- Automotive

- Autonomous Trucks Market

Autonomous Trucks Market Size, Share, and Growth Forecast 2026 - 2033

Autonomous Trucks Market by Propulsion Type (Diesel, Electric, Hybrid), Vehicle Type (Light Duty Trucks, Medium Duty Trucks, Heavy Duty Trucks), Sensor Type (Camera, Radar, Lidar, Ultrasonic, Others), Application (Last Mile Delivery Trucks, Mining Trucks, Shuttles), and Level of Autonomy (L1, L2 & L3, L4, L5), and Regional Analysis for 2026 - 2033

Autonomous Trucks Market Size and Trend Analysis

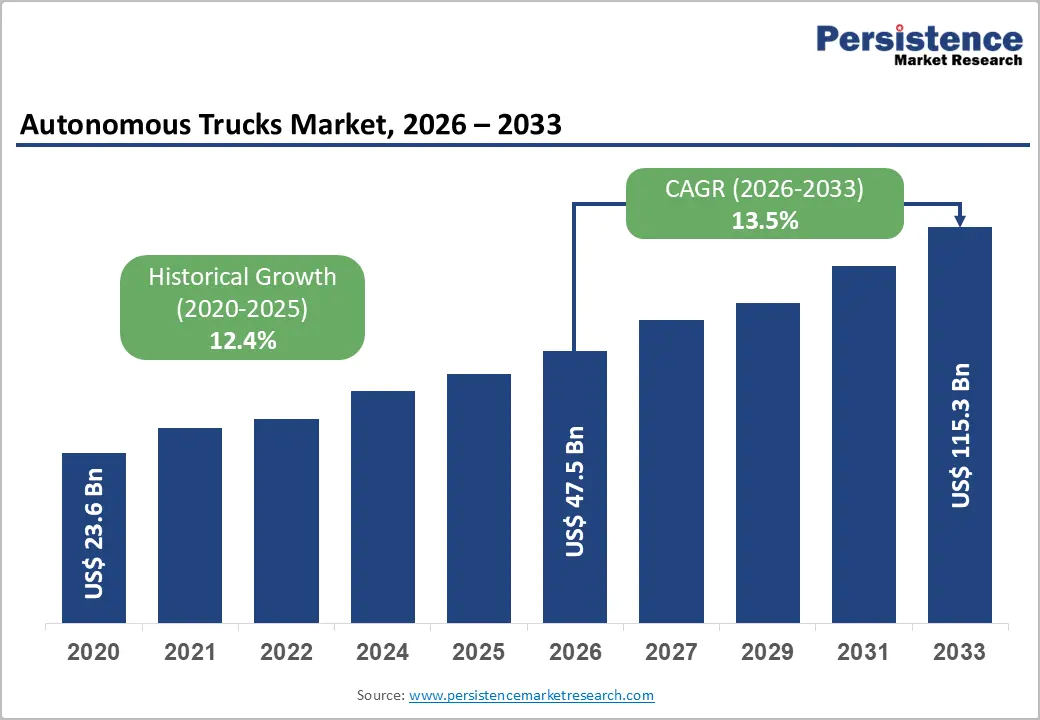

The global Autonomous Trucks market size is valued at US$ 47.5 billion in 2026 and is projected to reach US$ 115.3 billion by 2033, growing at a CAGR of 13.5% between 2026 and 2033. This robust growth is primarily driven by the accelerating adoption of advanced driver-assistance systems (ADAS) and artificial intelligence-based freight automation technologies, which are fundamentally transforming long-haul logistics.

Rise in driver shortages are estimated at over 80,000 unfilled positions in the United States alone, according to the American Trucking Associations (ATA) combined with tightening emissions regulations and surging e-commerce freight volumes.

