- Industrial Machinery

- Hydraulic Insertion Machine Market

Hydraulic Insertion Machine Market Size, Share, and Growth Forecast 2026 - 2033

Hydraulic Insertion Machine Market by Machine Type (Fully Automatic Hydraulic Insertion Machines, Semi-Automatic Hydraulic Insertion Machines, Manual Hydraulic Insertion Machines), Operation Type (Hydraulic Press-Fit Insertion, Servo-Hydraulic Insertion, Pneumatic-Hydraulic Hybrid Insertion), Application, End-user, and Regional Analysis, 2026 - 2033

Hydraulic Insertion Machine Market Size and Trend Analysis

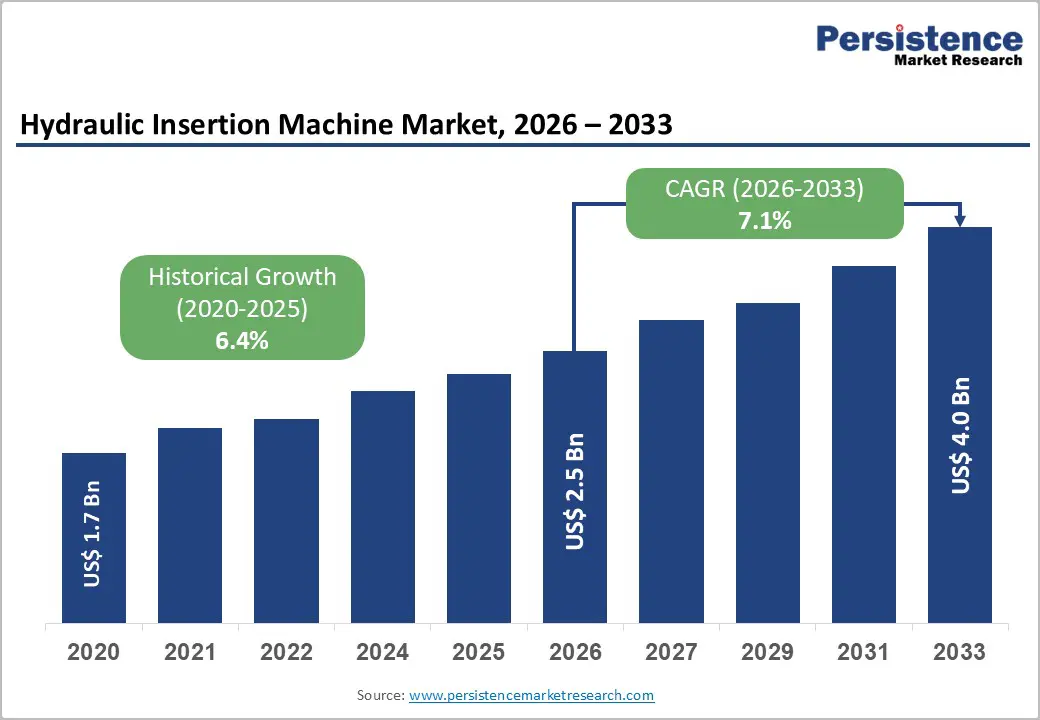

The global hydraulic insertion machine market is expected to be valued at US$ 2.50 billion in 2026 and is projected to reach US$ 4.04 billion by 2033, growing at a CAGR of 7.1% between 2026 and 2033.

Accelerating electrification across the automotive and aerospace sectors is restructuring capital equipment procurement cycles, placing precision press-fit assembly systems at the centre of production line upgrade decisions worldwide.

