- Pharmaceuticals

- Cachexia Treatment Market

Cachexia Treatment Market Size, Share, and Growth Forecast, 2026 - 2033

Cachexia Treatment Market by Therapy Type (Pharmacological Therapy, Others), Application (Cancer, Chronic Obstructive Pulmonary Disease (COPD), Others), End-user (Hospitals, Specialty Clinics, Home Care Settings, Others), and Regional Analysis for 2026 - 2033

Cachexia Treatment Market Size and Trends Analysis

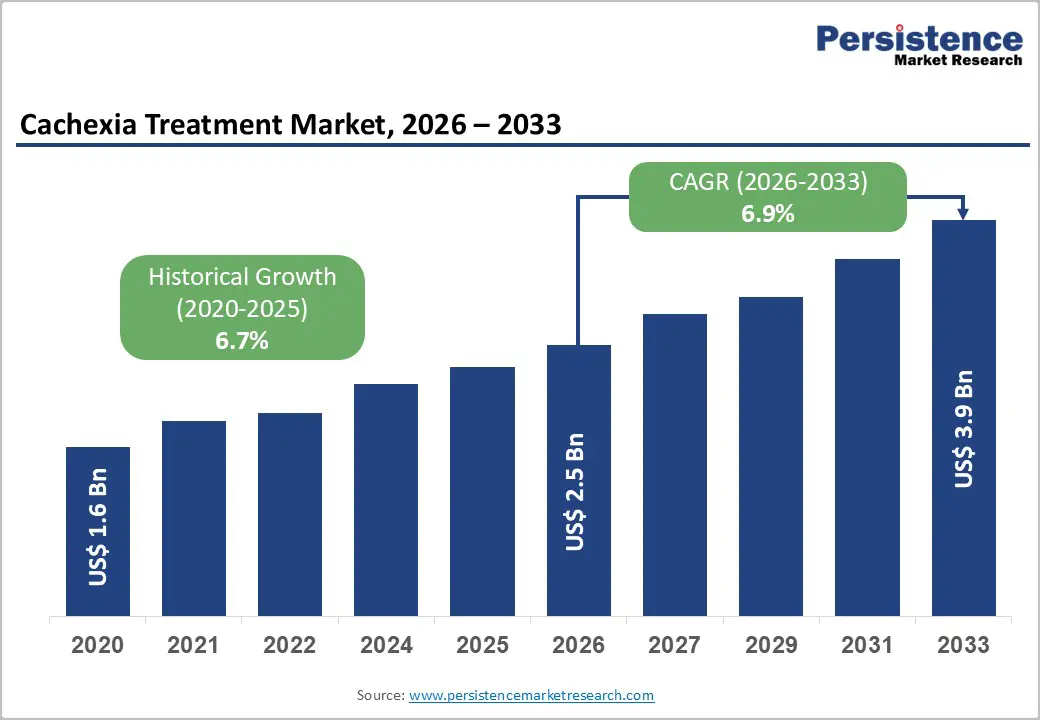

The global cachexia treatment market size is likely to be valued at US$2.5 billion in 2026, and is expected to reach US$3.9 billion by 2033, growing at a CAGR of 6.9% during the forecast period from 2026 to 2033, driven by the increasing clinical recognition of Cachexia, a complex metabolic disorder characterized by involuntary weight loss, skeletal muscle wasting, fatigue, and progressive functional decline.

Unlike simple malnutrition, cachexia is caused by a combination of systemic inflammation, metabolic imbalances, and neurohormonal changes, making it resistant to standard nutritional interventions. The condition is most commonly associated with chronic and advanced diseases such as Cancer, Chronic Obstructive Pulmonary Disease, Congestive Heart Failure, and Chronic Kidney Disease.

The treatment landscape for cachexia includes a combination of pharmacological therapies, such as corticosteroids, progestins, anabolic agents, and ghrelin receptor agonists, alongside nutritional interventions, structured exercise programs, and multimodal treatment strategies. Increasing awareness among healthcare professionals, particularly oncologists, pulmonologists, and nephrologists, regarding the importance of early diagnosis and timely intervention is contributing to the expansion of the overall patient treatment base.

