- Rail

- Freight Cars Market

Freight Cars Market Size, Share, and Growth Forecast, 2026 - 2033

Freight Cars Market by Car Type (Box Car, Flat Car, Tank Car, Gondola Car, Reefer Car), Material Carried (Bulk Cargo, Liquid Cargo, General Cargo, Perishable Goods, Automobiles & Vehicles), Application (Mining & Minerals, Energy & Petroleum, Agriculture & Food Processing, Chemicals & Pharmaceuticals, Automotive & Heavy Machinery, Construction & Steel), and Regional Analysis for 2026 - 2033

Freight Cars Market Share and Trends Analysis

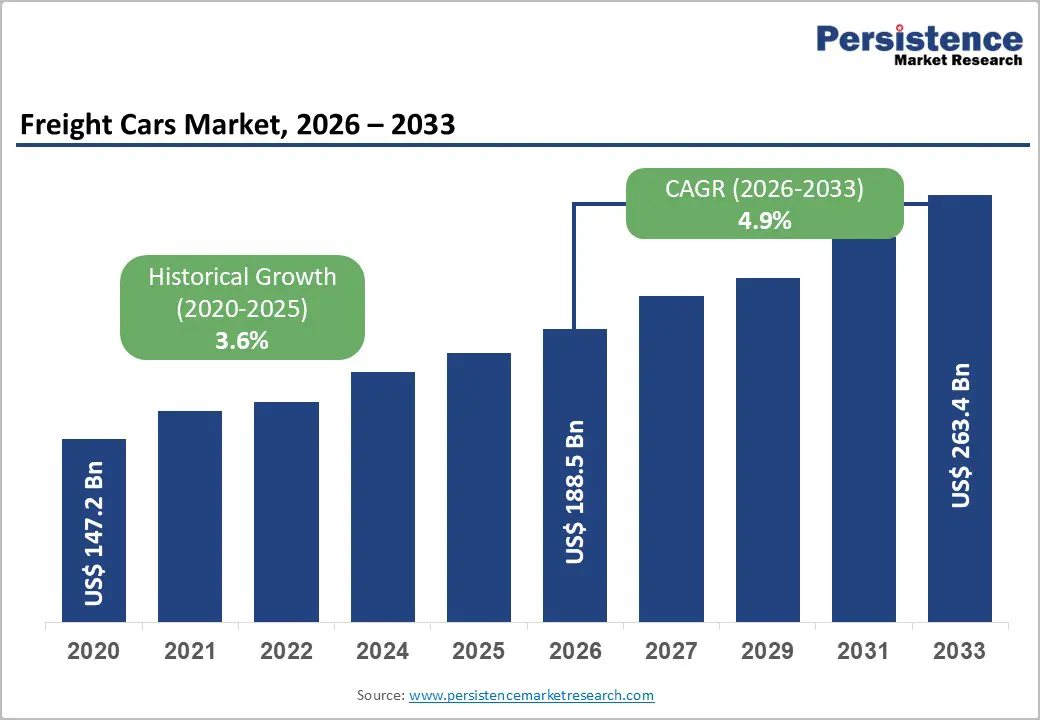

The global freight cars market size is likely to be valued at US$ 188.5 billion in 2026, and is projected to reach US$ 263.4 billion by 2033, growing at a CAGR of 4.9% during the forecast period 2026−2033. Market growth is driven by rising global trade volumes, modernization of rail networks, and increasing demand for cost-efficient freight transport solutions. The expansion of industrial production in emerging economies and urbanization trends are driving increased cargo transport needs, directly supporting fleet expansion and higher utilization of freight cars. Technological integration in rail logistics, including predictive maintenance, real-time monitoring, and automation, improves operational efficiency and reduces downtime, encouraging transport operators to adopt advanced freight car models.

Governments across North America, Europe, and the Asia Pacific are strengthening rail infrastructure and promoting rail freight over road transport to reduce environmental impact and congestion, creating a favorable policy environment. Diversification of freight cargo types, such as liquid chemicals, perishables, and automobiles, requires specialized freight cars with tailored safety and temperature-control features, thereby boosting market adoption. Private investment in rail operators and logistics providers is increasing, enabling procurement of modernized cars and deployment of digital fleet management systems.

