- Nutraceuticals & Functional Foods

- Dietary Supplements Market

Dietary Supplements Market Size, Share, and Growth Forecast 2026 - 2033

Dietary Supplements Market by Supplement Types (Botanicals, Vitamins, Amino Acids, Enzymes, Probiotics, Others), by Form (Tablets, Capsules, Liquid, Gummies, Powder), by Function, by Sales Channel, and Regional Analysis, 2026 - 2033

Dietary Supplements Market Size and Trend Analysis

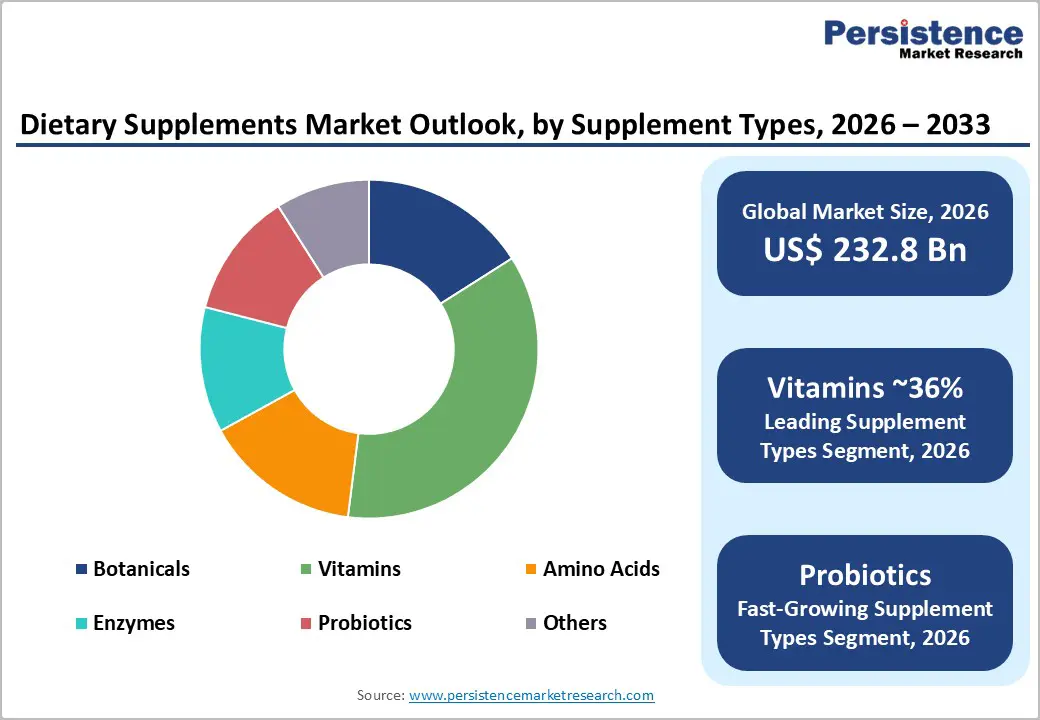

The global dietary supplements market size is expected to be valued at US$ 232.8 billion in 2026 and projected to reach US$ 409.5 billion by 2033, growing at a CAGR of 8.4% between 2026 and 2033.

The market is experiencing strong growth, driven by rising health consciousness, aging populations, and increasing demand for preventive healthcare. Consumers are shifting toward natural, plant-based, and clean-label supplements, fuelling innovations in herbal extracts, probiotics, and functional ingredients. The e-commerce boom has transformed distribution, making supplements more accessible, while personalised nutrition trends drive demand for DNA-based and condition-specific formulations.

Key Industry Highlights:

