- Automotive Components & Materials

- Automotive Starter And Alternator Market

Automotive Starter And Alternator Market Size, Share, and Growth Forecast 2026 - 2033

Automotive Starter And Alternator Market by Product Type (Alternators, Starter Motors), Sales Channel (OEMs, Aftermarket), Vehicle Type (Passenger Vehicles, Commercial Vehicles, Off-Road Vehicles), and Regional Analysis for 2026 - 2033

Automotive Starter And Alternator Market Size and Trend Analysis

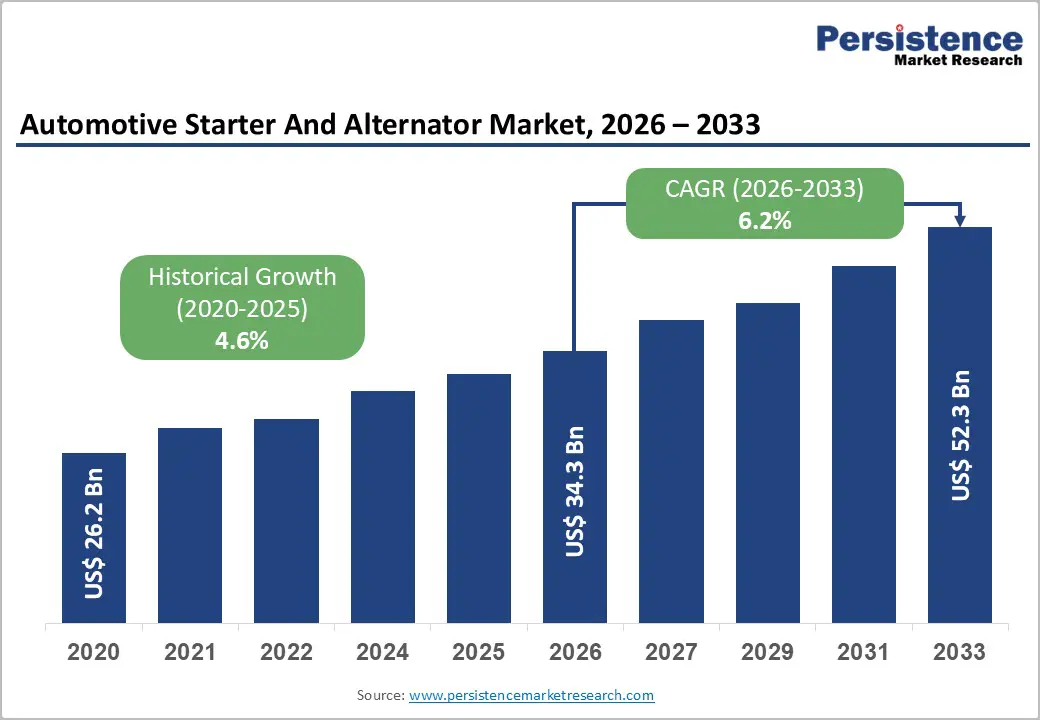

The global Automotive Starter And Alternator market size is valued at US$ 34.3 Bn in 2026 and is projected to reach US$ 52.3 Bn by 2033, growing at a CAGR of 6.2% between 2026 and 2033.

This robust expansion is driven by the sustained rise in global vehicle production, particularly across Asia Pacific and emerging economies, combined with mounting regulatory pressure on fuel efficiency and emissions. The increasing penetration of start-stop systems, mild hybrid architectures incorporating 48V belt-integrated starter generators (BSGs), and integrated starter-generators (ISGs) is generating consistent demand for advanced starting and charging components.

