- Specialty & Fine Chemicals

- Capric Acid Market

Capric Acid Market Size, Share, and Growth Forecast, 2026 - 2033

Capric Acid Market by Grade (Industrial, Pharmaceutical, Technical, Food), Application (Food and Beverages, Pharmaceuticals, Personal Care & Cosmetics, Industrial Chemicals), Purity (>99%, 97-99%, 95-97%), and Regional Analysis for 2026 - 2033

Capric Acid Market Share and Trends Analysis

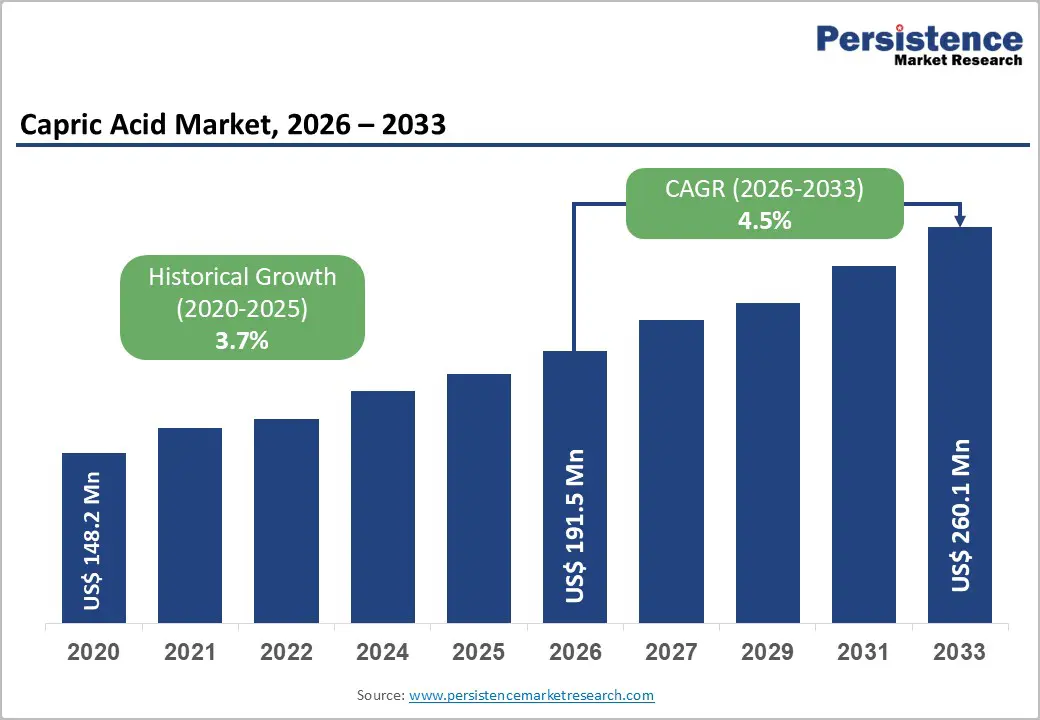

The global capric acid market size is likely to be valued at US$ 191.5 million in 2026, and is projected to reach US$ 260.1 million by 2033, growing at a CAGR of 4.5% during the forecast period 2026 - 2033.

The sustained expansion of the global capric acid market is underpinned by three primary forces: rising demand across personal care and cosmetic formulations, expanding applications in the food and pharmaceutical industries, and growing adoption of medium-chain fatty acid (MCFA) derivatives in functional nutrition. Capric acid (decanoic acid, C10:0) is a saturated medium-chain fatty acid derived predominantly from coconut and palm kernel oil, and its versatile ester chemistry has cemented its role across multiple high-value end-use sectors.