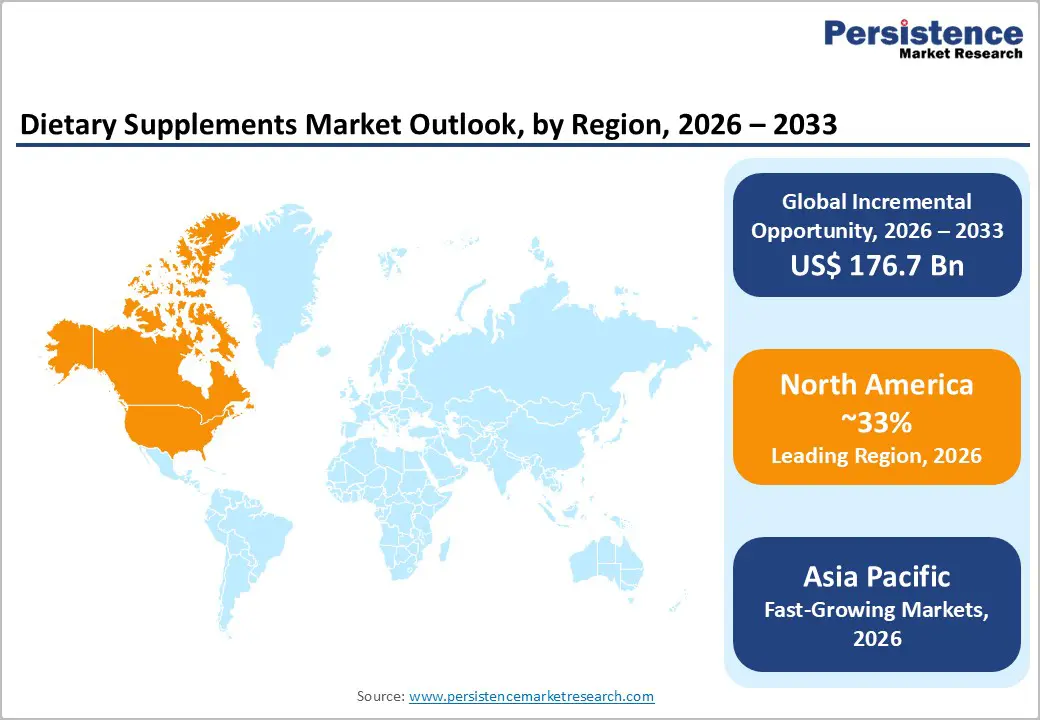

- North America will remain the leading dietary supplements market, supported by high incomes, strong supplement culture, established regulations, and diverse vitamin and nutrition brands.

- Asia Pacific is the fastest growing region, driven by expanding middle class populations, positive attitudes toward functional foods, and rapid growth of e-commerce platforms.

- Vitamins dominate supplement types, accounting for about 36% global revenues, as multivitamins and single nutrient products address widespread micronutrient deficiencies worldwide.

- Probiotics and gut health supplements represent one of the fastest growing segments, supported by microbiome research, digestive health awareness, and increased investments in product development.

- Key opportunity lies in combining clinically proven ingredients with digital personalized nutrition platforms using diagnostics, data analytics, and subscription models for tailored supplement solutions.

| Key Insights | Details |

|---|---|

|

Dietary Supplements Market Size (2026E) |

US$ 232.8 billion |

|

Market Value Forecast (2033F) |

US$ 409.5 billion |

|

Projected Growth CAGR (2026–2033) |

8.4% |

|

Historical Market Growth (2020–2025) |

6.8% |

Market Dynamics

Drivers - Flexible, convenient formats to suit individual lifestyles

Modern consumers demand dietary supplements that fit seamlessly into their fast-paced, mobile lifestyles, driving innovation in delivery formats beyond traditional pills and capsules. People increasingly prefer to on-the-go, hassle-free options like gummies, effervescent powders, dissolvable strips, liquid shots, and even functional foods to integrate supplementation effortlessly into their daily routines. A unique example is Healthycell’s microgel technology, which replaces bulky pills with gel-based nutrient packs that can be consumed straight from a sachet or mixed into beverages. Similarly, Cachet Pharma's melt-in-the-mouth vitamin strips provide a rapid-absorption alternative for those who dislike swallowing pills. Meanwhile, nootropic-infused coffee creamers and protein bars enriched with adaptogens are redefining how consumers supplement their diets.

The demand for customised, portable, and enjoyable supplement experiences is also fueling the rise of single-serving supplement pods and subscription-based daily packs, ensuring precise dosing without the complexity of multiple bottles. As personal health becomes increasingly integrated into everyday habits, brands offering flexible, lifestyle-friendly supplement formats will gain a competitive edge in the evolving market.

AI-Powered Personalized Nutrition Revolution

Artificial intelligence (AI) is reshaping the dietary supplements industry by enabling hyper-personalized nutrition solutions tailored to an individual’s unique physiology. Advanced algorithms analyze gut microbiome data, genetic predispositions, metabolic markers, and lifestyle habits to generate precise supplement recommendations. This shift moves away from the one-size-fits-all approach, optimizing nutrient intake based on real-time health insights. AI-driven models integrate wearable device tracking, continuous glucose monitoring (CGM), and epigenetic analysis to refine supplement plans dynamically.

