- Automotive Components & Materials

- Automotive Leaf Spring Market

Automotive Leaf Spring Market Size, Share, and Growth Forecast, 2026 - 2033

Automotive Leaf Spring Market by Product Type (Parabolic, Elliptic, Semi-Elliptic, Others), Material Type (Metal, Composite), Vehicle Type (Passenger Car, Light Commercial Vehicle, Heavy Commercial Vehicle), and Regional Analysis for 2026 - 2033

Automotive Leaf Spring Market Share and Trends Analysis

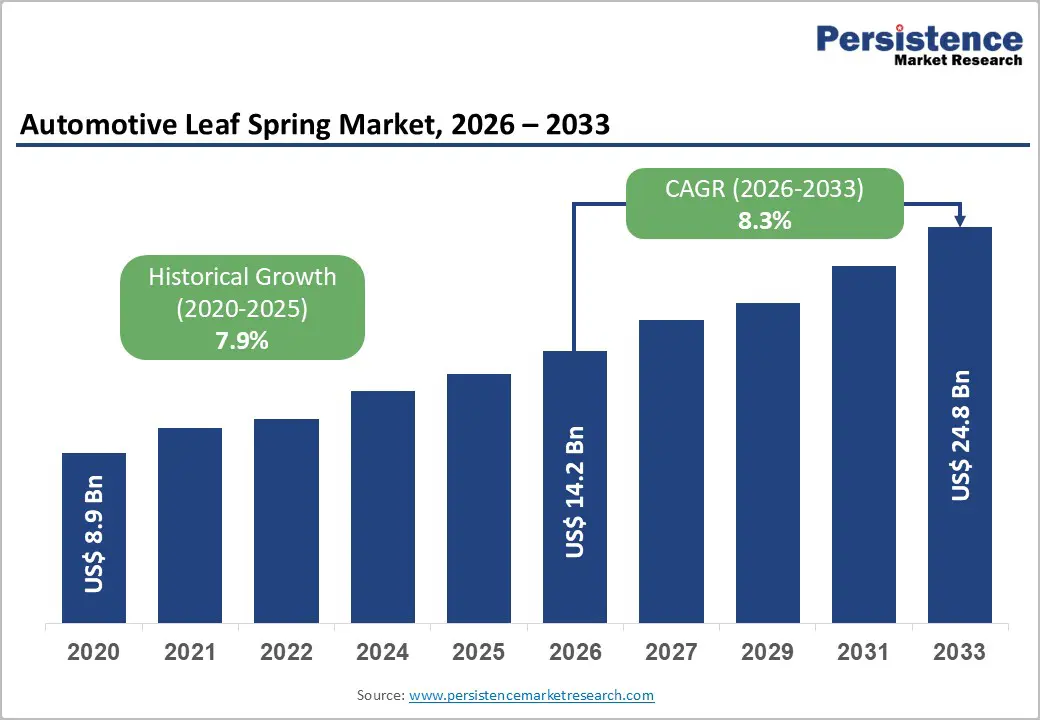

The global automotive leaf spring market size is likely to be valued at US$ 14.2 billion in 2026 and is estimated to reach US$ 24.8 billion by 2033, growing at a CAGR of 8.3% during the forecast period 2026−2033. Market growth is driven by rising freight transportation activity and increasing demand for durable suspension systems in commercial vehicles. Expansion of logistics networks in emerging economies strengthens replacement demand, while industrialization increases vehicle utilization intensity.

Regulatory frameworks from authorities such as the U.S. National Highway Traffic Safety Administration (NHTSA) and the European Commission Directorate-General for Mobility and Transport support standardized suspension adoption for improved stability and load control. Material innovations, including composite and high-strength steel, enhance fatigue resistance and reduce weight, supporting emission reduction goals. Electric commercial vehicle growth and infrastructure-driven long-haul transport expansion further reinforce sustained demand for leaf spring systems.

