- Semiconductor Materials & Components

- Braking Resistor Market

Braking Resistor Market Size, Share, and Growth Forecast, 2026 – 2033

Braking Resistor Market by Product (Wire-Wound Braking Resistors, Edge-Wound Braking Resistors, Grid Braking Resistors, Liquid-Cooled Braking Resistors, Enclosed / Encapsulated Braking Resistors, Others), Power Rating (Low Power, Medium Power, High Power), Industry, and Regional Analysis for 2026 – 2033

Braking Resistor Market Size and Trends

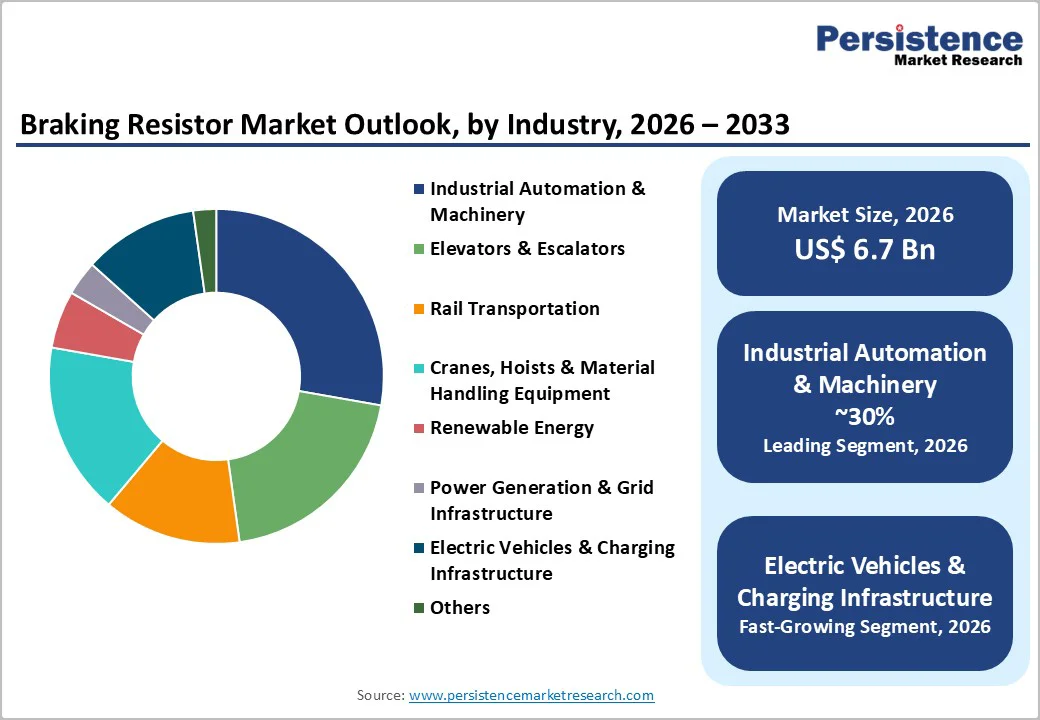

The global Braking Resistor Market is projected to grow from US$ 6.7 Bn in 2026 to US$ 10.1 Bn by 2033. It is anticipated to grow at a CAGR of 6.1% from 2026 to 2033.

The market expansion is propelled by the global electrification mega-trend spanning automotive, industrial automation, renewable energy infrastructure, and transportation systems. Stringent energy efficiency regulations, particularly the EU Ecodesign Regulation (EU) 2019/1781 mandating higher efficiency standards for variable speed drives and IEC 61800-5-1 safety requirements for adjustable speed electrical power drive systems, are compelling manufacturers and end-users to adopt advanced braking solutions.

Key Industry Highlights:

- Leading Product: Wire-wound braking resistors dominate the market with over 35% share in 2026, generating revenues above US$ 2.3 Bn, supported by their cost-effectiveness, proven thermal reliability, wide power-rating coverage, and strong adoption across industrial automation, elevators, cranes, and renewable energy systems. Liquid-cooled braking resistors are the fastest-growing product segment, expanding at a 9.7% CAGR through 2033, driven by EVs, mining electrification, and space-constrained high-power applications.

- Leading Power Rating: Medium power braking resistors (5 kW–50 kW) account for over 43% of the 2026 market, reflecting their extensive deployment in VFD-driven industrial machinery, building automation, and light-duty EV systems. High-power braking resistors (>50 kW) are the fastest-growing segment, with a 10.3% CAGR, driven by heavy rail, electric mining equipment, marine propulsion, and multi-megawatt industrial drive systems.

- Leading Industry: Industrial automation and machinery remain the largest end-use segment with over 25% market share in 2026, driven by accelerating VFD penetration, Industry 4.0 adoption, and continuous modernization of manufacturing facilities. Electric vehicles and charging infrastructure constitute the fastest-growing industry, expanding at a 9.5% CAGR, supported by global EV sales growth, commercial EV electrification, and high-power fast-charging installations.

