- Pharmaceuticals

- Cholangiocarcinoma Treatment Market

Cholangiocarcinoma Treatment Market Size, Share and Growth Forecast, 2026 - 2033

Cholangiocarcinoma Treatment Market by Product Type (Gemcitabine, Cisplatin, Capecitabine, Oxaliplatin), Treatment Type (Drug Therapy, Radiation Therapy, Surgery), Applications (Intrahepatic Cholangiocarcinoma(iCCA), Extrahepatic Cholangiocarcinoma), and Regional Analysis for 2026 - 2033

Cholangiocarcinoma Treatment Market Share and Trends Analysis

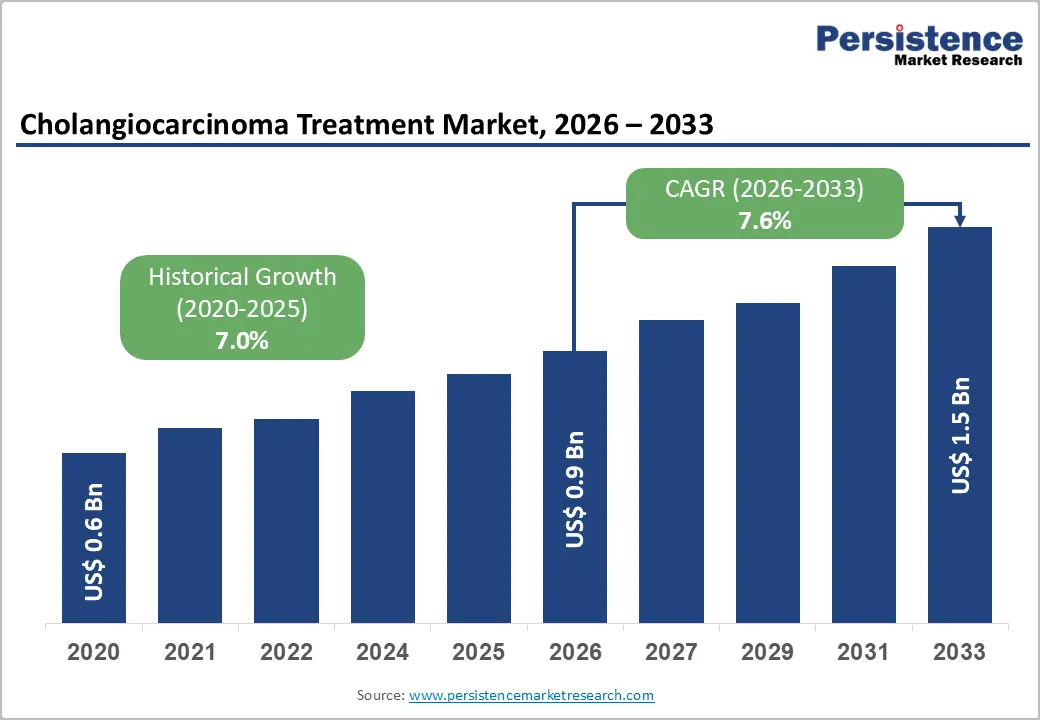

The global cholangiocarcinoma treatment market size is likely to be valued at US$ 0.9 billion in 2026 and is projected to reach US$ 1.5 billion by 2033, growing at a CAGR of 7.6% during the forecast period 2026 - 2033.

The market is growing as oncology treatment preferences shift toward targeted and combination therapies that offer improved survival outcomes and better tolerability than traditional chemotherapy. Increasing adoption of drugs such as gemcitabine-based regimens reflects demand for clinically validated, evidence-based care.

Growth in end-use applications, particularly for intrahepatic cholangiocarcinoma, is driven by rising incidence and expanded diagnostic capabilities. Additionally, urbanization and rising healthcare expenditure in emerging markets are improving access to cancer care infrastructure, enabling earlier diagnosis and greater treatment uptake, thereby directly supporting sustained market expansion.

Key Industry Highlights

- Leading Treatment Segment: Drug therapy is set to command around 68% of the revenue share in 2026, while radiation therapy is likely to grow the fastest at 8.1% CAGR through 2033, supported by technological advancements in precision treatment.