Key Industry Highlights:

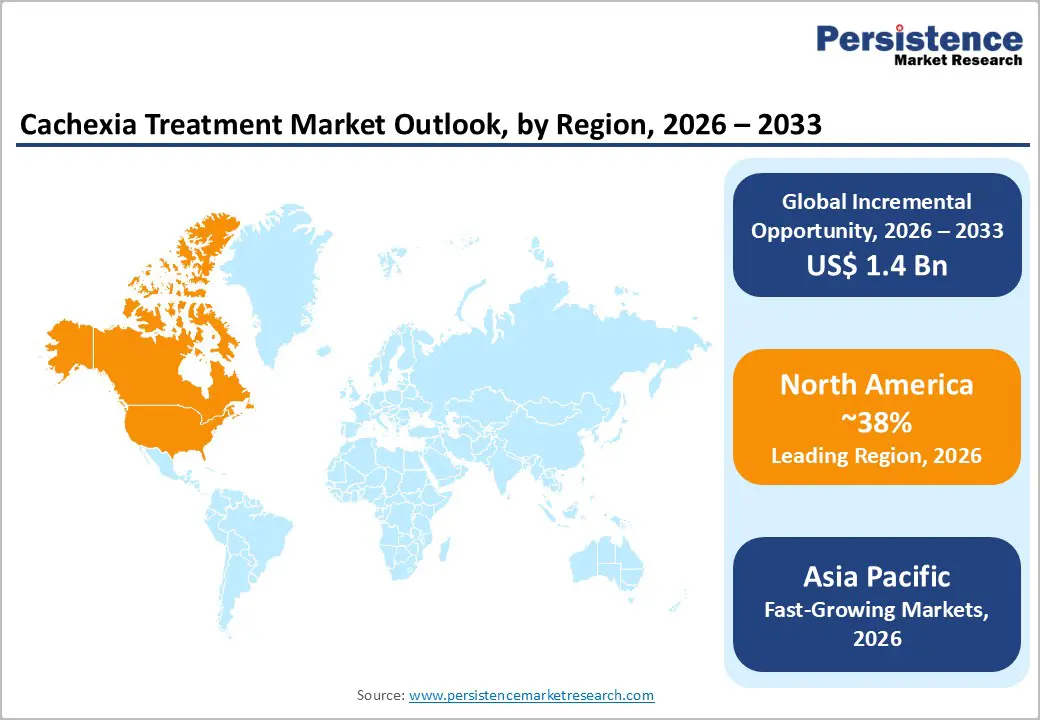

- Leading Region: North America, anticipated to account for a 38% market share in 2026, underpinned by strong healthcare infrastructure, high R&D investments, and early diagnosis rates exceeding 60% in oncology settings.

- Fastest-growing Region: Asia Pacific, supported by expanding pharmaceutical manufacturing hubs, rising chronic disease burden, and increasing government healthcare expenditure.

- Dominant Therapy Type: Pharmacological therapy, to hold approximately 70% of the market share, owing to robust drug approval activities and clinical pipeline momentum.