Key Industry Highlights

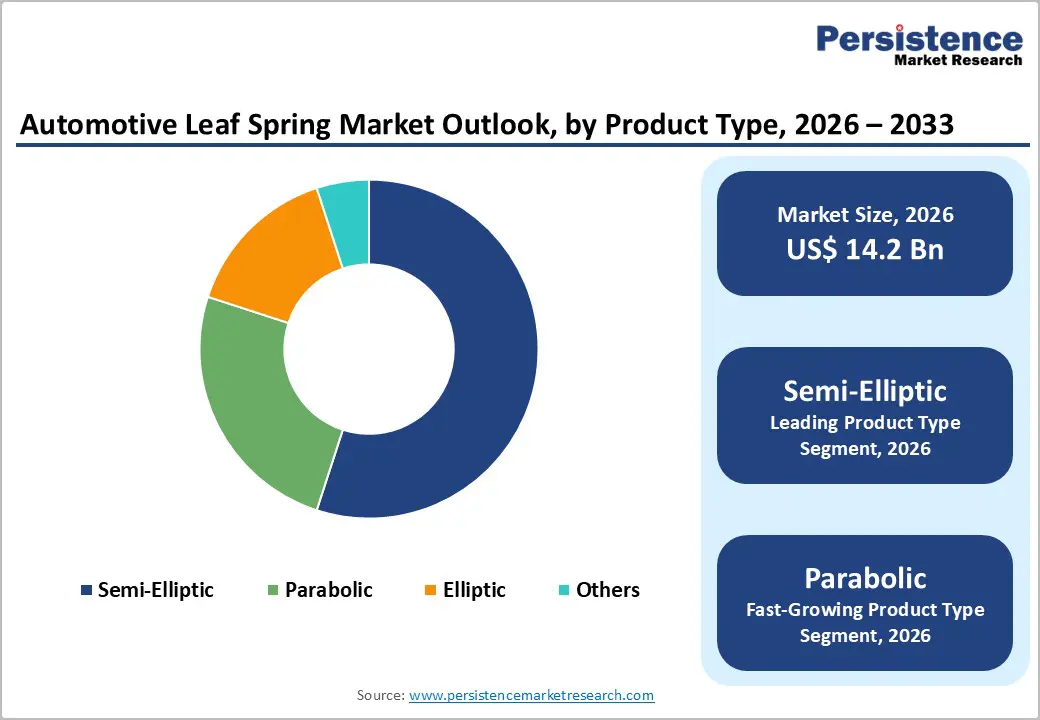

- Leading Product Type: Semi-elliptic segments are expected to command around 55% of revenue in 2026 due to widespread adoption in heavy and light commercial vehicle platforms and strong load-bearing efficiency.

- Fastest-Growing Product Type: Parabolic leaf springs are likely to be the fastest-growing during 2026–2033 due to lightweighting, efficiency gains, improved durability, and OEM adoption.

- Leading Vehicle Type: Heavy commercial vehicles are anticipated to secure around 45% revenue share in 2026 due to sustained freight transport demand and infrastructure-linked logistics expansion.

- Fastest-Growing Vehicle Type: Light commercial vehicles are expected to be the fastest-growing segment during 2026–2033 due to e-commerce logistics and urban delivery fleet expansion.