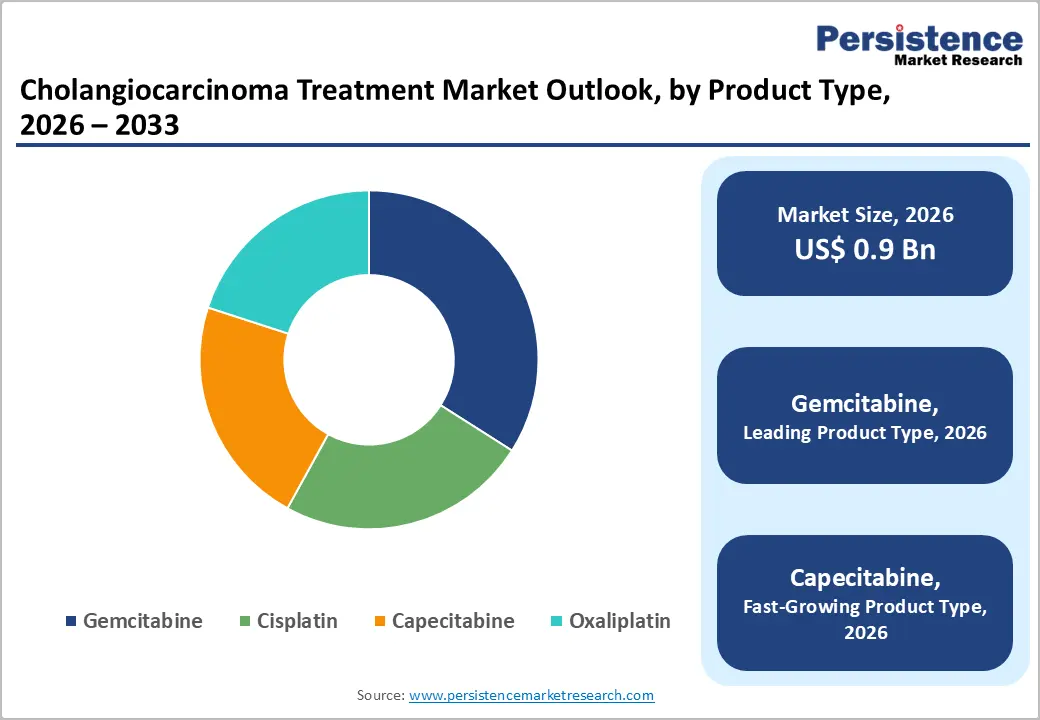

- Product Type Trends: Gemcitabine is set to command approximately 34% of the revenue share in 2026, while capecitabine is likely to grow the fastest, with a 8.4% CAGR through 2033, driven by its oral administration and increasing use in adjuvant therapy.

- Application Insights: Intrahepatic cholangiocarcinoma (iCCA) is set to command around 62.0% of the revenue share in 2026, while extrahepatic cholangiocarcinoma is likely to grow the fastest at 7.9% CAGR through 2033, supported by improved diagnostic rates.