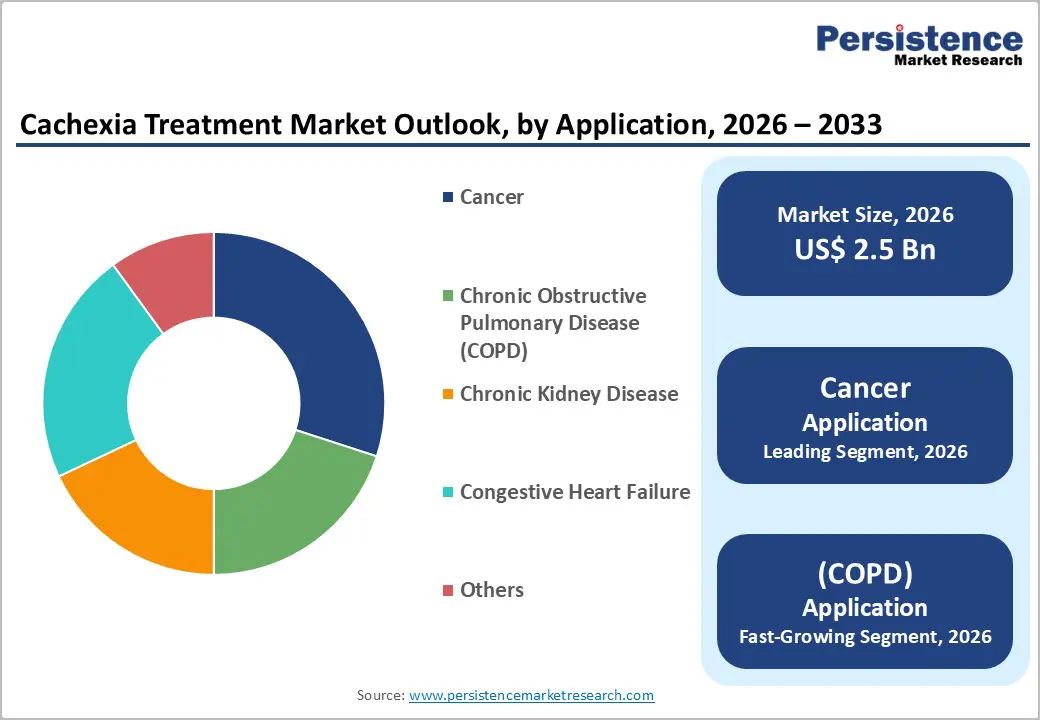

- Leading Application: Cancer is anticipated to lead with over 30% of advanced cancer patients developing clinically significant cachexia, directly driving prescription volumes.

| Key Insights | Details |

|---|---|

| Cachexia Treatment Market Size (2026E) | US$2.5 Bn |

| Market Value Forecast (2033F) | US$3.9 Bn |

| Projected Growth CAGR (2026 - 2033) | 6.9% |

| Historical Market Growth (2020 - 2025) | 6.7% |

DRO Analysis

Driver - Rising Global Cancer Burden and Cachexia Prevalence

Cancer-associated cachexia is the single largest indication driving treatment demand, affecting approximately 50-80% of advanced-stage cancer patients, depending on the tumor type. According to the World Health Organization, global cancer incidence exceeded 20 million new cases in 2022 and is projected to surpass 26 million by 2030. Gastrointestinal cancers, including pancreatic, gastric, and colorectal, demonstrate the highest cachexia prevalence rates, exceeding 80% in pancreatic cancer patients. This translates directly into expanding prescription volumes for appetite stimulants, anabolic steroids, and anti-inflammatory agents.

Clinical data consistently demonstrate that cachexia is responsible for approximately 20-30% of all cancer-related deaths, not from the primary malignancy itself but from metabolic and muscular failure. This alarming fatality contribution has prompted global oncology treatment guidelines to formally incorporate cachexia screening and intervention as part of standard cancer care pathways. In the U.S. alone, the National Cancer Institute estimates over 1.9 million new cancer cases annually, of which a substantial proportion will develop clinically significant cachexia requiring therapeutic intervention.

Expanding Pharmaceutical Pipeline and Novel Therapeutic Approvals

The cachexia treatment pipeline has witnessed a significant surge in clinical activity over the past decade, with multiple investigational agents targeting novel molecular pathways now progressing through Phase II and Phase III trials. Key therapeutic mechanisms under investigation include selective androgen receptor modulators (SARMs), myostatin inhibitors, IL-6 pathway antagonists, ghrelin receptor agonists, and beta-2 adrenergic agonists. Regulatory agencies in the U.S. and Europe have granted Fast Track and Orphan Drug designations to several cachexia candidates, shortening development timelines and reducing approval costs.

The commercialization of anamorelin, a ghrelin receptor agonist approved in Japan for cancer cachexia, represents a landmark in the global market's evolution, validating the commercial viability of targeted cachexia pharmacotherapies. In the U.S., the FDA's evolving guidance on cachexia as a registrable indication is encouraging major pharmaceutical companies, including Pfizer Inc., Amgen Inc., and Novartis AG, to invest substantially in late-stage development programs. Increased competition among innovators is expected to yield multiple new product launches through 2030, broadening treatment choice and market revenue.

Restraint - Absence of Standardized Diagnostic Criteria and Regulatory Ambiguity

One of the most persistent obstacles limiting the market's growth trajectory is the lack of universally accepted and clinically standardized diagnostic criteria. While the 2011 international consensus definition established weight-loss thresholds and benchmarks for inflammatory biomarkers, practical application across diverse clinical settings remains inconsistent. Many healthcare institutions, particularly in emerging markets, lack the validated biomarker assessment tools, such as serum C-reactive protein, IL-6 quantification, or dual-energy X-ray absorptiometry (DEXA) scanning, needed to rigorously diagnose and stage cachexia. This diagnostic gap results in underdiagnosis, delayed treatment initiation, and a smaller pool of patients eligible for clinical trial enrollment, ultimately constraining pharmaceutical revenues.