Key Industry Highlights

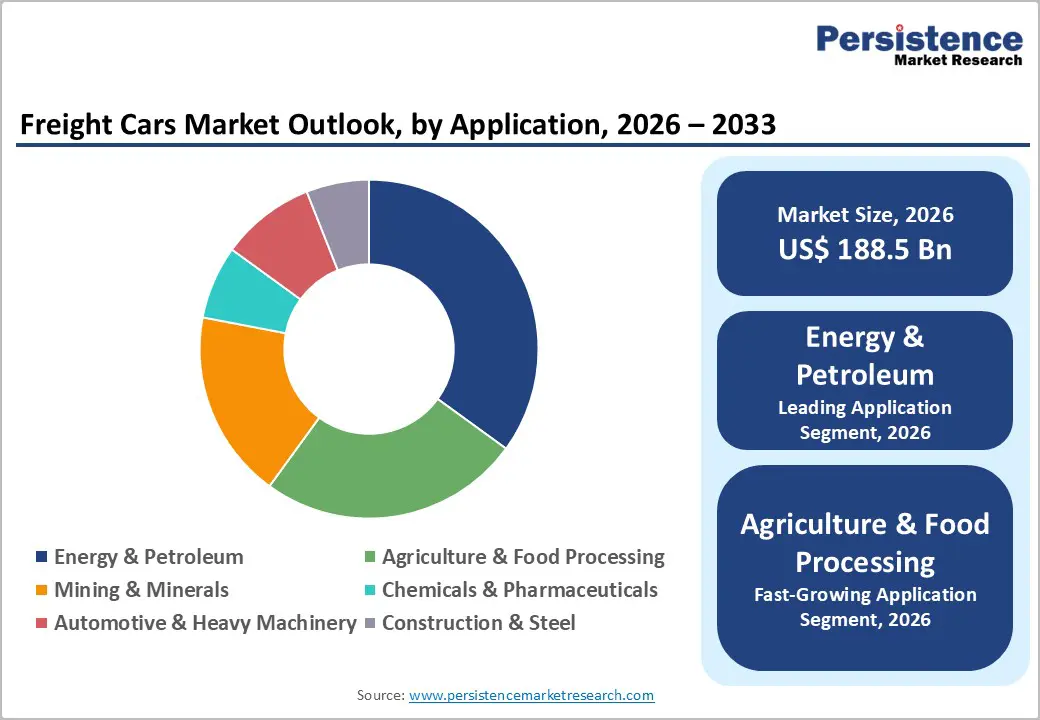

- Leading Application: Energy & petroleum is expected to lead with an estimated 35% market share in 2026, owing to high-volume tank car transport and secure handling of hazardous liquids.

- Fastest-growing Application: Agriculture & food processing is projected to register the highest 2026-2033 CAGR, fueled by the skyrocketing demand for grains.

