- Hardware & Software IT Services

- Business Continuity Management Planning Solution Market

Business Continuity Management Planning Solution Market Size, Share, and Growth Forecast, 2026 - 2033

Business Continuity Management Planning Solution Market by Component Type (Software, Services), Deployment Mode (On-Premises, Cloud, Hybrid), End user (BFSI, IT & Telecommunications, Government & Public Sector, Healthcare & Life Sciences, Manufacturing, Energy & Utilities, Retail & E-Commerce, Misc.) and Regional Analysis for 2026 - 2033

Business Continuity Management Planning Solution Market Size and Trends Analysis

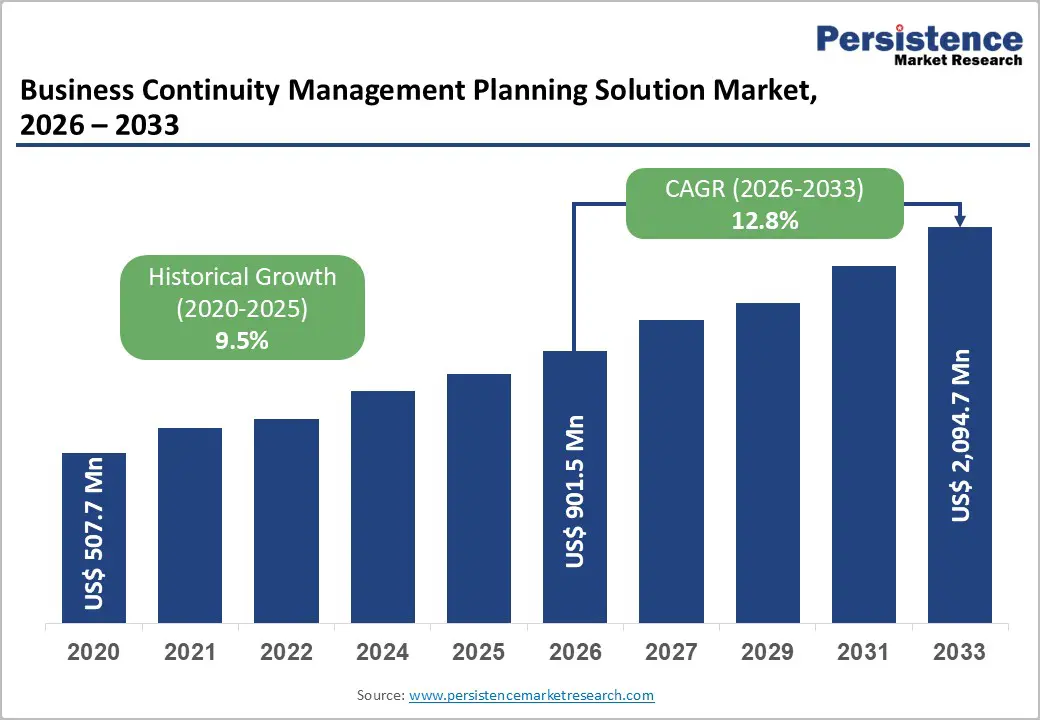

The Global Business Continuity Management Planning Solution Market size was valued at US$ 901.5 Million in 2026 and is projected to reach US$ 2,094.7 Million by 2033, growing at a CAGR of 12.8% between 2026 and 2033. The market has demonstrated substantial momentum from its 2020 valuation of US$ 507.7 Million, achieving a historical CAGR of 9.5%. This acceleration reflects enterprises' strategic prioritisation of operational resilience frameworks amid complex threat landscapes encompassing cyber vulnerabilities, natural disasters, and regulatory compliance mandates. Financial institutions, healthcare providers, and telecommunications operators are deploying comprehensive continuity solutions to safeguard critical operations, minimise downtime costs, and maintain stakeholder confidence during disruption events

Key Industry?Highlights:

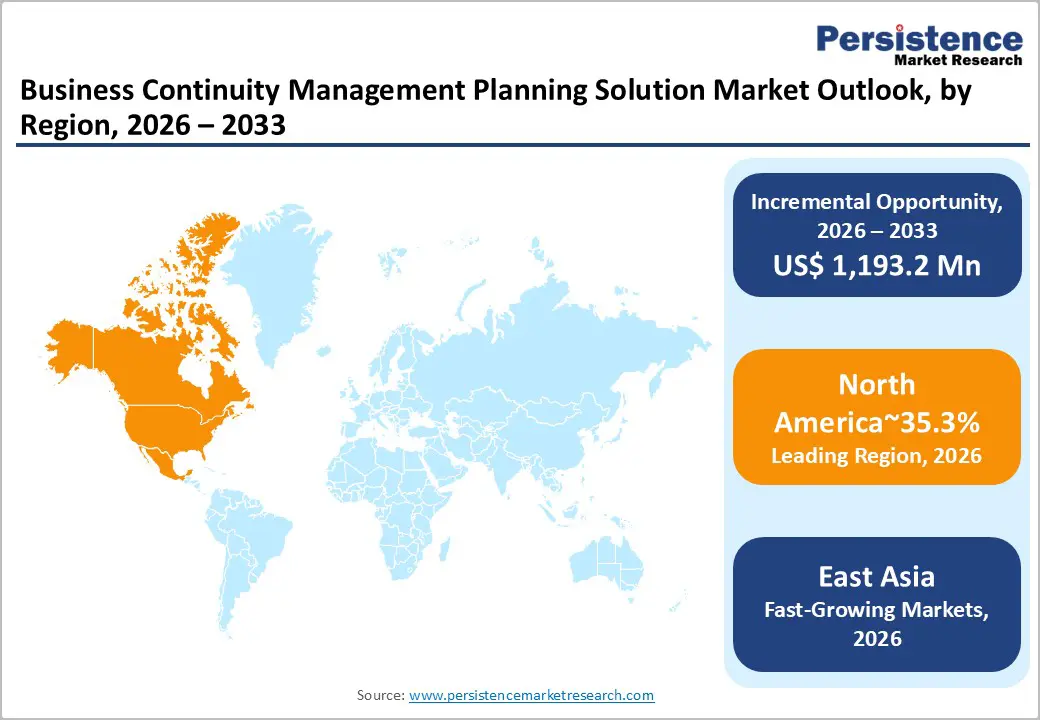

- Leading Region: North America leads the global market with a dominant 35.3% share, driven by mature regulatory frameworks, high digital adoption, and strong enterprise investment in continuity and resilience planning.

- Dominant Segment: Software remains the leading component segment with 63.6% share in 2026, reflecting enterprise preference for scalable SaaS platforms that centralise planning, testing, and recovery workflows.