Regulatory agencies such as the U.S. FDA and the European Medicines Agency (EMA) have not yet established definitive surrogate endpoints for the approval of cachexia drugs, making it challenging for sponsors to design and power registration trials. Without consensus on whether primary endpoints should reflect body weight gain, lean body mass accretion, improvements in physical function, or quality-of-life metrics, clinical development programs face a heightened risk of trial failure despite biologically active compounds. This ambiguity increases time-to-market, inflates R&D costs, and discourages smaller biopharmaceutical firms from entering the space.

High Cost of Novel Therapies and Reimbursement Challenges

Advanced pharmacological interventions for cachexia, particularly biologics, SARMs, and recombinant hormone analogs, carry substantial list prices that create significant access barriers in cost-sensitive healthcare systems. In markets without robust orphan disease reimbursement frameworks, payers frequently categorize cachexia treatments as supportive care rather than disease-modifying therapies, limiting insurance coverage and out-of-pocket affordability.

Even in high-income markets such as the U.S. and Germany, formulary inclusion for newer cachexia agents often requires extensive health technology assessments, resulting in 12-24 months of time delays post-approval before commercial prescriptions can be generated at scale. These reimbursement challenges suppress market penetration and constrain the revenue potential of novel therapeutics.

Opportunity - Combination Therapy Protocols Unlocking Multimodal Treatment Paradigms

Emerging clinical evidence underscores the transformative potential of multimodal combination approaches for cachexia management, which markedly outperform traditional single-agent therapies. Recent phase III trials, including those involving advanced cancer patients, have shown that integrating pharmacological agents such as selective androgen receptor modulators (SARMs), such as enobosarm, or ghrelin mimetics, such as anamorelin, with structured exercise regimens and high-protein nutritional supplementation yields superior clinical outcomes.

This evidence-driven shift is reshaping the market, fostering commercial opportunities for pharmaceutical innovators. Companies are pivoting toward co-packaged therapeutic bundles, pre-formulated kits combining anti-cachectic drugs, oral nutritional supplements (ONS), and exercise protocols tailored to patient profiles (e.g., cancer vs. COPD). Partnerships with nutraceutical firms, such as those between AstraZeneca and specialized ONS providers, enable integrated care programs delivered via telehealth platforms, ensuring adherence and real-time monitoring. Ancillary models include subscription-based cachexia management kits (e.g., quarterly deliveries with app-guided workouts) and hospital-partnered protocols, projected to add US$ 300-400 Mn in value. Reimbursement tailwinds, with CMS and EU payers recognizing the efficacy of multimodal approaches, further accelerate adoption.

Untapped Market Potential in Non-Cancer Indications

While cancer-associated cachexia dominates current treatment revenues in the market, the non-oncology cachexia addressable market, spanning COPD, congestive heart failure (CHF), and chronic kidney disease (CKD), presents a substantially underpenetrated commercial opportunity. COPD patients worldwide suffer from this debilitating condition, where cachexia manifests in severe cases as progressive muscle wasting that worsens respiratory function and daily mobility. Dedicated pharmacological treatments for this population remain extremely limited, relying heavily on off-label options and supportive care, leaving a vast untapped potential for targeted interventions that address underlying inflammatory and metabolic drivers.

Cardiac cachexia in heart failure patients accelerates disease progression through sarcopenia and weakened cardiac performance, amplifying overall health decline. In CKD, cachexia compounds challenges in dialysis-dependent individuals by promoting frailty and treatment resistance. These non-oncology indications share overlapping pathophysiological mechanisms with cancer cachexia, such as chronic inflammation and protein catabolism, making them prime candidates for therapeutic extensions from existing oncology pipelines. Regulatory approval for these broader indications would dramatically expand the addressable patient pool, enabling label expansions that transform single-indication drugs into versatile platforms. Pharmaceutical innovators such as Bristol-Myers Squibb, AbbVie Inc., and Boehringer Ingelheim are actively exploring these extensions through dedicated clinical programs.

Segmental Insights

Therapy Type Insights

Pharmacological therapy is anticipated to dominate with over 70% of the share in 2026. This segment encompasses corticosteroids (dexamethasone, methylprednisolone), progestins (megestrol acetate, medroxyprogesterone acetate), anabolic agents (oxandrolone, nandrolone), and next-generation molecular therapies including ghrelin receptor agonists and myostatin inhibitors. The introduction of novel agents such as anamorelin in select markets is progressively shifting the pharmacological therapy landscape toward more mechanism-specific, targeted interventions with improved safety profiles. Megestrol acetate, a commonly used progestin for managing cancer cachexia, is marketed under the brand Megace® by Bristol Myers Squibb. It remains a foundational therapy due to its well-established effectiveness in enhancing appetite and promoting weight gain in cancer patients, combined with its affordability and widespread acceptance across oncology settings.

