- Executive Summary

- Global Medical Plastic Market Snapshot 2026 and 2033

- Market Opportunity Assessment, 2026-2033, US$ Bn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Value Chain Analysis

- Macro-Economic Factors

- Global GDP Outlook

- Europe Medical Industry Overview

- Europe Medical Products Market Growth Outlook

- Forecast Factors - Relevance and Impact

- COVID-19 Impact Assessment

- PESTLE Analysis

- Porter's Five Forces Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Technology Landscape

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Trends

- Price Trend Analysis, 2020 - 2033

- Region-wise Price Analysis

- Price by Segments

- Price Impact Factors

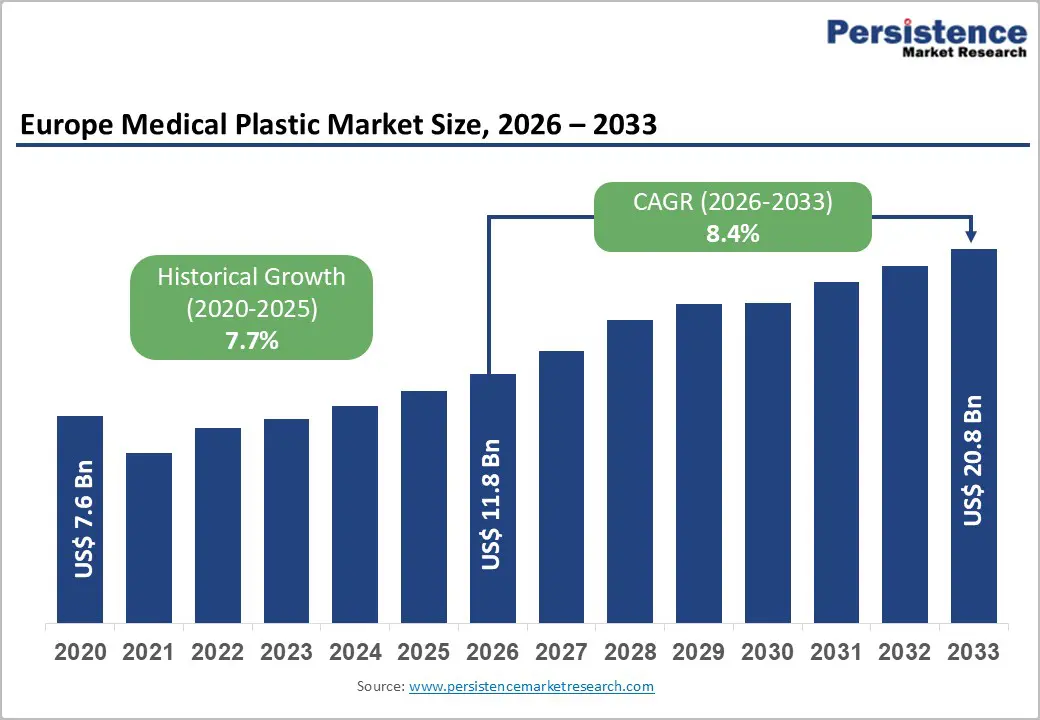

- Europe Medical Plastic Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Europe Medical Plastic Market Outlook: Product Type

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis by Product Type, 2020-2025

- Current Market Size (US$ Bn) and Volume (Tons) Forecast, by Product Type, 2026-2033

- Polycarbonate

- Polyamide

- Polyurethane

- Polysulfone

- Polypropylene

- Others

- Market Attractiveness Analysis: Product Type

- Global Medical Plastic Market Outlook: Application

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis by Application, 2020-2025

- Current Market Size (US$ Bn) and Volume (Tons) Forecast, by Application, 2026-2033

- Catheters

- Venous Cannula

- Membranes

- Venous Reservoir

- Capillaries

- Others

- Market Attractiveness Analysis: Application

- Global Medical Plastic Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis by Region, 2020-2025

- Current Market Size (US$ Bn) and Volume (Tons) Forecast, by Region, 2026-2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Market Attractiveness Analysis: Region

- Germany Medical Plastic Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Germany Market Size (US$ Bn) and Volume (Tons) Forecast, by Product Type, 2026-2033

