- Automotive Components & Materials

- Automotive Turbocharger Market

Automotive Turbocharger Market Size, Share, and Growth Forecast 2026 – 2033

Automotive Turbocharger Market by Fuel Type (Gasoline, Diesel), Technology Type (Variable Geometry Turbocharger, Mechanical Turbocharger, Electric Turbocharger), Vehicle Type (Passenger Car, Light Commercial Vehicle, Heavy Commercial Vehicle), and Regional Analysis for 2026–2033

Automotive Turbocharger Market Size and Trend Analysis

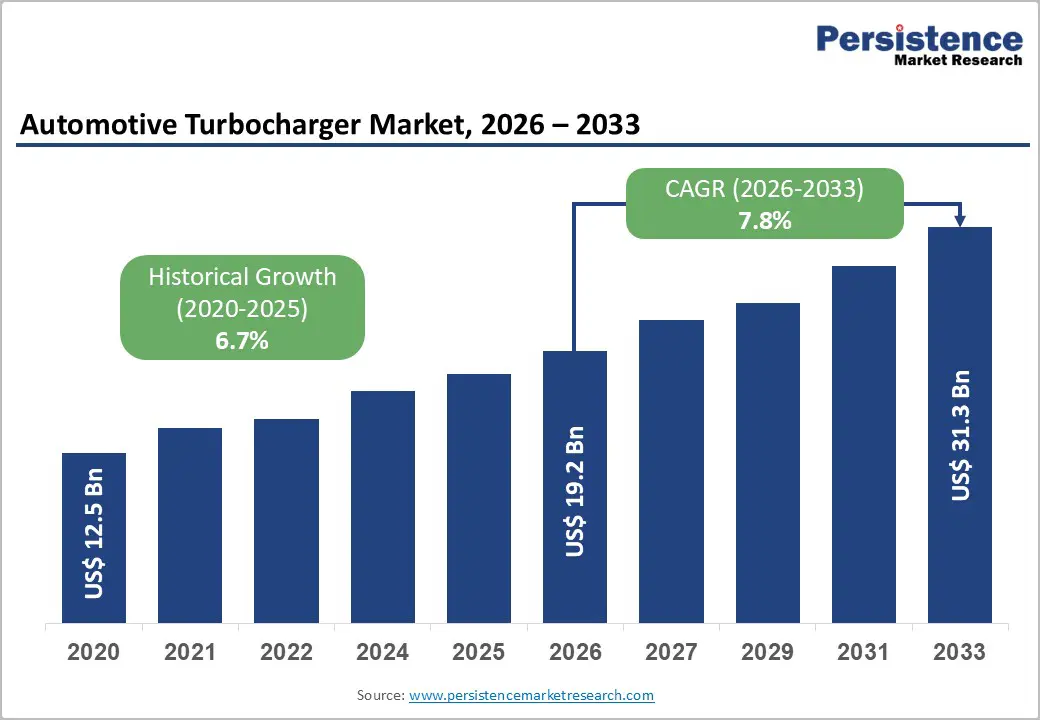

The global automotive turbocharger market size is supposed to be valued at US$ 19.2 billion in 2026 and is projected to reach US$ 31.3 billion by 2033, growing at a CAGR of 7.8% between 2026 and 2033. The market's sustained expansion is driven by increasingly stringent global vehicle emissions regulations compelling automakers to adopt downsized, turbocharged internal combustion engines as the most cost-effective near-term pathway to fuel efficiency and CO2 compliance.

The European Union's CO2 emission standards mandate a fleet-average target of 95 g CO2/km for passenger cars a threshold achievable in turbocharged downsized engines but not in naturally aspirated configurations of equivalent displacement.