Key Industry Highlights:

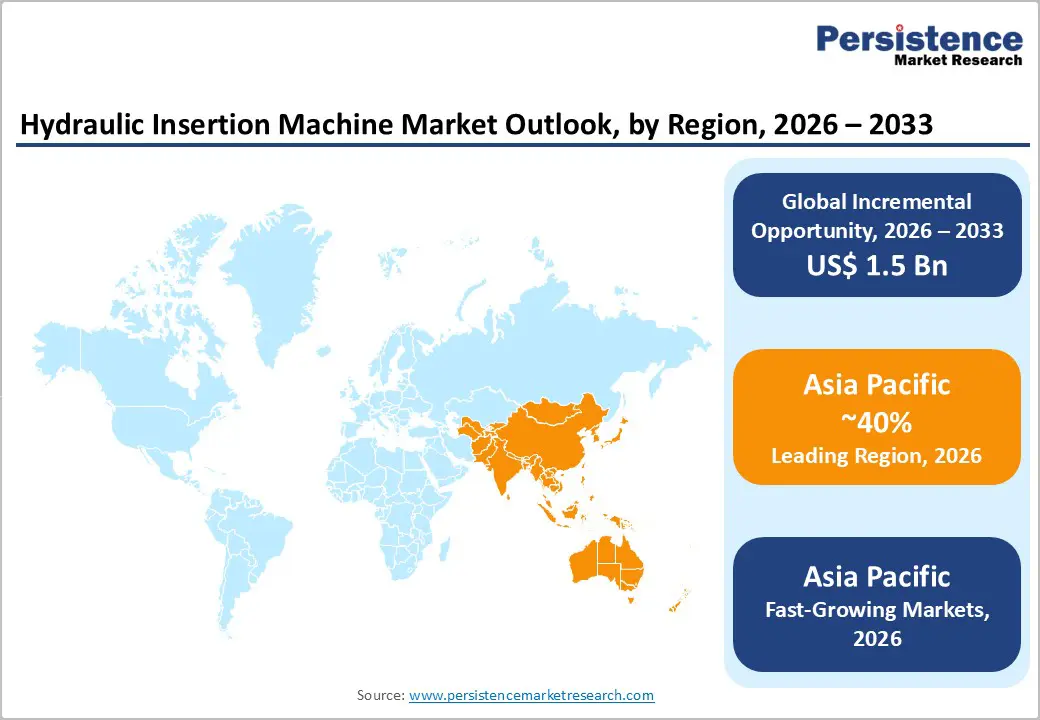

- Leading Region: Asia Pacific leads the global hydraulic insertion machine market with a 40.0% revenue share in 2026, equivalent to US$ 1.00 Billion, driven by China's vehicle production volumes exceeding 30 Million units annually and India's PLI-backed automotive component manufacturing expansion.

