- Industrial Machinery

- Fabric Inspection Machine Market

Fabric Inspection Machine Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Fabric Inspection Market by Machine Type (Roll-to-Roll Inspection Machines, Flatbed Inspection Machines, Woven Fabric Inspection Machines), Technology (Automatic, Semi-automatic, Manual), Industry(Textiles & Apparel, Home Textiles, Technical Textiles, Others), and Regional Analysis for 2026 to 2033

Market Overview

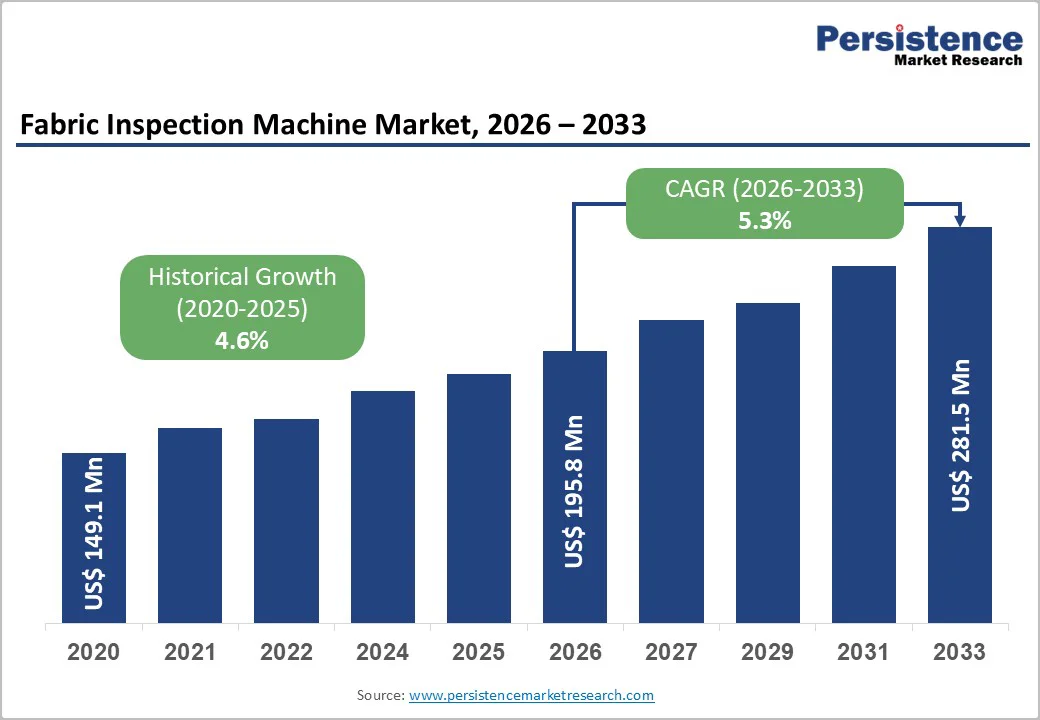

The global fabric inspection machine market size was valued at US$195.8 Million in 2026 and is projected to reach US$281.5 Million by 2033, growing at a CAGR of 5.3% between 2026 and 2033.

This growth reflects rising automation intensity in textile manufacturing, tighter export quality norms, and the transition from manual to digital inspection methods across high-volume fabric production lines. The historical phase from 2020 to 2026 registered a CAGR of 4.7%, indicating that adoption is accelerating as inspection becomes a core element of operational excellence rather than a peripheral quality function. Increased emphasis on first-pass yield, traceability, and sustainable production is encouraging mills and converters in Asia Pacific, Europe, and North America to upgrade legacy systems with integrated, data-enabled inspection platforms.

Key Highlights Summary

- Machine type leadership: Roll-to-roll inspection machines hold about 38% share, supported by their suitability for continuous high-speed production lines handling a broad range of fabrics.

- Fastest-growing machine subsegment: Woven fabric inspection machines grow at about 5.3% CAGR, capturing demand from higher-value woven applications in apparel, home, and technical textiles.

- Technology mix: Semi-automatic machines lead with ~39% share today, but automatic inspection systems are the fastest-growing technology at ~6.3% CAGR and are gaining share via AI and machine vision integration.

- End-use pattern: Textiles & Apparel account for around 48% of demand, while the automotive segment grows at roughly 5.9% CAGR on the back of stringent OEM quality and safety requirements.