Key Industry Highlights:

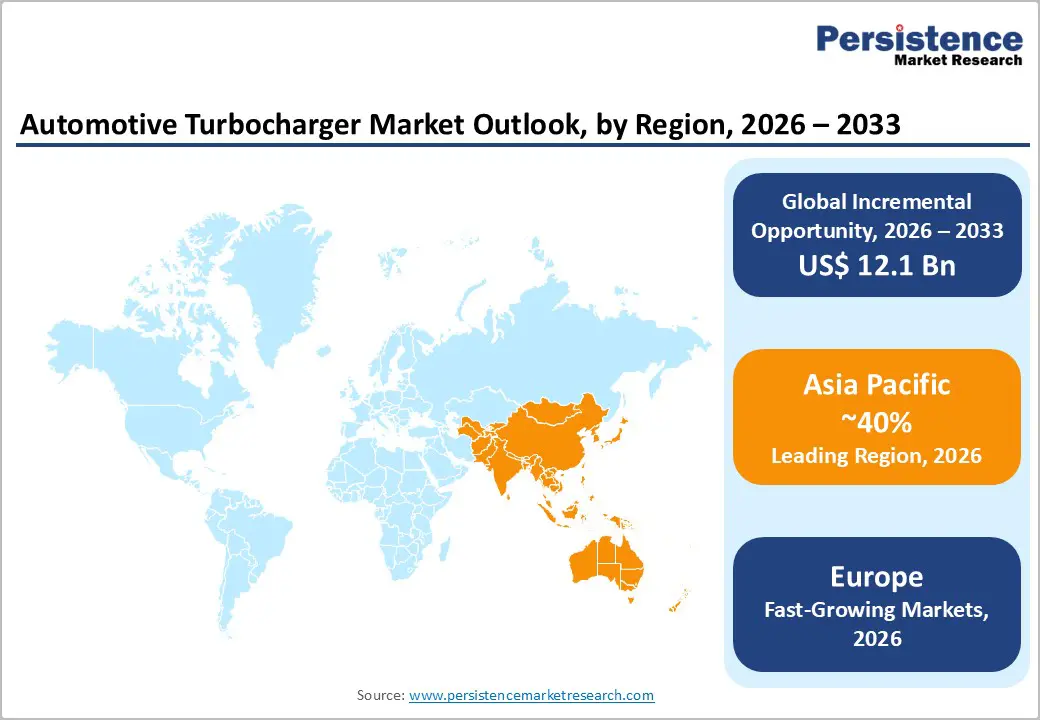

- Leading Region – Asia Pacific leads the global automotive turbocharger market with approximately 43% revenue share in 2026, anchored by China's 30-million-unit annual vehicle production, universal China 6b emission standard compliance requirements, and India's record 4.2 million passenger vehicle sales in FY2023-24.

- Fastest Growing Market – Europe is the global leader in automotive turbocharger adoption by penetration rate, with turbocharged engines representing new vehicle registrations across both diesel and petrol categories.