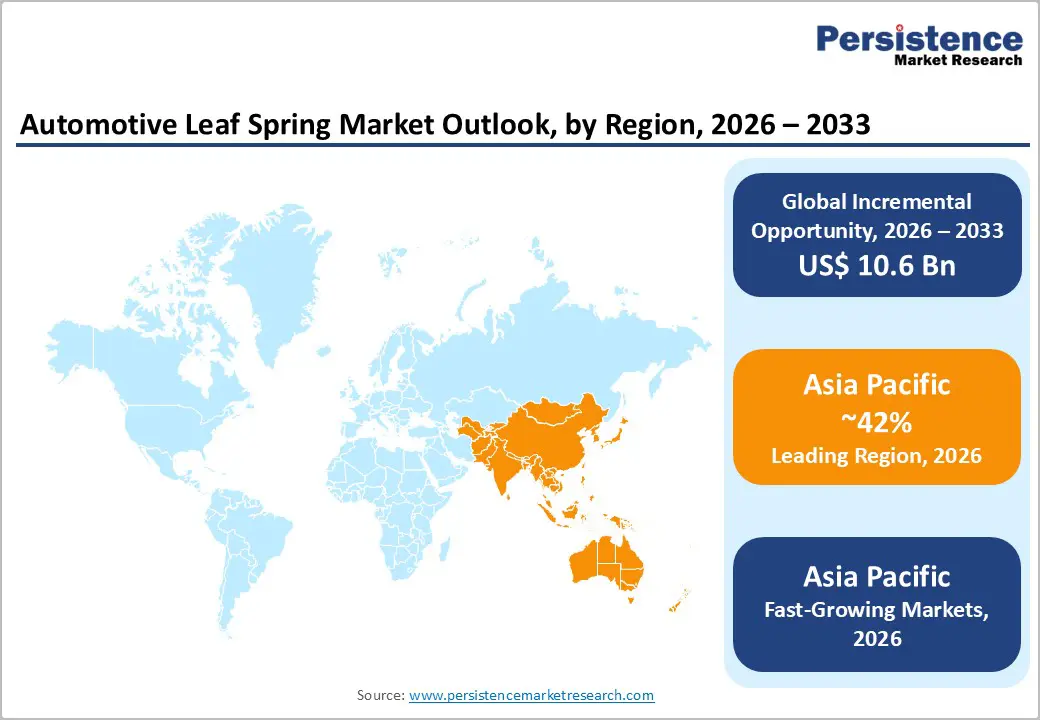

- Regional Leadership: Asia Pacific is expected to lead with an estimated 42% market share in 2026, while Asia Pacific is also forecasted to be the fastest-growing market during 2026–2033, supported by industrialization and electrification trends.

- Competitive Environment: Moderately fragmented structure with strong OEM integration, cost competition, and increasing material innovation focus.

- Innovation Trends: Shift toward composite materials, lightweight engineering, and electrification-compatible suspension redesign.

| Key Insights | Details |

|---|---|

|

Automotive Leaf Spring Market Size (2026E) |

US$ 14.2 Bn |

|

Market Value Forecast (2033F) |

US$ 24.8 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

8.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

7.9% |

DRO Analysis

Driver - Expansion of Commercial Vehicle Production and Logistics Demand

Automotive leaf spring market growth is driven by expansion of commercial vehicle production and logistics demand across global freight corridors. Freight transportation expansion strengthens structural demand for heavy duty trucks and trailers, increasing operational utilization cycles and accelerating suspension wear across long haul routes. According to 2025 data from the U.S. Department of Transportation Bureau of Transportation Statistics, transborder freight reached nearly 1.6 trillion dollars across North American corridors, indicating strong cross border mobility and reinforcing durable suspension requirements. Elevated freight density increases load repetition and accelerates component replacement cycles in commercial fleet operations, driving sustained aftermarket replacement demand growth.

Industrial production scaling and logistics network expansion reinforce demand consistency across commercial vehicle fleets. Manufacturing output growth increases shipment frequency across highway and intermodal routes, requiring suspension systems capable of sustained load stability under variable operating conditions. Fleet operators prioritize robust mechanical architectures to reduce downtime and maintenance interruptions in high utilization environments. Expansion of e commerce logistics ecosystems strengthens short and medium haul transport activity, amplifying daily operational strain on vehicle platforms. These dynamics elevate reliance on leaf spring configurations as cost efficient solutions for load bearing performance across heavy duty and light commercial vehicle categories, supporting fleet efficiency.