- Polycarbonate

- Polyamide

- Polyurethane

- Polysulfone

- Polypropylene

- Others

- Germany Market Size (US$ Bn) and Volume (Tons) Forecast, by Application, 2026-2033

- Catheters

- Venous Cannula

- Membranes

- Venous Reservoir

- Capillaries

- Others

- Italy Medical Plastic Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Italy Market Size (US$ Bn) and Volume (Tons) Forecast, by Product Type, 2026-2033

- Polycarbonate

- Polyamide

- Polyurethane

- Polysulfone

- Polypropylene

- Others

- Italy Market Size (US$ Bn) and Volume (Tons) Forecast, by Application, 2026-2033

- Catheters

- Venous Cannula

- Membranes

- Venous Reservoir

- Capillaries

- Others

- France Medical Plastic Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- France Market Size (US$ Bn) and Volume (Tons) Forecast, by Product Type, 2026-2033

- Polycarbonate

- Polyamide

- Polyurethane

- Polysulfone

- Polypropylene

- Others

- France Market Size (US$ Bn) and Volume (Tons) Forecast, by Application, 2026-2033

- Catheters

- Venous Cannula

- Membranes

- Venous Reservoir

- Capillaries

- Others

- France Market Size (US$ Bn) and Volume (Tons) Forecast, by , 2026-2033

- U.K. Medical Plastic Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- U.K. Market Size (US$ Bn) and Volume (Tons) Forecast, by Product Type, 2026-2033

- Polycarbonate

- Polyamide

- Polyurethane

- Polysulfone

- Polypropylene

- Others

- U.K. Market Size (US$ Bn) and Volume (Tons) Forecast, by Application, 2026-2033

- Catheters

- Venous Cannula

- Membranes

- Venous Reservoir

- Capillaries

- Others

- Spain Medical Plastic Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Spain Market Size (US$ Bn) and Volume (Tons) Forecast, by Product Type, 2026-2033

- Polycarbonate

- Polyamide

- Polyurethane

- Polysulfone

- Polypropylene

- Others

- Spain Market Size (US$ Bn) and Volume (Tons) Forecast, by Application, 2026-2033

- Catheters

- Venous Cannula

- Membranes

- Venous Reservoir

- Capillaries

- Others

- Russia Medical Plastic Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Russia Market Size (US$ Bn) and Volume (Tons) Forecast, by Product Type, 2026-2033

- Polycarbonate

- Polyamide

- Polyurethane

- Polysulfone

- Polypropylene

- Others

- Russia Market Size (US$ Bn) and Volume (Tons) Forecast, by Application, 2026-2033

- Catheters

- Venous Cannula

- Membranes

- Venous Reservoir

- Capillaries

- Others

- Rest of Europe Medical Plastic Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Rest of Europe Market Size (US$ Bn) and Volume (Tons) Forecast, by Product Type, 2026-2033

- Polycarbonate

- Polyamide

- Polyurethane

- Polysulfone

- Polypropylene

- Others

- Russia Market Size (US$ Bn) and Volume (Tons) Forecast, by Application, 2026-2033

- Catheters

- Venous Cannula

- Membranes

- Venous Reservoir

- Capillaries

- Others

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- BASF SE

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- Evonik Industries AG

- Celanese Corporation

- Solvay S.A

- Covestro AG

- DuPont de Nemours

- DSM N.V.

- LyondellBasell Industries Holdings B.V

- SABIC

- The Lubrizol Corporation

- BASF SE

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Plastics, Polymers & Resins

- Europe Medical Plastic Market

Europe Medical Plastic Market Size, Share, and Growth Forecast 2026 - 2033

Europe Medical Plastic Market by Product Type (Polycarbonate, PVC, Polyamide, Polyurethane, Polysulfone, Polypropylene, and Others), Application (Catheters, Tubing, Venous Cannula, Membranes, Venous Reservoir, Capillaries, and Others), and Regional Analysis for 2026 to 2033

Key Industry Highlights:

