- Automotive Components & Materials

- Automotive Inverter Market

Automotive Inverter Market Size, Share, and Growth Forecast 2026 - 2033

Automotive Inverter Market by Propulsion Type (Battery Electric Vehicle (BEV), Hybrid Electric Vehicle (HEV), Plug-in Hybrid Electric Vehicle (PHEV), Fuel Cell Electric Vehicle (FCEV)), Vehicle Type (Passenger Vehicles, Commercial Vehicles), End-user (OEM, Aftermarket), Regional Analysis, 2026 - 2033

Automotive Inverter Market Size and Trend Analysis

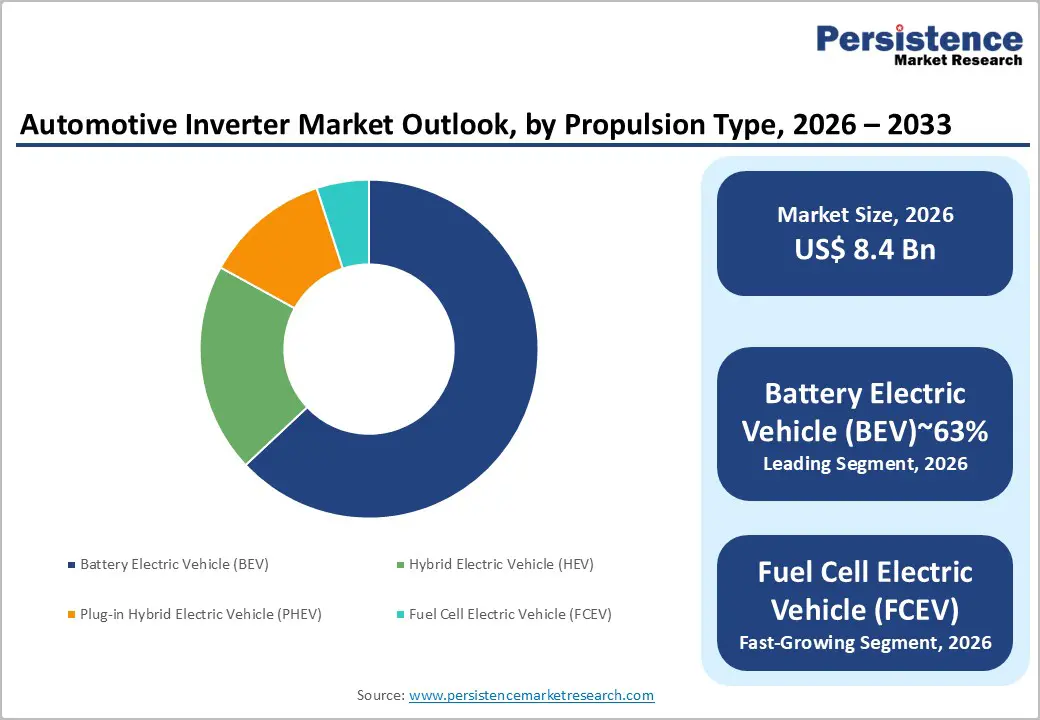

The global automotive inverter market is expected to be valued at US$ 8.40 billion in 2026 and is projected to reach US$ 25.51 billion by 2033, growing at a CAGR of 17.2% between 2026 and 2033.

The silicon carbide (SiC) semiconductor transition is restructuring traction inverter supply chains faster than any previous EV powertrain technology shift, forcing inverter manufacturers to renegotiate wafer supply agreements and redesign thermal management architectures simultaneously.