Rising Adoption in Aftermarket Replacement Demand

Aftermarket replacement demand strengthens structural consumption cycles across commercial and light duty fleets. Frequent exposure to heavy loads, uneven terrain, and continuous operation accelerates fatigue in suspension assemblies, increasing replacement frequency across maintenance schedules. Fleet operators prioritize cost efficient component renewal to minimize downtime and preserve load stability. Expansion of used vehicle transactions further enlarges replacement activity across independent workshops. 2025 U.S. Department of Transportation Freight Analysis Framework indicates freight ton miles remained above the pre-pandemic baseline index level, signaling sustained logistics intensity across corridors. Supports continuous demand for durable suspension components within aftermarket channels, sustaining operational continuity across fleet ecosystems.

Lifecycle degradation patterns in leaf spring assemblies generate recurring demand across service intervals in transport fleets. Extended operating cycles, heavy payload conditions, variable road quality intensify stress accumulation in steel and composite structures. Fleet managers allocate maintenance budgets toward predictable replacement planning to control operational risk and reduce unscheduled breakdowns. Growth in long distance freight corridors increases wear exposure, raising frequency of suspension refurbishment cycles. Expansion of multi axle commercial platforms reinforces component loading requirements across distribution networks. Rising asset utilization rates across aging vehicle pools strengthen aftermarket penetration, reinforcing stable demand streams across maintenance ecosystems and mobility support providers.

Restraint - Vehicle Lightweighting and Emission Reduction Pressure

Pressure to reduce vehicle mass and emissions influences material selection across suspension systems in Automotive Original Equipment Manufacturer (OEM) programs. Manufacturers prioritize weight reduction to improve fuel efficiency and extend electric driving range. Steel-based leaf springs present limitations due to higher mass compared to aluminum alloys, composites, and air suspension systems. Design transitions reduce dependence on conventional suspension assemblies in passenger and light commercial segments. Emission compliance requirements linked to global carbon frameworks accelerate redesign cycles, increasing substitution risk within new platform development initiatives.

Regulatory tightening across major automotive markets accelerates adoption of lightweight vehicle architectures. Emission targets linked to fleet-wide carbon reduction drive continuous optimization of vehicle dynamics and load efficiency within Automotive OEM strategies. Traditional suspension systems create constraints in achieving lower curb weight objectives, influencing procurement and engineering decisions. Investment shifts toward advanced materials and adaptive suspension technologies reduce focus on conventional steel assemblies. Supplier adaptation pressure rises while legacy product standardization declines, weakening long-term demand stability in efficiency-focused vehicle segments.

Structural Fatigue, Sagging, and Maintenance Requirements

Structural fatigue in leaf spring systems reduces long-term durability under repeated load cycles in commercial vehicles. Continuous stress from uneven road conditions and heavy cargo results in microcrack formation within steel layers, leading to progressive weakening of suspension performance. This degradation increases downtime for inspections and corrective interventions, raising operational costs for fleet operators. Sagging under sustained load further affects ride stability and axle alignment, which limits vehicle efficiency in high-utilization environments. Maintenance requirements intensify as components require frequent replacement or reinforcement to maintain safety standards, creating recurring expenditure pressure for end users across logistics and transportation operations.

Sagging effects alter load distribution across axles, reducing tire life and increasing fuel consumption due to misalignment-related drag. Structural deformation also impacts braking efficiency and vehicle control, which elevates compliance risks for commercial fleets operating under strict safety regulations. Maintenance intensity increases labor demand within service networks, disrupting fleet availability and scheduling efficiency. Frequent inspection cycles create additional downtime, lowering asset utilization rates in time-sensitive logistics operations. Rising lifecycle maintenance costs reduce preference among operators seeking low-maintenance suspension alternatives, influencing procurement decisions toward advanced suspension technologies with improved durability and reduced service frequency.

