- Automotive Components & Materials

- Automotive Battery Market

Automotive Battery Market Size, Share, Trends, Growth, Regional Forecasts 2026–2033

Automotive Battery Market By Battery Type (Lithium-ion Battery, Lead-acid Battery, Nickel-based Battery, Others), Battery Capacity (Below 25 kWh, 25–50 kWh, 50–100 kWh, Above 100 kWh), Propulsion Type (ICE, HEV, PHEV, BEV, FCEV), Vehicle Type (Passenger Vehicles, Light Commercial Vehicle, Heavy Commercial Vehicle, Buses & Coaches, Two & Three Wheelers, Off‑highway Vehicles), Sales Channel (OEM, Aftermarket), and Regional Analysis for 2026–2033

Automotive Battery Market Trends & Analysis

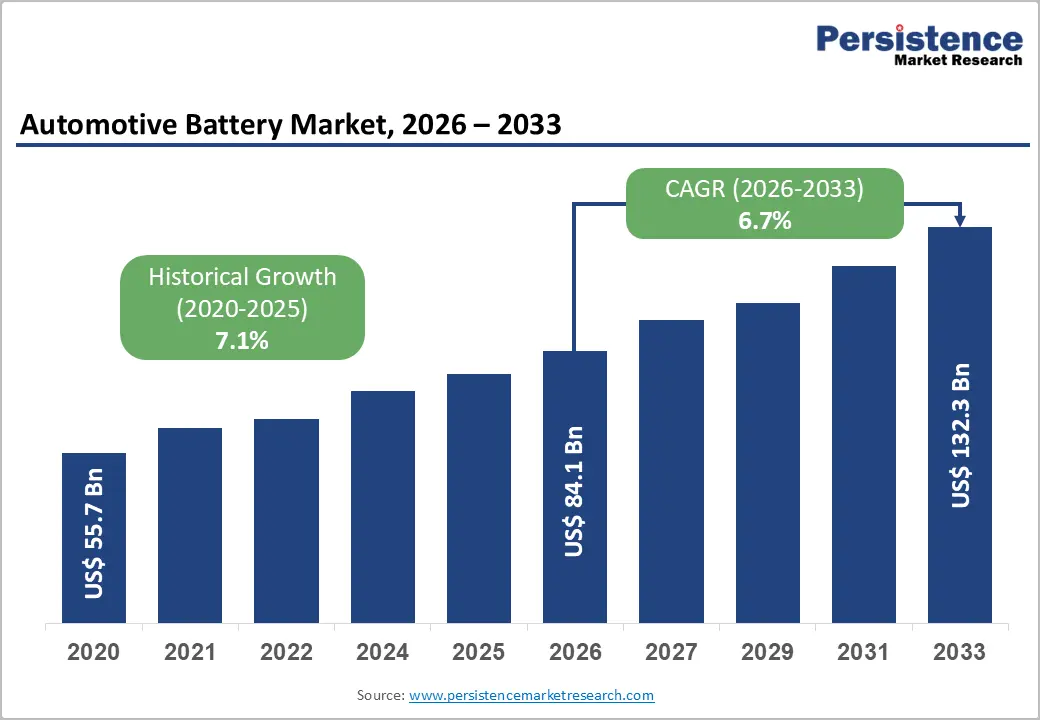

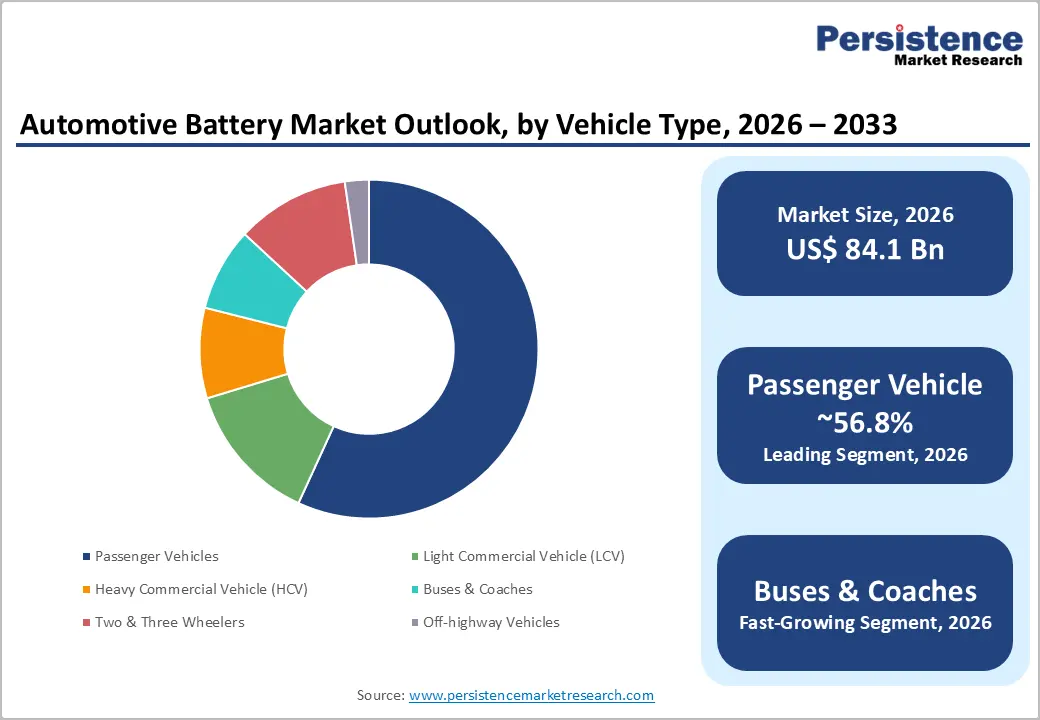

The global Automotive Battery Market size is projected at US$ 84.1 billion in 2026 and is projected to reach US$ 132.3 billion by 2033, growing at a CAGR of 6.7% between 2026 and 2033. Growth is underpinned by rapid electrification: global electric-car sales neared 14 million in 2023, representing 18% of all cars sold, and are expected to exceed 20 million annual sales by 2025 as EV adoption enters the mass market. Strong policy support in China, Europe, and the United States, combined with major gigafactory investments, is driving structural shifts in automotive supply chains and long-term demand for advanced lithium-ion batteries.

Key Industry Highlights:

- EV Momentum: Global electric-car sales neared 14 million (18% of all new cars) in 2023 and are expected to exceed 20 million in 2025, structurally lifting battery demand across passenger and commercial vehicle segments worldwide.

- Segment Leaders: Lithium-ion Battery (LFP, NMC, NCA) leads battery types with about 68.5% share; 50–100 kWh packs dominate capacity with 39.4% share; BEVs drive propulsion demand with 34.9% share; passenger vehicles account for 56.8% of revenues.

- High-growth Segments: Lithium-ion technology grows at around 9.0% CAGR, Above 100 kWh capacity at 10.7% CAGR, FCEVs at 16.4% CAGR, and Buses & Coaches at 9.8% CAGR as heavy-duty and public-transport electrification scales.

