- Specialty & Fine Chemicals

- Flame Retardant Market

Flame Retardant Market Size, Share, and Growth Forecast 2026 - 2033

Flame Retardant Market by Product (Halogenated, Non-halogenated), Application (Polyolefins, Epoxy Resins, UPE, PVC, ETP, Rubber, Styrenics, Others), End-user (Construction, Transportation, Electrical & Electronics, Others), and Regional Analysis 2026 - 2033

Flame Retardant Market Size and Trend Analysis

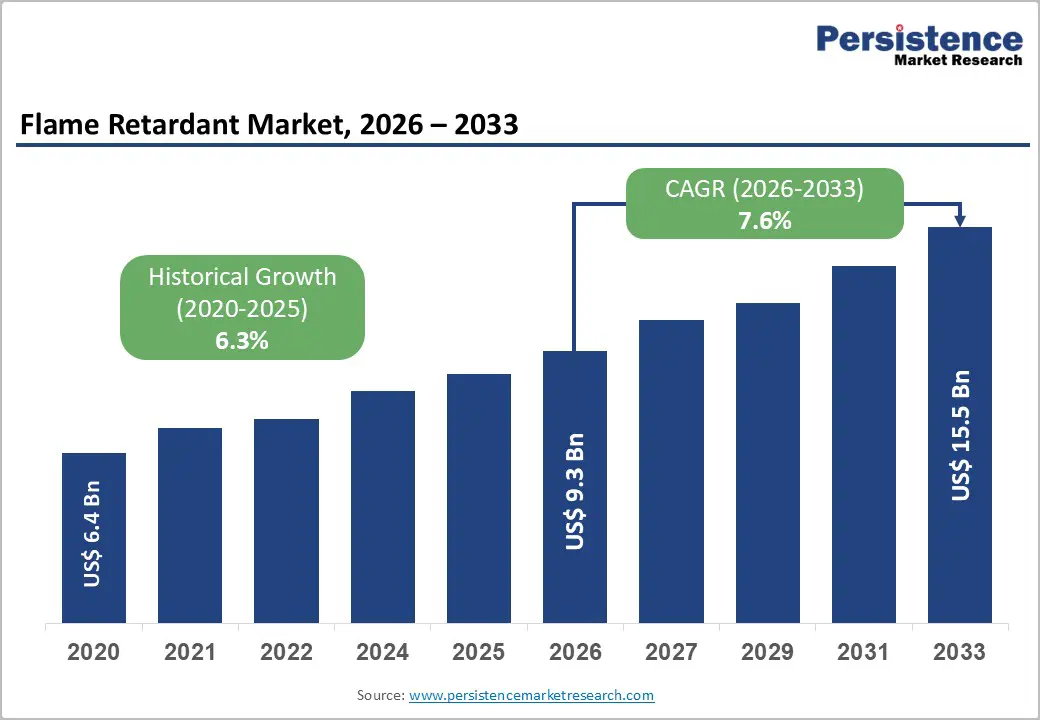

The global Flame Retardant market size is likely to be valued at US$ 9.3 billion in 2026 and is expected to reach US$ 15.5 billion by 2033, growing at a CAGR of 7.6% during the forecast period from 2026 to 2033.

The market's robust and accelerating growth trajectory is fundamentally anchored in the global construction sector's rapid expansion, the electrification of transportation, and escalating fire safety regulatory requirements across all major end-use industries, factors that collectively mandate increasing flame retardant incorporation into polymers, resins, and composite materials.