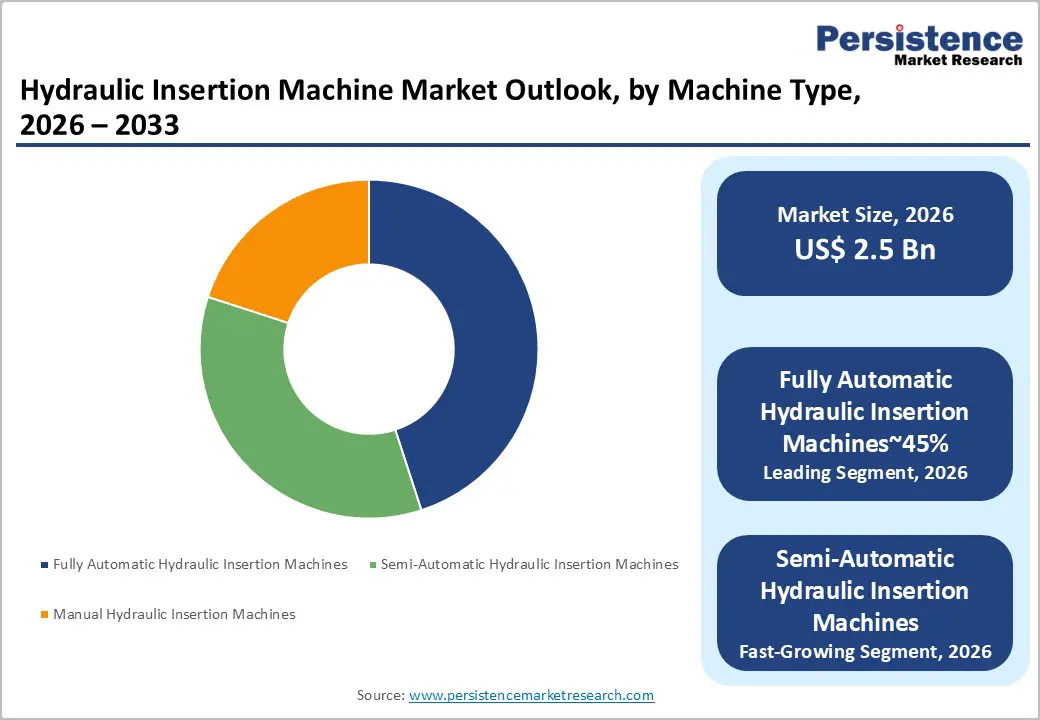

- Leading Segment: Fully automatic hydraulic insertion machines dominate machine type segmentation at 45% share, reflecting automotive OEM mandates for sub-8-second bushing insertion cycle times and Cpk process capability requirements that eliminate semi-automatic or manual alternatives from safety-critical assembly lines; this segment's technical entry barrier ensures structural stability against low-cost substitution through the forecast horizon.

- Fast-Growing Segment: Semi-automatic hydraulic insertion machines are the fast-growing machine type segment, with electronics contract manufacturers across Vietnam and Thailand adopting guided hydraulic press stations for connector and heat-sink insertion on server and networking hardware motherboards, a use case validated by Foxconn's 2023 capacity expansion and set to broaden as IPC-A-620 workmanship standard revisions tighten force-insertion specification requirements for high-density interconnect assemblies.

- Key Opportunity: The integration of IoT-enabled hydraulic force control systems into insertion platforms represents the highest-value strategic opportunity in the market between 2026 and 2033, with premium-tier connected platforms commanding price premiums up to 25% over conventional analogue machines.

Market Dynamics

Driver - Surge in Electric Vehicle Platform Investment Compelling High-Force Press-Fit Automation

Automotive OEMs retooling for battery electric vehicle architectures require hydraulic force control systems capable of inserting bushing arrays and stator bearings into aluminium housings at tolerances below ±0.02 mm, a standard that manual or pneumatic alternatives cannot reliably meet at scale.

The U.S. Inflation Reduction Act of 2022 allocated US$ 369 billion toward clean energy manufacturing incentives, prompting General Motors to commit US$ 7 Billion to domestic EV plant upgrades through 2025, each facility requiring new-generation industrial hydraulic equipment lines. Over the next two to three years, every major EV skateboard platform retooling cycle will generate a discrete, multi-unit procurement event for servo-hydraulic insertion and automated assembly machinery suppliers with proven process validation credentials.

Industrial Re-Shoring and Factory Modernisation Driving Capex in Precision Insertion Equipment

Governments across North America and Europe are actively subsidising domestic industrial machinery investment, creating a structural capex tailwind for hydraulic insertion machine procurement that bypasses typical budget deferral cycles. Germany's Federal Ministry for Economic Affairs and Climate Action approved €1 Billion under the Zukunftsinvestitionen programme in 2023, prioritising advanced manufacturing automation including CNC hydraulic presses and riveting and clinching machines for the country's Mittelstand supply chain.

As re-shoring initiatives translate into greenfield assembly plant openings across the U.S. Midwest and Central Europe through 2027, demand for fully automated hydraulic insertion machines with integrated quality monitoring will outpace the capacity of existing installed fleets, compelling fresh capital investment cycles.

