- Clothing, Footwear, & Accessories

- Costume Jewelery Market

Costume Jewelery Market Size, Share and Growth Forecast, 2026 - 2033

Costume Jewelery Market by Product Type (Necklaces & chains, Earrings, Rings, Bracelets & bangles, Anklets, Hair accessories), End User (Women, Men, Children, Unisex), Material (Metal, Plastic & resin, Glass, Fabric, Sustainable materials), and Regional Analysis for 2026 - 2033

Costume Jewelery Market Share and Trends Analysis

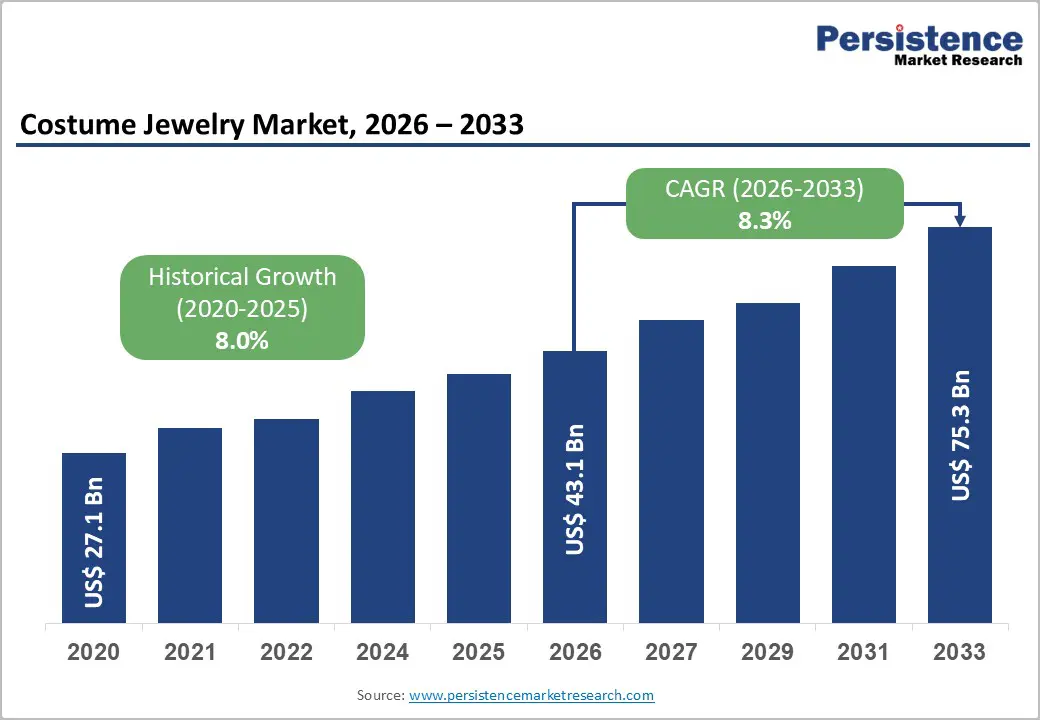

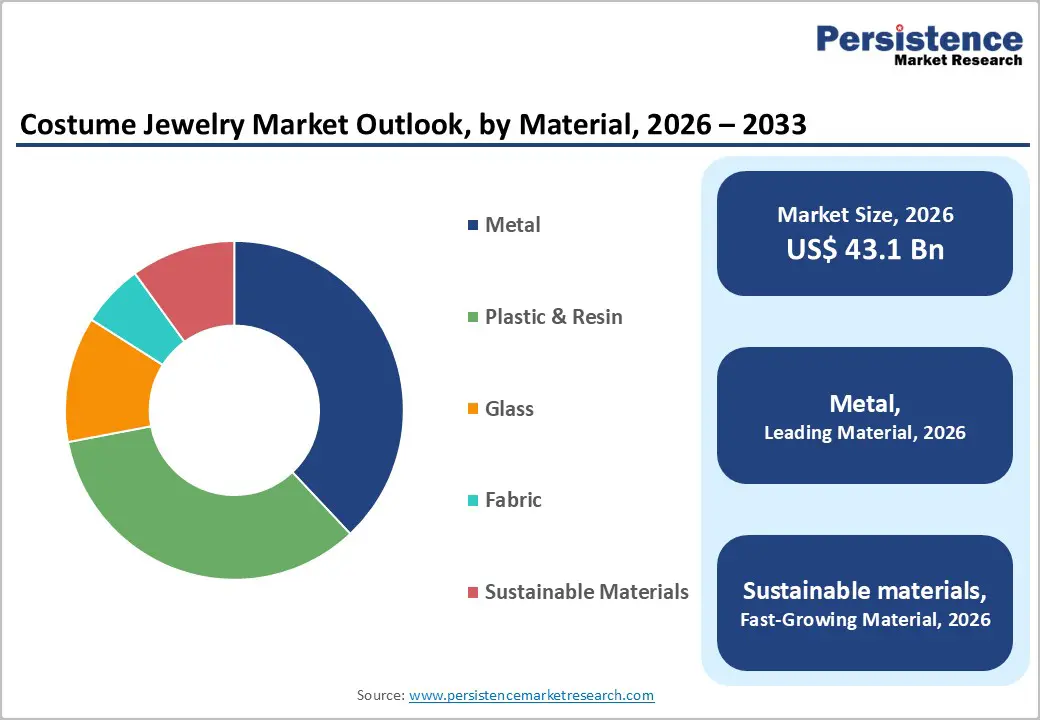

The global Costume Jewelery market size is likely to be valued at US$ 43.1 billion in 2026 and is projected to reach US$ 75.3 billion by 2033, growing at a CAGR of 8.3% during the forecast period of 2026-2033.

