed for use on automated clinical chemistry analyzers such as the cobas platforms.

Cardiac markers represent the fastest-growing analyte type, due to increasing demand for early detection and monitoring of cardiovascular conditions. Biomarkers such as cardiac troponin, creatine kinase-MB (CK-MB), and C-reactive protein are widely used in hospitals and emergency departments to assess myocardial injury and cardiac risk. The rising incidence of heart disease has increased the routine testing of these markers in clinical laboratories. Siemens Healthineers CK-MB Mass cardiac biomarker assay, designed for use on its clinical diagnostic platforms such as the Atellica and Dimension systems. The test measures the creatine kinase-MB (CK-MB) isoenzyme, a key cardiac marker used to support the diagnosis of acute myocardial infarction (heart attack) in hospital laboratories and emergency settings.

Platform Insights

Automated chemistry analyzers are expected to dominate the market, contributing nearly 58% of revenue in 2026, fueled by their extensive use in high-volume clinical laboratories. These systems enable laboratories to perform multiple biochemical and protein-based assays with minimal manual handling, improving efficiency and turnaround time. Immunoturbidimetric tests for biomarkers such as C-reactive protein, immunoglobulins, and complement proteins are commonly integrated into automated chemistry platforms. cobas® clinical chemistry analyzer series developed by F. Hoffmann-La Roche Ltd. Systems such as the cobas c 311 and cobas c 111 automated chemistry analyzers are widely used in hospitals and diagnostic laboratories to perform routine biochemical and protein-based assays, including immunoturbidimetric tests.

Compact/POC systems represent the fastest-growing platform, increasing demand for rapid diagnostic testing outside centralized laboratories. These systems enable physicians and healthcare providers to perform biomarker testing directly in clinics, emergency departments, and outpatient settings. Compact analyzers require minimal laboratory infrastructure and deliver quick results, supporting faster clinical decision-making during patient visits. The Microsemi CRP point-of-care analyzer was developed by HORIBA Medical. The Microsemi CRP is a compact near-patient diagnostic system designed to measure C-reactive protein (CRP) and perform a full blood count (FBC) using a very small whole-blood sample.

Regional Insights

North America Immunoturbidimetric Kits Market Trends

North America is expected to dominate, accounting for 38% of the revenue in 2026, fueled by advanced clinical laboratory infrastructure, high diagnostic testing volumes, and widespread adoption of automated chemistry analyzers. Hospitals and reference laboratories in the U.S. and Canada routinely use immunoturbidimetric assays to measure protein biomarkers such as C-reactive protein, immunoglobulins, and complement proteins for infection, inflammation, and chronic disease monitoring. The region benefits from strong regulatory oversight and standardized laboratory practices that support reliable diagnostic testing. In the U.S., clinical laboratories must comply with the Clinical Laboratory Improvement Amendments (CLIA), which establish national quality standards to ensure accuracy, reliability, and timeliness of diagnostic test results across laboratories performing human specimen testing.

Regulatory approval pathways for in-vitro diagnostic assays also influence market development in North America. The U.S. Food and Drug Administration (FDA) requires manufacturers of diagnostic tests to obtain regulatory clearance, such as the 510(k) premarket notification, before marketing many in vitro diagnostic devices. A relevant case occurred in 2023 when ALPCO received FDA 510(k) clearance for its Calprotectin Immunoturbidimetric Assay, designed to help diagnose inflammatory bowel disease and differentiate it from irritable bowel syndrome.

Europe Immunoturbidimetric Kits Market Trends

Europe is witnessing steady growth in the immunoturbidimetric kits market due to the expansion of advanced clinical laboratories, increasing diagnostic testing for inflammatory and chronic diseases, and strong regulatory frameworks governing in vitro diagnostics. Hospitals and diagnostic centers across countries such as Germany, France, and the U.K. routinely use immunoturbidimetric assays to quantify proteins such as C-reactive protein, immunoglobulins, and complement components. These assays support clinical decision-making in infection monitoring, autoimmune disorders, and cardiovascular risk assessment. The European healthcare system places significant emphasis on laboratory diagnostics, with estimates indicating that around 70% of clinical decisions rely on in-vitro diagnostic (IVD) test results, highlighting the critical role of laboratory assays in patient management.