Restraints - High Capital Expenditure and Extended Payback Periods Limiting Adoption Among Small Manufacturers

Fully automatic hydraulic insertion machines with servo-hydraulic force control and in-line inspection capabilities carry typical unit price points between US$ 150,000 and US$ 500,000, creating a prohibitive entry threshold for small and medium-sized metal fabrication and industrial machinery job shops operating on thin margins.

The U.S. Small Business Administration reports that manufacturing SMEs with fewer than 100 employees account for approximately 98% of all U.S. fabrication establishments, yet fewer than 12% have deployed any form of automated press-fit assembly systems, a direct consequence of capital cost barriers rather than operational need. New entrants offering modular or leased hydraulic insertion platforms face the additional challenge of convincing procurement teams accustomed to depreciation schedules built around fully owned assets.

Raw Material Price Volatility and Supply Chain Disruptions Compressing Equipment Manufacturer Margins

Hydraulic cylinder bodies, high-pressure valve manifolds, and precision-ground guide columns depend on specialised alloy steel and stainless steel grades whose prices have exhibited ±30% annual volatility since 2021, per World Steel Association data, squeezing gross margins for industrial insertion equipment OEMs that operate on fixed-price long-term supply contracts.

The U.S. Section 232 steel and aluminium tariffs, maintained and extended under the Trade Expansion Act, continue to impose cost premiums of 25% on imported steel inputs for North American equipment assemblers, adding approximately 8 to 12 weeks to procurement lead times when domestic mill allocations are constrained. Incumbent manufacturers with vertically integrated casting and machining operations absorb this friction more effectively than contract-assembly-reliant new entrants, reinforcing a two-tier competitive structure.

Opportunities - Smart Manufacturing Integration Opening a Premium Tier for IoT-Enabled Hydraulic Insertion Platforms

Equipment manufacturers that embed real-time force-displacement monitoring, digital twin calibration, and OPC-UA connectivity into their hydraulic press automation platforms can command price premiums of 15% over conventional analogue-control machines, targeting Industry 4.0-ready factories that require full traceability of every insertion event.

Bosch Rexroth AG launched its ctrlX AUTOMATION ecosystem in 2023, integrating open-architecture IIoT controls into hydraulic motion systems, a move that signals the commercial readiness of smart manufacturing systems for insertion applications and validates the investment thesis for connected precision press-fit solutions. Suppliers that achieve ISO 9283 robot performance certification for their automated assembly machinery, and that can demonstrate sub-0.5% process deviation rates through real-time analytics dashboards, will be best positioned to capture long-term service and software revenue streams alongside the initial hardware sale.

Aerospace MRO Expansion Creating Recurring Demand for Portable and Bench-Top Hydraulic Insertion Tools

The post-pandemic commercial aviation recovery, with IATA projecting global passenger numbers to exceed 4.7 billion by 2026, surpassing 2019 levels, is forcing MRO facilities at major hubs to accelerate engine and airframe component replacement cycles, generating recurring procurement demand for compact hydraulic insertion equipment suited to bearing and bushing installation in confined nacelle and landing gear environments.

Airbus announced in 2024 the expansion of its Aerostructures MRO capacity in Toulouse, integrating servo-hydraulic assembly stations specifically designed for A320neo family landing gear bushing installation, validating both the application category and the procurement channel. Component manufacturers and MRO integrators holding AS9100 Rev D quality management certification and the tooling flexibility to address both new-production and repair insertion workflows are best positioned to capture this recurring, non-cyclical demand stream.

Category-wise Analysis

Machine Type Insights

Fully automatic hydraulic insertion machines are likely to command 45% of the global hydraulic insertion machine market in 2026, equivalent to US$ 1.12 billion, reflecting their dominance in high-volume, zero-defect manufacturing environments where human variability must be eliminated. Tier-1 automotive suppliers operating just-in-time assembly lines, such as those producing suspension subframe assemblies for BMW Group plants, rely on fully automatic hydraulic insertion machines to install dozens of rubber-metal bushings per vehicle at cycle times under 8 seconds, a throughput benchmark no semi-automatic configuration can match.