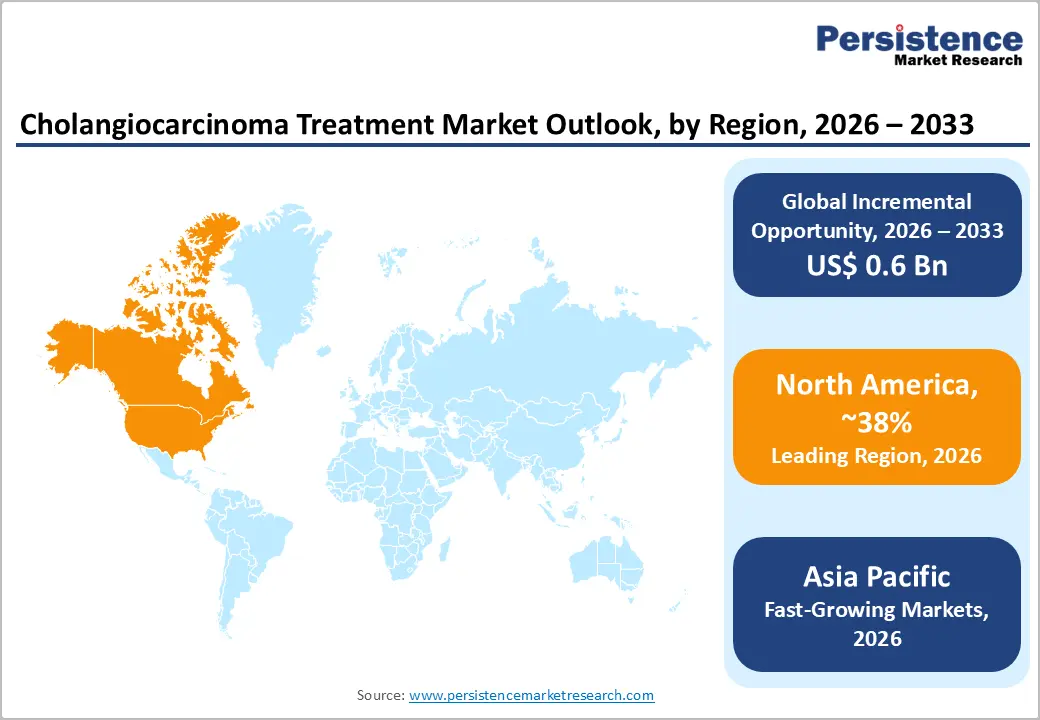

- Regional Leadership: North America is set to command around 38.0% of the revenue share in 2026, while Asia Pacific is likely to grow the fastest at 8.6% CAGR through 2033, driven by rising disease prevalence and expanding healthcare infrastructure.

- Competitive Environment: Market competition is set to intensify, with targeted therapy approvals and strategic collaborations likely to drive innovation-led growth and pipeline expansion through 2033.

| Key Insights | Details |

|---|---|

| Cholangiocarcinoma Treatment Market Size (2026E) | US$ 0.9 Bn |

| Market Value Forecast (2033F) | US$ 1.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.0% |

DRO Analysis

Driver - Rising Disease Burden and Late-Stage Diagnosis Driving Treatment Demand

Cholangiocarcinoma incidence has been increasing globally, with data from international cancer registries such as GLOBOCAN indicating a higher prevalence in Asia and Western countries. Studies published by global oncology societies report that over 60-70% of cases are diagnosed at advanced stages, limiting curative options and increasing reliance on systemic therapies. This epidemiological trend directly drives demand for chemotherapy drugs such as gemcitabine and cisplatin, which remain first-line treatments. The growing disease burden creates sustained demand for cholangiocarcinoma treatment drugs, reinforcing long-term market growth and investment in oncology pipelines.

Recent global estimates indicate that approximately 210,000 new cholangiocarcinoma cases are diagnosed annually, highlighting a steadily expanding patient pool. Additionally, clinical evidence confirms that only 20-30% of patients are eligible for curative surgery, reinforcing reliance on drug-based and palliative treatments. This imbalance between diagnosis and curative eligibility significantly increases long-term therapy demand. As awareness improves and diagnostic capabilities expand, more patients are entering treatment pathways, directly supporting higher therapy utilization rates and strengthening the commercial outlook of cholangiocarcinoma therapeutics globally.

Advancements in Drug Therapies and Expanding Oncology Infrastructure

The oncology sector has witnessed rapid innovation, with regulatory bodies such as the U.S. FDA and EMA approving targeted therapies and immunotherapies for biliary tract cancers. Clinical trial data from oncology research institutions show improved survival when combining gemcitabine with cisplatin, a regimen that has become a standard of care. Furthermore, biomarker-driven therapies are gaining traction, enhancing treatment personalization. These advancements are increasing the adoption of drug therapy as the dominant treatment modality, strengthening the cholangiocarcinoma therapeutics market through higher treatment efficacy and improved patient outcomes.

Scientific consensus published in 2025 highlights that combination regimens integrating chemotherapy with immune checkpoint inhibitors are now the standard of care for advanced cases, reflecting a shift toward more effective multi-modal treatments. In parallel, over 50+ companies and 60+ drug candidates are currently in development pipelines, indicating strong innovation momentum and sustained R&D investment. Healthcare infrastructure improvements, particularly in emerging economies, further amplify these advancements by expanding access to treatment. Together, innovation and infrastructure growth are accelerating patient access, improving outcomes, and driving long-term expansion of the global cholangiocarcinoma treatment market.

Restraints - High Treatment Costs and Limited Accessibility across Healthcare Systems

Cholangiocarcinoma treatment involves expensive chemotherapy regimens, surgical procedures, and supportive care. Reports from global health organizations indicate that oncology treatment costs can exceed $10,000 per patient annually, particularly in developed markets. In low- and middle-income countries, limited insurance coverage and out-of-pocket expenditure restrict access to advanced therapies. This creates a significant affordability barrier, reducing treatment penetration and slowing overall market expansion for cholangiocarcinoma therapies. The high cost burden also discourages timely treatment initiation among economically vulnerable populations.

