- Industrial Machinery

- Decanter Centrifuge Market

Decanter Centrifuge Market Size, Share, and Growth Forecast, 2026 - 2033

Decanter Centrifuge Market by Product Type (Two‑Phase Decanter Centrifuge, Three‑Phase Decanter Centrifuge, Others), Application (Chemical & Petrochemical, Food & Beverage, Others), Design, and Regional Analysis for 2026 - 2033

Decanter Centrifuge Market Size and Trends Analysis

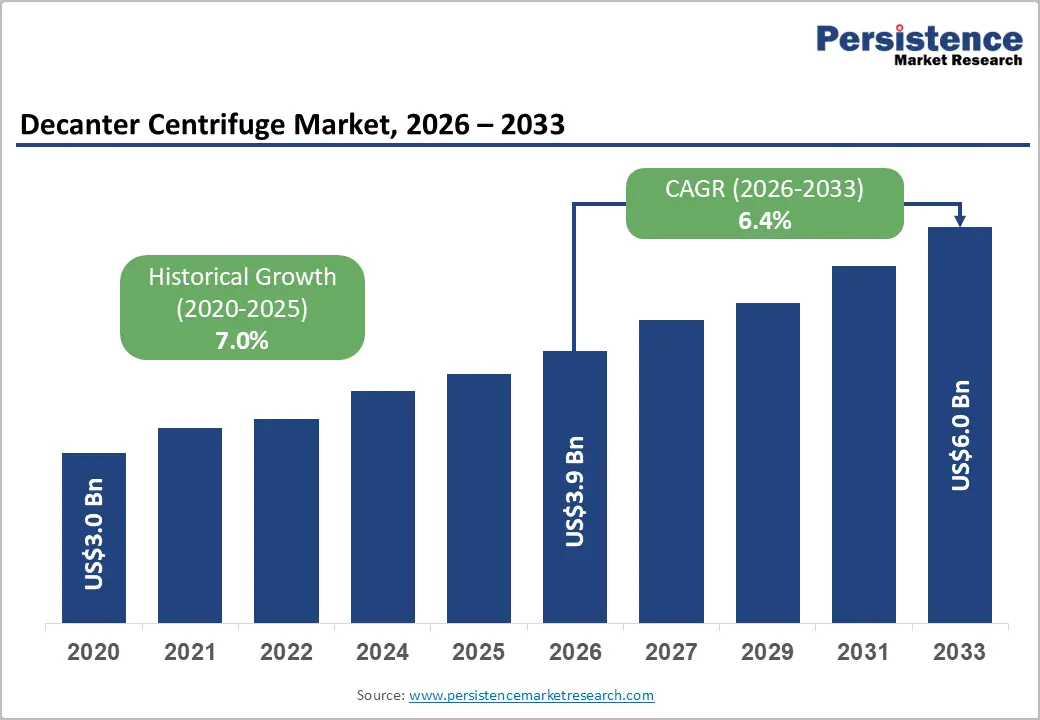

The global decanter centrifuge market size is likely to be valued at US$3.9 billion in 2026 and is expected to reach US$6.0 billion by 2033, growing at a CAGR of 6.4% during the forecast period from 2026 to 2033, driven by stricter wastewater treatment regulations, rising demand for continuous solid-liquid separation systems, and expanding use in chemical, food processing, mining, and oil recovery operations.

Technological improvements in automation, energy efficiency, and process monitoring are also supporting replacement demand across municipal and industrial facilities.