Semi-Automatic Hydraulic Insertion Machines represent the fastest-growing machine type segment, propelled by the expansion of electronics contract manufacturing in Southeast Asia where operators require guided insertion force control without the capital outlay of full robotics integration.

Operation Type Insights

Hydraulic press-fit insertion accounts for 56% of the global hydraulic insertion machine market in 2026, equivalent to US$ 1.40 billion, driven by its unmatched ability to generate consistent, programmable insertion forces ranging from 2 kN to 2,000 kN without the positional drift associated with pneumatic alternatives.

Servo-Hydraulic Insertion is the fastest-growing operation type, driven by the proliferation of closed-loop force-position control requirements in next-generation electric motor and battery module assembly lines, where millimetre-level insertion accuracy determines product reliability. Kistler Group, a specialist in measurement and process monitoring, integrated its maXYmos process monitoring system with servo-hydraulic press units in 2024, enabling real-time OK/NOK classification of every insertion event for EV battery cell module assemblers in Central Europe, a use case that demonstrates servo-hydraulic systems' superior suitability for safety-critical intelligent insertion workflows.

Application Insights

Fastener insertion is likely to register 35% of the global hydraulic insertion machine market in 2026, equivalent to US$ 880 million, sustained by the intensity of fastener usage across automotive, heavy machinery, and structural steel fabrication sectors, where hydraulic insertion machines ensure clinch nut, weld stud, and self-clinching standoff installation meets torque-pullout specifications first time, every time.

Bearing & bushing installation is the fast-growing application segment, accelerated by the electric vehicle drivetrain transition requiring precision bearing press-fit into aluminium motor housings where interference tolerance windows are tighter than in cast-iron predecessors by a factor of approximately 1.5×. SKF Group introduced its OptiAlign bearing installation monitoring system in 2023, designed to interface with hydraulic press-fit platforms to verify seating force curves against pre-defined acceptance envelopes for EV traction motor bearings, opening a new category of instrumented bearing installation machines for drivetrain component suppliers.

End-user Insights

Automotive Manufacturing accounts for 41.0% of the global hydraulic insertion machine market in 2026, equivalent to US$ 1.02 billion, reflecting the sector's unparalleled density of press-fit assembly operations across powertrain, suspension, body-in-white, and interior module production lines. Toyota's global manufacturing system specifies hydraulic insertion machines for wheel bearing hub assembly across all of its 28 global plants, using force-monitoring integration to enforce Cpk values above 1.67 for safety-critical bearing seats, a process discipline that cascade-qualifies the hydraulic insertion platform category with every new model platform launch.

Aerospace & Defence is the fast-growing end-user segment, catalysed by record-level defence budget commitments across NATO member states, 32 of which agreed in June 2024 to maintain or increase defence spending above 2% of GDP, triggering procurement of new airframe and missile structural component assembly lines that depend on precision rivet and bushing insertion equipment.

Regional Insights

North America Hydraulic Insertion Machine Market Trends and Insights

North America accounts for 26% of the global hydraulic insertion machine market in 2026, representing US$ 650 million, with the U.S. automotive re-shoring wave and defence modernisation programmes providing compounding demand tailwinds that differentiate the region from cyclical capex dependency. The CHIPS and Science Act 2022 allocated US$ 52 billion toward semiconductor fabrication infrastructure in the United States, and each new fab construction project requires precision automated assembly machinery for cleanroom-compatible component insertion in HVAC, power distribution, and precision fixture manufacturing stages.

North America's installed base of hydraulic insertion equipment is skewing toward higher-capability servo-hydraulic and IoT-integrated configurations as buyers prioritise process qualification documentation demanded by automotive and defence primes.