The market demonstrates steady, consumption-driven growth, primarily supported by rising disposable incomes and increasing urbanization across developing economies. As middle-class populations expand, particularly in the Asia Pacific, consumers are allocating a greater share of income toward affordable fashion and lifestyle products, including costume jewelery.

Key Industry Highlights

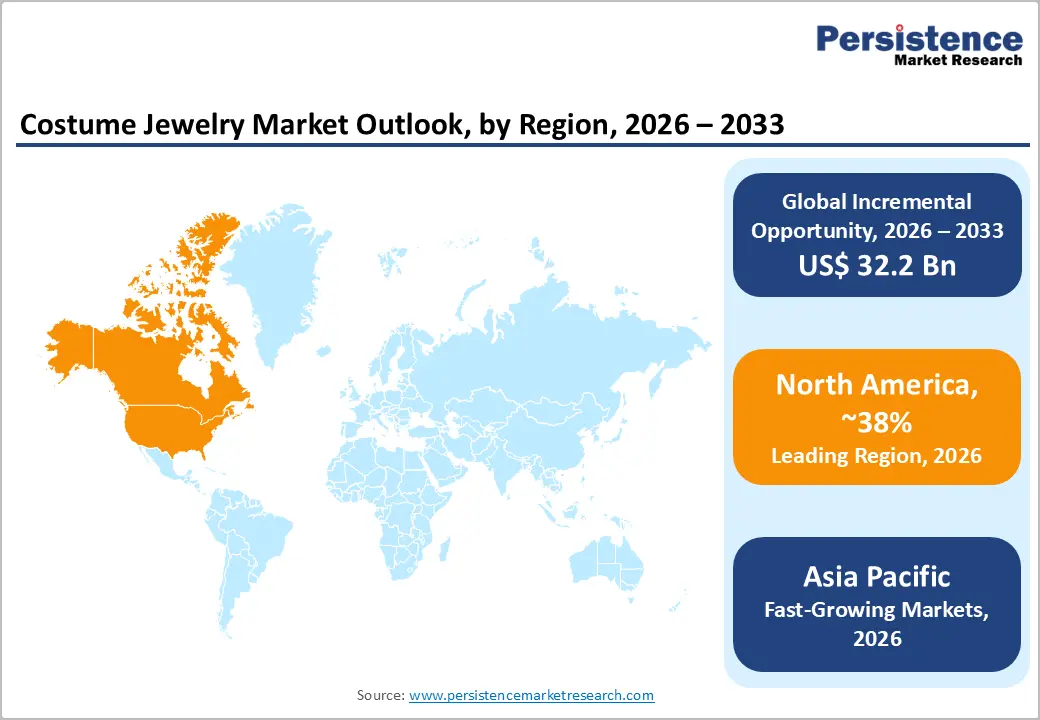

- Regional Leadership: North America is poised to dominate with over 38% share in 2026, and Asia Pacific is projected to register a CAGR of over 9% through 2033, driven by strong manufacturing capabilities and rising consumption in China, India, and Southeast Asia.