Key Industry Highlights:

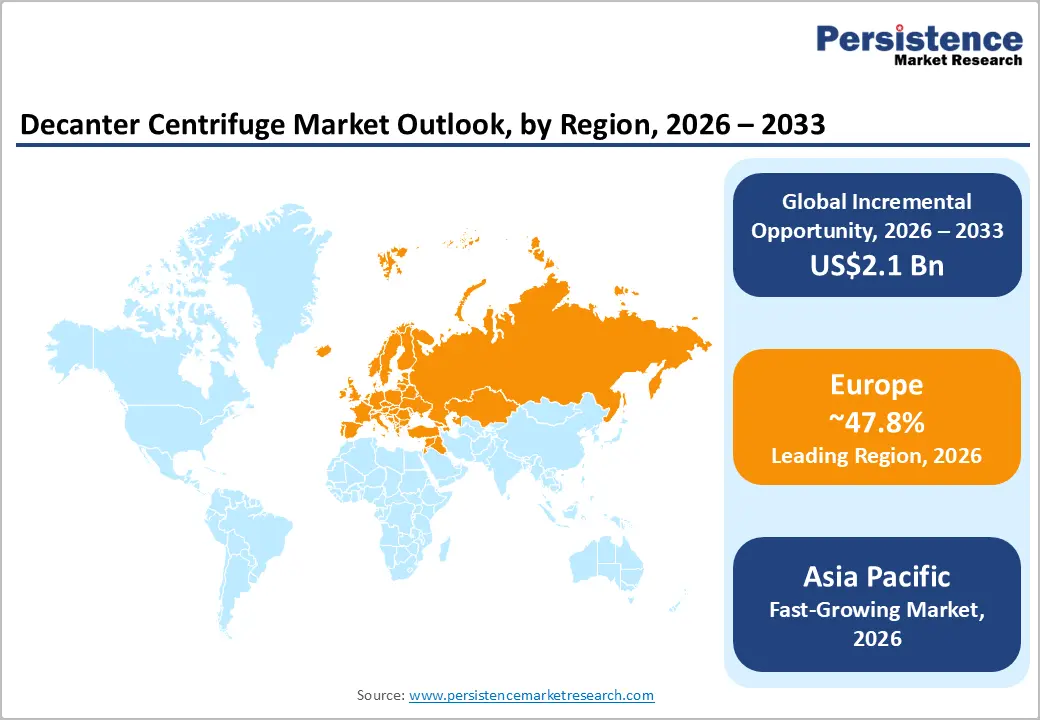

- Leading Region: Europe, accounting for approximately 47.8% of market revenue in 2026, supported by strong wastewater treatment infrastructure and strict environmental regulations.

- Fastest-growing Region: Asia Pacific is projected to grow at the fastest pace, during the forecast period, due to rapid industrialization, wastewater infrastructure expansion, and rising manufacturing activity.

