- Industrial Goods & Service

- Coiled Tubing Market

Coiled Tubing Market Size, Share, and Growth Forecast 2026 - 2033

Coiled Tubing Market by Services (Well Intervention & Production (Well Completion, Well Cleaning, Others), Drilling, Others), by Operations (Circulation, Pumping, Logging, Perforation, Others), by Application (Onshore, Offshore), and Regional Analysis, 2026 - 2033

Coiled Tubing Market Size and Trend Analysis

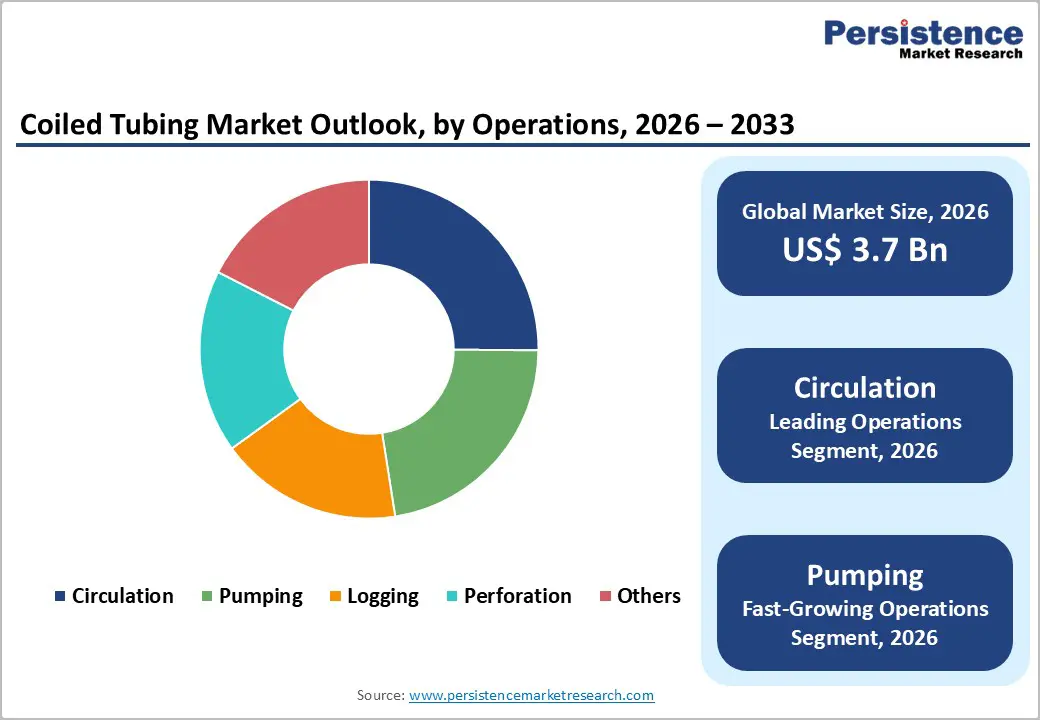

The global coiled tubing market size is expected to be valued at US$ 3.7 billion in 2026 and projected to reach US$ 5.3 billion by 2033, growing at a CAGR of 5.2% between 2026 and 2033.

Growth is driven by rising demand for efficient well intervention in aging oilfields, where operators prioritize cost-effective and time-saving solutions over conventional workover rigs. Advancements in high-strength materials and real-time monitoring technologies are enabling deeper, complex well operations with improved safety and efficiency. Additionally, increasing offshore exploration and production activities, along with higher rig utilization across key basins, are further supporting market expansion globally.

Key Industry Highlights:

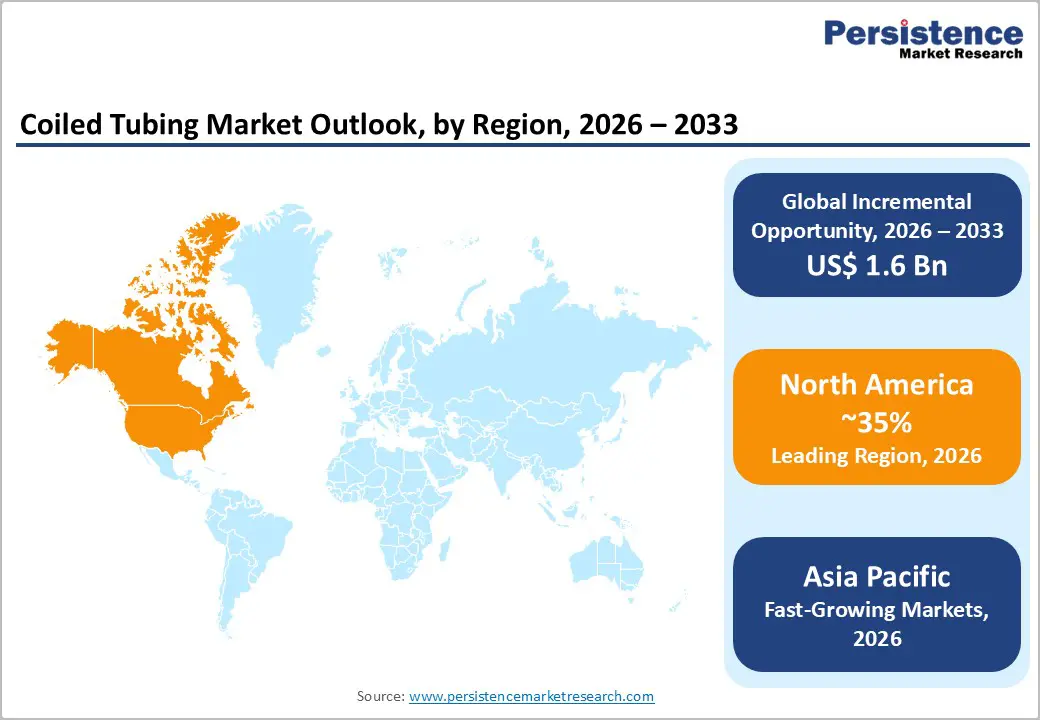

- Leading Region: North America dominates with 35% share, supported by strong shale activity and extensive mature field interventions.

- Fastest Growing Region: Asia Pacific emerges as the fastest-growing region, driven by expanding upstream activities in China and India.

- Leading Service Category: Well Intervention & Production leads with 55% share due to its efficiency in live-well operations and production optimization.

- Leading Application Category: Onshore dominates with 65% share, supported by large-scale shale developments and cost-efficient operations.

- Key Opportunity: High-strength coiled tubing materials present significant growth opportunities in complex and deep offshore operations.

| Key Insights | Details |

|---|---|

| Coiled Tubing Size (2026E) | US$ 3.7 billion |

| Market Value Forecast (2033F) | US$ 5.3 billion |

| Projected Growth CAGR (2026 - 2033) | 5.2% |

| Historical Market Growth (2020 - 2025) | 4.4% |

Market Dynamics

Drivers - Increasing Demand for Cost-Effective Well Intervention in Mature Oilfields

Mature oilfields account for a significant share of global production and require frequent intervention to sustain output. Coiled tubing enables efficient operations such as well cleanouts, acidizing, and nitrogen lifting without shutting down production. Its ability to operate under live well conditions minimizes downtime and enhances productivity, making it a preferred solution for operators managing aging assets.

Operators increasingly rely on coiled tubing to reduce operational costs and improve recovery from declining wells. Compared to conventional workover rigs, it offers faster deployment and lower logistical complexity. This advantage is crucial as thousands of wells require periodic maintenance, strengthening coiled tubing’s role in extending field life and ensuring economically viable production from mature reservoirs.

Growing Use of Coiled Tubing in Unconventional Oil and Gas Operations

The rapid growth of unconventional resources such as shale oil and gas has significantly increased the demand for coiled tubing services. These operations require advanced techniques like frac plug milling and wellbore cleanouts in horizontal wells, where coiled tubing provides continuous operation and reduced intervention time, improving overall efficiency and supporting higher production rates.

Additionally, increasing horizontal drilling activity across key regions is driving adoption. Coiled tubing supports complex well architectures with improved precision and flexibility. Technological advancements, including real-time monitoring and enhanced materials, further boost performance, making it an essential tool for operators seeking cost-effective and efficient solutions in unconventional oil and gas development.