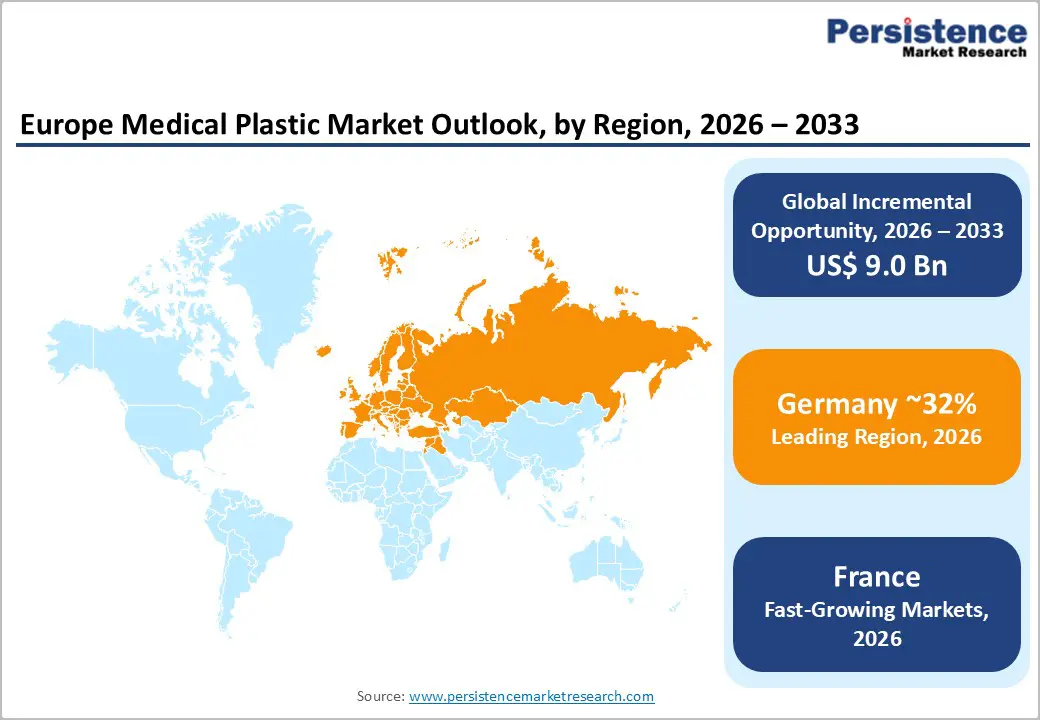

- Leading Country: Germany leads the European Medical Plastic Market with the continent's largest medical device manufacturing sector generating over €35 billion annually, anchored by polymer innovators including BASF SE, Covestro AG, and Evonik Industries AG, supported by stringent BfArM oversight and strong hospital procurement of premium biocompatible polymer components.

- Fastest Growing Country: France emerges as the fastest-growing major European market, driven by the €19 billion Ségur de la Santé modernization program, expanding dialysis patient population exceeding 46,000 active patients, and a growing medical technology cluster.