Key Industry Highlights:

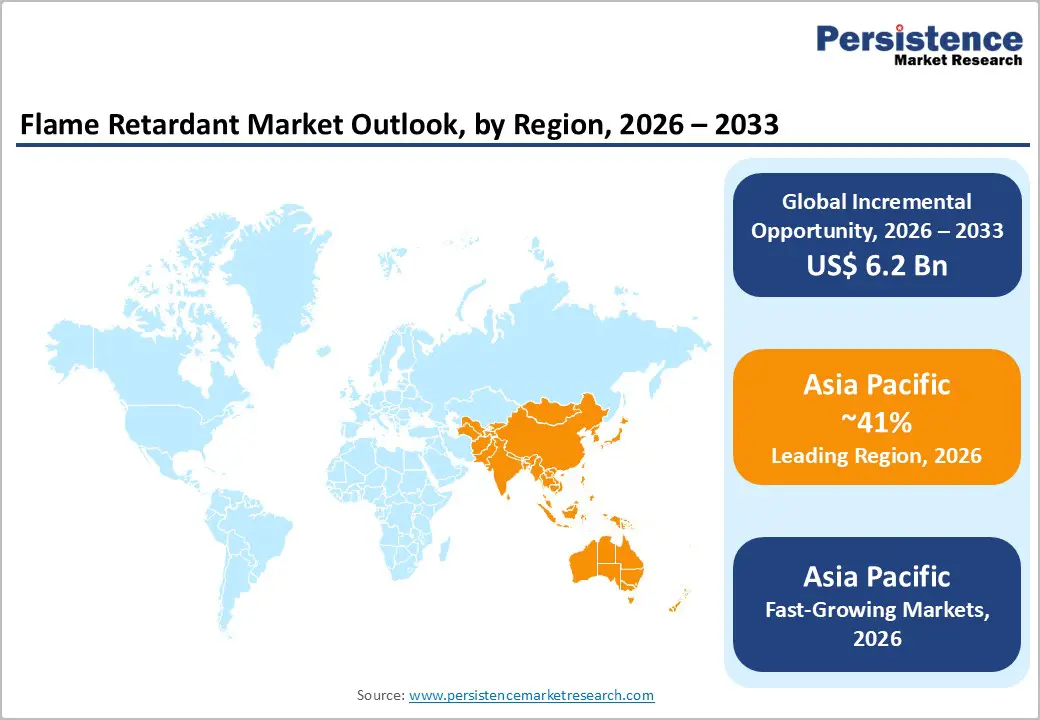

- Leading Region: Asia Pacific leads the global Flame Retardant market, holding 41% share, driven by China's world-scale construction and wire and cable industries under mandatory GB 8624 and GB/T 18380 fire standards, India's PM Gati Shakti infrastructure program, and the region's dominant electronics manufacturing base spanning South Korea, Japan, Taiwan, and ASEAN nations.

- Fastest-Growing Region: Asia Pacific is also the fastest-growing region with a rising CAGR of 8.9%, with India's Smart Cities Mission targeting 100 urban development projects, China's National Bureau of Statistics documenting billions of square meters of annual new construction, and accelerating EV manufacturing across the region, generating structurally new polymer flame retardant demand in battery and powertrain component applications.