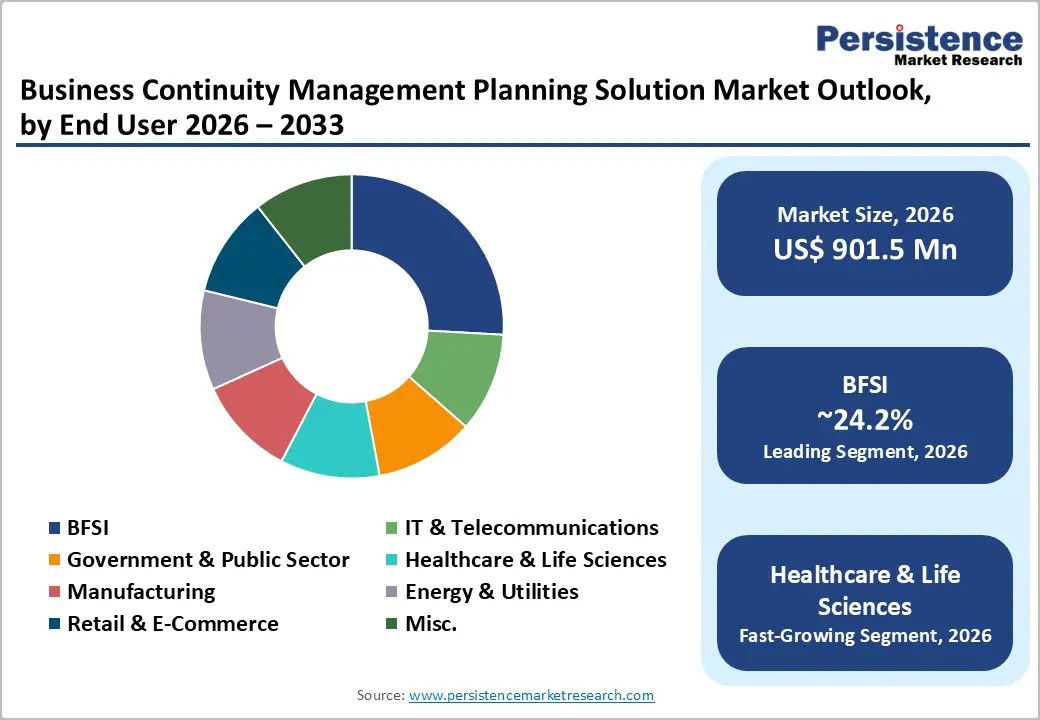

- Leading End User Segment: BFSI is the largest end-user segment at 24.2% in 2026, supported by stringent operational resilience mandates and zero-tolerance for downtime across payment systems, trading platforms, and customer channels.

- Fastest-Growing Segment: Healthcare & Life Sciences is the fastest-growing segment, propelled by digital health expansion, EMR adoption, telemedicine growth, and patient-safety-driven continuity requirements.

- Key Driver: Key growth drivers include cloud dependency, regulatory compliance pressures, and rising telecom network complexity, each increasing enterprise demand for proactive continuity planning tools.

| Key Insights | Details |

|---|---|

| Business Continuity Management Planning Solution Market Size (2026E) | US$ 901.5 Mn |

| Market Value Forecast (2033F) | US$ 2,094.7 Mn |

| Projected Growth (CAGR 2026 to 2033) | 12.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 9.5% |

Market Dynamics

Growth Drivers

Digital Transformation and Cloud Infrastructure Dependency

Digital transformation initiatives across enterprises have fundamentally altered operational architectures, creating critical dependencies on interconnected systems, cloud platforms, and data-driven processes that demand robust continuity frameworks.

India's banking, financial services, and insurance (BFSI) sector exemplifies this evolution, expanding 50 times in market capitalization to reach Rs. 91,00,000 crore (US$ 1 trillion) in 2025 from Rs. 1,80,000 crore (US$ 20.28 billion) in 2005, now contributing 27% to the country's GDP. This transformation, driven by the financialization of savings and digitisation, has seen banks' market capitalisation share decline from 85 percent to 57 percent as NBFCs, fintechs, and insurers gain prominence through technology-enabled service delivery. As organisations migrate critical workloads to cloud environments and implement real-time payment systems, the Market experiences heightened demand from enterprises requiring automated failover capabilities, disaster recovery protocols, and comprehensive business impact assessments to protect digital assets and maintain operational continuity across distributed infrastructure environments.

Regulatory Compliance and Risk Management Imperatives

Financial regulators and industry oversight bodies worldwide have intensified business continuity requirements, mandating documented recovery strategies, regular testing protocols, and demonstrated resilience capabilities across regulated entities.

The European Union's financial and insurance activities sector generated €0.9 trillion in value added in 2022 and employed nearly 5 million people across almost 867,000 enterprises, with a gross operating rate of 24.0 percent surpassing the business economy average. Germany, France, Italy, Spain, and Poland together accounted for over 65 percent of value added, highlighting the sector's concentrated economic significance and regulatory scrutiny. These institutions face stringent operational resilience requirements from authorities, including the European Central Bank, requiring comprehensive continuity frameworks that document critical business services, establish recovery time objectives, and maintain third-party risk management protocols.

The Market benefits from this regulatory environment as organisations deploy specialised software and services to demonstrate compliance, conduct scenario-based testing, and maintain audit-ready documentation across complex operational ecosystems.

Telecommunications Network Complexity and Service Availability Requirements

Modern telecommunications infrastructure supports critical societal functions, with service providers managing unprecedented network complexity while facing zero-tolerance expectations for downtime across mobile, broadband, and enterprise connectivity services.

India's telecom sector recorded a subscriber base of 1.21 billion and a tele-density of 86.09 percent as of June 2025, while internet subscribers reached 979 million, with gross telecom revenue rising from US$ 39.22 billion in FY24 to US$ 43.42 billion in FY25. Wireless services dominate over 96 percent of total subscriptions, while broadband connections surged from 149.75 million in 2016 to 979 million in 2025. The rollout of 5G networks, which contributed nearly a quarter of total wireless data usage in FY25, and ongoing fibre expansion under BharatNet initiative, create layered dependencies requiring sophisticated continuity planning across network elements, data centers, and customer service operations.