- Dominant Product Types: Necklaces & chains are expected to lead with around 30% share in 2026, while earrings are likely to emerge as the fastest-growing segment, supported by affordability and high replacement frequency.

- Leading End Users: Women are anticipated to dominate with over 65% share in 2026, while unisex jewelry is set to be the fastest-growing segment, reflecting increasing demand for gender-neutral designs.

- Dominant Materials: Metal-based jewelry is projected to lead with approximately 40% share in 2026, while sustainable materials are expected to witness the fastest growth, driven by rising ESG compliance and consumer awareness.

- Key Market Trends: Trends include sustainability adoption, expansion of digital retail channels, and growing demand for personalization, enhancing customer engagement and brand differentiation.

- Competitive Environment: Competitive dynamics focus on ESG integration, expansion of direct-to-consumer (DTC) models, and digital innovation, strengthening market positioning and profitability.

| Key Insights | Details |

|---|---|

|

Costume Jewelery Market Size (2026E) |

US$ 43.1 Bn |

|

Market Value Forecast (2033F) |

US$ 75.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

8.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

8.0% |

DRO Analysis

Driver - Rising Disposable Income and Fast Fashion Consumption Trends

According to the World Bank and IMF macroeconomic outlooks, global middle-class population expansion, especially in Asia, continues to drive discretionary spending. Costume Jewelery benefits directly from this trend as it offers affordable alternatives to precious Jewelery, with price points accessible to a broader demographic. Fast fashion brands such as Zara and H&M have reported double-digit accessory category growth, indicating strong demand cycles. This consumption pattern drives repeat purchases, with consumers buying multiple pieces per season. As a result, volume sales growth remains a primary revenue driver, particularly in urban markets with high fashion sensitivity.

The increasing affordability of fashion-led accessories is also encouraging frequent wardrobe refresh cycles across younger consumer groups. Recent fashion industry movements further reinforce this trend. Jewelery is increasingly positioned as a core fashion element rather than a secondary accessory, with consumers styling entire outfits around statement pieces.

Additionally, major retail events such as global online sale campaigns in 2025 highlighted strong consumer preference for affordable, luxury-look accessories, with products priced as low as a few dollars gaining mass traction. This shift indicates that consumers are prioritizing high-frequency, low-cost purchases, strengthening the role of costume Jewelery in everyday fashion consumption and sustaining consistent market demand. The rise of social media styling trends has further amplified impulse buying behavior across global markets.

Expansion of E-commerce and Product Innovation with Sustainable Material Adoption

Data from UNCTAD and Statista indicate that global e-commerce penetration exceeded 22% of total retail sales in 2025, with fashion accessories being one of the fastest-growing categories. Platforms such as Amazon, Myntra, and SHEIN have significantly increased the visibility and accessibility of costume Jewelery. Digital channels allow direct-to-consumer (DTC) brands to scale rapidly, reducing dependency on physical retail. Additionally, influencer marketing and social commerce have enhanced product discovery. This shift has led to higher inventory turnover rates and improved margins, particularly for small and mid-sized brands leveraging data-driven personalization strategies. The continued rise of mobile-first shopping is also making costume Jewelery one of the most frequently purchased impulse fashion categories globally.

Industry developments highlight rapid technological and sustainability-driven transformation. The adoption of AI-powered shopping experiences, virtual try-ons, and creator-led storefronts has significantly improved online engagement and conversion rates across fashion accessories. Sustainability has emerged as a critical purchase driver, with a growing share of consumers showing strong interest in eco-friendly Jewelery, even as awareness continues to evolve. These shifts are encouraging brands to innovate with recyclable and bio-based materials while leveraging digital platforms, creating a dual growth engine driven by technology adoption and sustainability alignment. These factors are reshaping product design, marketing strategies, and customer engagement models across the industry.

Restraints - Volatility in Raw Material Costs and Supply Chain Disruptions

In 2025, global supply chains faced disruptions due to geopolitical tensions and fluctuating commodity prices. Reports from the World Trade Organization (WTO) indicate increased logistics costs by 8–12% in certain trade corridors, impacting manufacturing margins. Materials such as metals and synthetic resins experienced price volatility, directly affecting production costs. For small manufacturers, this creates margin compression and pricing challenges, limiting competitiveness in price-sensitive markets. This also leads to unstable procurement cycles, making it difficult to maintain consistent output for fast-moving fashion collections.