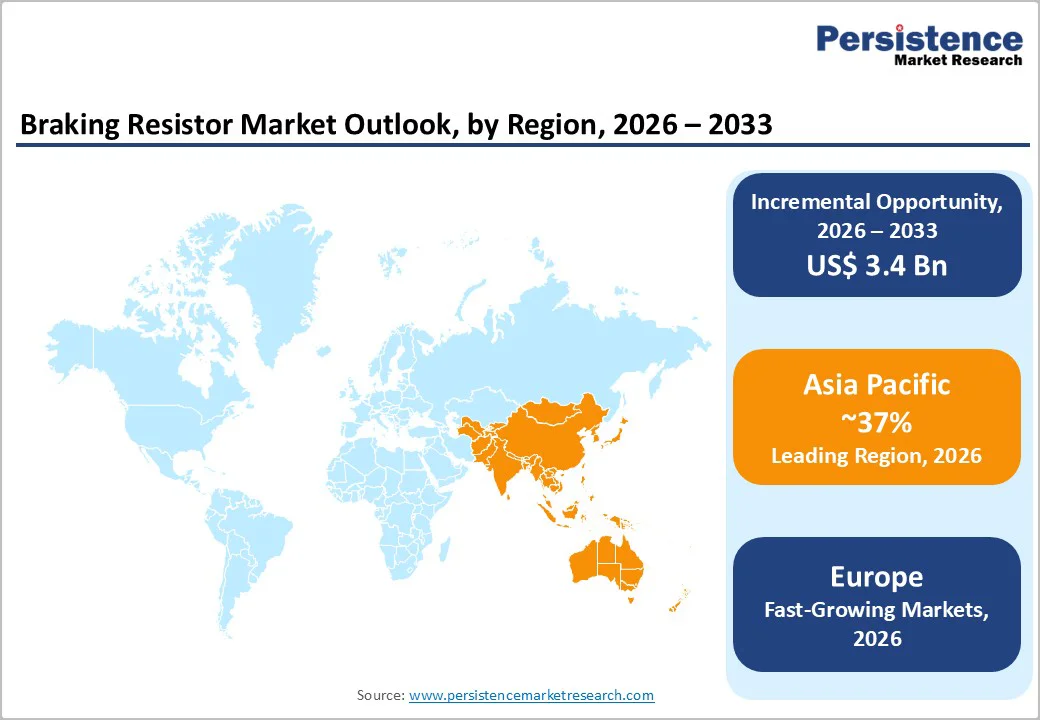

- Leading Region: North America leads the global market with over 30% share in 2026, supported by a mature industrial base, extensive VFD installations, renewable energy investments, and clear regulatory frameworks. Asia Pacific is the largest and fastest-growing region, accounting for over 37% of global share, driven by China’s EV dominance, India’s elevator and urban infrastructure boom, and accelerating manufacturing automation across ASEAN economies.

| Global Market Attribute | Key Insights |

|---|---|

| Braking Resistor Market Size (2026E) | US$6.7 Bn |

| Market Value Forecast (2033F) | US$10.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.4% |

Market Dynamics

Driver

Renewable Energy Infrastructure and Grid Stability Investments

Wind turbines, especially offshore installations rated at 8–15 MW, employ dynamic braking resistors during emergency shutdown procedures and maintenance operations to dissipate stored kinetic energy safely. Solar photovoltaic inverter systems utilize braking resistors to manage harmonic filtering and prevent voltage transients during grid disturbances. Global renewable power capacity increased by 585 GW in a single year, representing a record 15.1% annual growth rate, surpassing 2023's 14.3%, with substantial capital investments flowing into North America, Europe, and Asia-Pacific. Government mandates, including the EU's Green Deal and China's carbon neutrality commitments through 2060, provide structural support for renewable energy infrastructure, ensuring sustained demand for braking resistors across utility-scale applications.

Industrial Automation and Variable Frequency Drives Proliferation

The global manufacturing sector's transition to Industry 4.0 paradigms has exponentially increased the installed base of variable-frequency drives (VFDs) and servo systems that rely on dynamic braking resistors for safe operational control. Industrial settings from automotive assembly to pharmaceutical manufacturing employ VFDs to optimize motor efficiency, reduce energy consumption, and enhance process precision. When these drive systems decelerate loads, regenerative energy must be safely dissipated to prevent voltage spikes that could damage sensitive power electronics. According to a study, the integration of VFDs in existing manufacturing processes continues accelerating across emerging economies, with particular momentum in China and India's electronics, textile, and metals processing sectors, where modern automation has become a competitive necessity rather than a discretionary investment.