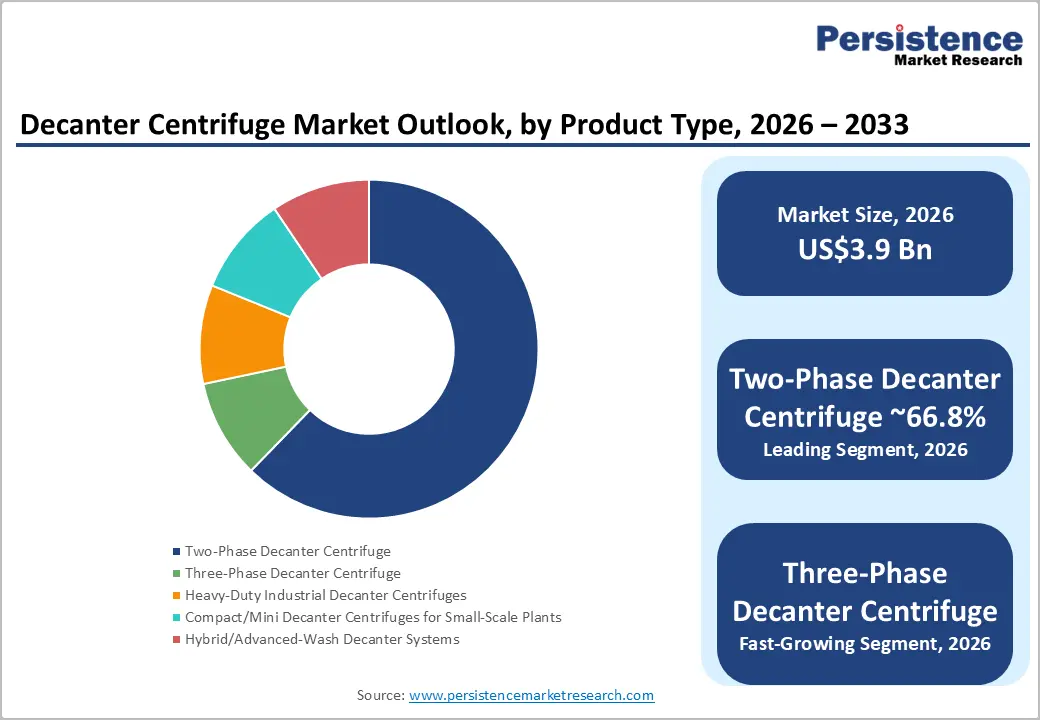

- Dominant Product Type: Two-phase decanter centrifuges, anticipated to account for nearly 66.9% of the market share in 2026, due to widespread use in wastewater treatment, sludge processing, and industrial solid-liquid separation.

- Leading Application: Horizontal decanter centrifuges, expected to hold more than 67.1% of the market share in 2026, owing to their high throughput capacity, continuous operation capability, and extensive use across industrial processing applications.

DRO Analysis

Driver - Stricter Wastewater Treatment Regulations Supporting Equipment Demand

Government agencies and environmental regulators across major economies are enforcing tighter wastewater treatment standards, directly increasing demand for advanced sludge dewatering and separation technologies. Municipal treatment plants and industrial facilities are under pressure to improve discharge quality, reduce sludge disposal volumes, and increase operational efficiency. Decanter centrifuges are widely adopted because they enable continuous operation, reduce moisture content in sludge, and lower transportation and disposal costs.

In Europe, revised wastewater treatment policies are expanding pollutant-control obligations and encouraging energy-efficient treatment infrastructure. In the U.S., wastewater modernization programs and industrial discharge standards continue to support investments in centrifuge-based sludge management systems. Emerging economies are also increasing investments in wastewater infrastructure as urban populations and industrial activity continue to rise. These regulatory developments are creating long-term demand for high-capacity horizontal decanter centrifuges across municipal and industrial treatment facilities.

Industrial Processing Expansion Increasing Demand for Continuous Separation Systems

Industries including chemicals, food processing, mining, pharmaceuticals, and oil & gas are increasingly shifting toward automated and continuous separation technologies to improve throughput and reduce operational downtime. Decanter centrifuges provide efficient separation of solids from liquids under high-volume processing conditions, making them essential in modern industrial production environments.

The growth of chemical processing capacity, expansion of food manufacturing facilities, and rising mineral-processing activities are increasing the need for reliable separation systems capable of operating under demanding conditions. Food manufacturers are also prioritizing hygienic and closed-loop processing systems to meet quality-control standards and reduce contamination risks. In mining and petrochemical applications, operators are adopting decanter centrifuges to improve slurry handling, recover valuable materials, and optimize waste management. Automation features such as real-time monitoring, programmable controls, and energy optimization are further increasing adoption across industrial processing facilities.

Restraint - High Capital Investment and Maintenance Complexity Limiting Adoption

Despite strong operational advantages, decanter centrifuges involve high upfront investment costs compared to conventional dewatering and filtration technologies. The equipment requires precision engineering, durable wear-resistant components, and advanced control systems, which significantly increase procurement costs for small and mid-sized operators.

Maintenance requirements also remain a challenge, particularly in applications involving abrasive slurries, corrosive materials, or continuous high-speed operation. Components such as scrolls, bearings, and rotating assemblies require periodic servicing and replacement, increasing lifecycle costs. Energy consumption and operational noise can also limit adoption in cost-sensitive projects.

These factors are particularly relevant in developing regions where industrial operators often prioritize lower-cost separation alternatives with shorter payback periods. Although manufacturers are introducing modular and energy-efficient systems, cost barriers continue to slow penetration in smaller industrial facilities and municipal projects with limited budgets.