Key Industry Highlights:

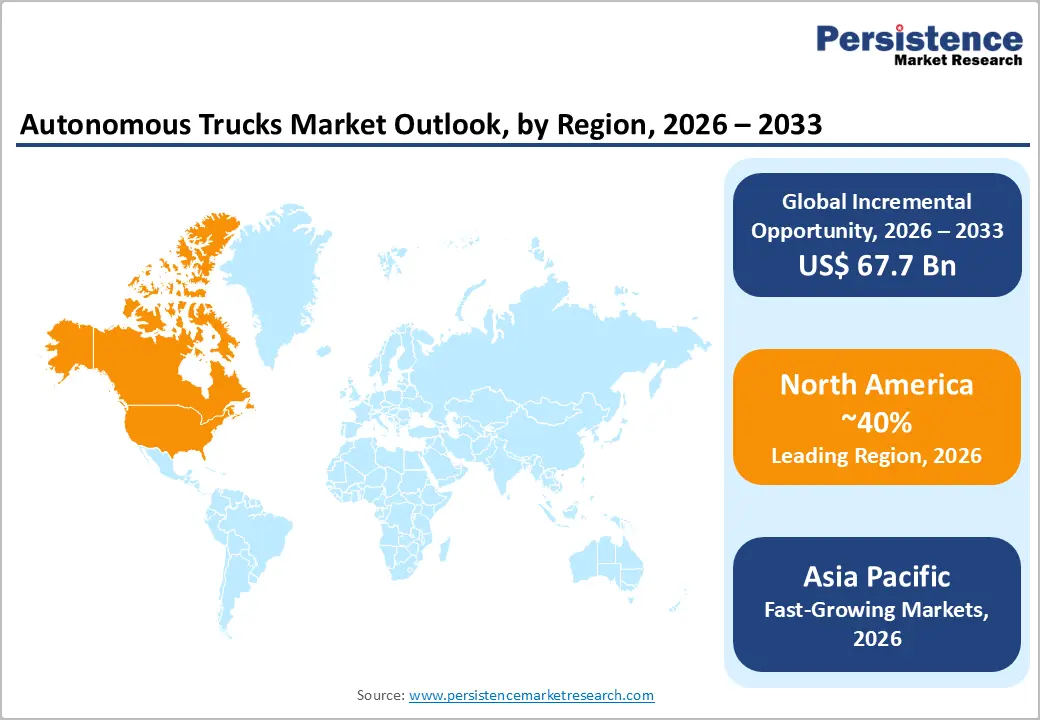

- Leading Region - North America leads the autonomous trucks market with approximately 38% of global revenue in 2025, driven by extensive highway infrastructure, progressive state-level AV regulations, and active commercial deployments by Aurora Innovation and Waymo Via on key U.S. interstate corridors.

- Fastest Growing Region – Asia Pacific is the fast-growing regional market, propelled by China's 16 government-designated intelligent vehicle pilot zones, Japan's 2023 approval of Level 4 motorway autonomy, and surging freight demand across Belt and Road logistics corridors.