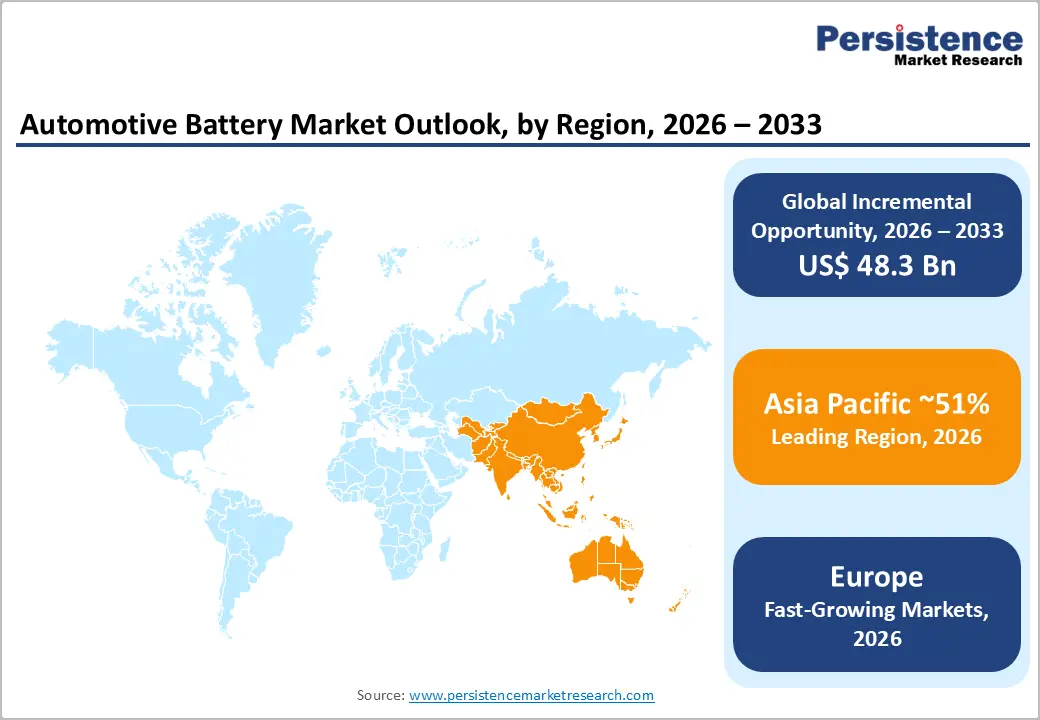

- Regional Dynamics: Asia Pacific leads with about 51% share, China contributing US$ 23.9 Bn; North America holds roughly 18.7%, including a US$ 12.8 Bn U.S. market; Europe grows fastest at around 6.5% CAGR with strong regulatory drivers.

- Strategic Investments: Major projects, including CATL’s €7.3 Bn/100 GWh Hungary gigafactory and LG Energy Solution–Honda’s US$ 4.4 Bn/40 GWh Ohio plant, are reshaping global supply, localisation and partnership structures in the automotive-battery ecosystem.

- Risk–Opportunity Balance: Supply-chain concentration, evolving trade policies and demand volatility pose notable risks, but localisation strategies, recycling initiatives and second-life applications provide additional levers to capture long-term value across regions.

Market Dynamics Analysis

Drivers - Rapid EV adoption and rising battery demand

Global electric-car sales exceeded 10 million units in 2022, then climbed to nearly 14 million in 2023, lifting EVs to 18% of global light-vehicle sales; projections indicate more than 20 million EV sales in 2025, or roughly one in four new vehicles sold. This surge has expanded the global electric-car fleet to around 40 million vehicles in 2023 and close to 58 million by end-2024, sharply increasing demand for traction batteries across segments and regions.

In 2024, EVs accounted for more than 22% of new car sales globally, with China near 50% and Europe and the United States also showing strong penetration. These trends lift demand for automotive batteries not only in BEVs but also in HEVs, PHEVs and FCEVs, supporting sustained growth in cell shipments and pack integration across the automotive value chain.

Technology advances in lithium-ion chemistry and manufacturing scale

The lithium-ion battery industry is comparatively consolidated, with leaders such as CATL, BYD, LG Energy Solution, Samsung SDI and Panasonic jointly accounting for roughly 50–60% of global market share, enabling large-scale investment in R&D and manufacturing. CATL alone holds about 37–39% of global EV-battery share and more than 50% of the LFP segment, while deploying over 390 GWh of annual capacity across its plants.

Industry data indicate global EV-battery usage reached about 686.7 GWh from January to October 2024, up 25% year-on-year, reflecting rapid capacity ramp-up and chemistry optimisation. High-nickel NMC/NCA chemistries deliver energy-density gains for long-range vehicles, while LFP provides cost-effective, durable solutions for mass-market and commercial EVs, collectively driving the dominance of Lithium-ion Battery (LFP, NMC, NCA) in the automotive battery mix.

Restraints - Supply-chain concentration and geopolitical risk

The EV-battery supply chain is highly concentrated: China accounts for the majority of cathode, anode and cell manufacturing, and leading Chinese and Korean firms dominate global EV-battery installations. This concentration exposes automakers to geopolitical tensions, trade restrictions and policy shifts, including tariffs and local-content rules in major markets, which can delay sourcing decisions and investment.

Regulatory scrutiny in the United States and Europe around foreign content, combined with evolving trade remedies against Chinese EVs and batteries, may constrain near-term sales growth or redirect investment flows, particularly for OEMs without diversified supply bases. These uncertainties add execution risk and can slow down large-scale procurement decisions for new battery programs.