Restraint

Regulatory Fragmentation and Complex Compliance Requirements

Braking resistor applications span multiple regulatory jurisdictions, each imposing distinct electromagnetic compatibility (EMC), safety, and environmental standards. Manufacturing equipment must comply with IEC 61800-3 for power drive system emissions; rail transportation systems require EN 50121 compliance; and marine applications demand adherence to various maritime safety regulations. This regulatory complexity increases product development costs, extends time-to-market for innovative solutions, and creates technical barriers preventing smaller manufacturers from competing effectively.

High Initial Capital Investment and Cost Sensitivity

Advanced braking resistor systems, particularly liquid-cooled and encapsulated designs for high-power applications, represent substantial capital expenditures for industrial customers. A single high-performance braking resistor unit for wind turbines or heavy-duty crane systems exceeds US$50,000, and complete system integration costs can run into the hundreds of thousands of dollars. Industrial customers, particularly in emerging economies with capital-constrained budgets, often defer adoption of premium resistor solutions and instead use legacy air-cooled or wire-wound designs, despite their inferior thermal performance and shorter operational lifespans. This cost sensitivity fundamentally limits market expansion in price-sensitive industrial segments and constrains the adoption of next-generation technologies among small and medium-sized manufacturers.

Opportunity

Mining Equipment Electrification and Off-Highway Vehicles

Mining electrification initiatives present substantial untapped opportunities, with 91% of surveyed mining companies considering electrification essential for decarbonization strategies. Electric dump trucks, loaders, drills, and excavators require robust braking systems capable of managing extreme duty cycles, high regenerative loads, and harsh environmental conditions. Battery-electric mining equipment manufacturers are introducing large-capacity vehicles with all-electric drivetrains and multi-megawatt power systems, which demand advanced braking-resistor solutions. The transition from diesel to electric mining fleets creates demand for high-power braking resistors as these applications routinely involve decelerating vehicles carrying hundreds of tons of payload on steep gradients.

Marine Vessel Electrification and Hybridization

Marine vessel electrification and hybridization are accelerating the adoption of electric propulsion, battery systems, and variable frequency drives (VFDs), all of which require braking resistors for safe energy dissipation. The growing use of hybrid propulsion in ferries, offshore support vessels, and naval ships increases demand for high-power, marine-grade braking resistors. Stricter emission regulations from IMO are further pushing shipowners toward electric and hybrid retrofits, expanding aftermarket opportunities. The shift toward DC grids and regenerative systems onboard vessels makes braking resistors critical for energy management and system reliability.

Category-wise Analysis

Product Analysis,

Wire-wound braking resistors maintain market leadership with over 35% market share in 2026, translating to revenues exceeding US$ 2.3 Bn. This dominance stems from their proven reliability, excellent heat dissipation characteristics, cost-effectiveness, and versatility across power ratings from hundreds of watts to multiple megawatts. Wire-wound designs utilizing spiral-wound resistance wire on ceramic formers achieve an optimal balance between thermal capacity, overload tolerance, and manufacturing scalability. The resistance material typically high-grade stainless steel or nichrome alloy exhibits minimal resistance drift over operating temperature ranges, ensuring consistent braking performance across duty cycles.

Liquid-cooled braking resistors constitute the fastest-growing segment with a CAGR of 9.7% through 2033. The segment's expansion is propelled by electric vehicle adoption, particularly in heavy-duty commercial applications where compact packaging and continuous high-power dissipation are critical requirements. Liquid-cooled designs achieve power densities 5-10 times higher than air-cooled equivalents, enabling 10% volume reduction and 15% weight savings, crucial factors in vehicle applications where space and weight directly impact payload capacity and energy efficiency. The ability to recover waste heat for productive uses adds operational value beyond simple energy dissipation.

Power Rating Analysis,

Medium-power braking resistors (5 kW – 50 kW) command the largest market share, over 43% in 2026, reflecting their alignment with the broadest application range across industrial automation, building systems, and light-duty EV applications. This segment encompasses standard VFD systems serving motors from 5 HP through 150 HP, covering the vast majority of installed industrial base globally. The dominance reflects established supply chains, standardized mounting interfaces, and proven thermal designs that minimize customer engineering requirements. Medium-power resistors command established market positions, with multiple competing suppliers, standardized product specifications, and lower unit pricing compared to specialized high-power alternatives.

High-power braking resistors (above 50 kW) represent the fastest-growing power segment with a CAGR of 10.3%, driven by large-scale industrial applications, heavy rail systems, mining equipment, and marine propulsion. Electric mining trucks with payload capacities exceeding 200 tons and multi-megawatt drive systems require braking resistor banks capable of dissipating 500 kW to several megawatts during downhill operation. High-speed rail systems, metro networks, and freight locomotives employ high-power resistor arrays to manage regenerative braking energy that cannot be immediately returned to the traction power network due to grid capacity constraints or absence of receptive loads.

