ID: PMRREP9926| 180 Pages | 16 Dec 2024 | Format: PDF, Excel, PPT* | Chemicals and Materials

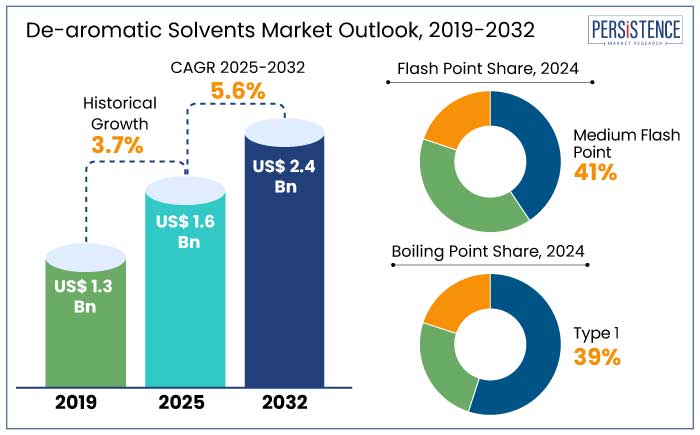

The global de-aromatic solvents market is to reach the size of US$ 1.6 Bn by 2025. It is anticipated to experience a CAGR of 5.6% during the assessment period to reach a value of US$ 2.4 Bn by 2032. By the end of the forecast period, bio-based solvents are predicted to account for 10% to 15% of the market share owing to the rising stringent environmental regulations and corporate sustainability goals.

Companies in the industry are focusing on renewable feedstocks like soy-based or plant-based derivatives. Advancements in recycling technologies are estimated to assist industries recover and reuse de-aromatic solvents, thereby decreasing costs and environmental impact. In-depth research in smart solvents with tunable properties are predicted to cater to niche applications in pharmaceuticals and electronics.

Key Highlights of the Industry

|

Market Attributes |

Key Insights |

|

De-aromatic Solvents Market Size (2025E) |

US$ 1.6 Bn |

|

Projected Market Value (2032F) |

US$ 2.4 Bn |

|

Global Market Growth Rate (CAGR 2025 to 2032) |

5.6% |

|

Historical Market Growth Rate (CAGR 2019 to 2023) |

3.7% |

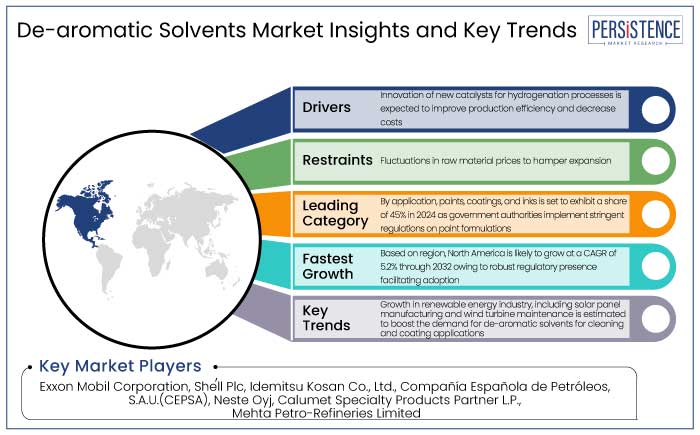

De-aromatic solvents market in North America is estimated to hold a share of 39% in 2024. Environmental Protection Agency (EPA) regulations in the U.S. have driven end use industries to adopt low-VOC solvents like de-aromatic solvents to comply with air quality standards. The Clean Air Act and Title III of the 1990 Clean Air Act Amendments aim to decrease VOCs in industrial processes, especially in paints, coatings, adhesives, and cleaning products.

Based on statistics provided by the EPA, VOC emissions from paints and coatings are responsible for 15% of total VOC emissions in the U.S. By switching to low-VIC solvents, industries can decrease their environmental footprint while complying with regulations.

The region is a front-runner in green chemistry and sustainable chemical practices, thereby promoting the use of eco-friendly solvents, including de-aromatic solvents in sectors like paints and costings. The California Air Resources Board (CARB) in California, enforces stringent VOC regulations in the country, thereby compelling manufacturers to switch to low-VOC and de-aromatic alternatives.

Companies in North America are focused on corporate social responsibility (CSR) initiatives and sustainability targets, resulting in high adoption of eco-friendly solvents, including de-aromatic solvents.

Medium flash points are estimated to hold a share of 41% in 2024. Flash points between 40°C to 60°C makes them safe compared to low-flash point solvents and more efficient in terms of performance compared to high flash point solvents. Solvents in medium flash point range are specifically suited for applications that require a balance between safe handling and effective solvency where fast evaporation and low toxicity are critical. Several countries, specially in North America and Europe have stringent regulations regarding solvents.