The nutritional therapy segment is likely to be the fastest-growing, due to the rising emphasis on early and comprehensive management of cachexia. Increasing clinical evidence highlights that timely nutritional intervention helps preserve muscle mass, improve treatment tolerance, and enhance quality of life in patients. Healthcare providers are increasingly adopting oral nutritional supplements, high-protein diets, and specialized formulations as part of standard care. Guidelines from organizations such as the European Society for Clinical Nutrition and Metabolism further promote structured nutrition plans. Ensure®, developed by Abbott Laboratories, is commonly used in cancer patients to help manage weight loss and muscle wasting associated with cachexia, offering high-calorie, protein-rich nutritional support to improve overall nutritional status.

Application Insights

Cancer is projected to dominate, accounting for 30% of the share in 2026. The mechanistic intersection of tumor-derived inflammatory cytokines (TNF-α, IL-6, IL-1β), altered lipid metabolism, hypermetabolism, and anorexia creates a profound and clinically distinct cachexia phenotype in cancer patients that is both more severe and more clinically visible than in other chronic disease contexts. Pancreatic, gastric, esophageal, lung, and colorectal cancers carry the highest cachexia prevalence rates and together constitute a substantial portion of global cancer mortality. Anamorelin, developed by Helsinn Group, is specifically indicated for managing cancer cachexia in patients with non-small cell lung cancer (NSCLC). Clinical studies have shown that it effectively enhances appetite and increases body weight in cancer patients, underscoring the strong clinical emphasis on treating cancer-associated cachexia.

Chronic obstructive pulmonary disease (COPD) is expected to be the fastest-growing application, due to its increasing global prevalence and growing clinical recognition of COPD-related muscle wasting. Progressive airflow limitation and chronic inflammation in COPD patients often lead to significant weight loss and reduced muscle mass, contributing to cachexia development. Improved diagnostic rates and longer patient survival are increasing the number of patients requiring long-term supportive care. Rising awareness among healthcare providers about early nutritional intervention, combined with the integration of pharmacological and rehabilitative therapies, is driving greater adoption of comprehensive cachexia management in COPD patients. A pilot study conducted by the National Cardiovascular Center, Japan, found that ghrelin therapy in COPD-related cachexia significantly improved appetite, promoted weight gain, and enhanced muscle strength over a 3-week treatment period. These findings highlight the increasing clinical emphasis on managing muscle wasting in COPD patients through targeted pharmacological approaches.

Regional Insights

North America Cachexia Treatment Market Trends

North America is projected to dominate, capturing the 38% of revenue in 2026, underpinned by an advanced healthcare infrastructure, high per-capita pharmaceutical expenditure, and a sophisticated oncology ecosystem. The U.S. accounts for the dominant share of North American revenue, driven by the nation's large cancer patient population, with the American Cancer Society estimating approximately 1.95 million new cancer diagnoses in 2023, of which a clinically significant proportion develops cachexia requiring therapeutic management.

FDA regulatory activity around cachexia has intensified, with multiple investigational agents receiving Orphan Drug Designation and Fast Track status, signaling growing institutional recognition of cachexia as a distinct and serious clinical condition. Leading U.S.-headquartered pharmaceutical companies, including Pfizer Inc., Amgen Inc., Bristol-Myers Squibb, Eli Lilly, and AbbVie, maintain active cachexia drug development programs, reinforcing North America's position as both the primary revenue generator and the most active innovation hub in the global market.

Europe Cachexia Treatment Market Trends

Europe is supported by a well-established palliative care infrastructure, proactive clinical guidelines from ESPEN and the European Association for Palliative Care (EAPC), and growing awareness of cachexia's impact on treatment outcomes across oncology and cardiology. France represents the second-largest European cachexia treatment market, driven by a centralized national oncology program (INCA), strong academic-industry collaboration, and government-mandated nutritional screening protocols in cancer care settings.

Germany leads in terms of revenue, supported by a large oncology patient population and a strong healthcare infrastructure. According to the Robert Koch Institute, the country records approximately 510,000 new cancer cases annually, significantly contributing to cachexia incidence and treatment demand. Leading institutions such as Charité Universitätsmedizin Berlin and the German Cancer Research Center play a key role in advancing translational research and enabling early adoption of innovative therapies. Germany’s statutory health insurance system (GKV) ensures broad reimbursement coverage for approved pharmacological therapies and medical nutrition products, driving high treatment penetration.