Key Industry Highlights

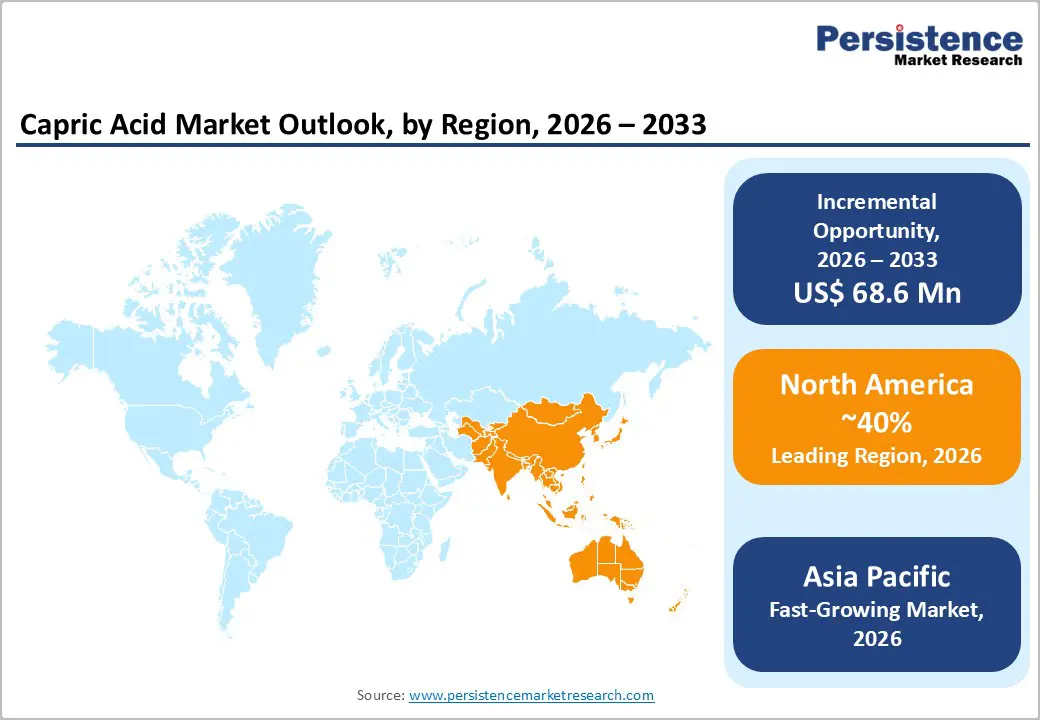

- Dominant Region & Fastest-growing Market: The Asia Pacific market is likely to lead in 2026 with about 40% share, as well as post the highest 2026 - 2033 CAGR, driven by a robust chemical manufacturing base.