- United States Hydraulic Insertion Machine Market Size

The United States commands an estimated 78% of the North American hydraulic insertion machine market, driven by the concentration of Tier-1 automotive suppliers in the Great Lakes region and aerospace prime contractors across Texas, California, and the Pacific Northwest. The U.S. Department of Defense's Fiscal Year 2025 procurement budget, totalling US$ 895 billion is sustaining multi-year airframe and missile component manufacturing contracts that require certified hydraulic insertion and riveting platforms.

Continued investment in EV battery gigafactories, with Panasonic Energy and LG Energy Solution each opening U.S. facilities before 2026, will extend the forward demand horizon for precision press-fit assembly systems into the next decade.

Europe Hydraulic Insertion Machine Market Trends and Insights

Europe accounts for 21.0% of the global hydraulic insertion machine market in 2026, representing US$ 530 million with Germany's engineering-intensive manufacturing base and France's aerospace industrial complex anchoring regional demand for premium hydraulic press automation and servo-hydraulic insertion systems. The EU Machinery Regulation (EU) 2023/1230, which replaces the Machinery Directive 2006/42/EC and enters full application in 2027, is compelling European equipment manufacturers to re-certify hydraulic insertion machines for updated safety and electromagnetic compatibility standards, accelerating fleet modernisation decisions.

European buyers disproportionately favour German and Austrian equipment OEMs, reinforcing a regional supply chain dynamic where proximity to machine tool clusters in Bavaria and Styria reduces lead times and after-sales service costs.

- Germany Hydraulic Insertion Machine Market Size

Germany represents an estimated 34% of the European hydraulic insertion machine market, sustained by its dense concentration of automotive OEMs, Tier-1 suppliers, and mechanical engineering Mittelstand firms that collectively operate some of the world's highest-density automated assembly machinery fleets.

Schaeffler Group's ongoing electrification investment, including its €3 Billion E-Mobility capex programme announced in 2022, continuously refreshes bearing insertion and press-fit assembly equipment requirements across its Herzogenaurach and Schweinfurt production sites. Germany's transition to electric drive units under the EU CO2 Emission Performance Standards for Cars Regulation 2023 will sustain above-average procurement intensity for hydraulic insertion equipment through 2030.

- United Kingdom Hydraulic Insertion Machine Market Size

The United Kingdom holds an estimated 16% share of the European hydraulic insertion machine market, with aerospace and defence manufacturing, concentrated in the Bristol-Bath corridor and the East Midlands, providing the primary demand anchor for high-force hydraulic insertion platforms. Rolls-Royce Holdings' UltraFan engine programme, with structural component assembly ongoing at its Derby facility, requires precision hydraulic bushing and bearing installation tooling qualified to AS9100 Rev D standards. The UK Advanced Manufacturing Plan, announced by HM Treasury in November 2023 with £4.5 billion in committed support, will stimulate further adoption of smart manufacturing systems, including instrumented hydraulic press automation among British supply chain manufacturers.

- France Hydraulic Insertion Machine Market Size

France accounts for an estimated 13% of the European hydraulic insertion machine market, with the country's Airbus and Safran supply chains and the Renault-Nissan-Mitsubishi Alliance manufacturing complex providing structural demand for both aerospace-grade riveting and clinching machines and automotive fastener insertion equipment. The France 2030 investment plan, with €30 Billion committed to re-industrialisation, specifically targets automotive electrification and aeronautics manufacturing upgrades that encompass assembly automation procurement. Renault's ElectriCity manufacturing campus in Douai, converting to all-electric vehicle production, is actively reequipping press-fit assembly lines with hydraulic insertion machines validated for aluminium EV platform component tolerances.

Asia Pacific Hydraulic Insertion Machine Market Trends and Insights

Asia Pacific accounts for 40% of the global hydraulic insertion machine market in 2026, and leads all regions as the fast-growing market at a CAGR of 7.2%, powered by China's industrial machinery manufacturing scale, India's accelerating automotive localisation, and Japan's precision engineering export competitiveness. China's Made in China 2025 successor industrial policy, extended through the 14th Five-Year Plan, prioritises domestic production of high-end CNC hydraulic presses and automated assembly machinery, simultaneously expanding the supply base and deepening the demand pool within a single national market.