Asia Pacific Cachexia Treatment Market Trends

Asia Pacific is likely to be the fastest-growing regional market for cachexia treatment, advancing at the highest regional CAGR during the forecast period. The region's growth trajectory is driven by escalating cancer incidence across China, India, Japan, and South Korea; improving healthcare infrastructure; expanding pharmaceutical manufacturing capabilities; and rising government investments in cancer care and palliative medicine. China and Japan collectively account for the largest share of Asia Pacific cachexia treatment revenues.

Japan holds a unique position as the first country globally to approve anamorelin (Adlumiz) for cancer cachexia, establishing a regulated commercial market for ghrelin receptor agonist therapy. Japan's rapidly aging population, with over 30% of citizens aged 65 or above, generates disproportionately high cancer and cachexia prevalence, creating sustained prescription demand. India represents a high-potential emerging market, characterized by a large and rapidly growing cancer burden, an expanding middle-income segment with improved healthcare access, and government initiatives, such as the National Cancer Grid, that promote standardized cancer care.

Competitive Landscape

The global cachexia treatment market is moderately competitive, with pharmaceutical companies focusing on novel pharmacological agents and supportive care solutions. Leading companies, including Pfizer Inc., Amgen Inc., and Novartis AG, are aggressively advancing cachexia-specific or dual-indication (sarcopenia-cachexia) candidates through Phase II and Phase III development. The primary strategic goal is to achieve the first U.S. FDA approval for a cachexia-specific pharmacotherapy, a regulatory milestone that would confer substantial first-mover commercial advantage and establish category leadership. Pipeline diversification across multiple molecular mechanisms is a deliberate risk mitigation strategy adopted by major players, reducing dependence on any single therapeutic approach.

Mid-cap and large pharmaceutical companies are increasingly pursuing licensing agreements and co-development partnerships with specialized biotech firms possessing proprietary cachexia technology platforms. Helsinn Healthcare's collaborations with regional distribution partners in Asia have been a model for market access expansion in Japan and emerging Asian markets. These collaborations enable faster geographic penetration, shared regulatory costs, and accelerated clinical program execution, all critical in a space where development timelines and capital requirements are substantial.

Key Industry Developments:

- In April 2026, Curanex Pharmaceuticals, Inc. (Nasdaq: CURX), a development-stage therapeutics company, announced that it expanded its drug development pipeline to include a new core indication in cancer cachexia. The company had previously focused on six core indications: ulcerative colitis, atopic dermatitis, COVID-19, diabetes, nonalcoholic fatty liver disease (NAFLD), and gout. With this strategic shift, Curanex actively prioritized cancer cachexia, a severe cancer-associated wasting condition characterized by progressive weight loss, muscle depletion, weakness, and declining physical function.

- In March 2026, Endevica Bio announced the spinout and launch of Kalohexis, a newly formed biotechnology company focused on advancing the clinical development of a portfolio of drug candidates targeting the melanocortin (MC) system for the treatment of metabolic disorders, including obesity and cancer cachexia. The leadership team of Endevica Bio also took charge of leading the newly established Kalohexis.

Companies Covered in Cachexia Treatment Market

- AstraZeneca

- Pfizer Inc.

- Amgen Inc.

- Merck & Co., Inc.

- Bristol-Myers Squibb Company

- Eli Lilly and Company

- Novartis AG

- GlaxoSmithKline plc

- Johnson & Johnson

- F. Hoffmann-La Roche Ltd

- Sanofi S.A.

- Teva Pharmaceutical Industries Ltd.

- AbbVie Inc.

- Boehringer Ingelheim International GmbH

- Takeda Pharmaceutical Company Limited

- Ipsen Pharma

- Helsinn Healthcare SA

Frequently Asked Questions

The global cachexia treatment market is projected to reach US$2.5 billion in 2026.

The cachexia treatment market is primarily driven by the rising prevalence of cancer and chronic illnesses associated with muscle wasting.

The cachexia treatment market is poised to witness a CAGR of 6.9% from 2026 to 2033.

Key opportunities in the cachexia treatment market include the development of novel pharmacological agents, the expansion of home care models, and growth in emerging markets with rising cancer burden.

Key players in the cachexia treatment market include Pfizer Inc., AstraZeneca, Amgen Inc., Merck & Co., Inc., and Bristol-Myers Squibb Company.