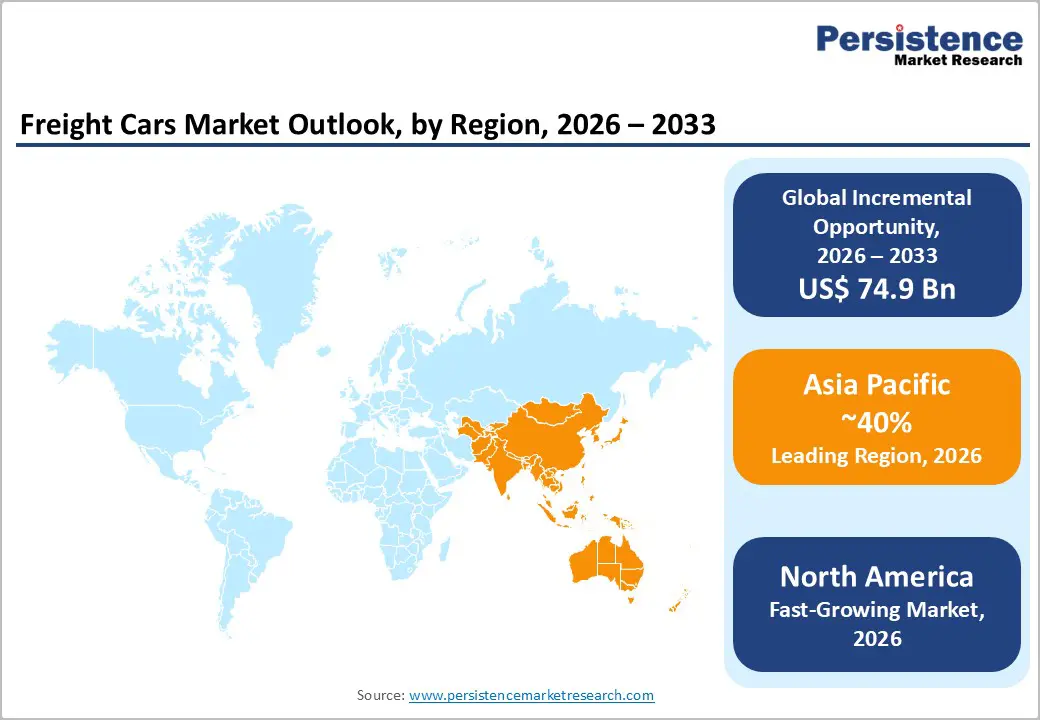

- Dominant Region: By 2026, the Asia Pacific is expected to dominate by holding roughly 44% market share, driven by China and India investing in high-capacity corridors.

- Fastest-growing Regional Market: North America is projected to be the fastest-growing market from 2026 to 2033, fueled by rail modernization and intermodal logistics.

- February 2026: W.H. Davis unveiled 35 next-generation box wagons to boost cargo capacity and operational flexibility.

| Key Insights | Details |

|---|---|

|

Freight Cars Market Size (2026E) |

US$ 188.5 Bn |

|

Market Value Forecast (2033F) |

US$ 263.4 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.9% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Industrial Expansion and Global Trade Growth

Industrial capacity growth directly correlates with freight movement requirements as manufacturers expand output and service broader distribution networks. Government data from India’s Ministry of Statistics and Programme Implementation (MoSPI) shows industrial production surged by 7.8% in December 2025, with manufacturing output leading the expansion and significant gains in sectors such as motor vehicles and basic metals. This growth reflects rising production of heavy and intermediate goods that rely on bulk transport infrastructure for delivery to ports, warehouses, and end markets. Domestic and export-focused factories demand consistent, high-volume land cargo movement, reinforcing rail transport’s strategic role in logistics chains, where fixed-route freight systems are more efficient for high-tonnage loads than roads.

Global trade expansion underpins cross-border goods movement, triggering higher demand for inland freight logistics to link production hubs with seaports and border crossings. Data from the United Nations Conference on Trade and Development (UNCTAD) indicates that world trade is on track to exceed US$ 35 trillion in 2025, rising about 7% from the previous year, driven by both goods and services. Larger trade volumes imply more raw materials entering manufacturing centers and finished goods requiring distribution across continents, increasing reliance on robust freight networks. Rail freight provides cost-effective long-haul capacity for containerized and bulk shipments, aligning with trade growth patterns that require predictable transit times and scalable cargo carriage.

Technological Modernization and Digitalization

Digital systems and modern technology are central to operational efficiency in freight rail, enabling real-time monitoring of rolling stock and infrastructure and reducing inefficiencies in scheduling, maintenance and logistics planning. Government-led digitalization efforts support the integration of telematics and sensor networks across freight operations, facilitating continuous data flow on location, condition and performance of rail assets. The operational benefits of these systems include improved asset utilization, reduced unscheduled maintenance and enhanced visibility of cargo movement, supporting more responsive decision-making for carriers and logistics managers. An example of industry momentum can be seen in telematics deployment trends. The global installed base of tracking devices on rail freight wagons reached 775,000 units worldwide by the end of 2024, reflecting expanding adoption of digital monitoring technologies.

Federal support mechanisms reinforce the move towards digital integration of freight transport. The U.S. Department of Transportation (DOT), through agencies such as the Bureau of Transportation Statistics (BTS), regularly collects detailed performance metrics on freight movement, strengthening national infrastructure planning and performance benchmarking, and reflecting the government's emphasis on data-driven transport policy. Government investment and regulatory attention on digital rail infrastructure signal recognition of its role in enhancing supply chain resilience, reducing transit delays and optimizing network throughput. Public sector frameworks that promote interoperability standards for digital systems and fund the deployment of advanced diagnostics and automation technologies contribute to a more efficient, resilient and competitive freight transport environment.

Regulatory and Operational Constraints

Operational limits and regulatory oversight emerge as key restraints due to their direct influence on capacity, costs, and the adoption of advanced practices in rail freight operations. In the U.S., new Federal Railroad Administration (FRA) requirements now mandate stringent compliance for newly built freight cars, including detailed provenance of materials and restrictions on components from certain countries of concern, enforced through certification before service entry and civil penalties for noncompliance. These rules increase production complexity and require additional documentation, engineering checks, and supply chain validation, slowing delivery timelines and elevating capital and administrative costs for original equipment manufacturers (OEMs) and operators. Conforming designs to evolving government standards simultaneously increases lead times and constrains flexibility in sourcing components or adopting innovative features when regulatory updates occur.