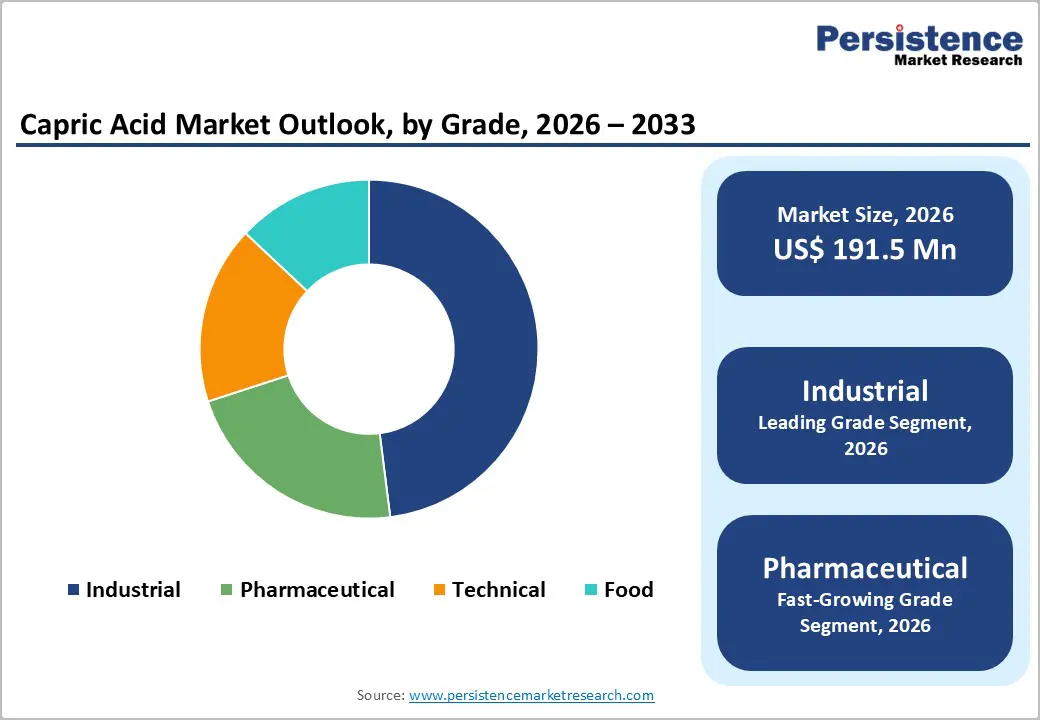

- Leading & Fastest-growing Grade: Industrial grade is slated to hold approximately 42% market revenue share in 2026, whereas pharmaceutical grade is set to be the fastest-growing through 2033.

- Leading & Fastest-growing Application: Personal care & cosmetics is poised to dominate with an estimated revenue share of 38% in 2026, while pharmaceuticals are expected to be the fastest-growing segment over the 2026 - 2033 forecast period.

- Major Driver: Medium-chain triglycerides (MCTs) that incorporate capric acid are gaining increasing clinical recognition for their benefits in ketogenic diet support, cognitive health enhancement, and anti-epileptic therapeutic protocols.

- Key Opportunity: Bio-based fatty acids emerge as essential feedstocks in green chemistry transformations, with capric acid standing out due to its natural derivation from renewable sources such as coconut and palm kernel oils.

| Key Insights | Details |

|---|---|

| Capric Acid Market Size (2026E) | US$ 191.5 Mn |

| Market Value Forecast (2033F) | US$ 260.1 Mn |

| Projected Growth (CAGR 2026 to 2033) | 4.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Surging Demand in Personal Care & Cosmetics

The global personal care and cosmetics industry is expanding rapidly as consumer demand for innovative products rises. Companies are prioritizing emollients and surfactants that enhance texture and performance in formulations such as creams and lotions. Capric acid and its triglyceride derivatives, including capric/caprylic triglycerides (CCT), serve as lightweight emollients, solubilizers, and skin-conditioning agents. Brands actively incorporate these ingredients to deliver smooth application and improved hydration without greasiness. This shift supports the creation of versatile cosmetics that meet diverse skin needs across various climates. Consumer preferences are evolving toward clean-label and naturally derived ingredients, prompting manufacturers to reformulate products away from petroleum-based options.

Bio-based medium-chain fatty acids (MCFAs), particularly those sourced from renewable materials such as coconut or palm kernel oil, are gaining prominence in this transition. The cosmetics sector has fully embraced these sustainable alternatives, fostering innovation in product lines such as serums and cleansers. Capric acid derivatives enhance stability and sensory appeal, enabling formulators to develop multifunctional products that address aging, sensitivity, and daily protection. This trend strengthens brand loyalty as shoppers seek transparency and eco-friendliness.

Expanding Functional Nutrition & Pharmaceutical Applications

Medium-chain triglycerides (MCTs) that incorporate capric acid are gaining increasing clinical recognition for their benefits in ketogenic diet support, cognitive health enhancement, and anti-epileptic therapeutic protocols. Nutritionists recommend MCTs as quick-energy sources that bypass traditional fat digestion pathways, which supports sustained mental clarity and physical endurance. Pharmaceutical developers integrate capric acid-based MCTs into formulations that target neurological conditions, ensuring rapid absorption for optimal therapeutic outcomes. This growing body of evidence strengthens their position in both wellness and medical applications. Regulatory bodies, such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA), acknowledge the safety and efficacy of MCFAs, which accelerate the adoption of pharmaceutical-grade capric acid.

Manufacturers now prioritize these ingredients in lipid-based drug delivery systems, antifungal topical agents, and nutraceutical encapsulation processes. The industry has expanded these uses significantly, creating reliable channels for incremental demand. Formulators value capric acid for its stability in capsules and emulsions, which improves bioavailability and patient compliance. This shift not only diversifies product portfolios but also aligns with precision medicine trends, where tailored lipid profiles enhance treatment precision. Suppliers benefit from heightened specifications, fostering partnerships that drive innovation in controlled-release technologies and personalized supplements.