Key Industry Highlights:

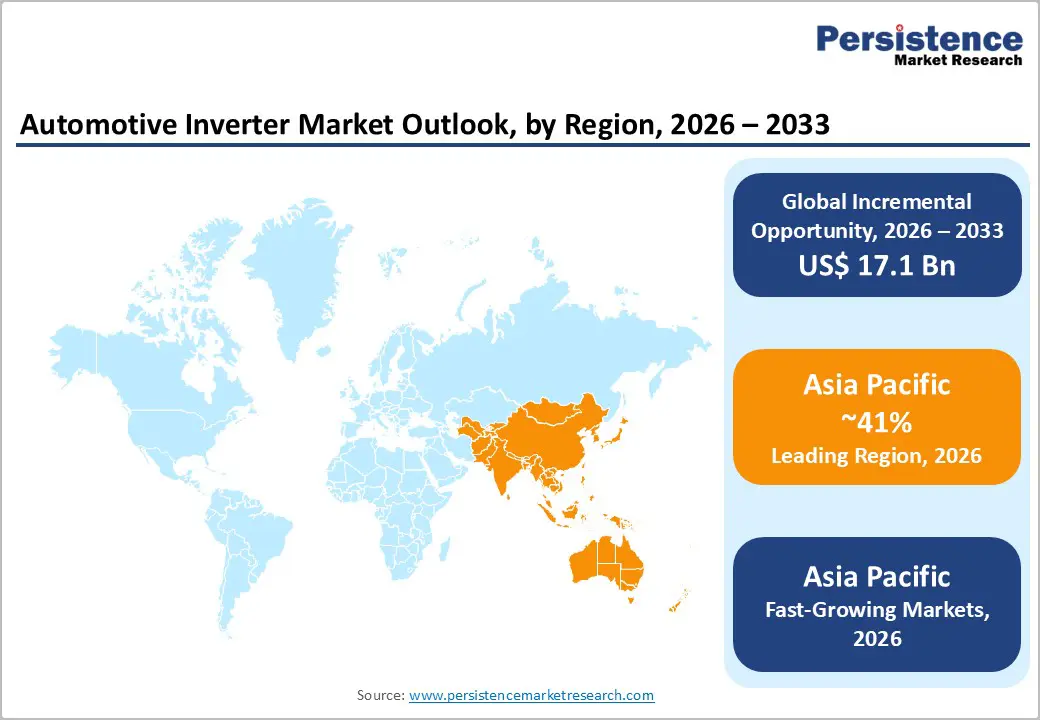

- Leading Region: Asia Pacific commands 41% of global automotive inverter revenue in 2026, representing US$ 3.44 billion, underpinned by China's NEV mandate-driven OEM production volumes and Japan's multi-propulsion electrification strategy spanning HEV, BEV, and FCEV platforms, a regional breadth that no other geography replicates and that sustains the region's 21.5% CAGR through 2033.

- Leading Segment: BEV drivetrains account for 63.0% of inverter segment revenue, equivalent to US$ 5.29 billion in 2026, because every BEV requires at least one dedicated traction inverter with no hybrid or combustion fallback, making the segment's revenue concentration structurally irreversible as long as BEV production volumes continue their upward trajectory.

- Fast-Growing Segment: FCEV-related inverter demand is the fast-growing sub-segment, with Hyundai's XCIENT Fuel Cell truck deployments in European freight and Toyota's Mirai fleet expansions establishing repeatable commercial use cases that will scale as the European Clean Hydrogen Alliance's 40 GW electrolyser target improves hydrogen fuel availability along established transport corridors after 2026.

- Key Opportunity: Integrated e-Axle systems represent the highest-value strategic opportunity in the automotive inverter space, as demonstrated by ZF Friedrichshafen's MEA3 launch in 2024. Suppliers capable of delivering inverter, motor, and gearbox as a validated single assembly capture two to three times the per-vehicle revenue of stand-alone inverter vendors and benefit from switching costs that make mid-cycle platform substitution commercially prohibitive for OEM engineering teams.

Market Dynamics

Drivers - Mandatory Fleet Electrification Targets Accelerating Inverter Procurement Volumes

Automakers sourcing traction inverters at scale must now plan procurement cycles around legally binding electrification mandates, which transforms inverter demand from discretionary to contractually obligated.

The U.S. Environmental Protection Agency's (EPA) Light-Duty Vehicle Greenhouse Gas Standards finalised in March 2024 project that EVs must represent approximately 67% of new light-duty vehicle sales by 2032, and General Motors committed in 2023 to an all-electric passenger lineup by 2035, anchoring multi-year inverter supply agreements with tier-one power electronics suppliers. Over the next two to three years, this regulatory pipeline will force inverter makers to expand SiC module production capacity or risk being locked out of platform nominations by automakers finalising their 2026-2028 model architectures.