Operational inefficiencies arise from mandated safety procedures and staffing requirements that affect throughput and scheduling. Data published by the U.S. Bureau of Transportation Statistics in December 2025 indicates that the Truck-Rail Freight Transportation Services Index, which measures rail freight output, experienced only modest growth of 0.2% year-over-year, reflecting subdued capacity expansion relative to demand. Compliance with uniform crew staffing rules, regular inspections, and federal safety mandates adds labor and procedural overhead that can slow operations, limit train speed or length, and increase terminal dwell times as carriers align with national requirements.

Fluctuating Fuel and Energy Costs Affecting Operational Expenses

Variability in fuel and energy prices significantly increases operational risk for rail logistics. Diesel and other distillate fuels account for a large share of recurring transport costs, and even minor market swings can create substantial budgetary pressure. Price volatility forces carriers to revise pricing structures, renegotiate contracts, or absorb cost differences, reducing predictability in financial planning and complicating cash flow management. Exposure extends beyond locomotive fuel to include yard operations, terminal machinery, and auxiliary power systems, magnifying the impact of energy fluctuations on total operating expenses.

Long-distance rail operations depend on precise scheduling and pre-planned fuel allocation, and sudden energy price increases raise the cost per ton mile, compressing margins on low-yield routes and affecting competitiveness. Carriers with fixed-rate contracts face mismatches between expected and actual costs, requiring adjustments through surcharges that may meet customer resistance. Capital allocation for fleet modernization or technology upgrades becomes constrained as resources are redirected toward maintaining liquidity.

Opportunity Analysis- Adoption of Green Freight Solutions

Transitioning to environmentally friendly freight systems presents significant potential for the rail transport sector. Governments and regulatory bodies worldwide are implementing strict emission standards, compelling logistics operators to reduce carbon footprints. Freight cars powered by electrification or low-emission technologies offer a pathway to meet sustainability mandates while lowering energy costs. Rail transport already exhibits higher fuel efficiency compared to road transport, and optimizing freight cars for green operations amplifies this advantage. Companies aiming to improve corporate social responsibility (CSR) ratings increasingly prioritize investment in low-emission logistics, aligning operational strategies with sustainability frameworks and reporting standards.

Advances in technology are driving the integration of energy-efficient designs, lightweight materials, and renewable energy sources into freight cars. Smart monitoring systems track energy consumption, enabling predictive maintenance and reducing operational waste. Shifts in consumer and business demand toward greener supply chains create opportunities for freight providers to differentiate services. Markets in emerging economies investing in rail infrastructure can incorporate green solutions from the outset, improving operational efficiency while meeting environmental objectives. Adoption of green freight systems also supports participation in carbon credit programs, offering financial incentives alongside environmental benefits.

Expansion of Intermodal Logistics Combining Rail with Road and Sea Transport

Integration of rail, road, and sea transport creates a seamless logistics network that enhances the efficiency of cargo movement. Intermodal systems allow freight cars to connect directly with trucks and shipping vessels, reducing transit times and minimizing handling delays. This integration supports bulk and containerized shipments, enabling faster delivery schedules and optimized route planning. Companies can manage inventory more effectively, reducing storage costs and improving supply chain responsiveness. Real-time tracking and digital coordination across modes strengthen operational visibility, allowing logistics managers to anticipate disruptions and adjust transport flows accordingly.

Intermodal logistics drives cost efficiency by leveraging the strengths of each transport mode. Rail freight offers energy-efficient long-distance transport, road networks provide last-mile delivery flexibility, and maritime shipping reduces international transportation costs. Freight cars play a central role in this network, serving as the link that moves cargo between terminals without repeated unloading and loading. Investment in terminals, container handling systems, and digital platforms further amplifies the value of rail integration. Increasing demand for global trade and e-commerce shipments intensifies pressure on traditional single-mode transport, creating opportunities for freight car manufacturers and logistics providers to capture new markets through intermodal solutions.

Category-wise Analysis

Car Type Insights

Box cars are likely to capture an estimated 32% of the freight cars market revenue share in 2026, due to their versatility and ability to transport a wide range of goods under secure conditions. Box cars are preferred for transporting general cargo, consumer goods, and packaged materials that require protection from weather and handling risks. Industries including retail, automotive parts, and food processing favor box cars for reliability, damage prevention, and compatibility with intermodal transport. Operational efficiency, ease of loading and unloading, and compatibility with containerized freight systems reinforce preference among transport operators. The modular design of box cars allows for flexible interior configurations, improving cargo volume utilization. Integration with telematics enables real-time monitoring of cargo conditions, helping build trust in the transport of sensitive goods. Manufacturers continue to innovate with lightweight materials, increasing payload capacity and reducing energy consumption.