A standout example is Bioniq, a company leveraging AI to create fully customized supplement regimens based on blood tests. Users receive periodic blood analysis, and their supplement formula is adjusted accordingly, ensuring optimal nutrient levels. Another pioneer, Care/of, utilizes AI-powered quizzes to tailor vitamin packs, considering dietary preferences, health goals, and lifestyle choices. These AI-driven subscription models are particularly popular among millennials and Gen Z, who prioritize convenience and data-backed wellness solutions.

Restraints - Regulatory Scrutiny, Quality Concerns, and Misinformation

The evolving regulatory landscape is significantly restricting innovation, market entry, and product marketing strategies in the dietary supplements industry. Governments and health agencies worldwide are implementing stricter compliance measures to curb misleading health claims, contamination risks, and the use of unapproved ingredients. In the United States, the FDA’s 2023 proposal to modernize the Dietary Supplement Health and Education Act (DSHEA) has introduced more stringent premarket review processes, forcing manufacturers to submit evidence of safety for new dietary ingredients (NDIs) before market launch. This move aims to eliminate harmful, untested formulations but is also delaying product approvals by months or even years, increasing compliance costs for supplement companies.

A notable recent U.S. example is the FDA’s crackdown on NMN (Nicotinamide Mononucleotide), a popular anti-aging supplement. In early 2023, the FDA revoked NMN’s classification as a dietary supplement, citing its prior investigation as a pharmaceutical drug. This decision forced major retailers like Amazon to remove NMN supplements from their platforms, disrupting the market and leaving supplement companies with unsellable stock. The case highlights how evolving regulations can abruptly disrupt supply chains and consumer access, impacting both established brands and new entrants. As regulatory scrutiny intensifies, dietary supplement firms must continuously adapt to shifting compliance demands, invest in rigorous clinical trials, and navigate uncertainty regarding ingredient approvals, making long-term business planning increasingly challenging.

Opportunities - High growth probiotics, microbiome focused and gut-health supplements

One of the most attractive opportunities lies in probiotics and broader microbiome-focused products, which are projected to outpace overall market growth. In Asia Pacific, where the vitamins category already holds the largest revenue share, prebiotics and probiotics are forecast to grow faster than the regional average through 2033, supported by consumer recognition of the link between gut health and immunity. Companies are investing in clinically documented strains, synbiotic formulations, and shelf-stable spore-based products that can be sold through mainstream retail and e-commerce without cold-chain constraints. Regulatory pathways in markets like China, where streamlined registration processes for specific probiotic strains have encouraged domestic fermentation investments, further stimulate innovation. Global brands and ingredient suppliers that can substantiate benefits for digestive comfort, immune support, and mental well-being are well placed to capture this high-growth pocket within the dietary supplements landscape.

Category-wise Analysis

Supplement Types Insights

Vitamins dominate the dietary supplements market due to their essential role in overall health, broad consumer appeal, and increasing awareness of preventive healthcare. Unlike other supplement types, vitamins cater to diverse demographics, including children, adults, and the elderly, making them a universal necessity. The rise in lifestyle-related disorders, such as cardiovascular diseases and weakened immunity, has driven consumers toward vitamin-based supplements, particularly vitamin C, D, and multivitamins.

Additionally, the aging population has fueled demand for vitamins that support bone health (vitamin D and calcium), cognitive function (B-complex), and skin health (vitamin E). The COVID-19 pandemic further accelerated the market as individuals sought immunity-boosting solutions, leading to a surge in sales of vitamins C and D. The convenience of various delivery formats, including gummies, tablets, soft gels, and powders, has also contributed to their widespread adoption.

Moreover, advancements in personalized nutrition and fortified foods have further strengthened the vitamin segment. Companies are leveraging scientific innovations to develop customized multivitamins targeting specific deficiencies, enhancing their market growth. With a shift toward proactive wellness and preventive care, the demand for vitamins continues to outpace other dietary supplement categories, solidifying their leadership in the market.

Form Analysis

Tablets dominate the dietary supplements market due to their affordability, stability, and ease of consumption. Among all supplement forms, tablets offer the highest ingredient density, allowing for precise dosage in a compact size. Their cost-effective production process makes them more affordable than liquid or gummy alternatives, ensuring widespread availability across different price segments. Additionally, tablets have a longer shelf life, making storage and bulk purchasing convenient.

Another key factor driving tablets' dominance is their versatility in formulation. They can be coated to improve taste, control release time, and enhance absorption. Sustained release and chewable tablets further expand their appeal, catering to individuals who may struggle with swallowing pills. Consumers also favor tablets due to their portability, requiring no refrigeration or special handling compared to liquid supplements.