SiC-Based Power Electronics Delivering Efficiency Gains That Justify Premium Platform Adoption

Automotive-grade SiC inverters reduce switching losses by approximately 40% compared to conventional IGBT technology, enabling longer driving range per charge cycle, a performance differential that OEM engineering teams now treat as a non-negotiable threshold for next-generation EV powertrain specifications.

Infineon Technologies AG launched its CoolSiC automotive MOSFET module series in 2023, targeting 800-volt EV architectures and securing design wins with European and Korean automakers integrating high-voltage e-Axle platforms. As 800-volt charging infrastructure proliferates, CharIN's high-power charging standards now support up to 350 kW peak delivery; the efficiency advantage of SiC-based DC-AC conversion will become a baseline expectation rather than a premium differentiator within three years.

Restraints - SiC Wafer Supply Constraints, Compressing Margins and Extending Lead Times

Automotive-grade SiC wafer shortages create a cost floor that prevents inverter manufacturers from passing full efficiency benefits to OEM customers at competitive price points, effectively compressing gross margins for inverter producers caught between rising input costs and downward pricing pressure from automakers.

The U.S. Department of Commerce identified SiC substrates as a critical semiconductor input under the CHIPS and Science Act of 2022, yet domestic six-inch SiC wafer capacity remains insufficient to meet projected automotive demand through at least 2026, with qualified wafer lead times extending to 52 weeks per industry procurement data. New entrants face a structurally disadvantaged position because established players such as Wolfspeed hold long-term wafer supply agreements that effectively gate access to the substrate supply chain.

High Development and Qualification Costs Creating Barriers for Tier-Two Suppliers

Automotive inverter qualification under AEC-Q101 reliability standards for power semiconductors requires testing cycles spanning 12 to 18 months and investment in dedicated validation infrastructure, a cost burden that disproportionately affects smaller tier-two suppliers attempting to enter the market.

The China Automotive Technology and Research Center (CATARC) mandates separate domestic certification pathways for power electronics used in vehicles sold in China, adding regulatory duplication costs estimated at 15% of total product development budgets for non-domestic entrants. This dual-qualification burden effectively narrows the competitive field, entrenching established tier-one inverter suppliers across both Western and Chinese automotive ecosystems.

Opportunities - Integrated E-Axle Systems Opening a High-Value Adjacent Market for Full-Stack Inverter Suppliers

Power electronics suppliers capable of delivering fully integrated e-Axle units, combining the inverter, motor, and gearbox into a single assembly, can capture significantly higher per-vehicle revenue than stand-alone inverter vendors, creating a compelling case for vertical integration investment.

ZF Friedrichshafen AG launched its MEA3 e-Axle in 2024, targeting both passenger cars and light commercial vehicles, demonstrating that the integration trend is accelerating across vehicle segments and is not limited to premium platforms. Suppliers that secure e-Axle platform nominations before automakers finalise 2027-2029 model architectures will lock in recurring volume that is extremely difficult for competitors to displace mid-cycle.

Emerging FCEV Heavy Transport Applications Unlocking a New Inverter Demand Pool

Hydrogen fuel cell electric vehicle deployments in long-haul freight and port logistics create a distinct inverter demand pool characterised by higher power ratings and longer duty cycles than passenger car applications, rewarding suppliers with industrial-grade thermal management expertise.

Hyundai Motor Company's XCIENT Fuel Cell heavy truck, deployed across Swiss freight operators since 2020 and expanded to European corridors through 2024, requires bespoke high-voltage inverter systems rated above 350 kW, a specification tier that commodity passenger-car inverter makers cannot address without significant redesign investment. Specialised power electronics firms with existing traction inverter portfolios for rail or industrial applications are best positioned to capture this segment, provided they complete automotive-grade qualification before FCEV heavy transport fleet procurement scales meaningfully after 2026.