Recent data from the American Cancer Society highlights that cancer-related costs exceeded US$21 billion in patient burden, with many oncology drugs priced above US$100,000 annually, intensifying affordability concerns. Additionally, health policy analyses published in 2025 indicate that new cancer therapies are significantly increasing healthcare system expenditure, placing pressure on reimbursement frameworks. These cost dynamics are limiting access to innovative treatments, particularly in emerging markets, and slowing the adoption of advanced cholangiocarcinoma therapies despite clinical benefits. This widening cost-access gap continues to challenge equitable distribution of treatment across regions.

Complex Diagnosis and Low Early Detection Rates Limiting Treatment Eligibility

Cholangiocarcinoma is often asymptomatic in early stages, leading to delayed diagnosis. Clinical studies suggest that early-stage detection rates remain below 30% globally, limiting the use of curative surgical interventions. Diagnostic challenges, including a lack of standardized screening protocols and reliance on imaging and biopsy, contribute to treatment delays. This structural limitation reduces the eligible patient pool for certain therapies, impacting revenue potential across multiple treatment segments in the cholangiocarcinoma market. The absence of early warning symptoms further complicates timely clinical intervention.

Recent clinical literature published in 2025 emphasizes that cholangiocarcinoma remains a highly heterogeneous and difficult-to-diagnose cancer, with a poor prognosis largely due to delayed detection and a lack of routine screening programs. Furthermore, healthcare system reports in Europe highlight persistent disparities in access to advanced diagnostics and molecular testing, limiting early identification of eligible patients for targeted therapies.

These systemic gaps in diagnostic infrastructure continue to delay treatment initiation and restrict the effective use of emerging therapies, thereby constraining overall market growth potential. This diagnostic complexity continues to pose a significant barrier to improving patient outcomes globally.

Opportunities - Expansion in Emerging Markets and Untapped Patient Populations

Emerging economies in Asia-Pacific, Latin America, and the Middle East offer significant growth opportunities driven by rising cancer incidence and improving healthcare systems. According to global health expenditure data, oncology spending in these regions is increasing faster than in developed markets. Expanding insurance coverage and government-funded cancer programs are enabling access to treatment for cholangiocarcinoma. These markets represent a large, previously underserved patient population, potentially contributing a substantial share to future market revenues. The improving affordability of essential cancer therapies is further supporting the adoption of treatment across these regions.

Recent public health initiatives in 2025-2026 further reinforce this opportunity, with governments in Asia expanding national cancer programs to improve early diagnosis and access to treatment. In parallel, leading cancer centers are expanding access to clinical trials in emerging regions, thereby improving patient inclusion in advanced therapies. For instance, ongoing clinical programs in 2026 are actively evaluating perioperative chemotherapy and targeted treatments, improving treatment accessibility beyond developed markets. These developments are accelerating treatment penetration, strengthening healthcare delivery systems, and unlocking long-term commercial potential in high-growth regions.

Advancements in Precision Medicine and Expanding Oncology Research Investments

Advances in genomics and molecular diagnostics are enabling the development of precision oncology treatments for cholangiocarcinoma. Research institutions and pharmaceutical companies are focusing on targeted therapies based on genetic mutations such as FGFR2 and IDH1. Clinical trials demonstrate improved outcomes in selected patient groups, supporting regulatory approvals. This shift toward personalized medicine creates opportunities for premium-priced therapies and expands the cholangiocarcinoma drug development pipeline, enhancing long-term market value. The growing role of biomarker testing is also improving patient stratification and treatment effectiveness.

Industry and regulatory developments in 2025-2026 strongly validate this trend, with the U.S. FDA granting breakthrough therapy designation to zenocutuzumab for NRG1-positive cholangiocarcinoma, highlighting the clinical potential of targeted therapies. Additionally, the FDA has approved combination regimens such as pembrolizumab with chemotherapy, reinforcing the shift toward precision-driven and multi-modal treatment approaches. Further momentum is evident with the FDA granting priority review to lirafugratinib in 2026, accelerating access to next-generation FGFR-targeted therapies. These advancements, combined with rising global R&D investments, are rapidly transforming the treatment landscape and creating high-value growth opportunities across the cholangiocarcinoma treatment market.