Feedstock Price Volatility of Coconut and Palm Kernel Oil

Capric acid production relies heavily on coconut oil and palm kernel oil (PKO) as primary feedstocks. Producers face ongoing challenges from price fluctuations tied to climate disruptions and crop shortfalls in key regions such as the Philippines and Indonesia. Farmers have to contend with reduced yields due to erratic weather patterns, which tighten supply chains and raise raw material costs. Governments adjust export policies in response to domestic needs, further impacting availability. Manufacturers are actively monitoring these factors to maintain steady operations. This linkage exposes the sector to external pressures that affect planning and profitability. Small and mid-size processors bear the brunt of procurement risks, as they lack advanced hedging tools to stabilize costs.

The industry is aggressively adopting more resilient strategies, such as vertical integration and alternative feedstocks from sustainable plantations. Capric acid makers are investing in risk management practices to safeguard margins and ensure consistent output. These dynamics constrain uniform market expansion, yet they spur innovation in cost-efficient extraction methods and regional sourcing networks. Suppliers are looking to gain a competitive edge by building flexible supply agreements that prioritize traceability and ethical farming.

Regulatory Complexity in Emerging Markets

Capric acid enjoys established regulatory clearances in major markets such as the U.S., the European Union (EU), and Japan. Authorities approve the ingredient for use in food, cosmetics, and pharmaceuticals based on proven safety profiles. Manufacturers are also benefiting from streamlined processes in these regions, which support efficient production and distribution. Companies are now aligning formulations with these standards to access premium channels. This foundation has enabled global players to scale operations confidently while meeting consumer expectations for quality. However, regulatory differences persist across Southeast Asian, Latin American, and African markets, erecting barriers to commercialization.

Governments enforce a range of food contact material standards and pharmaceutical excipient approvals, complicating compliance efforts. Registration timelines are extended by bureaucratic steps, delaying product launches and increasing production costs. Industry groups, such as the American Oil Chemists' Society (AOCS) and the European Food Safety Authority (EFSA), advocate for uniform guidelines to ease these hurdles. Harmonization efforts will have advanced in select areas, yet uneven progress continues to challenge integrated supply chains. Multinational firms can adapt by localizing teams and partnering with regional experts to navigate complexities. These dynamics favor agile suppliers who invest in preemptive testing and advocacy.

Bio-Based & Sustainable Chemistry Transition

Bio-based fatty acids are essential feedstocks in green chemistry transformations, with capric acid standing out for its natural origin from renewable sources such as coconut and palm kernel oils. Governments and organizations promote these materials through policies that encourage low-carbon production methods. Companies align their operations with such initiatives to secure a competitive advantage in evolving supply chains. This positioning allows producers to meet rising demands from sectors focused on environmental responsibility. Capric acid aligns closely with regulatory frameworks, including the EU's Chemicals Strategy for Sustainability and the United States' Bioeconomy Executive Order.

Authorities prioritize the procurement of verified sustainable ingredients, which opens the door to preferential contracts and future mandates. Producers invest in certified supply chains, such as those endorsed by the Roundtable on Sustainable Palm Oil (RSPO) and Rainforest Alliance, to ensure traceability from farm to factory. Consumer goods multinationals commit to Scope 3 emission reductions, forging long-term offtake agreements that reward compliant suppliers with premium pricing. These efforts are transforming market dynamics, favoring firms that integrate sustainability into core strategies. Innovators can gain loyalty from brands seeking verified green credentials while fostering resilience against resource scarcity.

Animal Feed Antimicrobials as Antibiotic Alternatives

Rising antibiotic resistance prompts regulators and farmers to seek effective alternatives to traditional treatments in animal production. Authorities across the EU, the U.S., and ASEAN impose restrictions on antibiotic growth promoters (AGPs), which accelerates the shift toward natural solutions. Producers actively explore antimicrobial feed additives to maintain livestock health and productivity without synthetic chemicals. Capric acid-based products emerge as reliable options, offering broad-spectrum activity against common pathogens. This transition supports sustainable farming practices that prioritize animal welfare and food safety standards.