Key Market Highlights

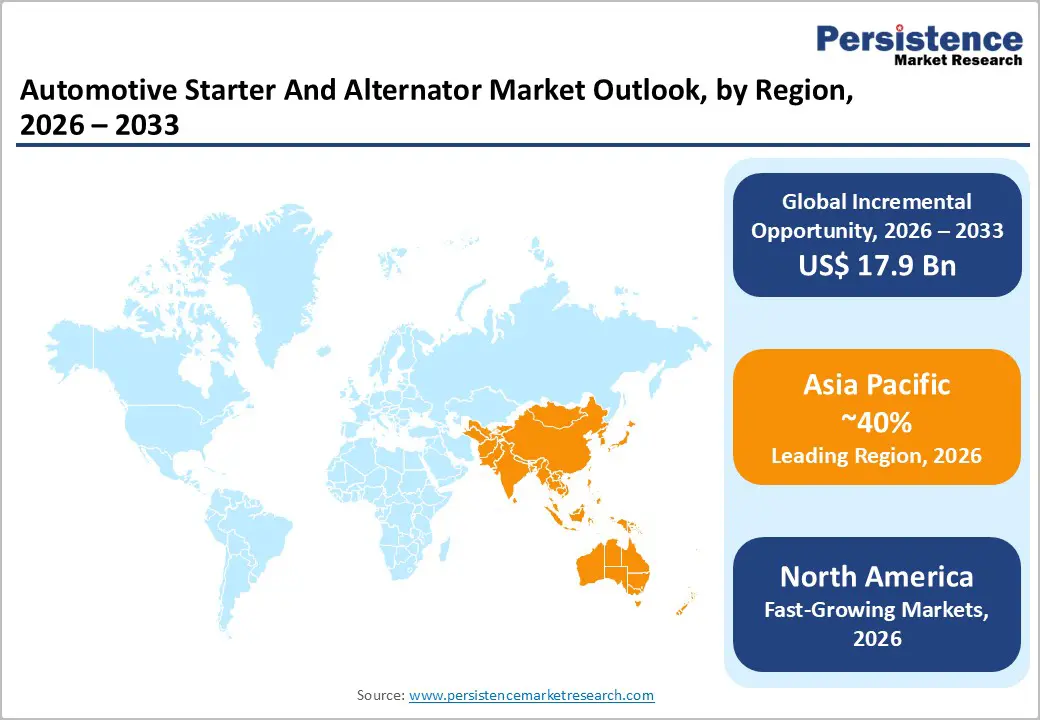

- Leading Region – Asia Pacific commands approximately 40% of global market share, driven by China's vehicle output of over 31.2 million units in 2024, Japan's technology leadership, and India's rapidly expanding automotive production base.

- Fastest Growing Region – India's vehicle production grew 4.7% in 2024, supported by the government's PLI Scheme for automotive components, and China posts a regional CAGR of 6.1%, making both markets key engines of near-term expansion.

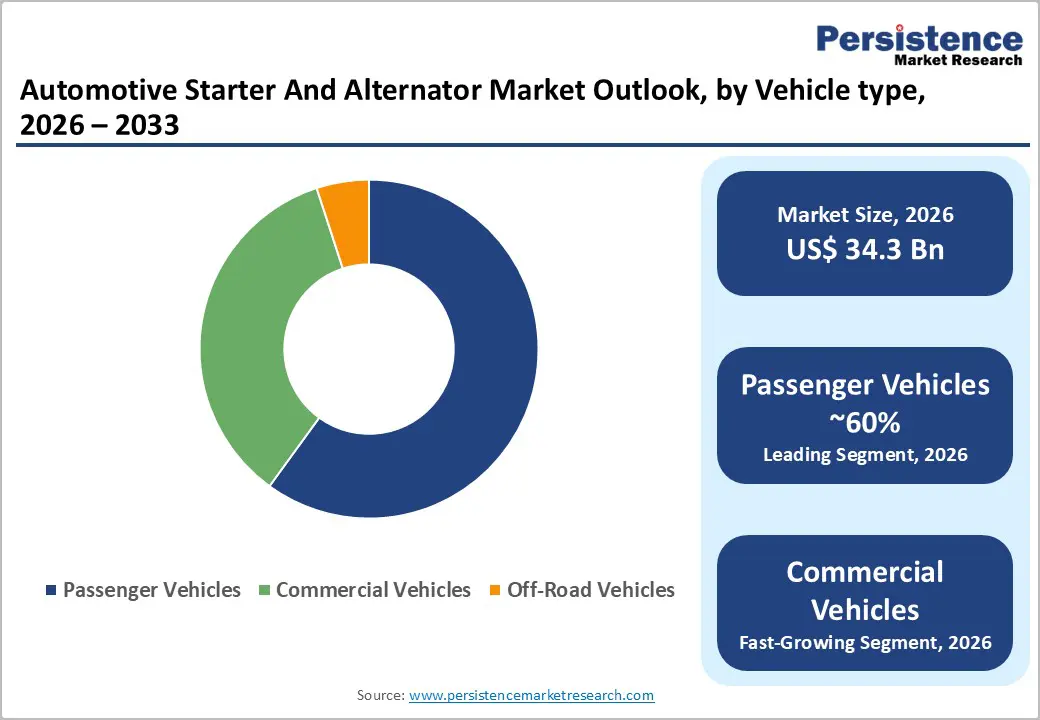

- Dominant Segment – Passenger vehicles lead by vehicle type, supported by over 27.5 million passenger cars produced in China alone in 2024, coupled with growing adoption of start-stop and mild hybrid systems in mass-market models.