Medium flash point solvents traditionally comply better with workplace safety standards and environmental regulations. These flash point solvents are widely used across a variety of industries, thereby making them a versatile option.

Medium flash point solvents provide a cost-effective balance between performance and safety. Solvents with medium flash points are also easier to handle and store compared to these with low flash points as they require more stringent storage conditions and safety protocols.

Type 1 is estimated to emerge as the leading boiling point with a share of 39% in 2024. They are highly values for their rapid evaporation rates, that make them ideal for applications where fast drying is critical. They are often preferred owing to their robust solvency properties. They can effectively dissolve a range of resins, oils, and other components in formulations.

High solvency power of low boiling point is especially useful in formulations that require faster drying while maintaining the ability of solvents to effectively dissolve and mix ingredients. Type 1 solvents that are low in VOCs, are well suited for formulations that require to comply with these regulations while offering high performance.

Type 1 solvents with lower boiling points have lower flash points, decreasing the risk of ignition compared to high-boiling solvents. These properties make them safe to handle, store, and use in various industrial settings.

Paints, coatings, and inks are emerging as the leading application with a share of 45% in 2024. Government authorities across the globe are enforcing stringent environmental regulations to decrease volatile organic compound (VOC) emissions from paints, coatings, and inks, that are a prominent sources of air pollution.

De-aromatic solvents fit well in the rising demand for sustainable and safe products owing to their lower toxicity compared to traditional aromatic solvents. De-aromatic solvents provide superior solvency properties, thereby making them effective in dissolving a variety of resins, oils, and other components used in paints, coatings, and inks.

Formulations of paints and coatings demand solvents that can effectively dissolve raw materials while offering smooth application and consistency. De-aromatic solvents assist in achieving these requirements without compromising on quality or performance.

The shift toward greener formulations have given rise to waterborne coatings in the paints and coatings industry. These coatings are less harmful to the environment and are therefore more user-friendly compared to solvent-borne coatings. De-aromatic solvents are used in waterborne coatings as co-solvents or evaporation agents to assist in achieving the right balance between drying speed, application, and safety.

Potential growth in the global de-aromatic solvents industry is predicted to be driven by development of bio-based and renewable de-aromatic solvents. Improvements in hydrogenation technologies and energy-efficient production methods is likely to enhance cost-effectiveness.

De-aromatic solvents are finding emerging applications in electronics, aerospace, and renewable energy sectors, thereby contributing to future growth. Rising focus on sustainability is estimated to drive the adoption of de-aromatic solvents across industries. Companies are expanding in niche market like agrochemicals and pharmaceuticals as they offer high growth potential.

The de-aromatic solvents market growth was robust at a CAGR of 5.6% during the historical period. Increasing enforcement of VOC reduction standards worldwide pushed industries to adopt low-VOC de-aromatic solvents. Rapid industrialization in Asia Pacific boosted demand, especially in paints, adhesives, and coatings. Innovation in hydrogeneration processes enhanced solvent quality and broadened their application scope.

The market witnessed a temporary decline in 202 owing to disruptions in supply chains and decreased industrial activity. Demand for these solvents rebounded strongly in 2021 and 2022 as industries resumed their operations and prioritized sustainable solutions. The pharmaceuticals industry witnessed increased adoption during the period owing to their safety profile for sensitive applications.

Recycling and Reuse Technologies to Open New Opportunities

Stringent environmental laws globally are encouraging industries to adopt solvent recycling to decrease hazardous waste and emissions. The European Union Waste Framework Directive emphasizes resource efficiency and circular economy practices.

The Resource Conservation and Recovery Act (RCRA) enforced solvent recycling to manage hazardous waste responsibility. Recycling solvents decreases raw material costs, offering industries a cost-effective alternative to continuous procurement.

High purity recycles solvents are often comparable in performance to virgin solvents, thereby making them suitable for reuse in demanding applications. Recycling aligns with corporate sustainability and Environmental, Social, and Governance (ESG) goals.

Fractional distillation is a common recycling method that separates solvents from contaminants by leveraging differences in boiling points. Advanced distillation systems enable recovery rates of 99%, thereby decreasing waste significantly.

Diversification of Applications to Augment Expansion

De-aromatic solvents offer unique advantages like minimal colour, low toxicity, and high solvency power, thereby making them adaptable for various industries. Their ability to replace conventional solvents in regulated industries, thereby driving demand in new sectors.