A key real-world disruption affecting the costume jewelery supply chain has been the tightening of trade compliance and shipment-level enforcement across major import hubs. The U.S. Consumer Product Safety Commission (CPSC) has issued multiple recalls of imported jewelery products after laboratory testing identified unsafe levels of lead and cadmium in low-cost accessories sold through large online marketplaces.

In parallel, European customs authorities intensified inspections at entry points such as Rotterdam and Hamburg ports, leading to the detention and rejection of non-compliant fashion Jewelery shipments originating from low-cost manufacturing clusters in Asia. These actions have directly disrupted inventory flows, increased rejection rates, and forced retailers to redesign supplier onboarding and testing protocols, thereby raising operational costs across the value chain.

Regulatory Compliance and Product Safety Standards

Regulations regarding chemical usage, such as restrictions on lead and cadmium in jewelery (notably in the EU and North America), have intensified. Several product recalls were reported due to non-compliance with safety standards, reinforcing stricter enforcement across major markets. These regulations increase testing, certification, and compliance costs, especially for exporters. As a result, entry barriers for new players rise, and existing players must invest in quality assurance systems, impacting profitability. This also extends product approval timelines, reducing responsiveness to fast-changing fashion trends.

A concrete example of tightening enforcement is the action taken by the U.S. Consumer Product Safety Commission (CPSC), which has mandated recalls of children’s and fashion Jewelery products sold via major e-commerce platforms after detecting hazardous levels of heavy metals exceeding federal safety limits. Similarly, European regulators under the European Chemicals Agency (ECHA) framework have strengthened REACH compliance enforcement, resulting in the withdrawal of non-compliant accessories from retail circulation. These regulatory actions have led to stricter import screening, mandatory third-party testing requirements, and increased documentation burdens for exporters. Consequently, manufacturers are facing longer clearance timelines, higher compliance expenditure, and reduced flexibility in launching fast-fashion collections.

Opportunities - Growth in Emerging Markets

According to OECD and World Bank data, consumer spending in emerging economies grew by over 6% in 2025, significantly outpacing developed markets. Countries such as India, Indonesia, and Brazil present strong demand potential due to young populations and rising fashion awareness. Localized designs and culturally relevant collections offer high-margin growth opportunities. This expansion is further reinforced by increasing affordability-driven demand across urban and semi-urban consumer bases, where costume jewelery is increasingly viewed as an everyday fashion essential.

Recent retail and policy-led developments are strengthening this opportunity. Governments across Asia, particularly in India and Southeast Asia, have continued to support digital commerce infrastructure expansion, improving logistics networks and cross-border e-commerce accessibility. At the same time, global fashion cycles have highlighted a strong shift toward “affordable luxury” and expressive jewelery trends, with chunky chains, pearls, stacked bracelets, and eco-inspired designs gaining visibility across global fashion showcases.

Additionally, the rise of AI-driven retail personalization (“cute tech”), social commerce platforms, and digital-first marketplaces is enabling faster product discovery, localized targeting, and improved conversion rates. These combined factors are accelerating penetration in underserved regions while expanding revenue opportunities for both global and regional brands.

Personalization and Customization Trends

In 2025, multiple fashion brands introduced AI-driven customization tools, allowing consumers to design personalized jewelery. Reports indicate that personalized products can increase conversion rates by up to 20%. This trend enables brands to differentiate and command premium pricing. Customization also enhances customer engagement, resulting in higher lifetime value (LTV) and repeat purchases. It is increasingly positioning jewelery as a form of identity expression rather than just a fashion accessory, especially among digitally native consumers seeking uniqueness and self-expression.

Industry movements are rapidly strengthening this opportunity through the deep integration of advanced retail technologies. The fashion sector is increasingly adopting AI-powered search systems, virtual try-on solutions, and personalized recommendation engines, enabling real-time product customization and highly interactive shopping experiences. The advancements in computer vision-based jewelery visualization and virtual accessory simulation are improving purchase confidence by allowing consumers to accurately preview designs before buying. These innovations are reducing return rates, increasing purchase intent, and supporting scalable hyper-personalized collections. As a result, customization is evolving into a core revenue driver, particularly for DTC brands and digital-first Jewelery retailers, while also complementing broader trends in social commerce and influencer-led product personalization.