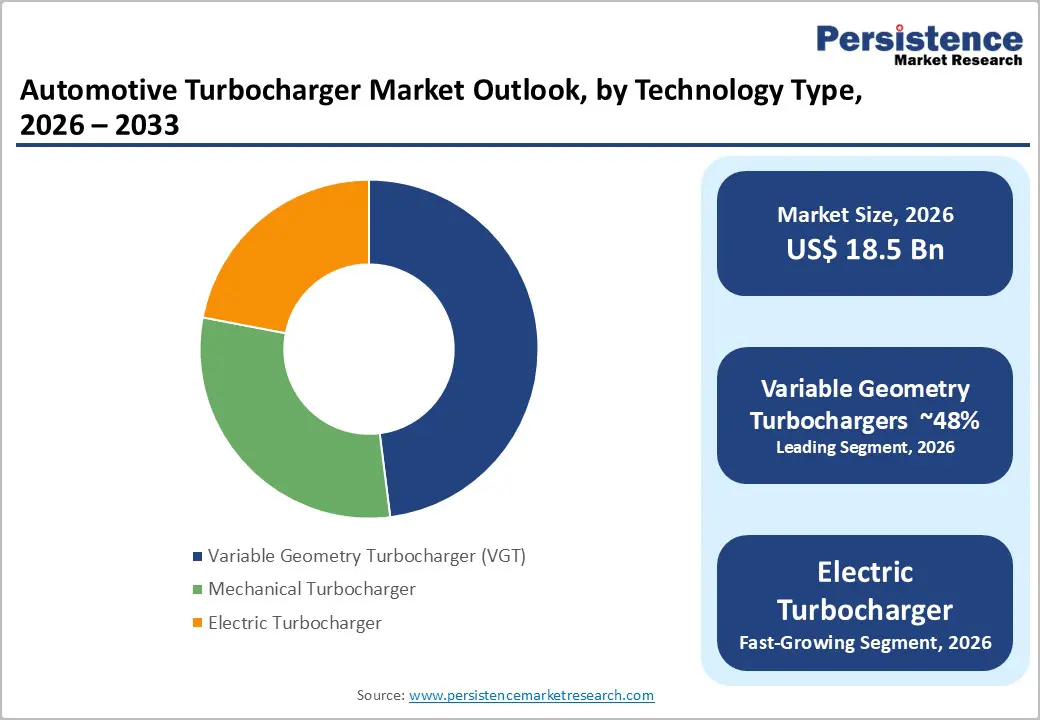

- Dominant Segment – Variable Geometry Turbochargers (VGT) dominate the technology segment with approximately 48% market share in 2026, driven by regulatory demand for optimized combustion efficiency across Euro 6 and China 6b compliant diesel and petrol engines, where VGT's adaptive boost control delivers measurably superior fuel economy and emissions performance.

- Fast-Growing Technology Segment – Electric turbochargers are the fastest-growing technology segment, projected to have a positive CAGR, fuelled by the rapid adoption of 48V mild-hybrid architectures, projected to reach over 20% of global new vehicle sales by 2026 per the ICCT, where e-turbos eliminate lag while enabling energy recovery from exhaust gas flow.

- Key Opportunity – The market opportunity lies in electric turbocharger development for 48V mild-hybrid and full-hybrid platforms, a segment where Garrett Motion and BorgWarner have established early commercial positions offering OEMs a cost-effective compliance and performance bridge as the industry navigates the decade-long transition from ICE to full electrification.

DRO Analysis

Drivers – Stringent Global Emissions Regulations Mandate Engine Downsizing and Boosting Technology

Global automotive emissions frameworks are the single most powerful structural driver of turbocharger adoption, as turbocharged downsized engines deliver equivalent or superior power output at significantly reduced displacement, directly satisfying both CO2fleet average targets and real-world driving emissions standards.

The European Union enforces a fleet-average CO2 limit of 95 g/km for passenger cars, with a tightened target of 93.6 g/km phasing in from 2025 under EU Regulation 2019/631. In the United States, the U.S. Environmental Protection Agency (EPA) and National Highway Traffic Safety Administration (NHTSA) set Corporate Average Fuel Economy (CAFE) standards requiring passenger car fleets to achieve approximately 49 mpg by 2026.

Robust Growth in Global Vehicle Production Sustaining Turbocharger Fitment Volumes

Global vehicle production volumes, recovering strongly from pandemic-era supply chain disruption, are providing a favorable demand backdrop for automotive turbocharger manufacturers. The International Organization of Motor Vehicle Manufacturers (OICA) reported global motor vehicle production of approximately 93.5 million units in 2023, the highest since 2019, with production concentrated in China, the United States, Japan, India, and Germany.

Turbocharger fitment rates have materially outpaced overall production growth: the European Automobile Manufacturers' Association (ACEA) estimates that over 90% of new diesel passenger cars sold in Europe are turbocharged, while gasoline turbocharger penetration in European new car registrations has exceeded 60%.

Restraints - Accelerating Electric Vehicle Transition, Reducing Long-Term ICE Turbocharger Demand

The global pivot toward battery electric vehicles (BEVs), which do not require turbochargers, represents the most significant structural headwind to the automotive turbocharger market over the forecast horizon. The International Energy Agency (IEA) reported that global BEV sales reached 14 million units in 2023, representing approximately 18% of global new car sales, with penetration rates exceeding 40% in China and 25% in Europe.

As BEV penetration accelerates toward regulatory mandates, the EU's effective ban on new ICE passenger car sales from 2035 and multiple automaker-specific phase-out commitments, the total addressable turbocharger market for passenger cars faces progressive volume erosion in mature economies over the 2030s, creating revenue concentration risk for turbocharger manufacturers heavily exposed to the European and Chinese passenger car segments.