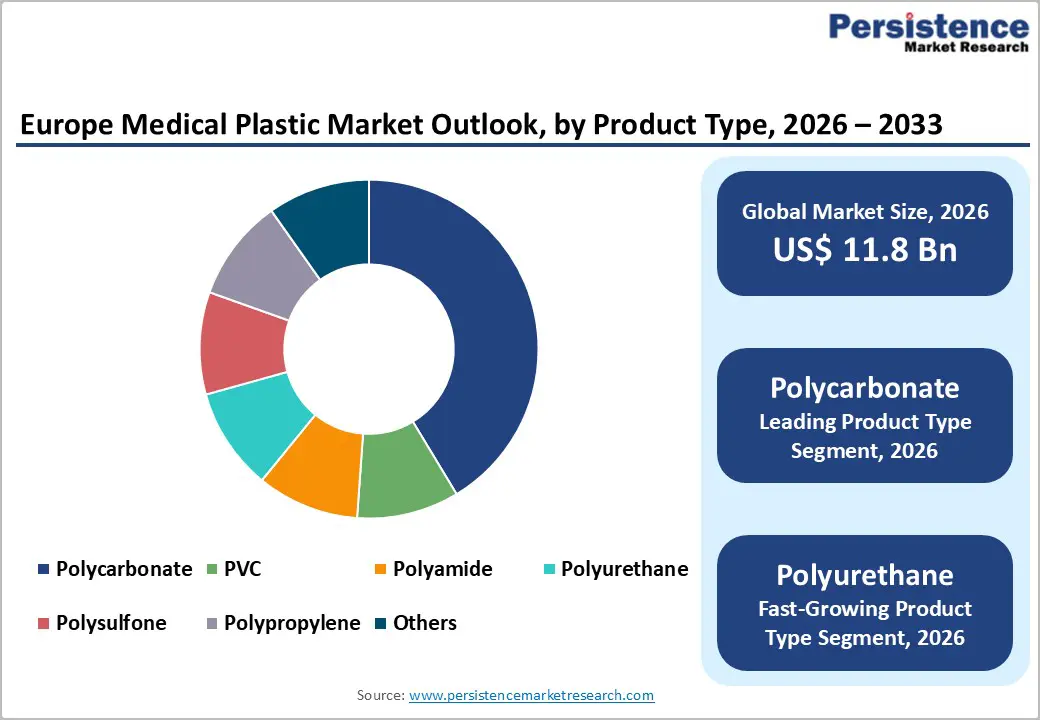

- Dominant Product Type: Polycarbonate dominates the product type segment with approximately 28% market share, driven by its optical clarity, sterilization compatibility with both gamma irradiation and ethylene oxide, and critical role in cardiac surgery blood management devices.

- Fastest Growing Application: Catheters represent the fastest-growing and dominant application segment, capturing approximately 32% share, fueled by over 1.8 million annual cardiac catheterization procedures across Europe.

- Key Opportunity: The key opportunity lies in bioresorbable and bio-based medical polymers for implantable and drug-delivery applications, where EU Green Deal sustainability mandates, favorable EMA regulatory guidance development, and clinical acceptance of PLA and PGA-based devices.

| Key Insights | Details |

|---|---|

| Europe Medical Plastic Market Size (2026E) | US$ 11.8 Bn |

| Market Value Forecast (2033F) | US$ 20.8 Bn |

| Projected Growth CAGR (2026 - 2033) | 8.4% |

| Historical Market Growth (2020 - 2025) | 7.7% |

Market Dynamics

Drivers - Surging Demand for Single-Use Medical Devices and Infection Control Protocols

The global emphasis on preventing healthcare-associated infections (HAIs) has fundamentally accelerated adoption of single-use medical plastic components across European hospitals and clinics. According to the European Centre for Disease Prevention and Control (ECDC), approximately 3.5 million patients acquire a healthcare-associated infection in the European Union annually, driving hospital procurement policies overwhelmingly toward disposable plastic devices that eliminate cross-contamination risks. The World Health Organization (WHO) endorses single-use device policies as a cornerstone of patient safety frameworks, prompting regulatory alignment across EU member states.

Medical-grade PVC, polypropylene, and polyurethane are extensively deployed in single-use catheters, IV tubing, and blood reservoir systems due to their combination of flexibility, chemical resistance, and validated sterilization compatibility. European Medical Device Regulation (MDR) 2017/745, fully enforced from May 2021, imposes rigorous biocompatibility and traceability requirements that effectively favor established high-quality polymer suppliers, reinforcing market consolidation among compliant material producers and device manufacturers.

Aging European Population and Expansion of Chronic Disease Management Programs

Europe's demographic shift is a structural long-term driver for medical plastic consumption, as older populations require more frequent and prolonged medical interventions involving polymer-based devices. Eurostat projects that persons aged 65 and over will account for approximately 29.4% of the EU's total population by 2050, compared to 21.3% in 2022, representing a substantial increase in patients requiring cardiovascular, dialysis, and respiratory care products.

The European Heart Network estimates that over 60 million Europeans currently live with cardiovascular disease, driving continuous demand for polysulfone membranes in dialysis systems, polycarbonate blood oxygenators, and polyurethane cardiac catheters. Dialysis treatment alone, according to the European Renal Association (ERA), involves over 350,000 patients across Europe, each undergoing 3 sessions per week, creating predictable recurring demand for medical-grade plastic components throughout the treatment pathway.

Restraints - Regulatory Compliance Complexity Under EU MDR and Biocompatibility Standards

The implementation of EU Medical Device Regulation (MDR) 2017/745 significantly increased compliance burdens for medical plastic manufacturers and device makers. Comprehensive biocompatibility testing under ISO 10993 standards, extended technical documentation requirements, and mandatory clinical evidence submissions have extended product approval timelines by 12 to 18 months on average, according to the European Commission's own implementation assessments.