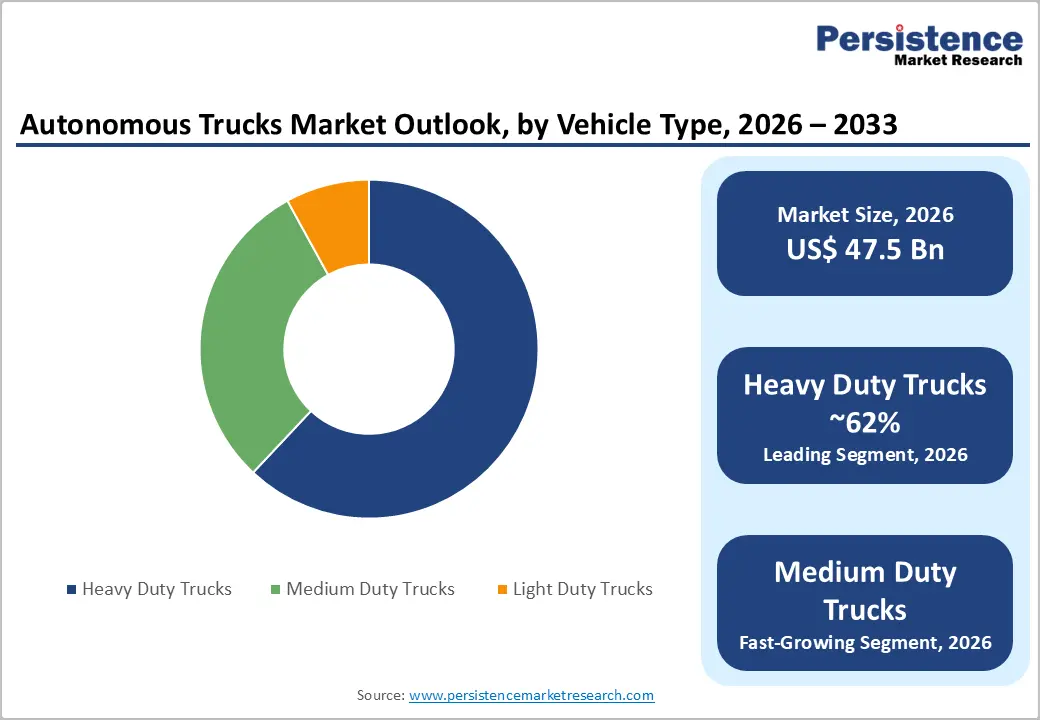

- Dominant Level of Autonomy – Heavy duty trucks dominate the vehicle type segment with ~62% market share, as Class 8 long-haul applications deliver the highest return on autonomous technology investment through reduced driver wages and extended operational uptime on high-mileage interstate freight routes.

- Fast-Growing Autonomy – The Level 4 autonomy segment is the fastest-growing classification, advancing from controlled pilots toward commercial deployment following Aurora Innovation's first fully driverless commercial run in April 2025 on the Dallas–Houston corridor without a safety driver.

- Key Opportunity - Mining sector autonomous truck deployment presents a high-value near-term opportunity, with established fleets from Caterpillar Inc. and Komatsu Ltd. demonstrating 15–20% haulage cost reductions, providing a proven commercial pathway for OEMs targeting geofenced off-highway applications.

Market Dynamics

Does Persistent Commercial Driver Shortage Accelerate Autonomous Fleet Adoption?

The chronic deficit of qualified commercial truck drivers is one of the most decisive structural catalysts for the autonomous trucks market. The American Trucking Associations (ATA) reported a shortage exceeding 80,000 drivers in 2023, a figure forecast to surpass 160,000 by 2031 if current trends persist. In Europe, the International Road Transport Union (IRU) estimates a shortfall of over 400,000 drivers across member states.

This labor scarcity is directly inflating freight costs, causing delivery delays, and disrupting supply chain efficiency. Autonomous trucks, operating with reduced human oversight, offer fleet operators a viable mitigation strategy. Pilot deployments by companies such as Aurora Innovation and Waymo Via on interstate corridors in Texas and the Sun Belt have demonstrated sustained operational viability, reinforcing confidence in the technology's commercial scalability.

Do Stringent Emissions Regulations and Decarbonization Mandates Spur Electric Autonomous Truck Development?

Tightening regulatory mandates targeting carbon emissions from heavy-duty freight vehicles are compelling OEMs to integrate autonomous capabilities alongside electric and hybrid powertrains. The U.S. Environmental Protection Agency (EPA) finalized the Phase 3 Greenhouse Gas Standards in 2024, requiring heavy-duty vehicles to reduce CO2 emissions by up to 60% by 2032 compared to 2021 baselines. Similarly, the European Union's Fit for 55 package mandates a 45% CO2 reduction for new heavy-duty trucks by 2030.

These regulatory trajectories are incentivizing freight operators to adopt electric autonomous trucks, where the combination of zero-emission drivetrains and optimized autonomous routing algorithms enhances both compliance and fuel efficiency. AB Volvo and Daimler Truck AG have both announced substantial R&D allocations exceeding EUR 500 Mn annually toward electrified autonomous commercial vehicles.

Are High Development and Integration Costs Limiting Mass Commercialization?

The prohibitive capital investment required to develop, validate, and deploy autonomous trucking systems remains a significant barrier to widespread commercialization. Industry analyses indicate that a fully equipped Level 4 autonomous heavy-duty truck can carry an incremental hardware and software cost of US$ 150,000–US$ 300,000 per unit above conventional equivalents, driven primarily by sensor suites, redundant compute platforms, and connectivity infrastructure.

For small-to-mid-size freight carriers, which constitute the majority of the 500,000+ registered trucking companies in the U.S. per Federal Motor Carrier Safety Administration (FMCSA) data, this cost differential is economically prohibitive, constraining adoption to large fleet operators and well-capitalized logistics conglomerates in the near term.

Are Fragmented Regulatory Frameworks Creating Cross-Jurisdictional Operational Uncertainty?

The absence of a unified international regulatory framework for autonomous commercial vehicle operation constitutes a material restraint on market expansion. In the United States, autonomous vehicle regulations are governed at the state level, resulting in a patchwork of divergent rules across 50 jurisdictions. While the National Highway Traffic Safety Administration (NHTSA) has issued voluntary guidelines, no binding federal framework mandating or standardizing autonomous truck operation exists as of 2025.