Category-wise Analysis

Product Type Insights

Gemcitabine is expected to remain the leading segment, accounting for approximately 34% of the market share in 2026, driven by its widespread use as a first-line chemotherapy agent in combination regimens. Clinical guidelines consistently position gemcitabine, particularly in combination with cisplatin, as the standard of care for advanced cholangiocarcinoma, supported by strong survival and disease-control outcomes. Its established clinical profile and extensive real-world usage ensure consistent demand across healthcare settings globally.

In 2025, updated oncology guidance incorporated gemcitabine-based chemo-immunotherapy combinations into frontline treatment pathways, reinforcing its central role. Clinical evidence presented during the year highlighted improved outcomes with checkpoint inhibitor combinations, accelerating adoption across hospitals and cancer centers. Additionally, continued bulk procurement by public healthcare systems, driven by its cost-effectiveness, further confirms its sustained clinical and commercial leadership.

Capecitabine is projected to be the fastest-growing segment, expanding at a CAGR of 8.4% through 2033, supported by its oral administration and increasing use in adjuvant therapy. Its convenience enables outpatient-based treatment, reducing hospital dependency and overall care costs while improving patient compliance. The drug’s favorable safety profile and suitability for long-term therapy enhance its adoption across diverse patient groups. In 2025, updated clinical guidelines in major markets reinforced its role as a standard adjuvant therapy following surgical resection. Healthcare systems also expanded oral chemotherapy programs to support decentralized cancer care delivery. Real-world evidence demonstrating higher adherence rates with oral regimens continues to accelerate its uptake globally.

Treatment Type Insights

Drug therapy is poised to dominate for an estimated 68% share in 2026, due to its applicability across all disease stages and its role as the primary treatment approach. Chemotherapy remains the backbone, increasingly supported by targeted therapies and immunotherapies that improve clinical outcomes. Its widespread clinical validation and inclusion in standardized treatment protocols ensure consistent global adoption.

In 2026, regulatory bodies expanded approvals for combination drug therapies that integrate immunotherapy, reinforcing their role in advanced treatment settings. Clinical data released in 2025 showed improved progression-free survival with these regimens, influencing physician preferences. Increased government funding for systemic therapies further supports accessibility and sustained dominance.

Radiation therapy is anticipated to be the fastest-growing segment, with a 8.1% CAGR through 2033, driven by advancements in precision technologies such as SBRT (Stereotactic Body Radiation Therapy). These technologies enable targeted tumor treatment while minimizing damage to surrounding tissues, improving patient outcomes and safety. Its growing use as both a primary and adjunct therapy is expanding its clinical relevance.

In 2025, healthcare providers accelerated the adoption of AI-enabled radiotherapy planning systems, enhancing treatment accuracy and efficiency. Clinical studies reported improved local tumor control rates with advanced radiation techniques, strengthening physicians' confidence. Additionally, increased investment in radiotherapy infrastructure is supporting broader accessibility and driving segment growth.

Regional Analysis

North America Cholangiocarcinoma Treatment Market Trends

North America is expected to continue to lead the cholangiocarcinoma treatment market, contributing nearly 38% of global revenue in 2026, with the United States at the center of this dominance. The region’s strength comes from a combination of advanced oncology infrastructure, high per-patient spending, and a regulatory environment that enables faster adoption of new therapies. Patients benefit from early access to innovative drugs, supported by structured reimbursement systems and well-established cancer care networks. This ecosystem ensures that even complex treatments are widely available, reinforcing consistent demand across both hospital and specialty care settings.

Momentum in past years has been driven by a clear push toward innovation and precision medicine. Federal funding programs have expanded support for cancer research, while regulatory bodies have accelerated review timelines for oncology drugs. At the same time, leading cancer centers have deepened their focus on cholangiocarcinoma through dedicated clinical trials and translational research. A notable shift has been the growing understanding of tumor biology, with recent studies uncovering new interactions within the tumor microenvironment, opening pathways for more effective immunotherapy approaches. This combination of policy support and scientific progress continues to anchor North America’s leadership.

Europe Cholangiocarcinoma Treatment Market Trends

Europe holds a solid position in the global market, supported by its structured healthcare systems and strong regulatory coordination. Countries such as Germany, the U.K., France, and Spain play a central role, offering broad access to cancer care through publicly funded systems. The region benefits from streamlined approval processes under a unified regulatory framework, allowing new therapies to reach multiple markets efficiently. Consistent adoption of standardized treatment protocols also ensures a relatively uniform quality of care across countries, supporting stable demand patterns.