Telecommunications operators leverage Business Continuity Management Planning Solution Market offerings to model network failure scenarios, automate failover procedures, and coordinate cross-functional recovery activities that minimise service disruptions and maintain contractual service level agreements with enterprise and government customers.

Market Restraining Factors

Implementation Complexity and Legacy System Integration

Organisations encounter substantial technical and operational challenges when deploying business continuity solutions across heterogeneous IT environments characterised by legacy applications, on-premises infrastructure, and multiple cloud platforms.

Latin America's banking sector faces urgent pressure to modernise legacy systems that are costly, inefficient, and unable to support real-time payments like Brazil's PIX, with over 50 percentof adults remaining unbanked. Integration requirements demand specialised expertise, extensive configuration, and prolonged implementation timelines that strain IT resources and delay value realisation. The Market confronts adoption barriers as enterprises weigh implementation risks against operational imperatives, particularly in sectors with complex regulatory requirements and limited technical capabilities.

Key Market Opportunities

Artificial Intelligence Integration and Predictive Analytics

Emerging artificial intelligence capabilities enable next-generation business continuity solutions that leverage machine learning algorithms to predict potential disruptions, automate recovery workflows, and optimize resource allocation during crisis events. The Business Continuity Management Planning Solution Market stands positioned to incorporate AI-driven risk assessment engines that analyze historical incident data, external threat intelligence feeds, and real-time system telemetry to identify vulnerabilities before they materialise into operational disruptions.

According to Eurostat, one in three individuals in the EU used generative AI tools in 2025, reflecting the rapid integration of advanced digital technologies into professional activities, while 52 percent of individuals used electronic identification to access online services. This widespread AI adoption creates organisational readiness for sophisticated continuity solutions that embed predictive capabilities, natural language processing for policy documentation, and intelligent orchestration of recovery procedures. Solution providers can differentiate through AI-powered features, including automated business impact analysis, scenario simulation with probabilistic modelling, and adaptive recovery strategies that adjust based on real-time conditions, addressing unmet customer needs for proactive rather than reactive continuity management.

Healthcare Digital Transformation and Patient Care Continuity

Healthcare organisations worldwide are accelerating digital health initiatives, electronic medical record deployments, and telemedicine platforms that create critical dependencies requiring comprehensive business continuity frameworks to protect patient safety and care delivery. China's insurance sector demonstrated robust growth by Q2 2025, with insurance assets growing 9.2 percent to RMB 39.2 trillion, while primary premium income reached RMB 3.7 trillion, reflecting enhanced risk management across the sector.

Healthcare providers face unique continuity requirements encompassing medical device integration, regulatory compliance with patient data protection mandates, and life-critical system dependencies that demand specialised solution capabilities.

The Business Continuity Management Planning Solution Market can capture this opportunity through healthcare-specific offerings that address clinical workflow preservation, medical equipment failover procedures, and patient record accessibility during disruption events. The convergence of healthcare IT systems, Internet of Medical Things deployments, and value-based care models creates demand for continuity solutions with healthcare-optimised templates, clinical impact assessment methodologies, and integration capabilities with electronic health record platforms and hospital information systems.

Category-wise Analysis

Component Type Insights

Software solutions dominate the Business Continuity Management Planning Solution Market, commanding 63.6% market share in 2026 through comprehensive platforms that enable organisations to document continuity plans, conduct business impact assessments, manage recovery workflows, and maintain compliance documentation within centralised environments.

The information and communication services sector in the EU comprised around 1.4 million enterprises and employed nearly 7.2 million people in 2022, generating approximately €667 billion in value added, with computer programming, consultancy, and related activities contributing 59.8 percent of total employment. These organisations deploy business continuity software to manage complex IT dependencies, automate testing procedures, and coordinate cross-functional recovery activities across distributed teams and infrastructure environments.

Enterprise preference for software-based solutions reflects the scalability, integration capabilities, and continuous improvement potential offered by modern SaaS platforms that eliminate on-premises infrastructure requirements while delivering regular feature enhancements, threat intelligence updates, and regulatory template modifications. Software vendors provide industry-specific modules addressing sector requirements in financial services, healthcare, telecommunications, and manufacturing, with pre-configured assessment frameworks, recovery procedure templates, and compliance reporting capabilities that accelerate deployment timelines and reduce implementation complexity for organisations establishing or modernising continuity programs.