Regional growth will intensify as ASEAN economies, particularly Vietnam and Thailand, attract automotive and electronics supply chain relocations that require the first-time installation of industrial hydraulic equipment in greenfield facilities.

- China Hydraulic Insertion Machine Market Size

China accounts for an estimated 52% of the Asia Pacific hydraulic insertion machine market, anchored by its status as the world's largest vehicle producer with 30.2 million units manufactured in 2023 per China Association of Automobile Manufacturers data. BYD's aggressive model launch cadence, releasing 30+ new EV and hybrid variants between 2022 and 2024, requires continuous retooling of press-fit and bearing installation lines across its Shenzhen, Xi'an, and Changsha manufacturing hubs. China's domestic hydraulic equipment manufacturers, led by Hengli Hydraulic and Bosch Rexroth's local joint ventures, are compressing import dependency and capturing a growing share of the country's equipment procurement budget.

- India Hydraulic Insertion Machine Market Size

India holds an estimated 18% of the Asia Pacific hydraulic insertion machine market and is the region's second-fastest-growing country market, energised by the Production Linked Incentive (PLI) Scheme for Automobile and Auto Components, which disbursed approximately INR 3,484 Crore to qualifying manufacturers in its first two approval tranches.

Tata Motors' Sanand EV plant expansion in Gujarat, producing the Tata Nexon EV, has integrated hydraulic fastener insertion and bearing installation stations sourced through both domestic and imported equipment channels, reflecting the sophistication of India's automotive assembly infrastructure.

India's automotive component sector, represented by the Automotive Component Manufacturers Association of India (ACMA), projects domestic component production to reach US$ 100 Billion by 2026, creating a sustained pipeline of hydraulic insertion machine procurement events.

- Japan Hydraulic Insertion Machine Market Size

Japan represents an estimated 21% of the Asia Pacific hydraulic insertion machine market, with the country's precision manufacturing culture and dominant position in industrial robot and machine tool exports sustaining demand for high-specification servo-hydraulic insertion and CNC hydraulic press platforms.

JTEKT Corporation, a major bearing and steering component manufacturer, operates hydraulic press-fit assembly lines across its Osaka and Nagoya plants that integrate real-time process monitoring aligned with JISB 1514 bearing installation standards, setting a technical benchmark that cascades to its supplier network. Japan's Ministry of Economy, Trade and Industry (METI) fiscal 2024 subsidy programme for manufacturing digitalisation is accelerating the replacement of analogue hydraulic insertion machines with IoT-enabled smart manufacturing systems across small and medium Tier-2 suppliers.

Competitive Landscape

The global hydraulic insertion machine market operates as a moderately consolidated oligopoly at the high-performance tier, with Bosch Rexroth AG and Parker Hannifin Corporation collectively commanding an estimated 28% combined revenue share through their integrated hydraulic motion control and automated assembly machinery portfolios.

Enerpac Tool Group differentiates through portable high-force hydraulic tooling for MRO and field insertion applications, occupying a distinct market niche that neither of the two system integrators efficiently addresses. Competition centres on process monitoring software integration, force-displacement traceability, and certified conformance to automotive quality management systems, capabilities that separate specification-winning incumbents from price-competing laggards. Kistler Group and Festo AG & Co. KG are the most disruptive entrants at the smart manufacturing interface, embedding process analytics directly into press-fit platforms and challenging established players' software-agnostic product architectures.

Key Developments:

- January, 2025: Bosch Rexroth AG expanded its servo-hydraulic press product line with integrated ctrlX CORE-based process monitoring, targeting EV battery module assembly customers in Germany and South Korea requiring IATF 16949-compliant force-displacement traceability on every insertion cycle.