What stands out in Europe is its research-driven approach to oncology. In 2025, several countries expanded investments in genomic medicine, integrating molecular testing more deeply into routine cancer care. This has improved the identification of patients eligible for targeted therapies. Collaborative research initiatives across European institutions have led to new findings around genetic markers linked to cholangiocarcinoma progression, helping refine both diagnosis and treatment strategies. Combined with ongoing upgrades in diagnostic infrastructure and cross-border clinical trials, these efforts are gradually strengthening the region’s role as an innovation-focused market.

Asia Pacific Cholangiocarcinoma Treatment Market

Asia Pacific is projected to be the fastest-growing region, with a CAGR of 8.6% through 2033, driven by rising disease burden and rapid healthcare transformation. Large populations in countries such as China, India, and Japan are driving higher case volumes, particularly for intrahepatic cholangiocarcinoma. At the same time, expanding healthcare access is bringing more patients into the formal treatment system. Improvements in insurance coverage, urban healthcare infrastructure, and awareness are all contributing to higher diagnosis and treatment rates, making the region a major growth engine.

Recent developments highlight how quickly the landscape is evolving. Governments across the region have increased oncology budgets and are actively scaling up cancer treatment capacity. Japan has streamlined approval pathways for innovative therapies, while China and India are investing in both infrastructure and local drug manufacturing. Alongside these systemic changes, researchers in the region have identified stronger correlations between chronic liver conditions and cholangiocarcinoma risk, which could significantly improve early detection strategies. With rising clinical trial activity and growing industry participation, the Asia Pacific is not just expanding; it is becoming increasingly influential in shaping future treatment approaches.

Competitive Landscape

The global cholangiocarcinoma treatment market is moderately fragmented, with leading players such as Roche, AstraZeneca, Merck & Co., and Bristol-Myers Squibb accounting for a notable revenue share. These companies leverage strong oncology pipelines, extensive clinical trial networks, and regulatory expertise to sustain their positions. Their focus remains on targeted therapies, immuno-oncology, and combination regimens, supported by continuous R&D investments. Strategic collaborations and accelerated approvals further strengthen their competitive advantage.

The emerging biotech firms and mid-sized players, such as Incyte and Exelixis, are targeting niche indications through precision medicine approaches. High entry barriers, including complex clinical trials and stringent regulations, limit new participants. However, biomarker-driven innovation is enabling smaller firms to enter specialized segments. The market is witnessing increasing partnerships, licensing deals, and acquisitions , intensifying competition and driving innovation.

Key Industry Developments:

- In January 2026, Lilly expanded a US$ 2.75B+ Insilico Medicine deal alongside collaborations with Innovent, Indupro, and NVIDIA to accelerate AI-based drug discovery and biomarker-driven therapies. This strengthens precision oncology capabilities, enabling faster development of targeted treatments for complex cancers, including cholangiocarcinoma.

- In August 2024, Merck & Co. & Daiichi Sankyo advanced their US$ 22B oncology partnership focused on antibody-drug conjugates across multiple solid tumors.

This enhances targeted therapy innovation, with potential application in biliary tract cancers and next-generation treatment approaches.

Companies Covered in Cholangiocarcinoma Treatment Market

- F. Hoffmann-La Roche Ltd.

- Pfizer Inc.

- Novartis AG

- Merck & Co., Inc.

- Bristol-Myers Squibb Company

- AstraZeneca PLC

- Eli Lilly and Company

- Sanofi S.A.

- Bayer AG

- Amgen Inc.

- Incyte Corporation

- Exelixis, Inc.

- Ipsen Group

Frequently Asked Questions

The global cholangiocarcinoma treatment market is projected to reach US$ 0.9 billion in 2026.

Rising disease incidence, increasing adoption of combination therapies, and advancements in targeted oncology treatments are driving the market.

The cholangiocarcinoma treatment market is expected to grow at a CAGR of 7.6% from 2026 to 2033.

Expanding access in emerging markets and advancements in precision medicine are creating significant growth opportunities.

F. Hoffmann-La Roche Ltd., AstraZeneca PLC, Merck & Co., and Bristol-Myers Squibb are key players.