Restraints - Increasing Regulatory Pressure and Emission Compliance Costs Impacting Operations

Stringent environmental regulations are creating challenges for coiled tubing operations, particularly in regions with strict carbon policies. Frameworks such as the European Union Emissions Trading System impose significant carbon costs, increasing the financial burden on diesel-powered equipment commonly used in coiled tubing services.

These compliance requirements elevate overall project costs due to the need for emission control technologies and cleaner alternatives. Studies from International Association of Oil & Gas Producers indicate rising operational expenses, which can slow adoption in highly regulated markets and encourage a gradual shift toward electrified or hybrid solutions still under development.

Limit

High Capital Investment and Maintenance Costs Limiting Market Expansion

Coiled tubing operations require substantial capital investment, with equipment costs running into several million dollars per unit. Leading providers such as Schlumberger highlight the high cost of advanced coiled tubing systems, making entry difficult for smaller operators and limiting widespread adoption across emerging markets.

In addition to initial investment, ongoing maintenance expenses further increase the financial burden. According to insights from the Society of Petroleum Engineers, upkeep of high-pressure systems and tubing fatigue management adds high annual costs, extending return on investment timelines and constraining fleet expansion during periods of oil price volatility.

Opportunities - Technological Advancements in High-Strength Materials Enhancing Operational Capabilities

Advancements in high-strength coiled tubing materials are creating significant growth opportunities by improving durability and performance. Innovations such as quench-and-temper steel alloys enhance fatigue resistance and enable operations in high-pressure environments, making them suitable for complex and deep well applications, particularly in challenging offshore conditions.

These developments are increasingly relevant for deepwater projects, supported by data from the Bureau of Ocean Energy Management. Equipment manufacturers like NOV Inc. are driving innovation, while evolving industry standards are expected to further accelerate the adoption of advanced materials in high-value drilling and intervention activities.

Rising Offshore Decommissioning Activities Driving Service Demand Globally

The growing number of aging offshore wells is driving demand for efficient decommissioning solutions, creating strong opportunities for coiled tubing services. Plug and abandonment operations require cost-effective and flexible technologies, where coiled tubing offers advantages in reducing operational complexity and improving execution timelines.

Regulatory frameworks in regions such as the North Sea, supported by the UK Oil and Gas Authority, encourage efficient decommissioning practices. Industry insights from Oil & Gas Journal highlight rising well-decommissioning volumes, while emerging offshore developments in the Asia Pacific further expand the addressable market for service providers.

Category-wise Analysis

Services Insights

Well Intervention & Production dominates the services segment, accounting for approximately 55% market share in 2025. Its leadership is driven by versatility in live-well operations, especially across mature fields that form a major portion of global production. Coiled tubing significantly reduces intervention time compared to conventional methods, making it highly effective for well completion, cleaning, and production optimization across both onshore and offshore assets.

Drilling services are emerging as the fastest-growing segment due to the increasing complexity of well architectures and the rising demand for efficient drilling support. Coiled tubing drilling enables continuous operations, reduces formation damage, and improves cost efficiency. Its growing adoption in underbalanced drilling and re-entry operations is expanding its role across unconventional and deepwell projects globally.

Operations Insights

Circulation holds the largest share of around 40% in 2025 within the operations segment, primarily due to its critical role in fluid displacement and debris removal during well cleanouts. It is widely used across intervention activities, offering high operational efficiency and reduced need for complex rig setups, making it a preferred choice in both conventional and unconventional wells.

Pumping operations are witnessing the fastest growth, supported by increasing demand for stimulation treatments and fluid injection processes. Coiled tubing enables precise pumping in high-pressure environments, improving treatment effectiveness. Its application in acidizing, fracturing support, and chemical injection is expanding rapidly, particularly in shale and tight reservoir developments.

Application Insights

Onshore applications account for approximately 65% of the market share in 2025, driven by large-scale shale developments and easier access to well sites. Lower logistical costs and higher operational flexibility make onshore deployments more economical, especially in key producing regions where frequent well interventions and maintenance activities are required to sustain production levels.

Offshore applications are the fastest growing segment, supported by increasing deepwater and ultra-deepwater exploration activities. Coiled tubing is gaining traction in offshore environments due to its ability to handle complex well conditions and reduce downtime. Advancements in equipment reliability and subsea capabilities are further strengthening its adoption in offshore intervention and completion operations.