- Fastest Growing Segment – The logistics and e-commerce boom is propelling light and heavy commercial vehicle fleet expansion, generating durable high-duty-cycle demand for advanced alternators and starter motors globally.

- Key Market Opportunity – The BSG market growing at a CAGR of 10.6% and the ISG market expanding at 8.7% CAGR through 2033 represent the most significant near-term revenue opportunity for component manufacturers investing in next-generation hybrid powertrain technologies.

| Key Insights | Details |

|---|---|

|

Automotive Starter and Alternator Market Size (2026E) |

US$ 34.3 Bn |

|

Market Value Forecast (2033F) |

US$ 52.3 Bn |

|

Projected Growth CAGR (2026–2033) |

6.2% |

|

Historical Market Growth (2020–2025) |

4.6% CAGR |

DRO Analysis

Market Growth Drivers

Rising Global Vehicle Production and Fleet Electrification

Rising global vehicle output remains the foremost catalyst for the Automotive Starter And Alternator market. According to data from the International Organization of Motor Vehicle Manufacturers (OICA), worldwide motor vehicle sales reached approximately 95 million units in 2024, and China alone produced over 31.2 million vehicles roughly one-third of global output. This surge in vehicle volumes directly amplifies demand for starting and charging components installed at the OEM level.

Simultaneously, the accelerating shift toward mild hybrid and start-stop technologies is redefining component specifications. The 48V mild hybrid segment, which integrates belt starter generators alongside conventional alternators, has seen adoption rates climb as automakers pursue compliance with tightening Euro 7 and Bharat Stage VI Phase II emission norms. This dual tailwind of volume growth and technology-driven content value increase sustains robust demand across both OEM and aftermarket channels.

Increasing Electrical Load in Modern Vehicles and Advanced Technology Adoption

Modern vehicles have substantially increased their reliance on electrical systems, directly amplifying the demand for high-capacity alternators and intelligent starter motors. Industry data indicates that the average vehicle integrated more than 75 electronic control units (ECUs) in 2024, compared with approximately 38 units in 2010, increasing alternator load requirements by over 96%. Advanced driver-assistance systems (ADAS) consume an estimated 650–900 W per vehicle, while infotainment and connectivity systems add an additional 400–600 W of electrical demand.

This growing onboard power appetite is prompting OEMs to adopt smart alternators capable of real-time voltage regulation and energy recuperation. The proliferation of integrated starter-generator (ISG) systems a market valued at approximately USD 4.6 billion in 2024 and expected to grow at a CAGR of 8.7% through 2033 underscores the technological evolution occurring in the starter-alternator space, creating premium revenue opportunities for component manufacturers.

Market Restraints

Rising Penetration of Battery Electric Vehicles (BEVs) Displacing Conventional Components

The accelerating adoption of battery electric vehicles (BEVs) represents a structural headwind for traditional starter motors and alternators, as fully electric powertrains eliminate the need for both components. BEVs accounted for approximately 18% of global new vehicle registrations in 2024, according to available industry data, and major economies are implementing aggressive EV mandates.

The European Union's ban on new internal combustion engine (ICE) vehicle sales by 2035 and China's new energy vehicle (NEV) penetration targets are expected to progressively reduce the addressable market for conventional alternators and starter motors in the long run, introducing margin pressure and volume uncertainty for market participants focused solely on legacy ICE applications.

Raw Material Price Volatility and Supply Chain Disruptions

Alternators and starter motors are manufactured using copper windings, permanent magnets incorporating rare earth elements, aluminum housings, and electronic control components all of which are subject to commodity price volatility. Copper prices have experienced significant fluctuations, and rare earth supply chains remain heavily concentrated in China, which controls over 60% of global rare earth production according to the U.S.

Geological Survey (USGS). Supply chain disruptions triggered by geopolitical tensions, semiconductor shortages, and logistical bottlenecks in the post-pandemic era have elevated manufacturing costs and compressed margins for Tier-1 suppliers. These input cost pressures restrict the ability of manufacturers to scale competitive pricing, particularly in price-sensitive emerging markets.

Market Opportunities

Expansion of the Mild Hybrid (48V) Ecosystem as a Bridge Technology

Mild hybrid vehicles powered by 48V electrical architectures represent a compelling near-term growth opportunity for the Automotive Starter And Alternator market. Unlike full EVs, mild hybrids retain the alternator and starter motor in a combined integrated or belt-driven starter-generator configuration, enabling fuel savings of 10–15% without the high cost of full electrification.