Category-wise Analysis

Propulsion Type Insights

The battery electric Vehicle (BEV) segment accounts for 63% of the global automotive inverter market in 2026, equivalent to US$ 5.29 billion, highlighting the segment’s strong and long-term dominance in inverter demand because every BEV requires a dedicated high-voltage traction inverter as a core drivetrain component.

According to the SAE International 2024 EV technology outlook, BEV drivetrains now achieve inverter power density levels above 50 kW per litre, strengthening the position of established suppliers and limiting platform changes for automakers. Meanwhile, the FCEV segment is growing steadily due to government-supported hydrogen corridor projects that encourage fleet deployment in applications where battery weight and charging downtime remain operational challenges.

Vehicle Type Insights

The passenger vehicles segment accounts for 95% of the global automotive inverter market in 2026, equivalent to US$ 7.98 billion, mainly driven by the significantly larger production volume of passenger electric vehicles compared to electrified commercial vehicles, which are still in the early stages of large-scale adoption. The segment’s dominance is strongly linked to rising consumer demand for electric passenger cars, including models such as the Volkswagen ID.4 and Hyundai IONIQ 6, both of which rely on dedicated three-phase traction inverters as a key part of their powertrain systems.

According to the European Automobile Manufacturers' Association, battery electric passenger car registrations in the European Union reached 1.5 million units in 2023, with each vehicle requiring at least one inverter assembly, reinforcing the segment’s leading revenue contribution. At the same time, the Commercial Vehicles segment is gaining momentum as logistics companies and public transit authorities accelerate fleet electrification to meet strict decarbonisation targets, creating growing demand for high-power inverter systems.

End-user Insights

The OEM segment accounts for 85% of the global automotive inverter market in 2026, equivalent to US$ 7.14 Billion, as automotive inverters are highly specialised and safety-critical drivetrain components designed specifically for individual vehicle platforms, making OEM procurement the primary sales channel. A strong example is BorgWarner Inc. and its Viper inverter platform, which is integrated into several European and North American vehicle programmes during the design stage and validated according to strict thermal cycling and electromagnetic compatibility standards.

This process makes the inverter an essential and non-replaceable part of the vehicle platform. According to the Japan Automobile Manufacturers Association, Japanese automakers produced more than 8 million electrified vehicles in fiscal year 2023, creating large-scale captive demand through OEM supply channels. Meanwhile, the Aftermarket segment is gradually expanding as ageing EV fleets move beyond warranty periods, increasing the need for inverter replacement, repair, and performance upgrade services across independent EV service networks worldwide.

Regional Insights

North America Automotive Inverter Market Trends and Insights

North America accounts for 20% of the global automotive inverter market in 2026, representing US$ 1.68 billion, with growth underpinned by the Inflation Reduction Act of 2022, which introduced a US$ 7,500 consumer EV tax credit contingent on North American battery and critical mineral sourcing requirements that incentivise domestic inverter supply chain development. The Act's domestic content provisions are reshaping tier-one inverter supplier facility decisions, with multiple Asian component makers announcing U.S. manufacturing investments to maintain eligibility within the OEM supply chain.

Over the forecast period, North America's inverter market will benefit disproportionately as automakers accelerate localisation of power electronics manufacturing to comply with evolving content thresholds.

- United States Automotive Inverter Market Size

The United States represents an estimated 82% of the North America automotive inverter market, approximately US$ 1.38 billion in 2026, driven by Ford Motor Company's BlueOval City investment programme in Tennessee, which brings dedicated EV and inverter-adjacent powertrain manufacturing capacity online through 2025-2026. As federally funded charging infrastructure under the Bipartisan Infrastructure Law expands EV range confidence among consumers, new-vehicle EV conversion rates will sustain inverter demand growth through the forecast period.

Europe Automotive Inverter Market Trends and Insights

Europe accounts for 26.0% of the global automotive inverter market in 2026, representing US$2.18 billion, with the European Green Deal and its binding fleet CO2 targets requiring new passenger car emissions to reach zero by 2035, driving automakers to commit capital to EV platform transitions that generate multi-year inverter sourcing obligations. The European Chips Act of 2023, with its €43 billion semiconductor investment objective, is creating downstream incentive for SiC inverter module production within the EU. Europe's regulatory visibility through 2035 makes it the market with the clearest long-term demand visibility for inverter manufacturers evaluating capacity expansion decisions.