Capric acid demonstrates proven efficacy in controlling bacteria such as Clostridium perfringens and Escherichia coli (E. coli) in poultry, swine, and aquaculture systems. Formulators incorporate it into feed blends to enhance gut integrity and reduce disease incidence, which improves overall herd performance. Regulatory approvals affirm its safety profile, positioning it as a compliant substitute in diverse applications. The industry will have integrated these additives widely, creating robust demand channels for suppliers. Livestock operators stand to benefit from consistent results that lower veterinary costs and boost efficiency, while innovators can refine delivery methods, such as microencapsulation, to maximize potency and stability during feed processing.

Category-wise Analysis

Grade Insights

Industrial grade is anticipated to dominate in 2026, commanding approximately 42% of the capric acid market revenue share, driven by bulk consumption in lubricants, plasticizers, and chemical intermediates. The segment's scale advantage is reinforced by established procurement relationships with oleochemical producers in Indonesia and Malaysia, where integrated production facilities enable cost-competitive supply. Industrial-grade volumes benefit from stable, contract-based demand from downstream chemical manufacturers, providing revenue predictability despite lower unit pricing relative to specialty grades.

Pharmaceutical grade is likely to be the fastest-growing segment during the 2026-2033 forecast period. This growth trajectory reflects the escalating use of ultra-high-purity capric acid (≥99.5% assay) in GMP-compliant drug formulations, clinical MCT nutrition, and topical excipients. Stringent pharmacopeial compliance and the associated quality assurance infrastructure command significant pricing premiums, attracting specialty oleochemical producers seeking to enhance margins through value-added product portfolios.

Application Insights

Personal care & cosmetics is expected to capture an estimated 38% of the capric acid market share in 2026, due to its emollient, emulsifying, and antimicrobial qualities, which make it vital in skincare and haircare formulations. A growing number of consumers is recognizing these benefits, fueling segment expansion. Demand for organic and natural personal care products surges, further propelling the segment's growth. Sustainable, eco-friendly cosmetic trends will further amplify the use of capric acid as brands prioritize bio-based ingredients.

Pharmaceuticals are predicted to be the fastest-growing segment over the 2026-2033 forecast period. In the pharmaceutical sector, capric acid serves as a key intermediate in the synthesis of drugs such as antibiotics, antifungals, and antiviral agents. Rising infectious disease prevalence drives demand, alongside active research and development efforts. Companies pursue advanced formulations to enhance efficacy and delivery. The expansion of pharmaceutical manufacturing in emerging economies can potentially unlock significant opportunities for capric acid suppliers. This segment also positions producers to capitalize on innovative therapies and global health needs.

Regional Insights

Asia Pacific Capric Acid Market Trends

Asia Pacific is likely to be both the leading and fastest-growing regional market for capric acid in 2026, accounting for approximately 40% of the market share. A strong industrial base supports production and distribution, meeting needs in sectors such as food processing, pharmaceuticals, and cosmetics. Manufacturers leverage local resources like coconut and palm kernel oils to supply essential ingredients efficiently. Companies actively invest in capacity upgrades to handle rising volumes, ensuring reliable availability for diverse applications. This dominance stems from integrated supply chains that connect raw material sources with end-users seamlessly. Population growth and swift urbanization fuel demand for everyday products in the region. Residents in bustling cities require more food additives, medicines, and personal care items, which boosts consumption of capric acid derivatives.

Nations such as China, India, and Japan drive this momentum through established manufacturing hubs and innovation centers. Governments promote sustainable practices, encouraging firms to adopt eco-friendly sourcing and processing methods. The area will have solidified its position further, as producers align with global trends toward green chemistry. Local players gain edges by tailoring offerings to regional preferences, from functional foods to advanced skincare. Asia Pacific is strongly positioned to shape the market's trajectory through 2033, offering suppliers opportunities to forge partnerships and capture value in high-growth economies committed to quality and responsibility.

Europe Capric Acid Market Trends

Europe is anticipated to emerge as a key market for capric acid, fueled by strong consumer interest in natural ingredients across multiple sectors. Industries such as food processing, pharmaceuticals, and personal care actively incorporate bio-based solutions to meet evolving preferences. Manufacturers prioritize capric acid for its versatile properties, which enhance product quality and functionality. Companies respond to this demand by expanding production capabilities and refining supply networks to ensure consistent delivery. This regional strength reflects a mature ecosystem that values innovation alongside reliability in everyday applications. Shoppers embrace organic options, prompting brands to reformulate with sustainable ingredients under rigorous oversight.