The European diagnostics market is governed by the In Vitro Diagnostic Regulation (IVDR), adopted by the European Parliament to regulate the development, approval, and commercialization of diagnostic devices. The regulation replaced the earlier In Vitro Diagnostic Directive and became fully applicable in May 2022, introducing stricter risk classification, enhanced clinical performance evaluation, and stronger post-market surveillance requirements for diagnostic products. Under the IVDR framework, most in-vitro diagnostic devices, including reagent kits used for protein biomarker testing, require assessment by notified bodies before market entry.

Asia Pacific Immunoturbidimetric Kits Market Trends

Asia Pacific is likely to be the fastest-growing region in 2026, supported by rapid growth in healthcare infrastructure, increasing diagnostic testing volumes, and rising awareness of early disease detection. Countries such as China, India, Japan, and South Korea are strengthening laboratory networks and investing in advanced clinical chemistry analyzers that support protein-based biomarker testing. Immunoturbidimetric assays are widely used in hospitals and diagnostic laboratories to measure inflammatory markers, immunoglobulins, and other proteins associated with chronic diseases and infections. The growing burden of infectious diseases and lifestyle-related conditions has increased the need for routine laboratory monitoring across the region.

Regulatory frameworks established by governments across the region play an important role in ensuring the quality and safety of diagnostic kits. In India, in-vitro diagnostic (IVD) kits are regulated under the Drugs and Cosmetics Act and the Medical Devices Rules, 2017, with oversight from the Central Drugs Standard Control Organization (CDSCO) under the Ministry of Health and Family Welfare. These rules govern the import, manufacturing, sale, and clinical performance evaluation of diagnostic reagents used in laboratories.

Competitive Landscape

The global immunoturbidimetric kits market is characterized by competition between large in-vitro diagnostics (IVD) manufacturers and specialized reagent providers that focus on specific biomarker assays. Established companies such as Siemens Healthineers and F. Hoffmann-La Roche Ltd maintain strong market positions in North America and Europe through integrated diagnostic ecosystems that combine automated chemistry analyzers with broad reagent menus. Their strong relationships with hospitals and reference laboratories support the adoption of immunoturbidimetric assays used for inflammation, infection, and cardiac biomarker testing.

In the Asia Pacific region, regional manufacturers and reagent suppliers compete by offering cost-efficient diagnostic kits that improve access to routine biomarker testing in emerging healthcare systems. Increasing demand for inflammation and infection markers is encouraging companies to expand assay portfolios designed for rapid protein measurement and high-throughput laboratory workflows. Industry participants are also pursuing strategic collaborations, partnerships, and acquisitions to strengthen product development capabilities and accelerate commercialization.

Key Industry Developments:

- In November 2023, F. Hoffmann-La Roche Ltd launched the Elecsys® Anti-HEV IgM and Elecsys® Anti-HEV IgG immunoassays in CE–mark–accepting countries to detect hepatitis E virus (HEV) infections. The assays enabled clinicians to identify HEV as the cause of patient symptoms, support appropriate treatment decisions, and monitor disease progression to prevent severe outcomes through timely antiviral therapy.

- In 2023, DiaSys Diagnostic Systems GmbH introduced new clinical chemistry reagents, including Cystatin C FS, Procalcitonin FS, CRP FS, HDL-c direct FS, and LDL-c direct FS. The company designed several of these assays as immunoturbidimetric reagents compatible with multiple automated chemistry analyzers, strengthening cardiovascular and infection biomarker testing capabilities in clinical laboratories.

Companies Covered in Immunoturbidimetric Kits Market

- DiaSys Diagnostic Systems GmbH

- Creative Diagnostics

- MTI Diagnostics

- Biogenix Inc. Pvt. Ltd.

- Reckon Diagnostics Pvt. Ltd.

- Siemens Healthineers

- F. Hoffmann-La Roche Ltd

- Randox Laboratories Ltd.

- Diazyme Laboratories, Inc.

- FUJIFILM Wako Chemicals Europe GmbH

Frequently Asked Questions

The global immunoturbidimetric kits market is projected to reach US$3.6 billion in 2026.

Rising chronic disease burden and high-throughput lab automation are key drivers.

The immunoturbidimetric kits market is poised to witness a CAGR of 6.8% from 2026 to 2033.

Multiplexed inflammation/infection marker panels and expansion in Asia Pacific and POC/physician office settings are key opportunities.

Siemens Healthineers, F. Hoffmann-La Roche Ltd, Randox Laboratories Ltd., DiaSys Diagnostic Systems GmbH, and Diazyme Laboratories, Inc. are the key players.