- Germany Automotive Inverter Market Size

Germany represents an estimated 35% of the European automotive inverter market, approximately US$ 763 million in 2026, anchored by Volkswagen Group's accelerated rollout of its MEB electric platform across multiple brands, each requiring standardised inverter modules procured at scale from qualified tier-one suppliers. Germany's dense automotive OEM and tier-one supplier ecosystem creates compounding inverter demand as platform electrification cascades across model lines through 2028.

- United Kingdom Automotive Inverter Market Size

The United Kingdom represents an estimated 14% of the European automotive inverter market, approximately US$ 305 Million in 2026, supported by the Zero Emission Vehicle (ZEV) Mandate, which requires 22% of new car sales to be zero-emission from 2024, creating a statutory floor under EV inverter demand that is independent of consumer sentiment cycles. Jaguar Land Rover's committed transition to an all-electric Jaguar brand by 2025 provides a concrete near-term volume signal for inverter suppliers serving the UK premium segment.

- France Automotive Inverter Market Size

France accounts for an estimated 13% of the European automotive inverter market, approximately US$ 283 Million in 2026, driven by Renault Group's Ampere EV subsidiary strategy, which targets volume BEV production in French facilities and creates captive domestic inverter procurement demand. The French government's bonus écologique incentive scheme, which provides up to €7,000 toward EV purchases for low-income households, is broadening the consumer base acquiring EVs and expanding total inverter-embedded vehicle volumes annually.

Asia Pacific Automotive Inverter Market Trends and Insights

Asia Pacific accounts for 41% of the global automotive inverter market in 2026, representing US$ 3.44 billion, and is the fast-growing region at a CAGR of 21.5% by 2033, propelled by China's position as the world's largest EV production and consumption market and by rapid electrification momentum in Japan, South Korea, and India. China's New Energy Vehicle (NEV) mandate, which requires automakers to earn NEV credits equivalent to 18% of total vehicle sales in 2023, rising progressively, compels both domestic and foreign automakers to source inverters at volumes that no other regional market can match.

The convergence of scale manufacturing, domestic SiC semiconductor development, and export-oriented EV production in the Asia Pacific will sustain the region's structural lead throughout the forecast period.

- China Automotive Inverter Market Size

China represents an estimated 62% of the Asia Pacific automotive inverter market, approximately US$2.13 billion in 2026, reflecting the country's production of over 9 million NEVs in 2023 per China Association of Automobile Manufacturers (CAAM) data, each embedding at least one traction inverter assembly. BYD's vertically integrated powertrain strategy, which includes in-house IGBT and SiC inverter module production at its Fudi subsidiary, demonstrates the depth of domestic inverter manufacturing capability that international suppliers must benchmark against to remain competitive.

- India Automotive Inverter Market Size

India accounts for an estimated 10% of the Asia Pacific automotive inverter market, approximately US$ 344 million in 2026, supported by the PM E-DRIVE scheme, under which the Indian government allocated INR 10,900 crore in 2024 to accelerate EV adoption across two-wheelers, three-wheelers, and electric buses. Tata Motors' Nexon EV, the dominant passenger BEV in India's market, deploys a localised inverter configuration that domestic tier-one suppliers are now engineering around, creating a foundation for indigenous inverter production capacity as volumes scale.

- Japan Automotive Inverter Market Size

Japan represents an estimated 18% of the Asia Pacific automotive inverter market, approximately US$ 619 million in 2026, anchored by Toyota Motor Corporation's hybrid and FCEV inverter volumes, which span the Prius hybrid lineup, the bZ4X BEV, and the second-generation Mirai FCEV, creating a uniquely diversified multi-propulsion inverter demand base. Japan's Green Growth Strategy, targeting 2 million fuel cell vehicles by 2030, provides a long-duration demand signal specifically for the FCEV inverter sub-segment that no other national strategy matches in explicitness.