Raw Material Price Volatility and Supply Chain Complexity Compressing Manufacturer Margins

Automotive turbochargers are precision-engineered components requiring high-temperature nickel-based superalloys, titanium aluminide turbine wheels, and specialized bearing systems, all of which are subject to significant commodity price volatility. Nickel prices on the London Metal Exchange (LME) experienced extreme volatility in 2022, spiking above US$ 100,000 per metric tonne before normalizing, creating acute margin pressure for turbocharger manufacturers with fixed-price OEM supply contracts.

The geographic concentration of rare earth and specialty metal processing, with China controlling over 85% of global rare earth refining capacity per the U.S. Geological Survey (USGS) introduces supply chain resilience risk that is difficult and expensive to hedge, particularly for electric turbocharger variants that incorporate rare earth permanent magnets.

Opportunities - Electric Turbocharger Adoption in Hybrid Powertrains Opening High-Value Growth Segment

The emergence of 48-volt mild hybrid and full hybrid powertrain architectures is creating a high-growth, high-value application for electric turbochargers (e-turbos) that eliminates the traditional turbo lag limitation while enabling energy recovery from exhaust gases. Garrett Motion, a leading turbocharger specialist, began supplying its first commercial 48V electric turbocharger in 2021 for the Mercedes-AMG inline-six engine, achieving near-instantaneous boost response across the full RPM range.

The International Council on Clean Transportation (ICCT) projects that 48V mild hybrid penetration in new global vehicle sales will reach over 20% by 2026 as automakers seek a cost-effective bridge technology between conventional ICE and full BEV powertrains. For turbocharger manufacturers, e-turbo content per vehicle is significantly higher in value than conventional turbochargers, offering a structural average selling price uplift that can partially offset passenger car volume erosion from BEV substitution.

Heavy Commercial Vehicle Electrification Limitations: Sustaining Long-Term Diesel Turbocharger Demand

Unlike passenger cars, heavy commercial vehicles (HCVs), including long-haul trucks, mining equipment, construction machinery, and marine applications, face barriers to full electrification due to payload limitations of current battery technology, refuelling time constraints, and the total cost of ownership disadvantage of battery-electric HCVs on long-haul routes.

The European Automobile Manufacturers' Association (ACEA) confirms that diesel engines will remain the dominant powertrain for European heavy trucks through at least 2030, with turbochargers being a universal fitment across all displacement categories. In India, the Ministry of Road Transport and Highways (MoRTH) projects commercial vehicle sales reaching 5 million units annually by 2030 as logistics infrastructure investment accelerates under the PM Gati Shakti national master plan.

Category-wise Analysis

Fuel Type Insights

Gasoline is the leading fuel type segment in the automotive turbocharger market, accounting for approximately 58% of total market share in 2025. Gasoline turbocharger dominance has been driven by the explosive growth of turbocharged petrol engines in the global passenger car segment, particularly as automakers responded to CO2 regulations by replacing naturally aspirated four- and six-cylinder petrol engines with smaller, more efficient turbocharged three- and four-cylinder units delivering equivalent performance.

Volkswagen Group's EA211 TSI engine family and Ford's EcoBoost range are emblematic of this transition, with turbocharged gasoline powertrains now representing most new passenger car registrations in Europe, North America, and China. The Society of Automotive Engineers (SAE) has documented continuous gains in specific power output and thermal efficiency from gasoline direct injection combined with turbocharging (TGDI), reinforcing the technology's relevance in increasingly hybrid-heavy powertrain portfolios.

Technology Type Insights

Variable Geometry Turbochargers (VGT) represent the dominant technology segment, commanding approximately 48% of the global automotive turbocharger market in 2026. VGT technology, which uses adjustable vanes in the turbine housing to optimize exhaust gas flow across a wide engine speed range, delivers superior low-end torque response, reduced turbo lag, and better fuel economy compared to fixed-geometry alternatives, making it the preferred specification for both diesel passenger cars and commercial vehicles in regulatory-constrained markets.