In the European Union, the UNECE Working Party 29 (WP.29) framework provides partial harmonization, but member-state implementation timelines vary significantly. This regulatory fragmentation compels manufacturers to develop compliance strategies for multiple overlapping jurisdictions, escalating time-to-market and legal overhead.

Does the Rapid Expansion of Last-Mile and E-Commerce Logistics Unlock High-Volume Autonomous Light-Duty Truck Demand?

The explosive growth of e-commerce fulfilment is creating an unprecedented demand environment for autonomous light-duty and medium-duty delivery trucks. According to the U.S. Census Bureau, e-commerce sales accounted for 15.9% of total U.S. retail sales in Q3 2024, with the segment continuing to outpace in-store retail growth. The United Parcel Service (UPS) and FedEx Corporation have both publicly disclosed multi-year autonomous vehicle pilot programs targeting urban and suburban last-mile operations.

Autonomous electric delivery trucks offering predictable route optimization, lower per-mile operating costs, and emissions compliance are increasingly positioned as the preferred solution for high-frequency, short-route delivery missions. As urban logistics density rises globally, fleet operators able to deploy scalable autonomous last-mile fleets stand to capture substantial cost advantages, with per-delivery cost reductions estimated at 30–40% versus manually operated alternatives.

Does Mining and Industrial Off-Highway Autonomous Trucks Emerge as Near-Term High-Value Application?

The mining sector represents one of the most commercially mature and immediately addressable application verticals for autonomous trucking technology. Unlike public road environments, mining sites offer controlled, geofenced operational domains that significantly reduce the safety certification complexity associated with open-highway autonomy.

Caterpillar Inc. reports that its autonomous mining truck fleet has collectively transported over 5 billion tonnes of material across global operations, demonstrating the technology's operational maturity. Komatsu Ltd. similarly operates a large fleet of autonomous haulage vehicles across sites in Australia, Chile, and Canada. The International Council on Mining & Metals (ICMM) projects that autonomous systems could reduce mining haulage costs by up to 15–20%, driven by improved utilization rates and reduced accident-related downtime.

Category-wise Analysis

Propulsion Type Insights

The diesel segment commands the dominant share within the propulsion type category, accounting for approximately 58% of the autonomous trucks market in 2026. Diesel-powered autonomous trucks continue to dominate primarily because the existing heavy-duty long-haul freight infrastructure fuel supply networks, maintenance ecosystems, and regulatory certifications is overwhelmingly calibrated for diesel powertrains.

Diesel engines offer superior range and payload-to-weight ratios critical for cross-continental freight applications where battery electric vehicles still face limitations. The U.S. Energy Information Administration (EIA) reports that diesel remains the fuel of choice for over 70% of Class 8 trucks currently in operation.

Vehicle Type Insights

The Heavy-Duty Trucks segment is the undisputed leader within the vehicle type category, representing approximately 62% of total market share. Heavy-duty trucks, Class 7 and Class 8 vehicles operating at gross vehicle weights exceeding 26,001 lbs are the primary target for autonomous technology deployment, given the economics of long-haul freight automation.

The return-on-investment calculus is most compelling for high-mileage intercity routes where driver wage costs and mandatory rest hours most significantly constrain throughput. The Federal Highway Administration (FHWA) estimates that Class 8 trucks account for nearly 68% of total U.S. freight ton-miles.

Sensor Type Insights

The Lidar segment holds the leading position within the sensor type category, accounting for approximately 34% of market share in 2026. Lidar sensors provide high-resolution three-dimensional environmental mapping with centimetre-level precision, which is indispensable for safe autonomous operation of large commercial vehicles in complex traffic environments. The Society of Automotive Engineers (SAE International) recognizes Lidar as a foundational sensing modality for achieving SAE Level 4 autonomy in highway freight applications.

Recent technological progress from suppliers, including Luminar Technologies and Innoviz Technologies, has reduced solid-state Lidar unit costs by over 80% since 2017, making large-scale fleet integration economically feasible.

Application Insights

The last mile delivery trucks application segment commands the largest share within the application category, representing approximately 45% of total market revenue. The rapid proliferation of e-commerce and on-demand logistics platforms has created intense demand for cost-efficient, high-frequency urban delivery solutions. Autonomous trucks operating in defined urban delivery corridors reduce labor dependency and enable 24/7 operational continuity without regulatory rest-hour constraints.