Smaller specialty polymer producers face disproportionate financial burdens from these requirements, with compliance costs estimated to range from €50,000 to €500,000 per product variant depending on device classification, effectively creating barriers that reduce competitive diversity and slow innovation deployment across the medical plastics value chain.

Environmental and Regulatory Pressure to Reduce Single-Use Plastics

The European Union's aggressive sustainability agenda presents a structural restraint for single-use medical plastic consumption. The EU Single-Use Plastics Directive (2019/904) targets a broad range of plastic products, and while medical devices are currently exempted, regulatory expansion discussions by the European Commission continue to create uncertainty for procurement and investment decisions.

Approximately 7% of European healthcare plastic waste consists of materials under active policy review, creating pressure on hospital procurement teams to seek alternatives. The European Healthcare Waste Management Association notes that hospitals generate over 600,000 tonnes of plastic waste annually in the EU, prompting sustainability-linked procurement criteria that complicate demand forecasting for conventional single-use medical plastics.

Opportunity - Advancement of High-Performance Bioresorbable and Bio-Based Medical Polymers

The development and commercialization of bioresorbable and bio-based medical polymers represent a transformative opportunity for companies operating in the medical plastics space. Bioresorbable polymers such as polylactic acid (PLA), polyglycolic acid (PGA), and copolymers thereof are gaining regulatory traction for implantable devices, sutures, drug-delivery scaffolds, and cardiovascular stents, eliminating secondary surgical removal procedures. The European Medicines Agency (EMA) and national competent authorities are actively developing clearer guidance pathways for combination products incorporating bioresorbable components.

Research published in peer-reviewed journals such as Biomaterials documents that PLA-based devices now achieve mechanical performance within 15% of conventional polymers for certain load-bearing applications. Companies such as BASF SE and DSM N.V. have invested in dedicated bio-based polymer R&D platforms targeting medical applications. As healthcare providers implement lifecycle sustainability commitments and EU Green Deal objectives permeate procurement criteria, bioresorbable solutions offer premium positioning with growing clinical acceptance.

Expansion of Extracorporeal Membrane Oxygenation (ECMO) and Advanced Blood Management Technologies

The significant expansion of extracorporeal membrane oxygenation (ECMO) procedures across European intensive care units following the COVID-19 pandemic has established a durable new demand vertical for high-performance medical plastics. Polysulfone and polymethylpentene hollow-fiber membranes, precision polycarbonate pump housings, and polyurethane coated cannulae are essential components of ECMO circuits. The Extracorporeal Life Support Organization (ELSO) registry data indicates a 54% increase in ECMO center registrations between 2019 and 2023, directly corresponding to increased device procurement.

Polysulfone membrane technology in particular enables gas transfer rates exceeding 250 mL/min per membrane module, meeting critical oxygenation requirements. Simultaneously, venous reservoir and capillary oxygenator segments are expanding with next-generation heparin-coated surfaces that require specialized polyurethane and polycarbonate substrates, creating technical differentiation opportunities for polymer suppliers capable of delivering medical-grade consistency at scale.

Category-wise Analysis

Product Type Insights

Polycarbonate dominates the product type segment, accounting for approximately 28% of the European medical plastics market, reflecting its unique combination of optical clarity, exceptional impact resistance, dimensional stability, and broad sterilization compatibility. These properties make polycarbonate indispensable for applications requiring visual inspection of fluid pathways, such as blood oxygenators, arterial filters, venous reservoir housings, and hard-shell perfusion components used extensively in cardiac surgery. According to PlasticsEurope, polycarbonate remains among the top three engineering thermoplastics by volume in European medical device manufacturing.

Bayer MaterialScience (now Covestro AG) pioneered medical-grade polycarbonate compounds under the Makrolon product family, establishing benchmarks for extractables and leachables compliance under ISO 10993-12. Polycarbonate components can withstand gamma irradiation up to 35 kGy and ethylene oxide sterilization without significant yellowing or embrittlement, critical requirements for terminal sterilization of complex multi-use and single-use devices across European healthcare procurement specifications.