Stringent environmental and safety regulations are promoting industries to adopt de-aromatic solvents as safer alternatives to conventional aromatic solvents like toluene and xylene. Rapid industrial growth in regions like Asia Pacific and Middle East has increased the demand for high-performance solvents in diverse applications. These solvents are being utilized as carriers and diluents in pesticide and herbicide formulations.

The oil and gas industry uses de-aromatic solvents for degreasing, cleaning, and in drilling fluids. Expanding exploration and production activities are prominent growth drivers in the industry.

Fluctuations in Raw Material Prices to Limit Growth

Production of de-aromatic solvents heavily relies on petroleum-based feedstocks, thereby making their market dynamics closely tie to crude oil price volatility. Disruptions in crude oil supply chains and volatility in prices caused by natural disasters, geopolitical events, ad infrastructure issues can result in raw material shortages and price surges. Refinery maintenance schedule or shutdowns can decrease the availability of feedstocks for de-aromatic solvent production.

Petrochemical feedstock used for de-aromatic solvents are in demand for producing fuels, polymer, and other chemicals, resulting in competitive pricing pressures. Increased demand for ethylene and propylene derivatives can divert feedstock availability, thereby raising prices for solvents. Raw materials account for 30% to 50% of the total production costs of de-aromatic solvents. Fluctuations in crude oil prices can substantially alter production economics.

Increasing Demand for Low VOC and Eco-friendly Solvents

Government authorities across the globe are imposing stringent regulations to limit VOC emissions, thereby encouraging industries to shift toward eco-friendly solvents. The REACH Regulation and Directive 2004/42/EC by the European Union (EU) aims to decrease VOC emissions in paints, coatings, and adhesives.

The EPA Clean Air Act in the U.S. mandates VOC limits for industrial applications. China’s Air Pollution Prevention and Control Action Plan focuses on decreasing industrial emissions. Industries are aligning with global sustainability goals, especially those outlined in the United Nations Sustainable Development Goals (SDGs) that encourage sustainable production practices.

End-users are opting for green-labelled products, thereby pushing manufacturers to innovate and adopt eco-friendly solvents. Global VOC emissions cap is estimated to tighten by 20% to 30% by 2030, thereby driving the demand for compliant solvent alternatives. A survey by the European Solvents Industry Group (ESIG) revealed that 70% of industrial users prioritize solvent solutions that are effective as well as environmentally sustainable.

Adoption of Bio-based and Renewable Solvents to Augment Demand

Rising consumer awareness and preference for green products are riving the demand for bio-based solvents. Companies are aligning with global sustainability frameworks like United Nations Sustainable Development Goals (SDGs), especially Goal 12 and Goal 13.

Global regulations are mandating reductions in hazardous and VOC-emitting substances, thereby pushing industries toward safer alternatives. Countries are incentivizing bio-based chemical production through tax benefits and subsidies to decrease dependency on fossil fuels.

Bio-based solvents typically have a lower carbon footprint compared to petroleum-based solvents. A survey conducted by the European Commission found that bio-based solvents coupled decrease greenhouse gas emissions by 50% to 80% compared to conventional solvents.

Companies in the de-aromatic solvents market are working toward creating low-toxicity, sustainable, and VOC-compliant de-aromatic solvents to meet the environmental regulations and consumer demand. They are offering custom-made solvents for particular industry requirements.

Businesses are introducing solvents with improved properties like low odor, high flash points, and better solvency power. Organizations are entering emerging markets where industrialization is at its peak. They are targeting industries like automotive, electronics, and construction.

Companies are also progressively collaborating with distributors and local players to expand market reach. They are also investing in advanced manufacturing technologies to decrease production costs. Businesses are establishing long-term supply contracts for raw materials and optimizing logistics.

Recent Industry Developments

The market is anticipated to reach a value of US$ 2.4 Bn by 2032.

Common uses for high purity solvents are in dry cleaning, paint thinners, nail polish removers, and glue solvents.

North America is estimated to emerge as the leading region with a share of 39% in 2024.

Exxon Mobil Corporation, Shell Plc, Idemitsu Kosan Co., Ltd. are the prominent companies in the market.

The market is predicted to witness a CAGR of 5.6% through th2031.

|

Attributes |

Details |

|

Forecast Period |

2025 to 2032 |

|

Historical Data Available for |

2019 to 2023 |

|

Market Analysis |

US$ Billion for Value |

|

Key Regions Covered |

|

|

Key Market Segments Covered |

|

|

Key Companies Profiled in the Report |

|

|

Report Coverage |

|

|

Customization and Pricing |

Available upon request |

By Flash Point

By Boiling Point

By Application

Region

Delivery Timelines

For more information on this report and its delivery timelines please get in touch with our sales team.

About Author