Professional services represent the fastest-growing component segment as organisations require specialised expertise for continuity program design, implementation support, testing facilitation, and ongoing optimisation activities that extend beyond software deployment. Cumulative FDI inflows into India's telecom sector reached Rs. 3,43,360 crore (US$ 40.07 billion) between April 2000 and March 2025, making it the fourth-largest sector for FDI equity inflows, with large-scale 5G rollouts, fibre expansion, and initiatives targeting rural connectivity, strengthening network infrastructure.

End User Insights

The Banking, Financial Services, and Insurance sector leads to end-user adoption with 24.2% market share in 2026, driven by stringent regulatory requirements, systemic risk considerations, and zero-tolerance expectations for service disruptions affecting payment systems, trading platforms, and customer access channels.

Financial institutions deploy sophisticated business continuity solutions encompassing core banking system redundancy, trading platform failover capabilities, payment processing backup procedures, and customer communication channel alternatives that maintain operational capacity during infrastructure failures, cyber incidents, or natural disasters. Regulatory frameworks from central banks, securities regulators, and insurance supervisory authorities mandate documented continuity plans, regular testing cycles, and board-level governance oversight that drive continuous investment in planning solutions and professional services supporting compliance demonstration and operational resilience enhancement across complex financial ecosystems.

Healthcare and Life Sciences represent the fastest-growing end-user segment as digital health adoption, electronic medical record ubiquity, and telemedicine expansion create critical system dependencies that directly impact patient safety and care delivery continuity. As of Q2 2025, China's banking and insurance sectors demonstrated robust growth with commercial banks maintaining strong asset quality with an NPL ratio of 1.49 percent and a capital adequacy ratio of 15.58 percent, while the insurance sector maintained a comprehensive solvency ratio of 204.5 percent, reflecting enhanced risk management. Similar risk management rigor now extends to healthcare organisations managing life-critical systems, patient data protection obligations, and regulatory compliance requirements under health information privacy frameworks.

Regional Insights and Trends

North America Market Trend

North America commands 35.3% of the global Business Continuity Management Planning Solution Market, driven by mature regulatory frameworks, advanced digital infrastructure, and concentrated enterprise spending across financial services, healthcare, and technology sectors headquartered in the United States and Canada. The region benefits from stringent business continuity requirements established by federal financial regulators, healthcare privacy enforcement agencies, and critical infrastructure protection mandates that compel organisations to maintain documented recovery capabilities and demonstrate operational resilience through regular testing and independent validation procedures.

According to Eurostat, household internet access in the EU reached 99 percent in the Netherlands and Luxembourg in 2025, while Denmark, the Netherlands, and Luxembourg reported that more than 99 percent of individuals had used the internet within the last three months, reflecting digital maturity comparable to North American markets.

North American enterprises similarly maintain near-universal connectivity alongside sophisticated IT environments characterised by multi-cloud deployments, distributed workforce models, and complex supply chain dependencies that necessitate comprehensive continuity frameworks addressing technology failures, cybersecurity incidents, and third-party service disruptions.

East Asia Market Trend

East Asia captures 18% of the global market, propelled by rapid digital transformation, telecommunications infrastructure expansion, and government initiatives promoting operational resilience across critical economic sectors in China, Japan, and South Korea. China's digital ecosystem reached 1.108 billion internet users by December 2024, adding over 16 million new users year-on-year, with internet penetration rising to 78.6 percent and mobile internet users accounting for 99.7 percent of all netizens. The diversification of access devices, including desktops, laptops, tablets, smart TVs, wearables, smart home devices, and connected vehicles, signals demand for resilient networks and high-bandwidth optical backhaul infrastructure supporting business continuity requirements.

By December 2024, social networking, instant messaging, online video, and short-video platforms each served more than one billion users in China, while online payment users surpassed 1.029 billion, e-government users reached 1.004 billion, and online shopping users climbed to 974 million. This deep integration of digital platforms into economic activity creates critical dependencies requiring comprehensive continuity frameworks across e-commerce operators, payment service providers, and government digital service platforms. Emerging applications, including online healthcare, smart mobility, connected vehicles, and generative AI which reached 249 million users significantly increase traffic volumes and reliability requirements across national networks, driving demand for continuity solutions addressing network infrastructure resilience, data center redundancy, and application failover capabilities.