Regulatory bodies enforce high standards that safeguard quality and environmental impact, fostering trust among users. Sustainability initiatives gain traction as firms adopt practices that reduce carbon footprints and promote ethical sourcing. Countries such as Germany, France, and the United Kingdom lead through advanced facilities and discerning markets. The chemical industry in Europe is expected to deepen its commitment to green chemistry, creating avenues for suppliers to thrive. Local producers differentiate via certifications and localized strategies, strengthening bonds with eco-conscious buyers. Stakeholders of the region have positioned capric acid as a cornerstone for future-oriented growth, balancing compliance with market aspirations for purity and responsibility.

North America Capric Acid Market Trends

North America is a vital market for capric acid, driven by robust pharmaceutical and personal care sectors. Developers integrate the ingredient into advanced formulations for drugs and beauty products, capitalizing on its proven efficacy. Manufacturers expand operations to meet steady needs from health-focused consumers. Companies innovate continuously, blending capric acid with cutting-edge technologies to improve treatment and cosmetic outcomes. This foundation supports reliable growth as industries prioritize quality-driven solutions. Consumers shift toward natural components, which accelerates the adoption of sustainable alternatives in mature economies.

Awareness of the advantages of capric acid can be spread through education campaigns and expert endorsements, influencing buying decisions. Demand for organic personal care products is rising, prompting brands to refine their portfolios accordingly. The United States leads the region in terms of sophisticated infrastructure and dedicated research and development efforts. The country’s chemical production capacity is likely to amplify its role through investments in bio-based innovation and regulatory alignment. Producers can seize opportunities by forging collaborations that emphasize traceability and performance, shaping the North America capric acid market growth.

Competitive Landscape

The global capric acid market presents a moderately consolidated structure. Companies such as IOI Oleo, Kuala Lumpur Kepong Berhad, Emery Oleochemicals, Wilmar International, and BASF account for approximately 39% of total market revenue. These organizations are leveraging integrated oleochemical production networks, established distribution channels, and long-term relationships with downstream manufacturers in order to sustain their market presence. Large manufacturers are also expanding production capacity through facility modernization and supply chain optimization in order to meet growing demand from industries that require medium-chain fatty acids for functional ingredient applications.

The market is supporting a diverse ecosystem of regional producers and small and medium sized enterprises (SMEs) that are contributing to competitive intensity across several application segments. These companies are often specializing in niche product formulations or customized oleochemical derivatives tailored to specific industrial needs. Competitive dynamics are therefore encouraging both large and mid-sized producers to expand their research and development activities. Innovation efforts are also focusing on developing sustainable production methods that rely on renewable feedstock such as PKO and coconut oil.

Key Industry Developments

- In January 2026, IIT Madras researchers developed a sustainable, non-toxic method to recover valuable metals such as copper and iron from e-waste using deep eutectic solvents (DES) made from natural, biodegradable compounds such as thymol and capric acid.

- In October 2025, a Central University of Kerala study revealed that civet coffee (Kopi Luwak), derived from Asian palm civet droppings, owes its premium aroma and creamy flavor to significantly higher fat content and elevated levels of caprylic and capric acid methyl esters.

Companies Covered in Capric Acid Market

- IOI Oleo GmbH

- KLK Oleo

- Emery Oleochemicals

- Wilmar International

- BASF SE

- Musim Mas

- Oleon NV

- Kao Corporation

- Godrej Industries

- Twin Rivers Technologies

- VVF Ltd.

- Pacific Oleochemicals

- Zhongshan Kemei Oleochemicals

- Ecogreen Oleochemicals

Frequently Asked Questions

The global capric acid market is projected to reach US$ 191.5 million in 2026.

The market is driven by rising demand in food, personal care, and pharmaceuticals, alongside health trends favoring medium-chain triglycerides.

The market is poised to witness a CAGR of 4.5% from 2026 to 2033.

Major opportunities lie in sustainable sourcing from certified palm/coconut chains, which offer expansion, and pharmaceutical innovations in drug delivery and animal feed alternatives that can create untapped demand channels.

IOI Oleo, KLK Oleo, Emery Oleochemicals, Wilmar International, and BASF SE are some of the key players in the market.