Category-wise Analysis

Product Type Insights

Necklaces & chains are expected to dominate the market, accounting for approximately 30% of total revenue in 2026, driven by high visibility, versatility, and strong styling impact across fashion categories. These products are widely used as statement accessories in everyday wear, festive styling, and runway-inspired collections. Their demand is reinforced by fast fashion-driven style cycles and strong influence from digital fashion content. Recent developments include H&M’s 2026 global accessory collection, emphasizing bold layered chain necklaces integrated into minimalist fashion lines, which gained rapid traction across online retail channels.

In parallel, Myntra’s AI-based fashion feed upgrades in late 2025 began prioritizing necklace-led outfit suggestions in styling recommendations, significantly improving product discovery and engagement. Additionally, London Fashion Week showcased industrial-inspired metallic chain designs, which quickly influenced mass-market accessory collections and strengthened global demand momentum.

Earrings are projected to be the fastest-growing product type, supported by affordability, design diversity, and frequent replacement cycles. Consumers often purchase multiple pairs for different occasions, making earrings a high-frequency fashion accessory. Lightweight, skin-friendly, and hypoallergenic designs are gaining strong traction among younger consumers. In parallel, Flipkart Fashion introduced an AI-driven “style match” feature in late 2025 that recommends earrings based on facial structure and outfit color profiling, improving conversion rates and personalization. Additionally, Milano Fashion Week highlighted abstract sculptural earrings and ear-architecture designs, which were rapidly translated into affordable retail versions across digital-first fashion platforms, reinforcing earrings as a high-velocity trend category.

Material Insights

Metal-based jewelery is expected to hold the leading position with approximately 40% share in 2026, driven by durability, aesthetic versatility, and compatibility with advanced plating technologies. These products are widely preferred for everyday and occasion wear due to their premium look at accessible prices. Improved surface finishing techniques have enhanced scratch resistance and color retention, strengthening customer satisfaction. Recent developments include H&M’s upgraded 2026 accessory line featuring titanium-coated brass designs focused on anti-tarnish performance. Shein also expanded double-layer electroplated collections to reduce fading in high-turnover products. Additionally, increased adoption of PVD coating in key manufacturing hubs has improved durability and finish quality across global supply chains.

Sustainable materials are the fastest-growing segment, supported by environmental awareness, regulatory pressure, and demand for ethical fashion. Recycled metals, biodegradable resins, and plant-based composites are increasingly replacing conventional inputs in new collections. Younger consumers are strongly influencing demand for transparency in sourcing and production practices. Recent developments include Mango’s 2026 recycled metal Jewelery capsule collection, launched across global retail stores. Zalando introduced a material transparency filter in late 2025 to improve visibility of sustainable products at checkout. Additionally, stricter EU border checks on imported Jewelery have accelerated the adoption of certified sustainable sourcing across supply chains.

Regional Analysis

North America Costume Jewelery Market Trends

North America is expected to be the leading regional market for costume jewelery, with over 38% share in 2026, while the United States acts as the primary revenue contributor. The region shows stable expansion supported by high disposable income and strong demand for fashion-forward accessories. Well-developed e-commerce infrastructure and omnichannel retail networks enhance accessibility across consumer groups. Frequent fashion refresh cycles and the strong influence of social media trends continue to drive repeat purchases. The presence of established fashion brands and rising direct-to-consumer players further strengthens market penetration. Consumers increasingly view costume jewelery as an affordable way to align with fast-changing fashion styles.

Recent developments highlight tighter regulatory oversight and rapid digital retail transformation. The U.S. Consumer Product Safety Commission (CPSC) has intensified enforcement on imported fashion Jewelery, leading to multiple recalls of products containing unsafe levels of lead and cadmium, directly impacting sourcing and compliance practices. In parallel, leading U.S. fashion e-commerce platforms have expanded AI-driven recommendation systems that personalize accessory suggestions based on browsing behavior and purchase history, improving conversion in jewelery categories. Additionally, 2026 fashion retail showcases in New York have emphasized “affordable luxury” accessory collections, reinforcing strong demand for trend-led costume jewelery across both online and offline retail channels.

Europe Costume Jewelery Market Trends

Europe remains a high-value market led by Germany, the United Kingdom, France, and Spain. Demand is strongly influenced by premium fashion preferences, design innovation, and consumer focus on product quality. Seasonal fashion cycles and luxury-inspired styling trends continue to support consistent accessory consumption. E-commerce growth complements traditional retail, creating a balanced omnichannel ecosystem. Consumers demonstrate a strong preference for ethically produced and aesthetically refined Jewelery, making design and sustainability key purchase drivers. Brand loyalty and heritage fashion influence remain strong across major markets.