Competitive Landscape

The global automotive inverter market operates as a concentrated oligopoly at the tier-one level, with Robert Bosch GmbH, DENSO Corporation, and Vitesco Technologies collectively commanding the largest OEM platform nomination positions across European, Japanese, and North American automakers. Competition centres on SiC module integration capability, thermal management architecture, and the ability to deliver vertically integrated e-Axle systems rather than stand-alone inverter units.

Onsemi is the most disruptive entrant, having secured automotive-grade SiC supply agreements with multiple EV platforms through its 2023 long-term supply deal with BMW Group, allowing it to compete at the semiconductor module level rather than the full inverter system level, a go-to-market distinction that separates it from traditional tier-one assemblers. Winners are separating themselves through platform-level co-development agreements signed two to three model cycles in advance; laggards relying on spot supply relationships are being systematically displaced.

Key Developments:

- January 2025: Infineon Technologies AG announced a €5 billion expansion of its SiC semiconductor fabrication facility in Kulim, Malaysia, targeting automotive traction inverter module supply for Asian and European OEMs entering volume production of 800-volt EV platforms from 2026 onward.

- March 2024: Vitesco Technologies completed integration into Schaeffler AG following a merger finalised in late 2023, creating a combined automotive power electronics and bearing systems group with annual revenues exceeding €19 billion, a consolidation explicitly aimed at competing for integrated e-Axle platform nominations against ZF Friedrichshafen AG and BorgWarner Inc.

- September 2024: STMicroelectronics and Renault Group's Ampere subsidiary announced a joint development agreement for next-generation SiC-based traction inverter modules targeting 2027 model-year BEV platforms, with inverter power density targets set 25% above current production benchmarks, a collaboration that signals how automakers are pulling semiconductor suppliers directly into powertrain co-design rather than procuring finished modules from tier-one assemblers.

Companies Covered in Automotive Inverter Market

- Robert Bosch GmbH

- DENSO Corporation

- Mitsubishi Electric Corporation

- ZF Friedrichshafen AG

- Continental AG

- Hitachi Astemo Ltd

- Valeo SA

- Toyota Industries Corporation

- BorgWarner Inc.

- Vitesco Technologies (Schaeffler AG)

- Infineon Technologies AG

- Magna International Inc.

- Nidec Corporation

- onsemi

- STMicroelectronics

- Wolfspeed Inc.

- Rohm Semiconductor

- Texas Instruments Incorporated

- Panasonic Holdings Corporation

- Aptiv PLC

Frequently Asked Questions

The global automotive inverter market is valued at US$8.40 billion in 2026 and is projected to reach US$25.51 billion, growing at a CAGR of 17.2% by 2033.

Rising EV adoption is driving growth in the automotive inverter market. Government support for vehicle electrification, investments in advanced SiC semiconductor production, and expanding electric vehicle fleets are increasing demand for efficient automotive inverters worldwide.

Battery electric vehicles (BEV) hold 63.0% of the global automotive inverter market in 2026 as every BEV unit requires a dedicated high-voltage traction inverter with no combustion or hybrid fallback alternative, creating an inescapable one-to-one relationship between vehicle production and inverter procurement.

Asia Pacific leads the global automotive inverter market with a 41.0% share, US$3.44 billion in 2026, driven by two structural factors: China's NEV credit mandate generating compulsory OEM electrification volumes at an unmatched scale, and Japan's government-backed Green Growth Strategy sustaining simultaneous inverter demand across HEV, BEV, and FCEV propulsion architectures.

The integrated e-Axle segment is likely fuel more opportunities where suppliers delivering combined inverter-motor-gearbox assemblies capture per-vehicle revenue two to three times higher than stand-alone inverter vendors. Tier-one power electronics firms with validated 800-volt thermal management architectures, such as those benchmarked against Porsche's Taycan platform, are best positioned, provided they secure OEM platform nominations before automakers finalise model architectures for 2028-2030 production programmes.

Robert Bosch GmbH, DENSO Corporation, and Mitsubishi Electric Corporation anchor the tier-one competitive set, competing primarily on SiC module integration depth, e-Axle systems capability, and OEM co-development relationships established years ahead of production nominations.