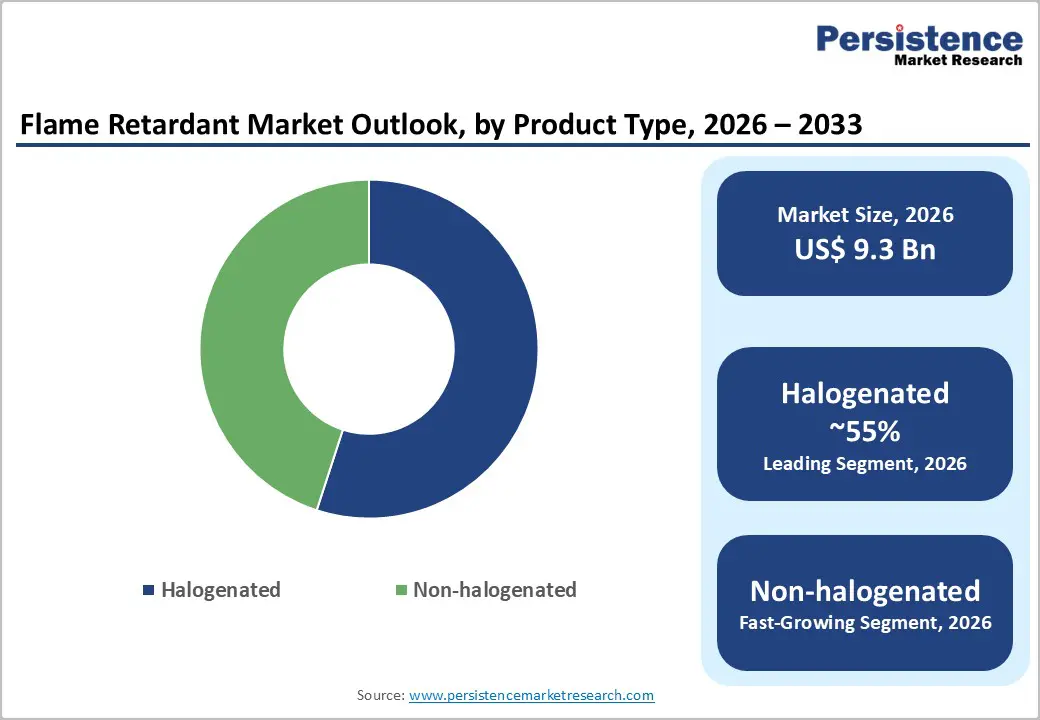

- Leading Product Segment: Halogenated flame retardants dominate the product segment with approximately 55% revenue share in 2026, anchored by TBBPA's entrenched position in PCB epoxy resin laminates under current RoHS exemptions and brominated systems' established performance advantages at lower additive loadings across styrenics, PVC, and engineering thermoplastic applications globally.

- Fastest-Growing Segment: Non-halogenated flame retardants are the fastest-growing product segment, propelled by the EU Chemicals Strategy for Sustainability, Stockholm Convention POPs restrictions on legacy BFRs, and corporate ESG mandates, with Nabaltec AG's APYRAL, Clariant's Exolit OP, and ADEKA Corporation's ADK STAB FP series leading commercial adoption across wire and cable, construction, and EV applications.

- Key Opportunity: EV battery systems and data center infrastructure expansion represent the key market opportunity, with IEA confirming 17 million EV sales in 2023 and IDC projecting US$ 1 trillion in cumulative data center investment through 2027, generating structurally growing procurement demand for halogen-free, UL 94 V-0-rated flame retardant engineering polymers from BASF, DuPont, and Avient Corporation.

| Key Insights | Details |

|---|---|

|

Flame Retardant Market Size (2026E) |

US$ 9.3 Billion |

|

Market Value Forecast (2033F) |

US$ 15.5 Billion |

|

Projected Growth CAGR (2026–2033) |

7.6% |

|

Historical Market Growth (2020–2025) |

6.3% |

Market Dynamics

Drivers - Stringent Global Fire Safety Regulations across Construction and Electrical Industries Mandating Flame Retardant Adoption

The increasing enforcement of fire safety regulations across the construction, electrical and electronics, and transportation industries is a major structural driver supporting the growth of the flame retardant market. Governments and regulatory authorities worldwide are introducing stricter safety standards that require manufacturers to integrate flame retardant formulations into a wide range of polymer and composite materials. In the European Union, the Construction Products Regulation (CPR) requires fire performance classification of construction materials under the EN 13501 standard series, mandating flame retardant treatment for insulation, cables, wall panels, and flooring products.

Similarly, in the United States, organizations such as the Consumer Product Safety Commission (CPSC) and the National Fire Protection Association (NFPA) enforce flammability standards including NFPA 701 for fabrics and NFPA 285 for exterior wall assemblies. In addition, the International Electrotechnical Commission’s IEC 60332 standard governing fire performance of electric cables is widely adopted across more than 150 countries, ensuring consistent demand for flame retardants used in wire and cable insulation worldwide.