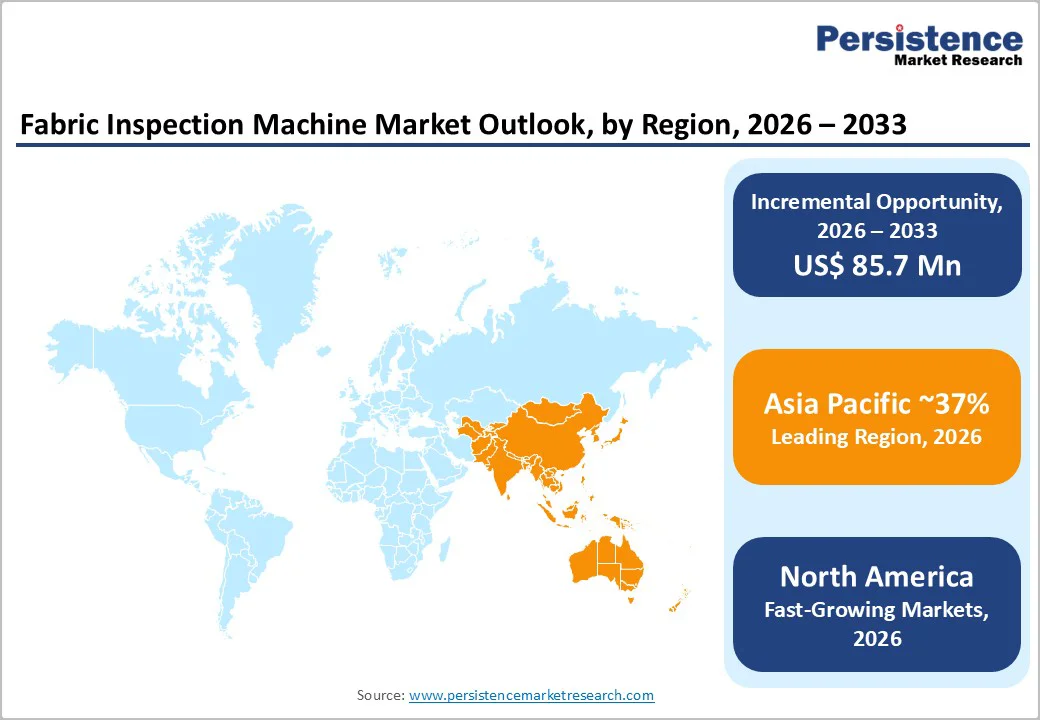

- Regional outlook: Asia-Pacific holds about 37% share and leads growth at ~6.6% CAGR, followed by Europe with a 25% share and a 4.5% CAGR, and North America with a ~5.0% CAGR.

- Strategic trends: AI-enabled vision, Industry 4.0 integration, and emerging market localization dominate recent strategic initiatives, supporting higher-value service revenues and deeper customer lock-in for leading suppliers.

| Key Insights | Details |

|---|---|

| Fabric Inspection Machine Market Size (2026E) | US$ 195.8 million |

| Market Value Forecast (2033F) | US$ 281.5 million |

| Projected Growth CAGR (2026 - 2033) | 5.3% |

| Historical Market Growth (2020 - 2025) | 4.6% |

Market Dynamics Analysis

Market Drivers

Expanding Textile Output and Rising Quality Standardization

Global textile and apparel output continues to expand, particularly in Asia-Pacific hubs such as China, India, Bangladesh, and Vietnam, which scale up capacities to serve international brands. Exporters must comply with buyer protocols, ISO norms, and EU safety requirements, elevating the need for structured fabric inspection to meet acceptable defect limits. In Bangladesh and Vietnam, export-driven garment clusters increasingly deploy inline and end-of-line inspection to satisfy AQL criteria and avoid costly rejection, driving demand for advanced inspection systems. As brands pursue near-zero-defect policies, automated inspection enables the detection of subtle weaving faults, stains, shade variation, and coating inconsistencies that manual methods overlook. This capability prevents chargebacks and return issues, improving productivity and payback cycles. A compounded driver emerges as brands digitize quality protocols across supplier networks, compelling even mid-size mills in emerging regions to adopt automated solutions to remain qualified suppliers.