Recent industry movements reflect increasing regulatory pressure and sustainability-led transformation. The European Chemicals Agency (ECHA), under REACH regulations, has strengthened inspections on imported Jewelery, particularly focusing on material traceability and restricted substances, pushing brands toward compliant sourcing practices. At the same time, European fashion retailers have expanded certified recycled-metal Jewelery collections across 2026 product lines, integrating sustainability into mainstream offerings. Additionally, major European fashion weeks have prominently showcased upcycled and lab-processed metallic Jewelery designs, accelerating the adoption of circular fashion practices and influencing both premium and mass-market accessory collections.

Asia Pacific Costume Jewelery Market Trends

Asia Pacific is likely to be the fastest-growing costume jewelery market, supported by a projected CAGR 9% in the forecast period. The growth is driven by a large youth population, rising disposable incomes, and increasing fashion awareness across urban centers. Strong manufacturing capabilities and cost-efficient production ecosystems reinforce the region’s dominance in global supply chains. Rapid expansion of e-commerce and mobile-first shopping platforms further enhances market penetration. Cultural diversity also supports high demand for localized and occasion-based Jewelery designs.

Recent developments highlight strong industrial scaling and digital commerce acceleration. China’s manufacturing clusters in Guangdong have increasingly adopted automated polishing and nano-coating systems in Jewelery production lines, improving durability and export quality standards, and strengthening global competitiveness. In India, national digital commerce initiatives have expanded integration of fashion retail across online marketplaces and local seller ecosystems, improving access for small Jewelery brands in Tier 2 and Tier 3 cities. Additionally, ASEAN fashion trade exhibitions in 2026 have highlighted rapid growth in export-oriented costume Jewelery production hubs, reflecting strong international demand and positioning the region as a central supply base for global fashion accessories.

Competitive Landscape

The costume jewelery market is highly fragmented, with competition driven by price, design frequency, and fast trend responsiveness rather than strong brand loyalty. Global fashion retailers and large e-commerce platforms collectively hold significant influence through scale, rapid inventory turnover, and integrated sourcing networks across Asia. These players leverage agile supply chains to quickly convert fashion trends into affordable jewelery collections. Competition remains intense due to low product differentiation and high substitution rates.

Fast fashion brands such as Zara, H&M, and Mango, along with digital-first platforms such as Shein and ASOS, dominate trend-driven demand through rapid product launches and influencer-led marketing. Regional manufacturers in China, India, and Southeast Asia maintain strong production dominance due to cost advantages and scalable capabilities. However, rising sustainability requirements and stricter material compliance standards are gradually increasing entry barriers. This is encouraging gradual consolidation and stronger vertical integration across leading players.

Key Industry Developments

- In October 2025, Kering’s divestment of its beauty division to L’Oréal reflects a strategic shift toward strengthening its core fashion and accessories portfolio. This restructuring allows greater focus on high-margin fashion categories, including Jewelery and lifestyle accessories, while streamlining brand priorities.

- In April 2025, Prada Group’s acquisition of Versace strengthened consolidation within the global fashion ecosystem, enhancing its influence across premium and accessible fashion accessory categories. The move is expected to accelerate luxury-to-affordable design spillover, improving product innovation in costume Jewelery offerings.

Companies Covered in Costume Jewelery Market

- Pandora A/S

- Swarovski AG

- Fossil Group Inc.

- H&M Group

- Zara

- Lovisa Holdings Ltd.

- Claire’s Holdings LLC

- Accessorize

- BaubleBar Inc.

- Mejuri Inc.

- Chopard

- Tanishq

- SHEIN

Frequently Asked Questions

The global costume Jewelery market is projected to reach US$ 43.1 billion in 2026.

Rising fast fashion consumption, e-commerce expansion, and demand for affordable fashion accessories are driving the market.

The market is expected to grow at a CAGR of 8.3% from 2026 to 2033.

Growth in emerging markets, personalization trends, and sustainable fashion adoption are key opportunities.

Major players include Zara, H&M, Shein, Mango, Pandora, Swarovski, Claire’s, and Etsy sellers ecosystem.