Opportunity - Water Reuse and Circular Economy Initiatives Creating Retrofit Opportunities

The global shift toward water reuse, sludge recovery, and circular economy practices is creating significant opportunities for decanter centrifuge manufacturers. Governments and industrial operators are increasingly investing in systems that reduce water wastage, recover reusable materials, and improve sludge management efficiency.

Decanter centrifuges are widely used in biosolids recovery, industrial wastewater recycling, and sludge thickening applications because they reduce waste volumes while improving water recovery rates. Retrofit opportunities are particularly strong in aging wastewater treatment facilities where operators are upgrading existing infrastructure to meet new environmental standards without constructing entirely new treatment plants.

Industrial sectors, including chemicals, food processing, and mining, are also investing in water recycling systems to reduce freshwater consumption and lower disposal costs. This trend is expected to generate long-term demand for high-efficiency dewatering and separation technologies.

Smart and Energy-Efficient Decanters Supporting Replacement Demand

Industrial operators are increasingly replacing conventional separation systems with digitally enabled decanter centrifuges that improve energy efficiency, process stability, and operational visibility. Manufacturers are introducing systems equipped with automated control platforms, sensor-based monitoring, predictive maintenance capabilities, and optimized energy management functions.

These technologies help operators reduce power consumption, improve separation consistency, and minimize unplanned downtime. Energy-efficient decanter systems are gaining traction in wastewater treatment, edible oil processing, starch production, and petrochemical applications where energy costs represent a significant portion of operating expenditure. The integration of digital monitoring and automation also supports preventive maintenance strategies, extending equipment lifespan and improving productivity. Vendors with strong service capabilities and intelligent process-control solutions are expected to gain a competitive advantage as industrial customers prioritize lifecycle performance over initial equipment cost.

Category-wise Analysis

Product Type Insights

The two-phase decanter centrifuge segment is anticipated to account for approximately 66.9% of the global market share during the forecast period. Its dominance is driven by extensive use in wastewater treatment, industrial sludge processing, food manufacturing, and chemical separation applications. Companies such as Alfa Laval and Flottweg supply two-phase systems for municipal sludge dewatering and beverage clarification, where continuous solid-liquid separation is essential.

These systems are preferred because they are easier to operate, require lower maintenance, and involve lower operating costs than three-phase alternatives. Their widespread deployment across wastewater treatment plants and industrial facilities continues to generate stable aftermarket demand for wear parts, maintenance services, and system upgrades. Rising investments in wastewater infrastructure and industrial process optimization are expected to sustain segment growth.

The three-phase decanter centrifuge segment is anticipated to witness the fastest growth over the forecast period due to rising demand for advanced liquid-liquid-solid separation technologies. These systems are widely used in refinery sludge treatment, edible oil recovery, petrochemical processing, and industrial waste recycling. Companies, including GEA and ANDRITZ, have expanded offerings for oil recovery and complex industrial separation applications.

Growth is being supported by increasing demand for higher recovery efficiency, lower product losses, and improved waste management. Technological advancements in automation, precision separation, and process monitoring are further improving operational performance. Expanding use in specialty food processing, biofuels, and petrochemical operations is expected to strengthen long-term demand despite higher capital costs.

Design Insights

The horizontal decanter centrifuge segment is anticipated to hold more than 67.1% of the market share in 2026, due to its high throughput capacity and suitability for continuous industrial processing. These systems are widely deployed in wastewater treatment, mining, chemical manufacturing, and oil & gas operations. For example, Centrisys and HAUS supply horizontal decanters for sludge dewatering and industrial slurry handling applications.

Horizontal designs remain the preferred choice, as they provide stable separation performance, operational flexibility, and efficient handling of large solids volumes. Their strong installed base also supports standardized maintenance practices, spare parts availability, and automation integration. Demand continues to grow in industries where durability and lifecycle performance are major purchasing priorities.

The vertical decanter centrifuge segment is anticipated to register the fastest growth due to increasing demand for compact and space-efficient separation systems. These centrifuges are gaining traction in pharmaceutical processing, pilot-scale food production, and facilities with limited installation space. Companies such as Tomoe Engineering offer vertical systems designed for specialized industrial and food-processing applications.