Rapid Electrification of Vehicles and Expansion of EV Battery Infrastructure Generating New Flame Retardant Demand

The rapid transition of the global automotive industry toward battery electric vehicles (BEVs) and hybrid electric vehicles (HEVs) is creating a new and highly technical demand segment for advanced flame retardant materials. Electric vehicles require specialized flame retardant solutions in battery pack enclosures, high-voltage cable harnesses, motor housings, and thermal management components to ensure operational safety. Lithium-ion batteries used in EVs carry inherent fire risks because they can undergo thermal runaway reactions that generate extreme heat exceeding 800°C. To mitigate this risk, manufacturers increasingly rely on flame retardant-treated polymers, composite materials, and protective coatings within battery management systems. According to the International Energy Agency’s Global EV Outlook 2024, global EV sales surpassed 17 million units in 2023, accounting for nearly 18% of total global car sales, while total EV stock exceeded 40 million vehicles. Each electric vehicle requires significantly higher quantities of flame-retarded polymer components compared to conventional vehicles, making EV adoption a strong long-term demand driver for flame retardant manufacturers.

Restraints - Health and Environmental Concerns Over Halogenated Flame Retardants Driving Regulatory Restrictions

Growing concerns regarding the environmental and human health impact of traditional halogenated flame retardants are becoming a key restraint for the flame retardant market. Certain brominated flame retardants, including polybrominated diphenyl ethers (PBDEs) and hexabromocyclododecane (HBCD), have been associated with environmental persistence, bioaccumulation, and potential endocrine disruption risks. As a result, global regulatory authorities are introducing stricter restrictions and phased bans on several halogenated flame retardant chemicals. The Stockholm Convention on Persistent Organic Pollutants, administered by the United Nations Environment Programme, has identified multiple brominated compounds as restricted substances due to their long-term environmental impact and toxicity concerns.

In addition, the European Chemicals Agency continues to expand the restriction and authorization lists under the REACH regulation, adding additional halogenated flame retardants for regulatory monitoring or phase-out. These regulatory developments create compliance challenges for manufacturers that rely on traditional brominated chemistry, forcing them to reformulate products, invest in alternative technologies, and adapt to evolving global environmental safety standards.

High Raw Material Costs and Supply Chain Volatility of Bromine and Phosphorus Impacting Market Stability

The flame retardant industry relies heavily on specialized raw materials such as bromine and phosphorus compounds, making the supply chain vulnerable to price fluctuations and supply disruptions. Bromine is a key raw material used in halogenated flame retardant systems, while phosphorus-based chemicals are widely used in non-halogenated alternatives. However, global bromine production is highly concentrated geographically, with Israel and Jordan accounting for a significant share of total global supply. This concentration increases the risk of supply shortages due to geopolitical tensions, logistics disruptions, or environmental compliance issues at major extraction facilities.

According to the United States Geological Survey’s Mineral Commodity Summaries, bromine is considered a strategically important mineral with limited production diversification. Such supply concentration can lead to sudden price volatility, which affects production costs for flame retardant manufacturers. Smaller and mid-sized producers without long-term raw material supply agreements are particularly exposed to these fluctuations, creating financial uncertainty and procurement challenges across the industry.

Opportunity - Non-Halogenated Flame Retardants Emerging as the Fastest-Growing Product Segment Driven by Regulatory and ESG Pressure

The global shift from halogenated to non-halogenated flame retardant systems represents one of the most important long-term growth opportunities in the flame retardant market. This transition is primarily driven by tightening environmental regulations, increasing corporate ESG commitments, and sustainability goals adopted by manufacturers and consumer brands. Non-halogenated flame retardants include metal hydroxides such as aluminum trihydroxide and magnesium hydroxide, as well as phosphorus-based and nitrogen-based compounds used in advanced intumescent systems.