Regional Insights

North America Coiled Tubing Market Trends and Insights

North America dominates the coiled tubing market, accounting for approximately 35% share in 2025. This leadership is driven by extensive shale developments, particularly in the Permian Basin, along with high rig activity and frequent well intervention requirements. Offshore advancements in the Gulf of Mexico and increasing adoption of low-emission technologies further strengthen the region’s market position.

The region continues to see strong demand due to ongoing unconventional resource development and technological innovation. Increasing deployment of automated and electric coiled tubing units is improving efficiency and sustainability. Additionally, continuous investments in upstream activities and infrastructure are expected to support long-term growth across both onshore and offshore operations.

Europe Coiled Tubing Market Trends and Insights

Europe is experiencing steady growth in the coiled tubing market, with a projected CAGR of approximately 5.8% during the forecast period. The North Sea remains a key contributor, where aging oilfields require frequent intervention and maintenance, supporting consistent demand for coiled tubing services across offshore assets.

Growth is further driven by stringent environmental regulations and energy transition initiatives across the region. Increasing focus on low-emission technologies, carbon capture projects, and efficient decommissioning practices is expanding application areas. Countries such as Norway, the UK, and Germany are emphasizing sustainable operations, boosting the adoption of advanced coiled tubing solutions.

Asia Pacific Coiled Tubing Market Trends and Insights

Asia Pacific holds approximately 30% share of the coiled tubing market and is emerging as a high-growth region. Expansion of upstream activities in countries like China and India, along with increasing rig counts and energy demand, are key factors driving market development across the region.

The region is witnessing rising investments in offshore exploration, particularly in Southeast Asia, which is accelerating demand for coiled tubing services. Additionally, cost-effective manufacturing capabilities and growing focus on enhancing domestic energy production are supporting market expansion, making the Asia Pacific a key future growth engine.

Competitive Landscape

The coiled tubing market is moderately consolidated, characterized by the presence of established global players and a mix of regional service providers. Companies are focusing on strategic expansions through partnerships and acquisitions to enhance service capabilities and geographic reach. Increasing demand for operational efficiency is encouraging firms to strengthen their service portfolios and optimize fleet deployment across key oil and gas regions.

Innovation remains a key competitive factor, with ongoing investments in advanced materials such as composite tubing to improve durability and fatigue resistance. Digital monitoring and real-time data integration are becoming important differentiators, enabling better performance tracking and decision-making. Additionally, flexible business models, including equipment rental and service-based offerings, are gaining traction.

Key Developments:

- In March 2025, Schlumberger launched the AXEssentials suite designed for real-time coiled tubing monitoring, significantly improving operational visibility, enhancing worker safety, and enabling more efficient decision-making across complex well intervention activities.

- In July 2024, Halliburton introduced eco-friendly electric coiled tubing units, which were trialed in the North Sea, demonstrating around 40% emission reduction while improving operational efficiency and supporting sustainability goals in offshore energy operations.

- In November 2023, Baker Hughes acquired a specialized coiled tubing service provider to strengthen its onshore shale capabilities, particularly in the Permian Basin, enhancing its service portfolio and expanding its presence in high-demand unconventional resource markets.

Companies Covered in Coiled Tubing Market

- Schlumberger Limited

- Halliburton Company

- Baker Hughes Company

- Weatherford International Plc

- NOV Inc.

- Calfrac Well Services Ltd.

- Trican Well Service

- Nabors Industries Ltd.

- C&J Energy Services Inc.

- RPC, Inc.

- Step Energy Services Ltd.

- Superior Energy Services

- Nine Energy Service

- Global Tubing LLC

- Coil Tubing Technology Inc.

Frequently Asked Questions

The global Coiled Tubing Market is expected to reach US$ 3.7 billion in 2026, driven by well intervention demand.

Mature field interventions in shale plays, reducing downtime by 40%, propel demand per EIA and SPE data.

North America holds 35% share in 2025, led by U.S. Permian shale activities.

High-strength tubing for offshore decommissioning, targeting 4,000+ wells by 2030.

Leading firms include Schlumberger, Halliburton, Baker Hughes, and Weatherford, focusing on tech innovations.