Garrett Motion, BorgWarner, and Mitsubishi Turbocharger and Engine Europe (MTEE) have established VGT as the de facto standard for European diesel applications, with over 95% of European diesel passenger cars fitted with variable geometry systems.

Vehicle Type Insights

Passenger cars constitute the leading vehicle type segment, representing approximately 62% of the global automotive turbocharger market share in 2026. The passenger car segment's dominance reflects both the sheer volume of global passenger vehicle production, as the OICA recorded approximately 69 million passenger cars produced globally in 2023, and the near-universal adoption of turbocharged powertrains across mainstream and premium segments in response to fuel economy and emissions mandates.

In Europe, turbocharger fitment rates for new passenger cars have exceeded 80% across both petrol and diesel engines, per ACEA data. In China, the CAAM reports that turbocharged engine penetration in domestic passenger car production exceeded 55% in 2023 and continues to rise as automakers comply with fuel consumption limits under the New Energy Vehicle (NEV) dual-credit policy that simultaneously incentivizes EV and efficient ICE deployment.

Regional Analysis

North America Automotive Turbocharger Market Trends & Analysis

North America is a well-established and growing market for automotive turbochargers, driven by a combination of EPA CAFE standards tightening, the widespread adoption of turbocharged gasoline direct injection engines by domestic OEMs, and robust commercial vehicle production. The United States and Canada together represent one of the world's largest light vehicle markets, with the OICA reporting North American light vehicle production of approximately 15.8 million units in 2023.

U.S. Automotive Turbocharger Market Size

The United States is the primary turbocharger market within North America, representing a leading market revenue in 2026, with an estimated market value of approximately US$ 2.8 Bn.

The U.S. market growth is defined by the dominant consumer preference for light trucks and SUVs. Ford’s F-150, the best-selling vehicle in America for over 40 consecutive years, is now available exclusively with turbocharged EcoBoost gasoline engines, and with the increasing penetration of turbocharged powertrains across Japanese and Korean brand compacts.

Europe Automotive Turbocharger Market Trends, Drivers, & Insights

Europe is the global leader in automotive turbocharger adoption by penetration rate, with turbocharged engines representing most new vehicle registrations across both diesel and petrol categories. ACEA data confirms that over 90% of new diesel passenger cars and more than 75% of new petrol passenger cars sold in Europe are turbocharged, the highest regional fitment rates globally.

Germany Automotive Turbocharger Market Size

Germany is Europe's largest automotive turbocharger market, with an estimated market value of approximately US$ 1.4 Bn in 2026, underpinned by its position as home to Volkswagen Group, BMW Group, Mercedes-Benz Group, and Porsche AG, four of the world's largest turbocharger end-users. The Verband der Automobilindustrie (VDA) reported German domestic passenger car production of approximately 4.1 million units in 2023, with virtually all diesel and most petrol engines featuring turbocharging.

U.K. Automotive Turbocharger Market Size

The United Kingdom's automotive turbocharger market is estimated at approximately US$ 620 Mn in 2026, supported by strong OEM activity from Jaguar Land Rover (JLR), MINI (BMW Group), and Vauxhall (Stellantis), all of which deploy turbocharged powertrains extensively across their model ranges.

France Automotive Turbocharger Market Size

France's automotive turbocharger market is estimated at approximately US$ 510 million in 2026, driven by strong domestic production from Stellantis (which incorporates Peugeot, Citroën, and Opel/Vauxhall brands) and Renault Group, both of which deploy turbocharged petrol and diesel engines across their high-volume European platforms.

Asia Pacific Automotive Turbocharger Market Drivers & Analysis

Asia Pacific is the largest regional market for automotive turbochargers globally, accounting for approximately 43% of total market revenue in 2026, driven by the region's commanding share of global vehicle production, rapidly tightening national emissions standards across China, India, Japan, and South Korea, and the growth of turbocharged engine adoption in the world's largest and fastest-growing automotive markets.

China Automotive Turbocharger Market Size

China is the world's largest single automotive turbocharger market, with an estimated market value of approximately US$ 5.8 billion in 2026, reflecting the country's dominant position in global vehicle production and the near-universal fitment of turbochargers on new ICE and hybrid passenger cars to comply with China 6b emission standards.