Market Volatility, Demand Uncertainty and Project Reprioritisation

EV-demand growth remains robust but has shown signs of normalisation, with some automakers revising near-term EV plans in response to changing incentives, interest-rate environments and consumer preferences. In late 2025, major OEMs cancelled or renegotiated sizable battery-supply deals, prompting manufacturers such as LG Energy Solution to rebalance capacity between EV and energy-storage markets.

Such adjustments can lead to under-utilised capacity in the short term, affecting profitability and capital-deployment decisions for new gigafactories. In addition, the relatively small but growing FCEV and high-capacity segments face infrastructure and adoption risks, making volume forecasts more uncertain for certain advanced chemistries and large battery formats.

Opportunities - Fuel-cell and xEV diversification, especially in commercial and fleet applications

Fuel-cell electric vehicles remain a small niche but are growing quickly: global FCEV stock increased by around 20% in 2023 to about 87,600 vehicles, with strong uptake in Asia, particularly Korea, and rising deployments in buses and medium- and heavy-duty trucks. The fuel cell electric vehicle (FCEV) segment in propulsion is thus expected to record the fastest growth, at roughly 16.4% CAGR, driving demand for high-power battery systems used in hybrid fuel-cell architectures.

Beyond FCEVs, HEVs and PHEVs continue to provide transitional pathways in markets with constrained charging infrastructure, supporting demand for mid-capacity packs and 12-volt auxiliary batteries. Together, these xEV segments represent a multi-billion-dollar opportunity alongside BEVs, especially in fleets seeking lower total cost of ownership and regulatory compliance in low-emission zones.

Localised Battery Ecosystems, Recycling and Second-life Applications

Regional industrial strategies to build domestic battery ecosystems create opportunities in cell manufacturing, pack assembly, recycling and second-life uses. In Europe, cumulative investments in battery and EV facilities since 2017 exceed €70 Bn, and countries such as Hungary, Spain and Germany are emerging as key battery and EV-manufacturing hubs. In parallel, China, the United States, India and others have announced large incentive schemes and localisation targets for advanced batteries.

End-of-life management adds another high-growth avenue: leading players such as CATL and BYD are investing in battery recycling and closed-loop supply chains to recover lithium, nickel and cobalt, aligning with circular-economy goals and regulatory requirements in major markets. As global EV sales rise into the tens of millions annually, recycling and second-life stationary applications could account for a meaningful portion of the incremental US$ 48+ Bn market expansion through 2033.

Category-wise Analysis

Battery Type Insights

Lithium-ion Battery (LFP, NMC, NCA) is the leading battery type, accounting for about 68.5% of global automotive-battery revenues in 2026, reflecting its dominance in BEVs, PHEVs and many HEVs across China, Europe and North America. Compared with Lead-acid Battery, Nickel-based Battery and Others, lithium-ion benefits from superior energy density, longer cycle life and ongoing cost reductions; its share is expected to remain structurally high given deep investments and continuous chemistry optimisation.

Battery Capacity Insights

Within capacity, the 50–100 kWh segment leads with around 39.4% share of automotive-battery revenues in 2026, as this range aligns with typical mid-size and SUV BEVs in major markets and balances driving range with cost and weight. Compared with Below 25 kWh, 25–50 kWh and Above 100 kWh, this band benefits from high volumes in mainstream passenger EVs and growing adoption in light commercial vehicles, although very high-capacity packs are rising in importance for premium and commercial segments.

The Above 100 kWh segment is expected to be the fastest-growing capacity band, with an estimated 10.7% CAGR over 2026–2033, driven by long-range SUVs, pickup trucks and electric buses and trucks that demand large battery packs.

Propulsion Type Insights

By propulsion, battery electric vehicles (BEVs) hold the leading share at approximately 34.9% of automotive-battery revenues in 2026, reflecting their dominant role in EV sales growth and the larger kWh per vehicle relative to HEVs and PHEVs. Compared with Internal Combustion Engine (ICE) vehicles (which still use 12-volt and auxiliary batteries), HEV, PHEV and FCEV segments, BEVs capture the largest energy-storage content and benefit most from zero-tailpipe-emission regulations and purchase incentives across major markets.

Fuel cell electric vehicles (FCEVs) are expected to be the fastest-growing propulsion segment, with an approximate 16.4% CAGR between 2026 and 2033, reflecting expanding deployments in buses, trucks and niche passenger segments, particularly in Asia and North America.