Opportunity - Integration with Electric and Hybrid Commercial Vehicles

Electrified commercial fleets increase demand for reinforced suspension systems across logistics and distribution operations. Battery pack integration elevates gross vehicle weight, requiring higher structural load support and improved fatigue resistance in chassis components. Design priorities in electric trucks emphasize energy efficiency, payload stability, and durability under continuous torque delivery. United States Department of Energy 2025 data indicates continued year-over-year increase in electric medium and heavy-duty vehicle deployment across fleet operators, reflecting accelerating transition in freight mobility. This shift strengthens adoption of high-strength and composite leaf spring configurations aligned with weight optimization and operational reliability requirements in demanding transport environments systems.

Electrification strategies across commercial transport networks reshape procurement patterns for suspension assemblies, emphasizing modular design compatibility across multiple drivetrain platforms. Urban delivery expansion under electric fleets increases exposure to frequent stop-start cycles, intensifying structural stress on load-bearing components. Regulatory electrification programs across major economies accelerate replacement of diesel-powered fleets, expanding demand base for durable suspension architectures. Material engineering advances in high-strength steel and composite structures improve weight efficiency while maintaining load stability under elevated payload conditions. Standardization trends in electric truck platforms encourage integration of reinforced leaf spring systems to support operational consistency, lifecycle efficiency, and fleet utilization optimization goals.

Adoption of Parabolic and Mono-leaf Designs

Parabolic and mono-leaf suspension architectures generate efficiency gains in commercial vehicle engineering by reducing inter-leaf friction and simplifying structural load transfer. Lower component density supports streamlined manufacturing workflows, enabling faster assembly cycles and reduced tooling complexity for original equipment manufacturers. Weight reduction improves fuel efficiency in combustion-powered fleets and extends operational range in electrified trucks. Improved flexibility enhances axle articulation under varying payload conditions, supporting stable performance across uneven road conditions. Maintenance intervals extend due to fewer wear interfaces, improving fleet uptime and operational continuity. Cost optimization priorities across logistics operators reinforce preference for simplified suspension configurations in vehicle production ecosystems.

Adoption momentum strengthens through improved structural optimization in commercial transport applications. Reduced inter-leaf contact enables smoother suspension response under variable loading cycles across freight movement. Lightweight construction enhances payload efficiency and supports energy savings in electric delivery fleets. Extended service life lowers maintenance frequency and improves vehicle utilization rates across high-demand logistics networks. Enhanced fatigue resistance supports durability in mining, construction, and long-haul transportation environments. Fleet modernization initiatives and electrification programs accelerate integration across emerging manufacturing hubs and global supply chains. Original equipment manufacturers prioritize cost efficiency, payload stability, and reduced lifecycle downtime in next-generation commercial vehicle platforms.

Category-wise Analysis

Product Type Insights

Semi-elliptic segment is likely to be the leading segment with 55% revenue share in 2026, due to widespread integration in commercial vehicle suspension architectures and proven structural reliability under high-load conditions. This configuration remains standard across heavy, light commercial, and agricultural vehicles. OEM adoption benefits from chassis compatibility and reduced production complexity. Regulatory frameworks from the European Commission Directorate-General for Mobility and Transport and the U.S. National Highway Traffic Safety Administration support load stability and safety compliance. Example includes long-haul freight trucks in logistics corridors. Demand remains strong across manufacturing and replacement cycles driven by durability and low maintenance requirements.

Parabolic leaf springs are expected to witness the fastest growth between 2026 and 2033, as the automotive industry's focus on weight reduction, ride quality improvement, and fuel efficiency increasingly favors advanced spring geometries over conventional multi-leaf designs. The tapered profile enables uniform stress distribution, reducing weight while maintaining load capacity. Example includes adoption in medium-duty cargo trucks used in urban logistics. OEM lightweighting programs and fuel economy targets drive integration. Reduced inter-leaf friction lowers maintenance needs and extends service life. Manufacturing advances reduce costs and expand application across commercial vehicle segments.