Pharmaceutical advancements have improved tablet formulations, making them easier to digest and absorb. While other forms like gummies and powders have gained popularity, especially among younger consumers, tablets continue to lead in sales volume due to their efficiency and reliability.

Regional Insights

North America Dietary Supplements Market Trends and Insights

North America leads the dietary supplements market due to high consumer awareness, a well-established healthcare system, and a strong culture of preventive wellness. The region’s aging population, particularly in the U.S. and Canada, is a significant driver, with seniors increasingly turning to supplements for cognitive health, joint support, and immune enhancement. The growing preference for personalized nutrition, fuelled by advancements in genetic testing and AI-driven supplement recommendations, has further strengthened market dominance.

E-commerce and direct-to-consumer models are also propelling growth, with brands leveraging AI-driven marketing and subscription-based models to retain customers. Furthermore, the region’s high disposable income and premiumization trends encourage consumers to invest in high-quality, scientifically backed supplements. With continuous innovation and consumer-driven trends, North America remains at the forefront of the global dietary supplements market.

Asia Pacific Dietary Supplements Market Trends and Insights

Asia Pacific is the fastest-growing dietary supplement market region due to rising health consciousness, expanding middle-class populations, and increasing disposable income. Countries like China, India, and Japan are witnessing a surge in demand for vitamins, minerals, and herbal supplements driven by urbanization and changing dietary habits.

India is emerging as a key player in the Asia Pacific dietary supplements market due to its rapidly growing health-conscious population and increasing preference for preventive healthcare. The country’s large millennial and Gen Z population is fuelling demand for fitness, immunity-boosting, and herbal supplements.

Manufacturers are increasingly localizing product formulations to cater to regional preferences, such as lactose-free and plant-based supplements for lactose-intolerant populations. With rapid innovation, strategic partnerships, and growing awareness of personalized nutrition, Asia Pacific is set to dominate the global dietary supplements market in the coming years.

Competitive Landscape

The global dietary supplements market is fragmented and intensely competitive, comprising multinational consumer health companies, specialist nutraceutical firms, direct selling organisations, and a long tail of regional and online brands. Leading players such as Abbott Laboratories, Amway, DuPont, Royal DSM N.V., Glanbia Plc., Bayer AG, GlaxoSmithKline Plc, Herbalife International, BASF SE, GNC Holdings Inc., Now Health Group Inc., Nature’s Bounty Co., and Solaray Inc. compete on brand trust, ingredient science, product breadth, and distribution reach. Many of these companies operate integrated value chains from ingredient manufacturing to finished products and invest in clinical trials, quality certifications, and digital marketing. Emerging business models include subscription based personalized packs, influencer driven direct to consumer brands, and strategic partnerships between ingredient innovators and consumer facing companies.

Key Developments:

- In January 2025, Eurofins Healthcare Assurance launched an innovative Good Manufacturing Practice (GMP) certification program for dietary and food supplements. The initiative aimed to improve compliance, safety, and quality across global supply chains. It was designed to help manufacturers, brands, agents, and retailers navigate the complex US regulatory landscape in the rapidly growing health and wellness market.

- In September 2024, Bayer took a significant step in the emerging healthy-aging space by offering consumers new tools to support their healthy-aging journey through its Age Factor™ ecosystem. This initiative combined a scientifically formulated dietary supplement, a leading-edge wellness companion app, and a saliva-based biological age test by Chronomics.

Companies Covered in Dietary Supplements Market

- Abbott Laboratories

- Amway (Nutrilife)

- DuPont

- NBTY Inc.

- Royal DSM N.V.

- Glanbia Plc.

- Bayer AG

- GlaxoSmithKline Plc

- Herbal life International

- BASF SE

- GNC Holdings Inc.

- Now Health Group Inc.

- Nature's Bounty Co.

- Solaray Inc.

- Others

Frequently Asked Questions

The global dietary supplements market is expected to reach about US$ 232.8 billion in 2026.

Increasing attention on health, greater customization of, rising consumer awareness regarding the severity of digestive disorders and benefits of dietary supplements, and rising consumption of dietary supplements in emerging countries are aiding market expansion.

North America leads the dietary supplements market due to high consumer usage, strong purchasing power, developed retail channels, and well-established regulatory oversight.

Key opportunity lies in probiotics and microbiome-focused supplements combined with personalized nutrition platforms using diagnostics and data-driven recommendations for customized health solutions.

Major companies include Abbott Laboratories, Amway, DuPont, Royal DSM, Glanbia, Bayer, Herbalife, BASF, GNC Holdings, Nature’s Bounty, and Now Health Group.