Labor Cost Pressures and Workforce Constraints

In North America and Western Europe, textile and technical textile manufacturers face rising labor costs and difficulty attracting younger workers for repetitive inspection activities. Manual inspection requires sustained visual focus under intense lighting, leading to fatigue, inconsistency, and high turnover, which directly influence defect rates. Even in lower-wage regions, sustained wage escalation and tightening minimum wage rules prompt producers to reconsider labor-dependent inspection models. Automated fabric inspection systems substantially reduce operator requirements per line and ensure consistent defect detection, lowering the cost per inspected meter over the equipment's lifespan. When capital cost is evaluated against savings in labor, scrap, rework, and reduced complaints, automation becomes economically viable even for mid-sized producers. Additionally, redeploying scarce personnel from monotonous inspections to higher-value roles, such as maintenance and process improvement, supports broader factory modernization. As labor pressures intensify globally, automation of fabric inspection becomes a structural necessity rather than a discretionary investment.

Market Restraints

High Capital Intensity and SME Affordability Gaps

Despite favorable economies of scale, many small and mid-sized textile companies still view the upfront cost of fabric inspection machines, especially automatic systems, as prohibitive relative to margins. SME capital budgets prioritize looms, dyeing, and finishing lines, leaving limited room for quality equipment unless driven by buyer requirements. Financing constraints, currency risks, and a lack of long-term credit in developing markets further extend payback periods. Consequently, manual tables and basic semi-automatic setups remain widespread. This limits market penetration and creates structural challenges for vendors unless flexible commercial models such as leasing or equipment-as-a-service gain traction.

Integration Complexity, Training Requirements, and Regulatory Overheads

Deploying inspection machines into production is not a plug-and-play step; mills must align fabric path, line speed, data capture and quality workflows with new systems. Projects involving automatic inspection typically require software integration with ERP, labs and warehouse platforms, adding time and cost that some mills hesitate to absorb. Operators and quality staff need training to read defect maps, adjust thresholds and tune parameters for varying fabrics, delaying full benefit realization. Additionally, equipment supplied to the EU and North American markets must meet machinery and electrical safety standards, increasing engineering and documentation effort, raising costs and slowing adoption.

Market Opportunities

Technical Textiles, Automotive, and High-Value Applications

Technical textiles, such as automotive fabrics, filtration media, medical textiles, geotextiles, and protective garments, are expanding faster than conventional apparel and place higher demands on inspection accuracy and data traceability. Automotive interior materials, airbags, seat covers, and headliners must comply with OEM specifications and safety requirements, creating extremely low defect tolerance and a clear preference for automated inspection with digital records. In medical and hygiene applications, regulatory frameworks mandate near-100% inspection to address contamination or structural risks. These specialized uses justify premium inspection systems with tailored software, high-resolution imaging, and advanced defect classification, resulting in higher vendor margins. Growth of electric vehicles, advanced filtration, and high-performance textiles broadens the base of critical fabrics. Suppliers offering validated, application-specific solutions gain outsized commercial advantage.

Digitalization, Industry 4.0, and Service-Based Revenue Streams

Inspection machines are shifting from standalone equipment to connected intelligence nodes within digital manufacturing environments, transmitting real-time data to dashboards, cloud platforms, and predictive maintenance systems. As mills adopt Industry 4.0, they seek solutions that not only find defects but also provide insights into process deviation, machine stability, and upstream causes. This creates opportunities for vendors to offer software modules, analytics subscriptions, remote monitoring, and performance-based services, expanding revenue beyond hardware. When inspection data is linked to loom settings, dyeing parameters, and finishing conditions, mills can correlate defect trends with process variables and improve outcomes. Suppliers that deliver open, interoperable platforms or collaborate with MES providers gain strategic value. Increasing data depth enables benchmarking, digital twins, and AI-supported optimization, securing long-term customer relationships.

Segmentation Analysis

Machine Type Analysis

Roll-to-roll inspection machines hold 38% of the global market, making them the dominant category. Their suitability for continuous inspection aligns with workflows in weaving, knitting, and finishing plants. They maintain reliable defect detection even at high speeds, supporting a wide range of substrates from apparel to industrial textiles. Compatibility with downstream cutting and packing minimizes fabric handling and reduces damage. Continuous vendor improvements in ergonomics, tension control, and visualization enhance reliability. As plants integrate inspection across multiple stages, roll-to-roll units remain central to quality architectures.

Roll-to-roll systems remain among the fastest-growing solutions as mills upgrade to automated, data-enabled platforms that reduce inspection bottlenecks. Woven inspection machines, growing at 5.3% CAGR, benefit from the rising use of structured woven fabrics across apparel, home textiles, and technical applications. Increasing quality expectations for woven articles, including airbags and filters, drive the adoption of specialized woven inspection systems, especially in the Asia-Pacific region.