- March, 2024: Parker Hannifin Corporation acquired Hänchen Hydraulik GmbH, a German precision hydraulic cylinder specialist, strengthening Parker's ability to supply custom high-precision actuator assemblies for aerospace and defence hydraulic insertion applications in the European market.

- September, 2024: Enerpac Tool Group launched its ZE-Series electric-hydraulic press platform, offering programmable force control up to 150 kN for semi-automatic bearing and bushing installation in MRO environments, directly addressing the growing installed base of EV drivetrain service centres.

Companies Covered in Hydraulic Insertion Machine Market

- Bosch Rexroth AG

- Parker Hannifin Corporation

- Eaton Corporation Plc

- Schaeffler Group

- Enerpac Tool Group

- Festo AG & Co. KG

- SMC Corporation

- HAWE Hydraulik SE

- Hydac International GmbH

- Linde Hydraulics

- Bucher Hydraulics GmbH

- Daikin Industries Ltd.

- Kistler Group

- Fasp Automazioni

- Ingimec Automation

- Tox Pressotechnik GmbH & Co. KG

- Schmidt Technology GmbH

- Alfing Kessler Sondermaschinen GmbH

- Schuler AG

- Dunkes GmbH

Frequently Asked Questions

The global hydraulic insertion machine market is valued at US$ 2.50 Billion in 2026 and is projected to reach US$ 4.04 Billion by 2033, advancing at a 7.1% CAGR. The primary growth catalyst is the electrification-driven retooling of automotive and aerospace manufacturing lines, which requires precision press-fit assembly systems capable of meeting tighter interference-fit tolerances in lightweight aluminium and composite structures.

The U.S. CHIPS and Science Act 2022 and allied industrial policy instruments are generating first-time automated assembly machinery procurement in semiconductor and clean energy manufacturing facilities; second, the IATF 16949:2016 automotive quality management standard's mandatory process traceability requirements are compelling OEM supply chains to replace legacy analogue press systems with documented, servo-controlled hydraulic insertion platforms. Together, these policies and quality system forces create non-deferrable replacement and greenfield equipment procurement cycles across multiple end-user industries.

Hydraulic Press-Fit Insertion commands the largest operation-type share at 56% of the global hydraulic insertion machine market in 2026, because no alternative actuation technology can deliver forces ranging from 2 kN to 2,000 kN with the programmable repeatability demanded by ISO-toleranced interference fits across heavy industrial and automotive applications.

Asia Pacific dominates the global hydraulic insertion machine market with a 40.0% share in 2026, equivalent to US$ 1.00 billion, driven by two structural factors: China's position as the world's largest automotive producer, sustaining continuous press-fit assembly equipment utilisation, and India's PLI Scheme for Automobile and Auto Components, accelerating domestic Tier-1 manufacturing investment that requires first-time hydraulic insertion machine installations. The region's 7.2% CAGR, above the global average, will be sustained by ASEAN manufacturing hub growth, particularly as Thailand and Vietnam absorb automotive and electronics supply chain diversification flows through 2030.

The aerospace MRO expansion cycle, where record commercial aircraft utilisation rates are driving bearing and bushing replacement frequencies beyond pre-pandemic norms across IATA-member airline maintenance facilities. Equipment manufacturers holding AS9100 Rev D certification and offering portable servo-hydraulic insertion platforms validated for nacelle and landing gear environments, a configuration Airbus has already integrated into its Toulouse MRO infrastructure, are best positioned to capture this recurring, non-cyclical revenue stream as airline fleets age and component replacement intervals shorten.

Bosch Rexroth AG, Parker Hannifin Corporation, and Enerpac Tool Group lead the global hydraulic insertion machine market, competing primarily on process monitoring software integration, force-displacement traceability certification, and compatibility with automotive and aerospace quality management frameworks.