These alternatives are gaining rapid adoption across wire and cable, construction insulation, and electronics applications where compliance with regulations such as REACH and RoHS is mandatory. The European Green Deal and the EU Chemicals Strategy for Sustainability aim to gradually eliminate hazardous chemicals, including persistent organic pollutants, from industrial applications. As a result, manufacturers are accelerating the development and adoption of environmentally safer flame retardant formulations. Leading suppliers including Huber Engineered Materials, Nabaltec AG, and ADEKA Corporation are expanding non-halogenated product portfolios to meet this growing market demand.

Data Center and 5G Infrastructure Expansion Creating High-Volume Demand for Flame Retardant Engineering Polymers

The rapid expansion of global data center infrastructure and next-generation 5G telecommunications networks is creating a strong new demand source for flame retardant materials. Modern data centers require large volumes of flame retardant-treated polymers for server racks, cable management systems, printed circuit boards, power equipment housings, and structural enclosures. As hyperscale cloud infrastructure continues to expand worldwide, demand for materials that meet strict fire safety standards such as UL 94 V-0 and 5VA ratings is increasing steadily. The International Data Corporation projects that global data center infrastructure investment will exceed US$1 trillion by 2027, highlighting the massive scale of future infrastructure expansion.

The GSMA’s Mobile Economy report indicates that global 5G connections surpassed 1.9 billion in 2023 and are expected to reach 5.5 billion by 2030. Each new base station, networking cabinet, and telecom equipment enclosure requires flame retardant engineering plastics, creating sustained procurement demand for advanced polymer compounds used in these rapidly expanding digital infrastructure ecosystems.

Category-wise Analysis

By Product Insights

Halogenated flame retardants lead the global Flame Retardant market by product type, accounting for approximately 55% of total product segment revenue in 2026. Their strong position is supported by widespread use across high-volume polymer applications such as PVC cables, styrenics, epoxy resins for printed circuit boards, and engineering thermoplastics. These materials provide effective flame resistance at relatively low additive levels compared to most non-halogenated alternatives. Halogenated systems, particularly brominated flame retardants like tetrabromobisphenol A (TBBPA) and decabromodiphenyl ethane (DBDPE), are among the most established chemistries in the market.

They benefit from decades of application data, regulatory approvals under certain RoHS and REACH exemptions for electronics, and well-developed global supply chains. Companies such as ICL, Albemarle Corporation, and Lanxess remain key suppliers of brominated flame retardants due to their large-scale manufacturing and technical expertise. At the same time, the non-halogenated segment is growing the fastest, driven by stricter environmental regulations and increasing demand for sustainable flame retardant solutions across construction, automotive, and wire and cable applications worldwide.

By Application Insights

Polyolefins represent the leading application segment in the global Flame Retardant market, accounting for approximately 28% of total application segment revenue in 2026. This dominance is mainly due to the widespread use of polyolefin polymers such as polyethylene (PE), polypropylene (PP), and their copolymers across multiple industries. These materials are commonly used in wire and cable insulation, construction membranes, piping systems, and automotive components. According to PlasticsEurope, polyolefins account for nearly half of global plastic production by volume.

Since many of these applications must meet strict fire safety standards, flame retardant additives are widely incorporated into polyolefin compounds. Non-halogenated systems such as intumescent additives and metal hydroxides are particularly important in wire and cable applications that must comply with standards like IEC 60332-1 and EN 50399. Companies such as Huber Engineered Materials and Nabaltec AG supply aluminum trihydroxide products specifically designed for these applications. Epoxy resins form the second-largest application segment, largely due to their use in printed circuit board laminates and structural composites.

By End-user Insights

The Electrical & Electronics sector is the largest end-use segment in the global Flame Retardant market, accounting for approximately 34% of total end-use segment revenue in 2026. This leadership reflects the extensive use of flame-retardant polymers in electronic devices, power distribution equipment, consumer electronics, data centers, and telecommunications infrastructure. Global safety standards such as IEC 60950 and IEC 62368 require electronic equipment to meet strict flammability requirements before entering most international markets. As a result, manufacturers across the electronics supply chain rely heavily on flame retardant materials for housings, connectors, and internal components.