Amazon.com, Inc. disclosed in its 2024 Sustainability Report that it operates over 10,000 electric delivery vehicles and is actively piloting autonomous last-mile platforms. The World Economic Forum (WEF) projects that urban freight volumes will increase by 78% by 2030, creating a structurally expanding addressable market for autonomous last-mile delivery trucks.

Level of Autonomy Insights

The L2 & L3 autonomy segment currently dominates the market, accounting for approximately 48% of total market share in 2026. This dominance reflects the current state of technology readiness and regulatory permissibility. Level 2 and Level 3 systems, which provide partial and conditional automation, respectively, are commercially deployed at scale on production vehicles from AB Volvo, Daimler Truck AG, and Paccar Inc. under validated highway assist and platooning configurations.

The SAE International J3016 standard governs the classification, and regulatory bodies in the United States, Germany, and Japan have issued specific approvals for Level 3 highway operation. While Level 4 systems represent the fast-growing segment, near-term volume and installed base are dominated by L2 & L3 deployments reflecting existing OEM production capabilities.

Regional Analysis

North America Autonomous Trucks Market Trends & Analysis

North America is the largest regional market for autonomous trucks, accounting for an estimated 38% of global revenue in 2026. The region benefits from a mature logistics infrastructure, progressive state-level autonomous vehicle regulatory frameworks, and deep venture and OEM investment in autonomous trucking startups. The U.S. Department of Transportation (USDOT) has allocated over US$ 500 Mn toward automated vehicle research and safety frameworks through various programs under the Bipartisan Infrastructure Law. Key technology corridors in Texas, Arizona, and California serve as primary testing and early commercial deployment zones for companies including Aurora Innovation, Waymo Via, and TuSimple Holdings.

U.S. Autonomous Trucks Market Trends

The United States represents over 85% of the North American autonomous trucks market, supported by substantial technology investment, active commercial pilots, and favorable regulatory developments in states such as Texas, Arizona, and California. The FMCSA's exemption and rulemaking processes for automated driving system (ADS)-equipped commercial vehicles are progressively enabling expanded autonomous freight operations.

Europe Autonomous Trucks Market Trends

Europe is the second-largest market, driven by stringent EU Green Deal emissions mandates, advanced automotive manufacturing competencies, and coordinated cross-border logistics corridors. The European Commission's approval of Level 3 autonomous driving under the UNECE WP.29 Regulation 157 has enabled OEMs to commercially deploy highway chauffeur systems on production trucks.

Germany Autonomous Trucks Market Insights

Germany commands approximately 28% of the European autonomous trucks market, driven by its strong OEM base and regulatory leadership. The BMDV has designated specific Autobahn corridors as approved testing environments for Level 4 commercial vehicle pilots, with Daimler Truck AG conducting active evaluations on A8 and A81 motorways.

U.K. Autonomous Trucks Market Share

The United Kingdom accounts for approximately 14% of the Europe market. The UK Centre for Connected and Autonomous Vehicles (CCAV) has funded multiple autonomous truck platooning trials, and the Automated Vehicles Act 2024 provides the legal framework for commercial deployment, positioning the U.K. as an emerging adoption leader post-Brexit.

France Autonomous Trucks Market Share

France represents approximately 11% of the European autonomous trucks market. Stellantis N.V. and logistics group GEODIS have conducted autonomous last-mile delivery truck pilots supported by French Ministry for Ecological Transition funding, with national decarbonization ambitions accelerating interest in electric autonomous platforms.

Asia Pacific Autonomous Trucks Market

Asia Pacific is the fastest-growing regional market, fuelled by massive freight demand in China, rapid government-led smart transportation infrastructure investment, and manufacturing cost advantages. China's Ministry of Industry and Information Technology (MIIT) has designated 16 pilot zones for intelligent connected vehicle testing as of 2024. Japan and South Korea are leveraging advanced robotics and semiconductor ecosystems to accelerate sensor and compute development for autonomous trucks.

China Autonomous Trucks Market

China is the dominant market in Asia Pacific, representing approximately 55% of regional revenue. Domestic leaders, including Plus AI and DeepRoute.ai, alongside global players, are scaling commercial pilots. The MIIT's 2023 policy on intelligent vehicle industry standards provides a structured pathway toward Level 4 commercialization on national expressways.