Technology Type Analysis

Semi-automatic inspection machines hold about 39% market share, making them today’s leading technology category. They combine motorized fabric movement and basic imaging or lighting support with manual decision-making from trained inspectors, delivering a balanced midpoint between simple manual tables and high-cost fully automatic platforms. For many mills, these systems meaningfully improve consistency, ergonomics, and productivity while maintaining feasible capital investments. Their widespread installed base is strong in small and mid-sized facilities handling varied styles and shorter runs. Yet, as digital integration and traceability expectations rise, their leadership may gradually yield to fully automatic systems.

Automatic inspection machines are the fastest-growing segment, with a 6.3% CAGR, using high-speed imaging and AI to reliably detect defects at continuous line speeds. Their appeal rises with labor savings, traceability, and compliance in regulated sectors. Adoption accelerates across Asia-Pacific as exporters meet global buyer needs. Paired with software, analytics, and remote support, automatic systems steadily capture additional market share.

End-Use Industry Analysis

The Textiles and Apparel segment accounts for about 48% of global demand, reflecting the scale of fashion-oriented fabric production and the importance of consistent quality in brand-focused markets. Garment manufacturers depend on reliable inspection to control cutting-room waste, prevent sewing disruptions, and reduce final rejections. Early defect identification enables mills to segregate and reprocess faulty fabric before costly downstream losses occur. As fashion cycles shorten and delivery expectations tighten, digital inspection supports reliability and brand protection. Increasingly, investments in automated inspection are viewed as essential to competitiveness in both fast-fashion and premium markets.

The Automotive segment is the fastest-growing, with a 5.9% CAGR, driven by increased use of textiles in interiors, safety systems, and insulation. OEM standards demand documented inspection, pushing suppliers toward advanced automated systems. EV growth expands textile applications, including acoustics, thermal management, and composites. These specialized materials require precise inspection, driving higher adoption intensity versus conventional apparel.

Regional Market Insights

North America

North America exhibits a mature yet steadily growing market, projected to expand at about 5.0% CAGR over the forecast period, underpinned by strong activity in technical textiles, automotive, aerospace, and medical applications. The United States leads regional demand, supported by clusters of technical textile manufacturers and automotive suppliers that require high-specification inspection capabilities for safety-critical and performance fabrics. Regulatory requirements from agencies such as OSHA and the FDA, along with strict OEM audit frameworks, reinforce disciplined quality processes and drive adoption of automated inspection where manual methods are no longer adequate.

The innovation ecosystem in North America, which includes machine vision suppliers, automation integrators, and software companies, encourages the rapid incorporation of cutting-edge technologies into inspection platforms. Many regional users favor systems with strong connectivity and analytics features that integrate with existing plant digitalization initiatives. Canada and Mexico contribute additional demand, with Mexico’s export-oriented automotive and apparel sectors representing an important growth pocket as companies upgrade older facilities to meet global customer expectations. Overall, the region is characterized by higher average selling prices, greater emphasis on technology sophistication, and growing appetite for service and analytics offerings.

Europe

Europe holds about 25% of the global Fabric Inspection Machine Market. It is projected to grow at a 4.5% CAGR, reflecting a combination of market maturity and targeted investments in high-value, specialized textile production. Germany plays a central role as both a major producer of technical textiles and a key supplier of advanced textile machinery, anchoring high adoption rates of inspection equipment in demanding applications such as automotive, filtration, protective clothing, and industrial fabrics. The United Kingdom, France, and Spain also maintain notable shares, with a mix of fashion, home textiles, and technical segments that collectively sustain stable demand for inspection technology.

The EU regulatory framework, covering product safety, chemicals (REACH), occupational safety, and emerging environmental requirements, encourages systematic quality control and documentation, thereby indirectly supporting investment in inspections. European mills are also at the forefront of sustainability and circular economy initiatives, which heighten the importance of consistent quality and traceability across recycled and bio-based textile streams. As digital product passports and extended producer responsibility schemes evolve, inspection data may increasingly feed into compliance reporting, enhancing the strategic value of inspection systems. Competitive dynamics in Europe favor suppliers that can combine advanced hardware with robust software, integration, and after-sales support tailored to complex, multi-plant operations.

Asia-Pacific

Asia-Pacific is the largest and fastest-growing regional market, accounting for around 37% of global share and expanding at approximately 6.6% CAGR through 2033. The region’s dominance stems from its central role in worldwide textile and apparel manufacturing, with China, India, Bangladesh, Vietnam, and other ASEAN economies collectively accounting for well over half of global fabric output. China remains the largest single producer and consumer of fabric inspection machines in the region, driven by its expansive textile base and increasing shift toward higher-value and technical textile production.