The World Semiconductor Trade Statistics organization reported global semiconductor revenues exceeding US$550 billion in 2023, highlighting the scale of electronics manufacturing that supports flame retardant demand. Advanced solutions such as FRX Innovations’ Nofia phosphonate oligomer technology and Clariant’s Exolit phosphorus-based products provide high-performance, non-halogenated alternatives for sensitive electronics applications. The construction industry represents the second-largest end-use segment, supported by strict building fire safety standards worldwide.

Regional Insights

North America Flame Retardant Trends

North America is a major regional market for flame retardants, supported by the United States’ strong fire safety regulations and enforcement frameworks. Standards issued by organizations such as the National Fire Protection Association (NFPA), UL certification bodies, and ASTM testing agencies require strict fire performance compliance across construction, automotive, and electrical products. These regulations create consistent demand for flame retardant materials across multiple industries. In addition, regulatory requirements from agencies such as the Federal Aviation Administration (FAA) and the Federal Railroad Administration (FRA) mandate high-performance fire-resistant materials for aircraft interiors and rail vehicles.

Albemarle Corporation and Huber Engineered Materials are among the leading domestic producers supplying flame retardants to both regional and global markets. Demand is also supported by the U.S. Green Building Council’s LEED certification program and ASTM E84 Class A standards for interior building materials. Meanwhile, California’s environmental regulations, including Proposition 65 and the DTSC Green Chemistry program, are accelerating the shift toward non-halogenated flame retardant technologies.

Europe Flame Retardant Trends

Europe is widely recognized as the global leader in flame retardant regulatory compliance and innovation in non-halogenated technologies. The region operates under strict chemical safety frameworks including the REACH Regulation, RoHS Directive, Construction Products Regulation (CPR), and the EU Chemicals Strategy for Sustainability. These policies require careful evaluation and registration of flame retardant substances before they can be used commercially. Germany leads regional demand due to its strong chemicals industry and large automotive, construction, and electronics sectors.

Major companies such as BASF SE, Clariant, and Lanxess play a significant role in supplying advanced flame retardant materials across Europe. Government policies such as the German Building Energy Act and the EU Energy Performance of Buildings Directive are increasing insulation installations, which must meet strict fire safety classifications. The United Kingdom continues to follow a similar framework through UK REACH after Brexit. Meanwhile, organizations such as the European Flame Retardants Association work with regulators to support balanced policies that maintain both fire safety and industrial innovation.

Asia Pacific Flame Retardant Trends

Asia Pacific is the largest and fastest-growing regional market for flame retardants, driven by rapid industrialization and strong growth in electronics, construction, and automotive manufacturing. China plays a central role as both the world’s largest producer and consumer of flame-retardant polymer materials used in cables, construction products, and electronics components. National fire safety standards such as GB 8624 for building materials and GB/T 18380 for wire and cable flammability require manufacturers to incorporate flame retardant technologies in many products.

China’s construction sector continues to expand significantly, adding billions of square meters of floor space each year and generating large demand for fire-safe building materials. India is also experiencing strong growth due to major infrastructure initiatives such as the PM Gati Shakti National Master Plan and the Smart Cities Mission. Meanwhile, Japan’s advanced electronics industry maintains demand for high-purity flame retardant materials that meet strict Japanese Industrial Standards.

Competitive Landscape

The global flame retardant market is moderately consolidated, with several large specialty chemical companies controlling the majority of high-volume product segments. Leading players such as Albemarle Corporation, ICL, LANXESS, BASF SE, and Clariant dominate the market through large manufacturing capacities, strong raw material integration, and global technical support networks. These companies compete by offering advanced product formulations, regulatory compliance expertise, and extensive application testing capabilities.