Vehicle Type Insights

Passenger Vehicles (Compact Car, Midsize Car, SUVs, Luxury Vehicles) represent the leading vehicle type, accounting for about 56.8% share of automotive-battery revenues in 2026, as they dominate global light-vehicle sales and EV penetration. Compared with Light Commercial Vehicle (LCV), Heavy Commercial Vehicle (HCV), Buses & Coaches, Two & Three Wheelers and Off-highway Vehicles, passenger vehicles benefit from strong consumer incentives, model availability and regulatory pressure, although electrification of commercial fleets is accelerating.

Within vehicle types, buses & coaches are projected to be the fast-growing segment, with an estimated 9.8% CAGR through 2033, driven by urban air-quality mandates, zero-emission public-transport targets and large battery packs per vehicle.

Sales Channel Insights

By sales channel, OEM dominates automotive-battery revenues with around 82.7% share in 2026, reflecting the fact that most high-value traction batteries are integrated at the vehicle-manufacturing stage under long-term supply contracts. Compared with the Aftermarket, OEM supply benefits from direct relationships with automakers, technology co-development and localisation initiatives, and is likely to retain its leadership as EV penetration increases and pack lifetimes improve.

The OEM channel is also the fast-growing segment, supported by rising factory-fit EV volumes; the Aftermarket grows more slowly at roughly 2.4% CAGR, driven mainly by replacement of 12-volt and auxiliary batteries, as long-range traction batteries typically have extended warranties and lifetimes.

Regional Market Insights

North America Automotive Battery Market Share

North America accounts for approximately 18.7% of the global automotive battery market, driven by accelerating EV adoption across the United States and Canada, expanding charging infrastructure networks, and strong federal as well as state-level incentives supporting clean mobility and localized battery manufacturing. Rising investments in gigafactories, battery recycling facilities, and regional EV supply chains are further strengthening North America’s position as a strategically important automotive battery production and innovation hub.

United States Automotive Battery Market

The United States contributes nearly US$12.8 billion in automotive battery revenues, supported by rapidly increasing electric vehicle adoption, Inflation Reduction Act (IRA)-linked tax incentives, and large-scale investments in battery cell and pack manufacturing facilities. Major domestic and international battery manufacturers are expanding localized production capacities to comply with local-content requirements and strengthen regional EV supply chains.

Growing investments in gigafactories, battery recycling infrastructure, and advanced energy storage technologies are further positioning the country as a leading North American hub for automotive battery production and innovation. Canada is emerging as a complementary hub for critical minerals, cathode materials and cell plants, while other North-American markets remain smaller but benefit from shared supply chains, regional trade agreements and cross-border vehicle platforms built by global OEMs.

Europe Automotive Battery Market Insights

Europe is likely to reach a prominent pace of around 6.5% CAGR, supported by stringent CO2 standards, ICE-phase-out timelines and ambitious national EV-adoption targets across EU member states and the U.K. Increasing investments in gigafactories, battery recycling infrastructure, and localized EV supply chains are further accelerating regional demand for advanced automotive battery technologies.

Germany Automotive Battery Market Trends

Germany remains one of Europe’s leading automotive battery markets, generating nearly US$5.7 billion in revenues, supported by its strong premium vehicle manufacturing ecosystem, rising electric vehicle penetration, and strategic role in Europe’s battery production expansion since 2017. Continuous investments in gigafactories, battery R&D centers, and localized EV supply chains by both European and Asian manufacturers are accelerating the country’s transition toward large-scale battery manufacturing and advanced energy storage technologies. Germany’s leadership in automotive engineering and industrial automation further strengthens its position within the European EV battery landscape.

The United Kingdom, France, and Spain also contribute significantly, with Spain and Hungary emerging as key destinations for new gigafactory investments, while EU-wide regulatory harmonisation on batteries, recycling and ESG reporting shapes competitive dynamics and investment decisions.

Asia Pacific Automotive Battery Market Trends

Asia Pacific dominates the global automotive battery market with an estimated 51% revenue share, reflecting the region’s leadership in electric vehicle production, battery cell manufacturing, and critical mineral processing activities. Major economies, including China, Japan, and South Korea, continue to drive regional growth through large-scale gigafactory investments, advanced battery technology development, and strong government support for EV adoption and localized supply chain expansion.