Application Insights

Catheters represent the leading application segment, capturing approximately 32% of the market, driven by their ubiquitous deployment across cardiovascular, urological, neurological, and gastrointestinal procedures throughout European hospitals. Catheters serve as the most voluminous single-use medical plastic application category, with the European Society of Cardiology (ESC) reporting over 1.8 million cardiac catheterization procedures performed annually across Europe. Medical-grade polyurethane and PVC dominate catheter shaft construction, with nylon (polyamide) braiding and polypropylene hubs providing structural reinforcement and Luer-lock compatibility.

The transition to hydrophilic-coated polyurethane catheters, which reduce friction by 50 to 90% compared to uncoated variants per clinical studies published in the Journal of Vascular and Interventional Radiology, is driving material premiumization in this segment. Regulatory compliance with ISO 10555 for intravascular catheters and ISO 10993 biocompatibility requirements ensures that established high-quality polymer suppliers maintain strong positions within this critical application.

Country Insights

Germany Medical Plastic Market Trends

Germany maintains market leadership within the European Medical Plastic Market, supported by its position as Europe's largest medical device manufacturing economy and home to globally influential healthcare organizations. According to Spectaris (the German Industry Association for Optical, Medical, and Mechatronic Technologies), Germany's medical device industry generates over €35 billion in annual revenue, with plastics constituting approximately 40% of material inputs. German device manufacturers operating under DIN EN ISO standards and the rigorous oversight of the Bundesinstitut für Arzneimittel und Medizinprodukte (BfArM) drive consistent demand for premium medical-grade polymer solutions meeting stringent biocompatibility criteria.

Major chemical companies headquartered in Germany, including BASF SE, Covestro AG, and Evonik Industries AG, maintain integrated medical polymer R&D and production platforms, enabling close collaboration with device manufacturers on application-specific formulations. The Fraunhofer Society's biomedical engineering institutes actively support polymer innovation for medical applications. German procurement practices emphasize total cost of ownership over initial price, favoring high-performance materials with documented clinical performance data, supporting premium polymer suppliers. The country's robust private healthcare infrastructure and comprehensive statutory health insurance covering over 90% of the population (per Statistisches Bundesamt) ensure sustained demand for catheter, tubing, and membrane products manufactured from advanced medical plastics.

India Medical Plastic Market Trends

Italy represents a significant and technically sophisticated segment of the European Medical Plastic Market, anchored by its well-established extracorporeal circuit and blood management technology sector centered in the Mirandola biomedical district in Emilia-Romagna. This cluster, recognized by the Italian Ministry of Economic Development as one of Europe's most concentrated medical device manufacturing hubs, produces a substantial proportion of global oxygenators, venous reservoirs, and blood tubing sets, all critically dependent on medical-grade polycarbonate, polyurethane, and polysulfone inputs. The district generates approximately €1.5 billion in annual medical device exports according to Confindustria Dispositivi Medici, reinforcing Italy's structural importance to European medical plastic demand.

Regulatory alignment with EU MDR 2017/745 requirements has driven Italian manufacturers to intensify quality management investments, benefiting suppliers of traceable, specification-controlled polymer grades. SORIN Group (now LivaNova PLC) and other Italian cardiac surgery device companies have historically anchored local polycarbonate and polysulfone demand for cardiopulmonary bypass components. Italy's national health service (Servizio Sanitario Nazionale) covers dialysis treatment for over 50,000 patients, according to the Italian Society of Nephrology (SIN), generating substantial polysulfone membrane and blood line consumption. Growing Italian medical device exports to Middle Eastern and African markets are further stimulating domestic manufacturing volumes and polymer procurement.

France Medical Plastic Market Trends

France constitutes the third-largest European Medical Plastic Market by value, underpinned by its centralized public healthcare system (Sécurité Sociale), advanced pharmaceutical and medical device manufacturing sector, and strong government investment in hospital modernization programs. The French Ministry of Health's Ségur de la Santé program committed €19 billion to healthcare system modernization, including hospital infrastructure upgrades that directly stimulate procurement of medical-grade plastic devices. France's dialysis patient population-estimated at over 46,000 active patients by the Agence de la Biomédecine-maintains consistent demand for polysulfone membranes and polyurethane blood circuit components across public and private dialysis centers.