Reefer car is expected to witness the fastest growth between 2026 and 2033, as demand for temperature-controlled transport increases for perishable foods, pharmaceuticals, and chemical products. Growth is driven by the global expansion of cold chain logistics and rising consumer demand for fresh and safe products. Increasing adoption of digital temperature monitoring, energy-efficient refrigeration units, and integration with supply chain management systems enhances operational appeal. Emerging economies are investing in cold chain infrastructure, including rail connectivity, providing scalable deployment opportunities. Pharmaceutical and food sectors prioritize compliance with storage standards, favoring reefer cars equipped with IoT-based monitoring systems. Operators benefit from higher service reliability, reduced spoilage, and access to premium revenue streams.

Application Insights

Energy & petroleum is positioned as the leading segment with nearly 35% market share in 2026, supported by high-volume transport of crude oil, refined products, and natural gas. Tank cars are optimized for the secure handling of hazardous liquids and meet rigorous safety and environmental regulations. Energy infrastructure expansion, particularly in North America, Asia Pacific, and Europe, ensures consistent cargo flow, supporting fleet utilization. Operators prioritize compliance with regulatory mandates, such as the FRA tank car standards and the European Union (EU) Agreement concerning the International Carriage of Dangerous Goods by Road (ADR) regulations. Integration with pipelines, ports, and refinery networks enhances logistical efficiency. Specialized tank cars with double-wall construction, leak detection systems, and corrosion-resistant coatings minimize operational risk and support reliability.

Agriculture & food processing is expected to emerge as the fastest-growing segment between 2026 and 2033, driven by rising demand for grains, packaged foods, and temperature-sensitive agricultural products. Expansion of modern food supply chains, including cold storage facilities and intermodal transport hubs, supports the adoption of specialized cars. Operators benefit from scalable deployment across rural and urban regions, enabling efficient movement of agricultural commodities. Integration of monitoring systems ensures compliance with storage and handling standards, supporting trust and reliability. Demand for perishable and packaged goods, coupled with government initiatives to enhance food security and logistics efficiency, increases adoption of suitable freight cars. Technological solutions such as modular box and reefer cars improve cargo protection and operational efficiency, sustaining high growth.

Regional Insights

North America Freight Cars Market Trends

North America is forecasted to be the fastest-growing market for freight cars between 2026 and 2033, stimulated by significant investment in rail infrastructure modernization and expansion of intermodal logistics networks. Increasing demand for energy-efficient long-haul transport drives adoption of freight cars with higher payload capacity and advanced safety features. Key industries, including automotive, chemicals, agriculture, and e-commerce, require reliable bulk and containerized cargo solutions, creating sustained pressure for fleet expansion. Implementation of digital monitoring systems and predictive maintenance technologies enables operators to optimize fleet utilization and reduce downtime, improving overall operational efficiency. Upgrades to terminals, automated loading systems, and real-time cargo tracking strengthen supply chain resilience, allowing integration across rail, road, and port networks, which accelerates market growth.

Policy initiatives focused on sustainable transport and reduction of carbon emissions support transition from road to rail for heavy cargo, making freight cars a central element of logistics strategy. Adoption of specialized freight car designs, such as double-stack container cars, refrigerated cars, and tankers, addresses diverse cargo requirements while reducing operational costs. Public-private collaborations facilitate investment in advanced infrastructure and digital platforms, enabling faster turnaround times and streamlined cargo flow. Rising cross-border trade volumes and emphasis on just-in-time delivery systems further increase demand for high-capacity, reliable freight solutions.

Europe Freight Cars Market Trends

Europe maintains a strong position in the freight cars market due to its advanced rail infrastructure and high adoption of technology-driven logistics solutions. Investment in high-speed freight corridors and modernization of existing cargo lines supports efficient movement of bulk and containerized goods across industrial and commercial hubs. Industries such as automotive, chemicals, and steel rely on specialized freight cars including tank, hopper, and flat cars to meet production and distribution requirements. Integration of real-time tracking, automated scheduling, and predictive maintenance enhances fleet utilization, reduces operational downtime, and improves cost efficiency. Expansion of intermodal terminals and inland ports allows seamless transfer between rail, road, and maritime transport, strengthening network connectivity and service reliability.