Europe Market Trend

Europe represents 25% of the global Business Continuity Management Planning Solution Market, supported by comprehensive regulatory frameworks, high digital maturity, and concentrated economic activity across financial services, telecommunications, and public sector organisations in Germany, France, the United Kingdom, and Nordic countries.

In 2022, the European Union's financial and insurance activities sector generated €0.9 trillion in value added across almost 867,000 enterprises, with Germany, France, Italy, Spain, and Poland accounting for over 65 percent of value added, while the sector exhibited high productivity with a wage-adjusted labour productivity ratio of 236.1 percent. These institutions face stringent operational resilience requirements from the European Banking Authority, the European Central Bank, and national financial regulators mandating comprehensive continuity frameworks, regular testing, and demonstrated recovery capabilities.

In 2023, the European banking sector held total assets of €43.6 trillion, with loans outstanding at €26.8 trillion and total deposits reaching €17.3 trillion, while the number of credit institutions fell to 5,304, driven by digitalisation and efficiency-focused restructuring. This consolidation creates larger, more complex institutions managing multi-country operations, cross-border payment systems, and integrated digital banking platforms that demand sophisticated business continuity solutions addressing operational dependencies, third-party service providers, and regulatory compliance requirements across multiple jurisdictions. Despite workforce reductions, banking remained a significant employer, accounting for over 2 million jobs, highlighting the sector's economic importance and continuity imperative.

Competitive Landscape

The Global Business Continuity Management Planning Solution market is moderately consolidated, with a mix of large technology firms and specialised vendors driving growth. Leading players such as IBM, Microsoft, Oracle, Fusion Risk Management, Continuity Logic, and Sungard Availability Services dominate through comprehensive solution portfolios, strategic partnerships, and investments in AI-powered and cloud-based planning tools. These companies leverage scale and ecosystem integration to serve large enterprises, while smaller niche vendors focus on flexible, industry-specific solutions, creating pockets of fragmentation. The market is highly competitive, with innovation in automation, real-time dashboards, and scenario planning shaping differentiation. Strategic collaborations, mergers, and acquisitions further strengthen the positions of leading players.

Competitive Landscape

- On September 30, 2025, Swimlane launched its Business Continuity Management (BCM) Solution on the Swimlane Turbine platform, offering a cost-effective, AI-powered platform with centralized oversight, unlimited users, and automated guidance to help organizations minimize downtime, financial loss, and reputational damage during disruptive events.

- On February 19, 2025, Fusion Risk Management launched BC Plan inFusion, a GenAI-powered capability that automates the upload, structuring, and integration of business continuity plans into its platform, enabling organizations to rapidly operationalize or enhance BC programs while reducing manual data management and improving real-time crisis readiness.

Companies Covered in Business Continuity Management Planning Solution Market

- Arcserve

- Dell EMC

- Continuity Logic

- CloudAlly

- Fusion Risk Management, Inc.

- Lockpath, Inc.

- Quantivate, LLC

- Rackspace US, Inc.

- StorageCraft Technology Corporation

- VMware

- MetricStream Inc.

- RecoveryPlanner.com

- Strategic BCP, Inc.

- Sungard Availability Services

- Synology Inc.

Frequently Asked Questions

The global Business Continuity Management Planning Solution Market is projected to be valued at US$ 901.5 Mn in 2026.

The Software segment is expected to account for approximately 63.6% of the global Business Continuity Management Planning Solution Market by Component type in 2026.

The market is expected to witness a CAGR of 12.8% from 2026 to 2033.

The Business Continuity Management Planning Solution Market growth is driven by accelerating digital transformation and cloud dependency, tightening regulatory compliance and operational resilience mandates, and rising telecom network complexity requiring zero-downtime service continuity.

Key market opportunities in the Business Continuity Management Planning Solution market include AI-driven predictive continuity analytics and automation, along with accelerating healthcare digital transformation that creates demand for patient-safety-focused continuity frameworks and clinical IT resilience solutions.