Industry Analysis,

Industrial automation and machinery applications account for over 25% of the 2026 market share, maintaining category leadership driven by ubiquitous adoption of variable-frequency drives across manufacturing ecosystems. Machine tools, conveyor systems, pumping stations, and textile machinery employ VFD-based motor control fundamentally dependent on braking resistors for safe deceleration, energy efficiency, and operational precision. The segment benefits from established automation infrastructure modernization cycles, sustained capital investment in manufacturing facility upgrades, and continuous increases in automation density within existing facilities.

Electric vehicles and charging infrastructure are growing at the highest rate with a 9.5% CAGR through 2033. EV production continues an exponential growth trajectory according to the IEA, the global electric car sales reached almost 14 million in developed markets and are rapidly penetrating emerging economies. Each EV requires sophisticated regenerative braking systems with carefully engineered braking-resistor components to absorb energy when regenerative capacity is saturated safely. Commercial EV platforms demand substantially larger braking resistor capacities than passenger vehicles, creating differentiated product requirements and pricing tiers. Expanding charging infrastructure, particularly fast-charging stations (150+ kW), requires grid stabilization circuits that employ specialized braking resistors to manage harmonic filtering and voltage transients.

Regional Insights

North America Braking Resistor Market Trends

The North American braking resistor market commands over 30% of the global market share in 2026, reflecting the region's mature industrial base, established VFD infrastructure, and strong renewable energy investments. The United States dominates regional market valuation, driven by manufacturing sector automation, substantial elevator installations in multi-story urban developments, and significant wind energy capacity. The regulatory environment, particularly NFPA and ANSI standards for industrial equipment, establishes transparent compliance frameworks that support market development and supplier standardization. Canada's resource extraction industries, mining, oil sands, and forestry, represent significant consumers of heavy-duty industrial braking resistors for mobile equipment and process machinery.

Asia Pacific Braking Resistor Market Trends

Asia-Pacific emerges as the highest-growth region, accounting for over 37% of the 2026 global market share and projected growth significantly exceeding that of other major areas. The region encompasses China's dominance in EV manufacturing, accounting for over 60% of global production, India's explosive urbanization-driven elevator and escalator expansion, and Southeast Asia's emerging adoption of manufacturing automation. ASEAN nations are experiencing accelerating manufacturing automation as companies diversify production away from China, creating sustained demand for industrial drive systems and supporting the expansion of braking resistors. Manufacturing capacity establishment, regional product optimization, and distribution partnership development.

Europe Braking Resistor Market Trends

Europe accounts for approximately 19% of the 2026 market share, driven by strict energy-efficiency regulations, aggressive renewable-energy deployment targets, and the region's automotive-electrification leadership. The European Union's Green Deal establishes ambitious sustainability objectives, mandates renewable energy to account for 55% of total electricity generation by 2030, and accelerates vehicle electrification by tightening emissions standards. Germany leads European market activity through manufacturing excellence and automotive industry concentration, while the UK and France contribute substantial investments in industrial automation and renewable energy.

Competitive Landscape

The global braking resistor market exhibits a moderately fragmented competitive structure. Companies leverage extensive product portfolios, global distribution networks, established customer relationships, and integrated power electronics capabilities to maintain competitive positions. Competition centers on technological innovation, product customization capabilities, thermal performance, reliability, compliance with evolving energy-efficiency standards, and total cost of ownership, rather than on initial purchase price alone.

Key Industry Developments

- In November 2024, Bourns, Inc. launched three new Riedon High Pulse Braking Resistor families: BR/BRT, BRS, and UWP, designed for high-energy pulse and braking applications.

- Offering power ratings up to 500 W and operating temperatures up to +275 °C, the resistors support reliable energy dissipation in motor drives, inverters, BESS, and power conversion systems.

Companies Covered in Braking Resistor Market

- Vishay Intertechnology, Inc.

- Cressall Resistors Ltd.

- ABB Ltd.

- Siemens AG

- Eaton Corporation plc

- Schneider Electric SE

- Rockwell Automation, Inc.

- Yaskawa Electric Corporation

- Danotherm Electric A/S

- TE Connectivity Ltd.

- Captech Pty Ltd.

- Others

Frequently Asked Questions

The global market is projected to be valued at US$6.7 Bn in 2026.

Growing needs to safely dissipate excess regenerative energy in electric motors and drives, ensuring system stability and equipment protection, is a key driver of the market.

The market is expected to witness a CAGR of 6.1% from 2026 to 2033.

Modernization of railways, elevators, and smart manufacturing facilities is creating sustained demand for high-performance braking resistors.

Vishay Intertechnology, Inc., Cressall Resistors Ltd. , ABB Ltd., Eaton Corporation plc, Schneider Electric SE, TE Connectivity Ltd. are among the leading key players.