India Automotive Turbocharger Market Size

India's automotive turbocharger market is estimated at approximately US$ 820 million in 2026 and is among the fastest-growing national markets globally, driven by record passenger vehicle production, the complete roll-out of Bharat Stage VI (BS-VI Phase 2) emission norms from April 2023, and rapid growth in turbocharged diesel commercial vehicle production.

Japan Automotive Turbocharger Market Size

Japan's automotive turbocharger market is estimated at approximately US$ 1.1 billion in 2026, anchored by the country's role as a global automotive production hub and as the home of three of the world's largest turbocharger manufacturers, HI Corporation, Mitsubishi Heavy Industries Turbocharger and Engine Europe (MHIENG), and Toyota Industries Corporation.

Competitive Landscape

The global automotive turbocharger market is moderately consolidated, with four multinational Tier-1 suppliers, Garrett Motion, BorgWarner Inc., IHI Corporation, and Mitsubishi Heavy Industries (MHI) collectively controlling approximately 65–70% of global OEM turbocharger supply by revenue. These leaders compete on technology differentiation (VGT, electric turbo, twin-scroll), global OEM qualification reach, and manufacturing cost efficiency. Honeywell's former turbo division, now operating independently as Garrett Motion following its 2018 spin-off, retains the broadest passenger car OEM customer portfolio.

Key Developments:

- In April 2025, Cummins launched its industry-first hydrogen internal combustion engine turbocharger for on-highway applications in Europe, featuring advanced aerodynamics and prognostics to address hydrogen’s combustion challenges.

- In January 2025, Cummins launched its next-generation 6.7L Turbo Diesel engine for Ram Heavy Duty trucks, featuring a new variable-geometry turbocharger and improved air management for higher output and serviceability.

Global Automotive Turbocharger Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 12.5 Bn |

|

Current Market Value (2026) |

US$ 19.2 Bn |

|

Projected Market Value (2033) |

US$ 31.3 Bn |

|

CAGR (2026-2033) |

7.8% |

|

Leading Region |

Asia Pacific, 43% share |

|

Dominant Application |

Variable Geometry Turbochargers, 62% share |

|

Top-ranking Product |

Variable Geometry Turbochargers, 48% |

|

Incremental Opportunity |

US$ 12.1 Bn |

Companies Covered in Automotive Turbocharger Market

- Garrett Motion

- BorgWarner,

- IHI Corporation

- MHIET

- Continental AG (Vitesco)

- Bosch Mahle Turbo Systems

- Toyota Industries

- Cummins

- Hunan Tyen Machinery

- OTICS Corporation

- UFI Filters

- Turbo Energy Private Limited

- Mahle GmbH

- AVL List GmbH

Frequently Asked Questions

The global automotive turbocharger market is estimated at US$ 19.2 billion in 2026 and is projected to reach US$ 31.3 billion by 2033, growing at a CAGR of 7.8% over the forecast period.

The two demand drivers are global vehicle emissions regulations and sustained vehicle production growth. The EU's fleet-average CO₂ limit of 95 g/km, China's 6b emission standards effective July 2023, and the EPA's CAFE standards collectively mandate turbocharged engine architectures as the most cost-effective compliance pathway for ICE-reliant automakers.

Passenger Cars dominate the automotive turbocharger market, accounting for approximately 62% of global revenue in 2026. The segment's leadership reflects the sheer scale of global passenger vehicle production, approximately 69 million units in 2023 per OICA, and the near-universal adoption of turbocharged powertrains in response to CO₂ and fuel economy regulations across Europe, China, and increasingly North America.

Asia Pacific leads the global automotive turbocharger market with approximately 43% of total revenue in 2026. China is the world's largest vehicle production market, with approximately 30 million units annually, where China's 6b Phase 2 emission standards have mandated universal turbocharger adoption across new ICE and hybrid production.

The global automotive turbocharger market is led by Garrett Motion Inc. (Switzerland), BorgWarner Inc. (U.S.), IHI Corporation (Japan), and Mitsubishi Heavy Industries Engine & Turbocharger (MHIET) (Japan), which collectively account for approximately 65–70% of global OEM supply revenue.