China Automotive Battery Market Insights

China accounts for nearly US$23.9 billion in automotive battery revenues, driven by its dominance as the world’s largest electric vehicle market and its strong domestic battery manufacturing ecosystem. The country is home to global battery leaders such as Contemporary Amperex Technology Co. Limited (CATL) and BYD Company Limited, which collectively represent a substantial share of worldwide EV battery installations. Continuous government support, rapid EV adoption, large-scale gigafactory investments, and vertically integrated supply chains continue to reinforce China’s leadership across battery materials, cell manufacturing, and energy storage technologies.

Japan focuses on advanced battery R&D and HEV/PHEV platforms, while India, with automotive-battery revenues of around US$3.7 billion, is scaling EV incentives, local-cell manufacturing, and two-/three-wheeler electrification, alongside rising ASEAN demand and manufacturing advantages in the broader region.

Competitive Landscape

The automotive-battery market is moderately consolidated at the cell-manufacturing level, with leading players capturing more than half of global lithium-ion market share, while pack integration and vehicle-level supply exhibit more fragmentation across regions and OEMs. Key differentiators include chemistry portfolios (LFP and high-nickel NMC/NCA), manufacturing scale, long-term OEM contracts and localisation strategies, while emerging business models focus on recycling, second-life applications and battery-as-a-service.

Dominant strategic themes encompass innovation in high-energy and fast-charging chemistries, cost leadership via gigafactory scale and vertical integration, and market expansion through cross-regional joint ventures, especially in North America and Europe, aligning with policy incentives and evolving trade regimes.

Strategic Developments

- In September 2025, CATL Debrecen gigafactory (Hungary): In September 2025, CATL confirmed its €7.3 Bn investment in a 100 GWh battery plant in Debrecen, Hungary, scheduled to start production in early 2026, significantly expanding its European EV-battery supply capacity for major OEMs.

- In February 2024, LG Energy Solution–Honda Ohio JV progress (U.S.): In February 2024, LG Energy Solution and Honda reported construction of their Ohio EV-battery plant, targeting 40 GWh/year capacity and up to US$ 4.4 Bn investment, was on track to support North-American EV production from 2025–2026.

- In December 2025, LG Energy Solution asset sale to Honda (U.S.): In December 2025, LG Energy Solution agreed to sell building assets of the Ohio battery plant to Honda for about US$ 2.86 Bn, optimising joint-venture operations while maintaining the 40 GWh EV-battery capacity plan for the site.

- In June 2025, BYD Komárom expansion (Hungary): In mid-2025, BYD announced a 32 billion forint (≈US$ 94 M) investment to triple e-bus and e-truck production at its Komárom plant to 1,250 units annually, reinforcing its European commercial-EV and battery-integration footprint.

Companies Covered in Automotive Battery Market

- Contemporary Amperex Technology Co. Limited (CATL)

- BYD Company Ltd.

- LG Energy Solution

- Panasonic Holdings Corporation

- Samsung SDI

- SK On

- CALB (China Aviation Lithium Battery)

- Gotion High-Tech

- EVE Energy

- Sunwoda

- Northvolt AB

- Envision AESC

- Toshiba Corporation

Frequently Asked Questions

The global Automotive Battery Market is anticipated at about US$ 84.05 Bn in 2026 and is projected to reach approximately US$ 132.34 Bn by 2033, driven primarily by accelerating EV adoption and higher battery content per vehicle.

The market is driven by rapid EV‑sales growth, large‑scale lithium‑ion technology advances, and supportive industrial policies and gigafactory investments across Asia Pacific, Europe and North America that localise production and secure long‑term supply for automakers.

Between 2026 and 2033, the Automotive Battery Market is expected to grow at a CAGR of around 6.7%, consistent with the increase from US$ 84.1 Bn to US$ 132.3 Bn over the forecast period.

Key opportunities include high‑capacity packs for long‑range EVs and commercial fleets, rapidly growing FCEV and xEV applications, and localised ecosystems in manufacturing, recycling and second‑life uses that together represent an incremental US$ 48+ Bn opportunity.

Major players include CATL, BYD, LG Energy Solution, Panasonic, Samsung SDI, SK On, CALB, Gotion High‑Tech, EVE Energy, Sunwoda, Northvolt, Envision AESC and Toshiba, which collectively shape global supply, technology roadmaps and regional localisation strategies.