Growth is being driven by industrial modernization projects and the increasing adoption of modular processing infrastructure. Vertical systems are becoming more attractive for operators seeking flexible layouts, reduced footprint requirements, and easier integration into existing facilities. Improvements in automation and process efficiency are also expanding their use across niche industrial applications.

Regional Insights

North America Decanter Centrifuge Market Trends

North America represents a significant share of the global decanter centrifuge market due to strong industrial infrastructure, established wastewater treatment systems, and widespread adoption of automated processing technologies. The region continues to witness stable demand from municipal wastewater treatment, chemical manufacturing, oil & gas operations, mining, and food processing industries. Increasing focus on sludge reduction, discharge compliance, and operational efficiency is encouraging investments in advanced dewatering technologies and energy-efficient separation systems.

U.S. Decanter Centrifuge Market Trends

The U.S. remains the dominant market within North America due to its extensive municipal wastewater treatment network, advanced chemical processing industry, and large oil & gas sector. Wastewater infrastructure modernization programs continue to support demand for high-capacity horizontal decanter centrifuges used in sludge dewatering and industrial wastewater treatment.

The country also maintains strong adoption across ethanol production, food processing, and mining applications, where continuous solid-liquid separation is critical for operational efficiency. Industrial operators increasingly prefer premium centrifuge systems that reduce downtime, improve throughput, and lower lifecycle costs. Rising investment in automation and sustainability-focused industrial infrastructure is expected to sustain long-term market growth.

Canada Decanter Centrifuge Market Trends

Canada represents a steadily growing market supported by investments in mining, oil sands processing, wastewater treatment, and environmental management projects. The country’s resource-intensive industries require reliable separation systems capable of handling abrasive slurries and high-solids industrial waste streams.

Municipal wastewater treatment upgrades and stricter environmental compliance standards are also supporting demand for advanced sludge dewatering technologies. Growth opportunities are particularly strong in mining regions and industrial processing facilities where operators are focused on improving water recovery and reducing waste disposal costs.

Europe Decanter Centrifuge Market Trends

Europe remains one of the most valuable regional markets for decanter centrifuges, accounting for an estimated market revenue of approximately 47.8% in 2026. The region benefits from strict environmental regulations, strong industrial automation capabilities, and widespread adoption of advanced wastewater treatment technologies. Industrial sustainability initiatives and energy-efficiency targets continue to accelerate investments in high-performance dewatering and separation systems.

Germany Decanter Centrifuge Market Trends

Germany represents the largest country-level market in Europe, due to its advanced industrial manufacturing sector and concentration of major centrifuge manufacturers. The country maintains strong demand from chemical processing, food manufacturing, wastewater treatment, and pharmaceutical industries.

Industrial operators in Germany continue to invest in energy-efficient processing technologies and automated separation systems to meet environmental and operational efficiency targets. Ongoing wastewater infrastructure modernization and industrial sustainability initiatives are expected to support replacement demand across municipal and industrial facilities.

U.K. Decanter Centrifuge Market Trends

The U.K. remains an important market due to growing investments in wastewater infrastructure upgrades and industrial environmental compliance programs. Municipal utilities are increasingly adopting advanced sludge dewatering technologies to improve treatment efficiency and reduce disposal costs.

Food processing and pharmaceutical manufacturing also contribute to equipment demand, particularly for hygienic and high-precision separation systems. Automation and predictive maintenance technologies are becoming key purchasing considerations among industrial operators.

Italy Decanter Centrifuge Market Trends

Italy maintains strong demand from food processing, pharmaceuticals, chemical manufacturing, and wastewater treatment applications. The country’s industrial base and established engineering expertise continue to support the adoption of advanced separation technologies.

The olive oil and wine industries also represent important niche applications for decanter centrifuges, particularly for premium product recovery and hygienic processing requirements.