LETI (CEA-Leti) and INSERM research institutes support polymer science innovation in France, contributing to development of functionalized medical plastics for next-generation diagnostic and therapeutic devices. French manufacturer Biomérieux and device companies within the Paris-Saclay cluster are active consumers of specialty medical polymers for diagnostic cartridges and biosensor housings. European Medicines Agency (EMA)-supervised regulatory harmonization ensures French device certifications provide market access across all 27 EU member states, incentivizing manufacturers to adopt compliant medical polymer grades. France's growing medical tourism sector and aging population (over 21% aged 65+ per INSEE) further support sustained medical device and plastic component consumption growth.

Competitive Landscape

Europe medical plastic market exhibits moderate consolidation, with a limited number of large multinational specialty chemical and polymer companies accounting for the majority of high-performance medical-grade polymer supply, while a broader ecosystem of regional compounders and distributors serves lower-specification applications. Leading companies including BASF SE, Covestro AG, Evonik Industries AG, Solvay S.A., and DuPont de Nemours differentiate through proprietary formulations, regulatory support packages, documented extractables and leachables profiles, and dedicated medical-grade manufacturing facilities with pharmaceutical-equivalent quality systems.

Emerging business model trends include supply agreements tied to device platform lifecycles, co-development partnerships for application-specific polymer grades, and sustainability-linked product lines featuring bio-based or recyclable polymer options designed to align with European healthcare providers' ESG commitments.

Key Developments:

- In January 2025, Evonik Industries AG introduced its next-generation VESTAMID polyamide grades specifically formulated for multilayer medical tubing, offering enhanced kink resistance and biocompatibility documentation compliant with EU MDR 2017/745 requirements for catheter shaft and guidewire coating applications.

- In September 2024, BASF SE announced a strategic investment in its Ultrason polysulfone and polyethersulfone production capacity in Ludwigshafen, expanding availability of medical-grade grades certified under ISO 10993 for membrane and filtration device applications addressing growing European dialysis and blood purification device demand.

- In April 2024, Covestro AG launched an expanded portfolio of Makrolon medical-grade polycarbonates with enhanced gamma radiation stability, targeting blood oxygenator and dialysis device manufacturers requiring improved clarity and mechanical consistency after terminal sterilization processes across European and global markets.

Companies Covered in Europe Medical Plastic Market

- BASF SE

- Evonik Industries AG

- Celanese Corporation

- Solvay S.A

- Covestro AG

- DuPont de Nemours

- DSM N.V.

- LyondellBasell Industries Holdings B.V

- SABIC

- The Lubrizol Corporation

- Arkema S.A.

- Röchling Medical

- Mitsubishi Chemical Group

- Eastman Chemical Company

- Teknor Apex Company

Frequently Asked Questions

The Europe Medical Plastic Market is projected to reach US$ 20.8 Bn by 2033, growing from US$ 11.8 Bn in 2025 at a CAGR of 8.4% during the forecast period. This growth reflects sustained demand from aging populations requiring cardiovascular, dialysis, and minimally invasive surgical devices that rely on medical-grade polymer components across European healthcare systems.

Demand is primarily driven by stringent infection control protocols mandating single-use plastic medical devices, with the ECDC estimating 3.5 million HAI cases annually in the EU. Simultaneously, Eurostat projections of 29.4% of EU population aged 65+ by 2050 and over 350,000 European dialysis patients create structural, recurring demand for high-performance polymer components in catheters, membranes, and extracorporeal circuits.

Polycarbonate leads the product type segment with approximately 28% market share, driven by its unique combination of optical clarity, impact resistance, and compatibility with both gamma irradiation and ethylene oxide sterilization.

Germany maintains market leadership with Europe's largest medical device manufacturing sector, generating over €35 billion annually, per Spectaris.

The commercialization of bioresorbable and bio-based medical polymers presents the most significant opportunity, as sustainability mandates under the EU Green Deal, improving the mechanical performance of PLA and PGA-based materials to within 15% of conventional polymers.

Key market players include BASF SE, Covestro AG, Evonik Industries AG, Solvay S.A., and DuPont de Nemours, which collectively command significant market influence through comprehensive medical-grade polymer portfolios, dedicated regulatory support services, and application-specific R&D programs.