India, Bangladesh, and Vietnam are key growth hotspots, attracting new investment in weaving, processing, and garment manufacturing facilities that must align with international buyer standards. These markets historically relied on manual or semi-automatic inspection but are now progressively upgrading to roll-to-roll and automatic systems to manage rising volumes and stricter quality expectations. As governments in the region support modernization through technology upgradation schemes and industrial policy, fabric inspection equipment is often bundled into larger automation projects encompassing spinning, weaving, dyeing, and finishing. The region also hosts a growing number of local and regional equipment manufacturers, which intensifies competition and drives cost-effective solutions tailored to local operating conditions.

Competitive Landscape

Market Structure

The Fabric Inspection Machine Market shows a moderately consolidated structure at the top, with key players (multinational and regional) together accounting for around 55-60% of global revenues, and a long tail of smaller local manufacturers serving niche or price-sensitive segments. Market leaders tend to provide broad product portfolios covering roll-to-roll, flatbed, and specialized inspection systems, often supplemented by proprietary software platforms and strong service networks. Mid-tier and emerging players focus on specific geographies (e.g., Asia-Pacific) or application domains (e.g., technical textiles) where they can differentiate on cost, customization, or responsiveness.

Strategic Developments

- In October 2024, Picanol unveiled its brand-new Supermax rapier weaving machine at ITMA ASIA + CITME 2024 in Shanghai, featuring integrated inspection capabilities and digital connectivity through the PicConnect platform. The machine targets Asian markets with advanced features including guided grippers, digital shedding, and AI-powered quality monitoring systems designed for precision fabric production.

- In April 2024, STEMMER IMAGING acquired 100% ownership of Phase 1 Technology Corp., a New York-based machine vision distributor, to establish direct North American market presence. The acquisition strengthened STEMMER IMAGING's vision technology portfolio, distributing cameras, sensors, lenses, and industrial lighting to textile and industrial automation sectors across North America.

- In January 2025, Siemens partnered with Spinnova to revolutionize sustainable fiber production using Siemens Xcelerator digital technologies, including digital twins, automation, and Opcenter software. The collaboration at Woodspin factory in Finland demonstrates integration of advanced digital inspection and process control with sustainable textile manufacturing, enabling faster production ramp-up and consistent quality assurance.

Business Strategies

Leading companies emphasize technology differentiation, integrated digital offerings, and geographic expansion over pure price competition. Core strategic themes include sustained R&D in AI and machine vision, development of modular product families that can scale with customer needs, and extension into value-added services such as analytics, remote monitoring, and performance optimization consulting. At the same time, vendors increasingly experiment with flexible commercial models, leasing, subscription-based software, and performance-linked service contracts, to reduce adoption barriers and lock in long-term relationships. Emerging business models centered on equipment-as-a-service and data-driven quality optimization are expected to gain traction, especially among large multinationals and advanced technical textile producers.

Companies Covered in Fabric Inspection Machine Market

- Saurer Group

- Picanol Group

- Cognex Corporation

- STEMMER IMAGING AG

- Siemens AG

- ABB Ltd.

- Erhardt+Leimer Group

- BST GmbH (BST eltromat)

- La Meccanica SpA

- Monforts Textilmaschinen GmbH & Co. KG

- Zhejiang Licheng Group

- Yuyao Textile Machinery

- Embee Corporation

- Menzel Maschinenbau

Frequently Asked Questions

The global Fabric Inspection Machine Market is valued at approximately US$195.8 Million in 2026 and is projected to reach around US$281.5 Million by 2033.

The market is driven primarily by expanding textile production, tightening international quality and regulatory standards, rapid advances in AI-based machine vision technologies, and labor cost pressures that collectively push mills toward automated, data-enabled inspection solutions.

Between 2026 and 2033, the Fabric Inspection Machine Market is expected to grow at a CAGR of about 5.3%.

Key opportunities include modernization and capacity expansion in emerging textile hubs, rapid growth of technical and automotive textiles requiring stringent inspection, and the development of connected, Industry 4.0-compatible platforms that enable recurring software, analytics, and service revenues for equipment suppliers.

The market is shaped by a combination of global machinery and vision technology leaders, such as Saurer, Picanol, Cognex, STEMMER IMAGING, Siemens, ABB, Erhardt+Leimer, and regional textile machinery manufacturers in Europe and Asia, that provide fabric inspection hardware, integrated software, and automation solutions to mills worldwide.