India Autonomous Trucks Market

India is an emerging market with growing potential driven by a INR 10 trillion+ national highway expansion program and rising logistics modernization demand. While regulatory frameworks are nascent, the Ministry of Road Transport and Highways (MoRTH) has initiated consultations on ADAS mandates for commercial vehicles, with full autonomy pilots expected post-2027.

Japan Autonomous Trucks Market

Japan holds approximately 18% of the Asia Pacific autonomous trucks market. The Ministry of Land, Infrastructure, Transport and Tourism (MLIT) approved Level 4 automated driving on motorways in 2023, enabling domestic OEMs including Hino Motors Ltd. and Isuzu Motors Ltd. to advance commercial deployments on priority freight corridors by 2025–2026.

Competitive Landscape

The autonomous trucks market exhibits a moderately fragmented competitive structure, characterized by an evolving ecosystem of established heavy-duty truck OEMs, specialist autonomous technology developers, and diversified Tier-1 suppliers. Major OEMs including Daimler Truck AG, AB Volvo, and Paccar Inc. are pursuing vertical integration strategies, acquiring or establishing joint ventures with technology developers. Autonomous-native companies such as Aurora Innovation and Waymo Via are differentiating through proprietary sensor fusion software and safety certification infrastructure.

Key Developments:

- In July 2025, Aeva Inc. expanded its collaboration with Daimler Truck North America LLC (DTNA) to advance the series production of its 4D LiDAR technology for autonomous vehicles. To address rapidly increasing demand, Aeva Inc. plans to establish annual production capacity for up to 200,000 units of 4D LiDAR in North America, targeting support for multiple customers, including DTNA, in deploying advanced sensing technology for autonomous vehicle applications.

- In July 2025, Pronto.ai acquired Safe AI to strengthen Pronto. Ai’s technological capabilities and expand its talent pool by integrating Safe AI’s 12-member engineering team and intellectual property, which enhances Pronto.ai’s position in the autonomous haulage systems market, supporting its strategy to accelerate the deployment of advanced self-driving technologies for commercial and industrial applications.

Global Autonomous Trucks Report - Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 23.6 Bn |

|

Current Market Value (2026) |

US$ 47.5 Bn |

|

Projected Market Value (2033) |

US$ 115.3 Bn |

|

CAGR (2026-2033) |

13.5% |

|

Leading Region |

North America, 40% share |

|

Dominant Application |

L2 & L3 autonomy segment, 48% share |

|

Top-ranking Product |

Diesel, 58% |

|

Incremental Opportunity |

US$ 67.6 Bn |

Companies Covered in Autonomous Trucks Market

- Daimler Truck AG

- AB Volvo

- PACCAR Inc.

- Tesla

- Waymo LLC

- Aurora Innovation, Inc.

- CreateAl Holdings Inc.

- PlusAI, Inc.

- Applied Intuition, Inc.

- Nuro, Inc.

Frequently Asked Questions

The global Autonomous Trucks market is estimated at US$ 47.5 Bn in 2026 and is projected to reach US$ 115.3 Bn by 2033, expanding at a CAGR of 13.5% over the forecast period.

The primary drivers include a severe and worsening commercial driver shortage exceeding 80,000 vacancies in the U.S. per the American Trucking Associations and tightening emissions regulations such as the EPA Phase 3 GHG Standards and the EU Fit for 55 packages.

Heavy Duty Trucks (Class 7 and 8) are the dominant segment, accounting for approximately 62% of total market share. Their leadership is attributable to the superior economic return on autonomous technology investment in long-haul, high-mileage freight applications, where elimination of mandatory driver rest periods and reduction in driver wages deliver the greatest operational cost savings.

North America is the leading regional market, representing approximately 38% of global revenue in 2025. The region's dominance is underpinned by the United States' extensive interstate highway network, progressive state-level autonomous vehicle legislation in Texas, Arizona, and California, and the largest concentration of autonomous trucking technology developers globally. The U.S. Department of Transportation's allocation of over US$ 500 Mn toward AV research under the Bipartisan Infrastructure Law further reinforces North America's leadership position.

The leading companies shaping the autonomous trucks market include Waymo Via (Alphabet Inc.), Aurora Innovation, Daimler Truck AG (through Torc Robotics), AB Volvo, Paccar Inc., TuSimple Holdings, Mobileye Global Inc., Knorr-Bremse AG, Navistar International, and UFI Filters.