Their laboratories conduct performance testing based on international standards such as UL, IEC, and EN to ensure that flame retardant materials meet strict safety requirements. Innovation in sustainable chemistry is also becoming an important competitive factor. For example, companies are developing halogen-free and environmentally friendly solutions to address evolving regulatory requirements. Firms such as FRX Innovations and Italmatch Chemicals are expanding in this area by offering specialized flame retardant technologies designed for modern polymer applications while supporting customers with regulatory documentation and formulation expertise.

Key Developments:

- In January 2025: Albemarle Corporation expanded production capacity for its SAYTEX brominated flame retardants at the Magnolia, Arkansas facility to address increasing global demand for fire-safety additives used in electronics, transportation, and industrial materials. The investment supports advanced polymer substrate applications and strengthens supply reliability for high-performance flame retardant systems.

- In September 2024: Clariant introduced an expanded Exolit OP series of halogen-free phosphorus flame retardants designed for engineering thermoplastics used in electric vehicle battery systems. The new solutions help manufacturers achieve UL 94 V-0 fire safety ratings while supporting lightweight, high-voltage battery enclosure designs in modern EV platforms.

- In March 2024: LANXESS expanded its Levagard and Disflamoll phosphorus-based flame retardant portfolio to strengthen its presence in Europe and Asia. The expanded product range focuses on halogen-free, REACH-compliant solutions for polyurethane foams and engineering plastics, supporting rising demand for sustainable fire-safety additives.

Companies Covered in Flame Retardant Market

- Albemarle Corporation

- ICL

- LANXESS

- Clariant

- Italmatch Chemicals S.p.A.

- Huber Engineered Materials

- BASF SE

- Thor

- DSM

- FRX Innovations

- DuPont

- J.M. Huber Corporation

- Nabaltec AG

- ADEKA Corporation

- Avient Corporation

- Momentive Performance Materials Inc.

- Presafer Chemical Co., Ltd.

- Ampacet Corporation

Frequently Asked Questions

The global Flame Retardant market is estimated to be valued at US$ 9.3 Billion in 2026 and is projected to reach US$ 15.5 Billion by 2033, registering a forecast CAGR of 7.6% from 2026 to 2033. The market recorded a historical CAGR of 6.3% between 2020 and 2025, driven by expanding fire safety regulations and growing demand from construction, electrical, and automotive end-use industries.

The key growth drivers are progressively tightening global fire safety regulations, with the EU's CPR, IEC 60332, UL 94, and NFPA standards mandating certified flame retardant systems across construction and electrical products, and the global EV transition, confirmed by the IEA's documentation of 17 million EV sales in 2023, generating structurally new demand for high-performance halogen-free flame retardant engineering thermoplastics in battery enclosure and powertrain component applications.

Halogenated flame retardants lead the Product category with approximately 55% revenue share in 2026, anchored by TBBPA's entrenched and RoHS-exempt position in PCB epoxy laminate manufacturing and brominated systems' established performance advantages at lower additive loadings across styrenics, PVC, and ETP applications. However, the Non-halogenated segment is the fastest-growing product category, driven by EU REACH restrictions, Stockholm Convention POPs listings, and corporate sustainability mandates.

Asia Pacific leads the global Flame Retardant market, anchored by China's mandatory GB 8624 and GB/T 18380 fire performance standards enforced across its world-scale construction and wire and cable industries, the region's dominant electronics manufacturing base, and India's PM Gati Shakti and Smart Cities Mission infrastructure programs generating accelerating flame retardant-treated construction material and cable procurement demand.

The most significant opportunity is the non-halogenated flame retardant segment's expansion driven by the EU Chemicals Strategy for Sustainability, Stockholm Convention restrictions on legacy brominated compounds, and EV battery system requirements, with Clariant's Exolit OP, Nabaltec AG's APYRAL, and ADEKA Corporation's ADK STAB FP series commercially positioned to capture structurally growing demand from automotive, wire and cable, and data center infrastructure application segments globally.