The global automotive belt starter generator (BSG) market was valued at USD 1.3 billion in 2024 and is projected to expand at a CAGR of 10.6% through 2034, indicating strong momentum. In May 2025, Valeo S.A. introduced its latest 48V Integrated Starter Generator (ISG) platform aimed at supporting mild hybrid deployment across Europe and Asia.

Growing Aftermarket Demand in Mature and Emerging Economies

The aftermarket for replacement starters and alternators is emerging as a resilient and increasingly profitable revenue stream for market participants. In regions such as North America and Europe, where the average vehicle age exceeds 12 years, the frequency of starter and alternator replacements is rising steadily.

The average operational lifespan of a starter motor ranges from 100,000 to 150,000 miles, creating a predictable replacement cycle that sustains aftermarket volumes even in markets where new vehicle sales are stagnant. In June 2025, DRiV (the aftermarket division of Tenneco) launched a comprehensive range of remanufactured starters and alternators under its Walker brand, backed by a three-year warranty, highlighting the commercial viability of the remanufactured segment.

Category-wise Analysis

Product Type Insights

Among the two product categories, Starter Motors hold the leading position in the Automotive Starter And Alternator market, accounting for approximately 55% of total market share. This dominance is attributable to their indispensable role in initiating internal combustion engines across virtually all conventional passenger cars, commercial vehicles, and off-road machinery globally. The rising adoption of start-stop systems which cycle the engine off during idling and restart it upon acceleration has amplified the operational load on starter motors, accelerating replacement cycles and driving premium product demand.

According to industry data, start-stop technology was featured in over 40% of newly produced vehicles in Europe by 2024, reinforcing the sustained demand for high-durability, high-cycle starter motors. Concurrently, technological innovation in brushless starter motor designs and compact high-torque configurations is enhancing product value and expanding addressable applications, including in emerging mild hybrid architectures.

Sales Channel Insights

The OEM (Original Equipment Manufacturer) sales channel dominates the Automotive Starter And Alternator market, commanding approximately 66% of total market share. OEM dominance reflects the integral nature of starters and alternators as factory-installed components in every new vehicle produced globally. Automakers maintain rigorous supplier qualification standards demanding precision engineering, regulatory compliance, and long-term supply assurance which consistently Favor established Tier-1 suppliers such as Denso Corporation, Valeo Group, and Bosch Mobility.

The strong recovery in global vehicle production post-2020 supply chain disruptions, with OICA reporting approximately 95 million vehicles sold in 2024, has directly reinforced OEM channel volumes. While the Aftermarket channel is growing at a faster rate driven by aging vehicle fleets and expanding organized distribution in emerging markets, the OEM segment remains structurally dominant due to high per-unit volume commitments and long-term supply agreements embedded in automaker procurement frameworks.

Vehicle Type Insights

Passenger Vehicles represent the leading vehicle type in the Automotive Starter And Alternator market, holding approximately 60% of the overall market share. This leadership is underpinned by the sheer volume of passenger car production globally with China alone manufacturing over 27.5 million passenger cars in 2024 according to OICA data and the growing integration of advanced in-vehicle technologies that escalate electrical load requirements.

The rising consumer preference for comfort, connectivity, and safety features, including infotainment systems, electronic power steering, and advanced ADAS, drives the need for higher-output alternators in passenger vehicles. Additionally, the growing adoption of start-stop technology and mild hybrid systems in mass-market passenger cars has elevated the technical specification and value of both starter motors and alternators within this segment.

Regional Analysis

Asia Pacific

Asia Pacific is the dominant and fastest-growing region in the global Automotive Starter And Alternator market, accounting for approximately 40% of global market revenue, driven by concentrated automotive manufacturing in China, Japan, and India. China's extraordinary vehicle output over 31.2 million units in 2024 per OICA combined with its rapidly expanding new energy vehicle (NEV) ecosystem, creates dual demand for both conventional ICE-type starters and alternators and advanced integrated starter-generator systems for hybrid models.

India is emerging as the fastest-growing sub-market within Asia Pacific, with domestic vehicle production growing 4.7% in 2024 according to the ACEA, supported by the government's PLI (Production Linked Incentive) Scheme for automotive components. The ASEAN region, particularly Thailand and Indonesia, is also expanding as a manufacturing base, offering cost advantages and proximity to key regional OEMs.