Asia Pacific Decanter Centrifuge Market Trends

Asia Pacific is anticipated to record the fastest regional growth during the forecast period, due to rapid industrialization, expanding wastewater infrastructure, and increasing manufacturing activity. The region benefits from strong growth in chemical processing, food manufacturing, mining, pharmaceuticals, and industrial wastewater treatment sectors.

Urban population growth and increasing industrial wastewater generation are creating substantial opportunities for advanced sludge dewatering and separation technologies. Government-led infrastructure modernization programs and rising environmental compliance requirements are further accelerating demand across developing economies. Lower manufacturing costs and expanding industrial capacity also strengthen the region’s position as a major production hub for industrial processing equipment.

China Decanter Centrifuge Market Trends

China remains the largest market within Asia Pacific because of its extensive chemical processing, mining, petrochemical, and industrial wastewater treatment sectors. Rapid industrial expansion and increasing environmental regulation continue to support demand for advanced decanter centrifuge systems.

The country is also investing heavily in wastewater treatment infrastructure and industrial process automation to improve operational efficiency and environmental performance. Mining and resource-processing industries remain major contributors to equipment demand.

India Decanter Centrifuge Market Trends

India is emerging as one of the fastest-growing markets, due to increasing investment in municipal wastewater treatment, industrial infrastructure, food processing, and pharmaceutical manufacturing. Government programs focused on sanitation, industrial modernization, and water management are accelerating the adoption of sludge dewatering technologies.

Growth opportunities are particularly strong in urban wastewater projects, dairy processing, edible oil manufacturing, and specialty chemical production. Rising industrial automation and increasing focus on operational efficiency are also supporting market expansion.

Competitive Landscape

The global decanter centrifuge market is moderately fragmented, with competition distributed among international engineering companies, specialized centrifuge manufacturers, and regional suppliers. Large multinational companies maintain strong positions in premium industrial applications through advanced engineering capabilities, extensive service networks, and established customer relationships.

Key market participants are prioritizing energy-efficient system design, digital automation, application-specific engineering, and service-led business models. Manufacturers are increasingly focusing on predictive maintenance solutions, retrofit-friendly equipment, and long-term lifecycle performance to strengthen customer retention and improve profitability across industrial processing applications.

Key Industry Developments:

- In April 2025, GEA Group introduced the Varipond C solution for decanter centrifuges, enabling faster and more precise adjustment of pond depth and separation zones while reducing energy consumption by nearly 30% in food, beverage, and refinery applications.

- In June 2025, Alfa Laval launched the Prodec 72 Oil Plus decanter centrifuge, designed to improve distiller's corn oil recovery and increase oil purity for ethanol producers, strengthening its separation technology portfolio for biofuel processing facilities.

Companies Covered in Decanter Centrifuge Market

- Alfa Laval AB

- GEA Group AG

- ANDRITZ AG

- Flottweg SE

- Pieralisi Maip S.p.A.

- Mitsubishi Kakoki Kaisha, Ltd.

- Tomoe Engineering Co., Ltd.

- HAUS Centrifuge Technologies

- FLSmidth & Co. A/S

- IHI Rotating Machinery Engineering Co., Ltd.

- Centrisys Corporation

- Hiller GmbH

- GN Solids Control Co., Ltd.

- Elgin Separation Solutions

- Trucent, Inc.

- SIEBTECHNIK TEMA GmbH

Frequently Asked Questions

The global decanter centrifuge market is anticipated to be valued at US$3.9 billion in 2026.

The decanter centrifuge market is expected to reach approximately US$6.0 billion by 2033.

Key trends include increasing wastewater treatment investments, rising adoption of energy-efficient centrifuge systems, growing demand for automated separation technologies, and expanding use in food processing, chemicals, and industrial water recycling applications.

The two-phase decanter centrifuge segment leads the market, accounting for nearly 66.9% of global market share due to its broad use in wastewater treatment and industrial solid-liquid separation.

The decanter centrifuge market is projected to grow at a CAGR of approximately 6.4% from 2026 to 2033.

Major companies include Alfa Laval, GEA Group, ANDRITZ AG, Flottweg SE, and Pieralisi Group.