Vehicle Type Insights

Heavy commercial vehicles are poised to lead with a forecasted over 45% market share in 2026, owing to continuous demand for high-load carrying capacity, infrastructure development projects, and long-distance freight transportation requirements. This segment relies extensively on leaf spring systems due to mechanical strength, durability, and resistance to repetitive high-stress loading conditions. Regulatory oversight from transport authorities ensures compliance with safety standards for load stability and axle performance. Example includes freight trucks used in interstate logistics corridors. Demand remains strong in emerging economies driven by industrialization, mining, and road freight expansion.

Light commercial vehicle segment is anticipated to be the fastest-growing segment between 2026 and 2033, driven by expansion of last-mile delivery networks, e-commerce logistics growth, and urban distribution efficiency requirements. Growth is driven by rising digital commerce penetration increasing intra-city fleet deployment. Government policies support urban logistics modernization and emission-controlled vehicle adoption. Example includes electric delivery vans used in courier operations across metro cities. Electric vehicle adoption increases suspension redesign needs due to higher weight. Fleet operators prioritize low maintenance and cost efficiency. Growth is supported by small business logistics ecosystems and decentralized warehousing networks.

Regional Insights

North America Automotive Leaf Spring Market Trends

North America demonstrates a highly developed automotive and logistics ecosystem supported by extensive freight corridors and strong commercial vehicle manufacturing capabilities. Demand for suspension systems remains elevated across long-haul trucking, construction transport, and industrial logistics operations. High freight intensity across interstate networks sustains continuous component utilization and replacement cycles. Regulatory oversight from transportation safety authorities enforces strict standards for load stability, durability, and operational safety. Expansion of e-commerce distribution strengthens light commercial vehicle deployment across urban and suburban routes, while industrial sectors maintain steady demand for heavy-duty applications.

North America advances vehicle engineering through adoption of lightweight materials, fuel efficiency solutions, and advanced suspension architectures. Electric commercial vehicle growth increases structural load requirements due to battery systems, strengthening demand for reinforced suspension designs. United States drives innovation in automotive components and manufacturing automation, Canada supports logistics infrastructure and resource transport efficiency, Mexico strengthens cost-efficient production and export supply chains. Fleet modernization accelerates replacement of aging vehicles with efficient platforms. Growth in smart mobility and predictive maintenance enhances suspension performance monitoring across commercial transport systems.

Europe Automotive Leaf Spring Market Trends

Europe demonstrates a mature automotive ecosystem supported by advanced engineering standards and strict regulatory oversight on safety, emissions, and load management. Commercial vehicle manufacturing centers across Germany, France, and Italy strengthen demand for high-durability suspension components used in freight and logistics operations. Cross-border transport corridors increase utilization intensity of heavy-duty fleets, sustaining replacement cycles. Regulatory frameworks under the European Commission Directorate-General for Mobility and Transport guide adoption of efficient suspension systems. Aging commercial fleets maintain steady aftermarket consumption across multiple vehicle categories.

Europe advances toward lightweight vehicle architectures through integration of composite materials and high-strength steel in suspension systems. Electric commercial vehicle adoption increases structural load requirements due to battery integration, strengthening demand for reinforced designs. Germany focuses on modular chassis innovation, while France emphasizes electrified mobility platforms. Italy supports efficient component manufacturing networks. Nordic economies accelerate low-emission transport adoption across logistics fleets. Rising automation in manufacturing improves consistency and reduces production variability across suspension component supply chains supporting long-term operational efficiency.

Asia Pacific Automotive Leaf Spring Market Trends

Asia Pacific is expected to lead with an estimated 42% of the automotive leaf spring market share, supported by large-scale commercial vehicle production capacity and sustained freight transport intensity. China drives volume demand through extensive highway logistics expansion and heavy truck manufacturing clusters. India contributes through rapid infrastructure buildout and rising deployment of medium and heavy commercial fleets across mining and construction sectors. Japan supports high-precision suspension engineering for advanced commercial platforms, while South Korea strengthens supply chain integration in automotive components. Cost-efficient manufacturing ecosystems reinforce adoption of conventional suspension systems across price-sensitive fleet operators. Industrial output concentration sustains continuous component consumption across OEM channels.