Sustainability initiatives and strict environmental regulations drive adoption of energy-efficient and low-emission freight solutions. Investment in electrified rail lines and innovative freight car designs with higher payload capacity supports compliance while maintaining operational performance. Public-private partnerships enable upgrades to digital logistics platforms, automated loading systems, and cargo monitoring tools, improving transparency and operational predictability. Increasing demand for cross-border trade and timely delivery of industrial goods amplifies reliance on rail transport as a competitive logistics solution. Advanced fleet management and predictive analytics allow operators to anticipate maintenance needs and optimize routing, improving service quality and reducing costs.

Asia Pacific Freight Cars Market Trends

Asia Pacific is poised to lead with an estimated 44% of the freight cars market share in 2026, supported by extensive investments in rail infrastructure and development of high-capacity freight corridors. Countries such as China and India contribute significantly to market leadership. China maintains the world’s largest rail freight network and continuously expands dedicated cargo lines to connect industrial zones and ports, enabling efficient bulk and containerized shipment movement. India drives growth through modernization of freight corridors and increased investment in intermodal terminals, improving last-mile connectivity and operational efficiency. Japan supports advanced logistics through high-tech freight cars with automated monitoring and predictive maintenance, ensuring reliability in handling industrial and export cargo.

Industrial growth, export-oriented manufacturing, and government policies favoring energy-efficient rail transport amplify demand in these countries. Steel, coal, chemical, and automotive sectors rely heavily on specialized freight cars such as hopper, tank, and flat cars, driving adoption. Public-private partnerships and technology deployment, including real-time tracking systems and automated scheduling, optimize cargo flow and reduce turnaround times. Investment in fleet expansion, modern terminals, and predictive maintenance solutions allows effective handling of increasing cargo volumes, ensuring reliability and cost efficiency.

Competitive Landscape

The global freight cars market exhibits a moderately consolidated structure, with leading manufacturers collectively holding approximately 60% of global revenue, reflecting significant influence over pricing, technology adoption, and product standards. Key players such as Caterpillar, Saint-Gobain, HOLCIM, Knauf Industries, and Sumitomo Corporation dominate high-value segments, leveraging advanced manufacturing capabilities, extensive distribution networks, and strong brand recognition. Capital-intensive production, stringent regulatory compliance, and integration of digital monitoring and safety technologies create high entry barriers, limiting the ability of new entrants to compete at scale.

Market concentration is particularly pronounced in specialized freight car segments such as tank cars and refrigerated cars, where adherence to safety and environmental regulations is critical. Leading operators benefit from economies of scale and long-standing relationships with industrial clients, ensuring consistent demand and reduced risk exposure. Conversely, fragmentation is more evident in bulk cargo and standard box car segments, where regional suppliers focus on competitive pricing, service customization, and flexible delivery schedules to capture niche demand. This dynamic allows regional manufacturers to maintain relevance despite the dominance of global players, particularly in markets with emerging infrastructure and industrial growth.

Key Industry Developments

- In November 2025, GATX Rail Europe and DB Cargo AG received competition authority approval for a sale-and-leaseback deal involving about 6,000 freight cars, enhancing flexibility for the operator and expanding the leasing fleet to roughly 36,500 units.

- In November 2025, Knorr-Bremse and VTG Rail UK signed a long-term framework agreement for exclusive delivery of at least 2,000 FreightControl Sentinel digital systems for freight wagons, advancing real-time monitoring, safety, and efficiency across modern freight operations.

- In August 2025, Egypt’s national rail operator announced plans to launch an international tender for the operation and management of more than 1,500 rail cars, including over 1,300 Russian and Hungarian-made coaches, as part of broader efforts to involve private firms in modernizing rail services and freight operations.

Companies Covered in Freight Cars Market

- Caterpillar.

- Saint-Gobain

- HOLCIM

- Knauf Industries.

- Sumitomo Corporation

- Kawasaki Heavy Industries, Ltd.

- Amsted Rail Company, Inc.

- Tata Steel

Frequently Asked Questions

The global freight cars market is projected to reach US$ 188.5 billion in 2026.

Rising industrial production, growing trade volumes, and investment in rail infrastructure are driving the market.

The market is poised to witness a CAGR of 4.9% from 2026 to 2033.

Development of intermodal logistics, adoption of advanced freight technologies, and fleet modernization present key market opportunities.

Some of the key market players include Caterpillar, Saint-Gobain, HOLCIM, Knauf Industries, and Sumitomo Corporation.