North America

North America holds a prominent position in the global Automotive Starter And Alternator market, driven by the United States' extensive vehicle parc exceeding 290 million registered vehicles in 2024, one of the highest concentrations in the world. This vast existing vehicle base creates sustained aftermarket replacement demand, particularly as the average vehicle age surpasses 12 years.

The U.S. market also benefits from robust regulatory frameworks including EPA and NHTSA efficiency standards that incentivize technology upgrades in alternators and starter motors. The North America market is also benefiting from the growing mild hybrid adoption, particularly in light trucks and SUVs, which represent the largest vehicle segment in the U.S. Strong R&D ecosystems anchored by major OEM facilities of General Motors, Ford, and Stellantis, combined with an active Tier-1 supplier presence, underpin the region's innovation pipeline in smart alternator and starter-generator systems.

Europe

Europe represents a strategically critical market for the Automotive Starter And Alternator industry, with Germany leading regional demand as the continent's largest automotive manufacturer, producing approximately 4 million vehicles in 2024 according to OICA data. The region's stringent Euro 7 emission norms and the EU's 2035 ICE ban are compelling automakers in Germany, France, Spain, and the U.K. to integrate mild hybrid architectures incorporating 48V BSG and ISG systems directly elevating component value per vehicle.

The European Automobile Manufacturers' Association (ACEA) reports that start-stop technology penetration in European new vehicle production has become near-universal for ICE vehicles, sustaining strong demand for high-cycle starter motors. The aftermarket in Europe is also well-organized and growing, with leading suppliers like Robert Bosch, Valeo Service, and Borg Automotive (under the Lucas and Elstock brands) offering both new and remanufactured starters and alternators backed by extended warranties. Regulatory harmonization across the region continues to support cross-border supply chain efficiency.

Competitive Landscape

The global Automotive Starter And Alternator market exhibits a moderately consolidated competitive structure, with leading players including Denso Corporation, Valeo Group, Bosch Mobility, Mitsubishi Electric, and BorgWarner Inc. collectively commanding a significant combined market share.

These incumbents leverage scale advantages, deep OEM relationships, and multi-decade technical expertise to maintain dominance. Key competitive strategies include investment in 48V mild hybrid technologies, strategic partnerships with EV platform developers, expansion of remanufacturing capabilities, and geographic diversification into high-growth markets in Asia and Africa.

Key Market Developments

- In June 2025, DRiV (the aftermarket division of Tenneco) introduced a range of remanufactured starters and alternators under its Walker brand, now offered alongside air conditioning components, all backed by a three-year warranty.

- In December 2024, Lucas TVS Ltd showcased advancements in its global strategy and technological capabilities in the automotive alternator and starter motor domain at industry platforms such as its annual Tech Show and IAA Transportation 2024.

Companies Covered in Automotive Starter And Alternator Market

- Denso Corporation

- Valeo Group

- Bosch Mobility (Robert Bosch GmbH)

- Mitsubishi Electric Corporation

- Hitachi Astemo, Ltd.

- Prestolite Electric (Broad-Ocean)

- SEG Automotive

- Delco Remy (BorgWarner Inc.)

- MAHLE Group

- Lucas TVS Ltd

Frequently Asked Questions

The global Automotive Starter And Alternator market is valued at US$ 34.3 Bn in 2026 and is projected to reach US$ 52.3 Bn by 2033, growing at a CAGR of 6.2% during the forecast period.

The key growth drivers include rising global vehicle production with OICA reporting approximately 95 million vehicles sold in 2024 the accelerating adoption of start-stop systems and 48V mild hybrid technologies, and increasing electrical load per vehicle driven by ADAS, infotainment, and electronic power steering.

Passenger Vehicles dominate the Automotive Starter And Alternator market by vehicle type, accounting for approximately 60% of total market share. This dominance is driven by the high global volume of passenger car production over 27.5 million in China alone in 2024 per OICA and growing integration of advanced electrical features and start-stop technology in mass-market models.

Asia Pacific is the leading region in the global Automotive Starter And Alternator market, contributing approximately 40% of total revenue share. China's dominance as the world's largest vehicle manufacturer, Japan's technological leadership in alternator and starter motor R&D, and India's rapidly growing vehicle production expanding 4.7% in 2024 collectively position the region as the primary growth engine, with China and India posting the highest sub-regional CAGRs of 6.1% and 5.6% respectively.

The leading companies in the Automotive Starter And Alternator market include Denso Corporation, Valeo Group , Bosch Mobility / Robert Bosch GmbH, Mitsubishi Electric Corporation, Hitachi Astemo, Ltd., and MAHLE Group.