Asia Pacific is forecasted to be the fastest-growing market for the automotive leaf spring market between 2026 and 2033, stimulated by accelerated logistics digitization and expansion of electric commercial mobility networks. China advances growth through large-scale electrification of delivery fleets and expansion of urban distribution corridors. India records rising penetration of last-mile delivery vehicles driven by e-commerce expansion and decentralized warehousing models. Japan supports growth through adoption of lightweight suspension technologies in hybrid commercial vehicles. South Korea drives innovation in modular vehicle platforms and advanced material integration. Continuous infrastructure expansion and fleet modernization programs strengthen demand momentum across commercial transportation systems.

Competitive Landscape

The global automotive leaf spring market is moderately fragmented with presence of global tier suppliers and regional manufacturers serving OEM and aftermarket channels. Competition is shaped by established suspension system producers with deep integration into commercial vehicle supply chains. Hendrickson, Jamna Auto Industries, Sogefi, NHK Spring, Tenneco, and Mubea Fahrwerksfedern maintain strong positioning through long-term OEM partnerships and diversified product portfolios. Market concentration remains balanced, supported by regional sourcing networks and wide participation in conventional steel-based manufacturing.

Competitive dynamics remain influenced by cost efficiency, material engineering capability, and production scalability across heavy and light commercial vehicle platforms. Hendrickson and NHK Spring strengthen presence through advanced suspension technologies, while Jamna Auto Industries and Mubea Fahrwerksfedern focus on high-volume commercial applications. Sogefi and Tenneco expand through integrated chassis and ride performance systems. Low entry barriers in conventional manufacturing sustain regional player participation, while differentiation relies on durability, lifecycle value, and supply reliability across OEM contracts.

Key Industry Developments

- In April 2026, TVS motor introduced Armado 200, a commercial three-wheeler engineered for demanding logistics applications, featuring leaf-spring suspension for improved load stability across challenging terrain, strengthening utility vehicle performance in emerging mobility corridors.

- In February 2026, Stellantis explored new leaf spring suspension concepts through a patent filing aimed at improving load distribution and durability in next-generation commercial and electrified vehicle platforms, reflecting continued engineering focus on cost-efficient heavy-duty suspension solutions.

- In January 2025, EMCO Industries introduced a high-performance mono-leaf spring designed for heavy-duty trailers, delivering significant weight reduction while improving fatigue life and durability for advanced commercial vehicle suspension systems.

Companies Covered in Automotive Leaf Spring Market

- Hendrickson USA, L.L.C.

- Jamna Auto Industries Ltd.

- Sogefi S.p.A.

- NHK Spring Co., Ltd.

- Tenneco Inc.

- Mubea Fahrwerksfedern GmbH

- ZF Friedrichshafen AG

- Eaton Corporation plc

- Supreme Spring

- Betts Spring Manufacturing

- Emco Industries

- IFC Composite Systems

- Dongfeng Motor Parts

- Hubei Henglong Auto System

- Ride Control LLC

Frequently Asked Questions

The automotive leaf spring market is projected to reach US$ 14.2 billion in 2026.

Rising freight transport activity, expansion of commercial vehicle fleets, and demand for durable, cost-efficient suspension systems in heavy and light commercial vehicles drive the automotive leaf spring market.

The automotive leaf spring market is poised to witness a CAGR of 8.3% from 2026 to 2033.

Growth in electric commercial vehicles, adoption of lightweight composite materials, and expansion of logistics and infrastructure development create key opportunities for the automotive leaf spring market.

Some of the key market players include Hendrickson, Jamna Auto Industries, Sogefi, NHK Spring, Tenneco, and Mubea Fahrwerksfedern.