- Executive Summary

- Global Agricultural Grade Zinc Chemicals Market Snapshot, 2026 and 2033

- Market Opportunity Assessment, 2026 - 2033, US$ Bn

- Key Market Trends

- Future Market Projections

- Premium Market Insights

- Industry Developments and Key Market Events

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definition

- Market Dynamics

- Drivers

- Restraints

- Opportunity

- Challenges

- Key Trends

- COVID-19 Impact Analysis

- Forecast Factors - Relevance and Impact

- Value Added Insights

- Value Chain Analysis

- Key Market Players

- Regulatory Landscape

- PESTLE Analysis

- Porter’s Five Force Analysis

- Consumer Behavior Analysis

- Price Trend Analysis, 2020-2025

- Key Factors Impacting Product Prices

- Pricing Analysis, By Product Type

- Regional Prices and Product Preferences

- Global Agricultural Grade Zinc Chemicals Market Outlook

- Market Size (US$ Bn) Analysis and Forecast

- Historical Market Size (US$ Bn) Analysis, 2020-2025

- Market Size (US$ Bn) Analysis and Forecast, 2026-2033

- Global Agricultural Grade Zinc Chemicals Market Outlook: Product Type

- Historical Market Size (US$ Bn) Analysis, By Product Type, 2020-2025

- Market Size (US$ Bn) Analysis and Forecast, By Product Type, 2026-2033

- Zinc Oxide

- Zinc Sulfate

- EDTA Chelated Zinc

- Sulphur Zinc Bentonite

- Others

- Market Attractiveness Analysis: Product Type

- Global Agricultural Grade Zinc Chemicals Market Outlook: Application

- Historical Market Size (US$ Bn) Analysis, By Application, 2020-2025

- Market Size (US$ Bn) Analysis and Forecast, By Application, 2026-2033

- Animal Feed

- Chemical Fertilizers

- Others

- Market Attractiveness Analysis: Application

- Market Size (US$ Bn) Analysis and Forecast

- Global Agricultural Grade Zinc Chemicals Market Outlook: Region

- Historical Market Size (US$ Bn) Analysis, By Region, 2020-2025

- Market Size (US$ Bn) Analysis and Forecast, By Region, 2026-2033

- North America

- Latin America

- Europe

- East Asia

- South Asia and Oceania

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Agricultural Grade Zinc Chemicals Market Outlook

- Historical Market Size (US$ Bn) Analysis, By Market, 2020-2025

- By Country

- By Product Type

- By Application

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026-2033

- U.S.

- Canada

- Market Size (US$ Bn) Analysis and Forecast, By Product Type, 2026-2033

- Zinc Oxide

- Zinc Sulfate

- EDTA Chelated Zinc

- Sulphur Zinc Bentonite

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Application, 2026-2033

- Animal Feed

- Chemical Fertilizers

- Others

- Market Attractiveness Analysis

- Historical Market Size (US$ Bn) Analysis, By Market, 2020-2025

- Europe Agricultural Grade Zinc Chemicals Market Outlook

- Historical Market Size (US$ Bn) Analysis, By Market, 2020-2025

- By Country

- By Product Type

- By Application

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026-2033

- Germany

- France

- U.K.

- Italy

- Spain

- Russia

- Rest of Europe

- Market Size (US$ Bn) Analysis and Forecast, By Product Type, 2026-2033

- Zinc Oxide

- Zinc Sulfate

- EDTA Chelated Zinc

- Sulphur Zinc Bentonite

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Application, 2026-2033

- Animal Feed

- Chemical Fertilizers

- Others

- Market Attractiveness Analysis

- Historical Market Size (US$ Bn) Analysis, By Market, 2020-2025

- East Asia Agricultural Grade Zinc Chemicals Market Outlook

- Historical Market Size (US$ Bn) Analysis, By Market, 2020-2025

- By Country

- By Product Type

- By Application

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026-2033

- China

- Japan

- South Korea

- Market Size (US$ Bn) Analysis and Forecast, By Product Type, 2026-2033

- Zinc Oxide

- Zinc Sulfate

- EDTA Chelated Zinc

- Sulphur Zinc Bentonite

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Application, 2026-2033

- Animal Feed

- Chemical Fertilizers

- Others

- Market Attractiveness Analysis

- Historical Market Size (US$ Bn) Analysis, By Market, 2020-2025

- South Asia & Oceania Agricultural Grade Zinc Chemicals Market Outlook

- Historical Market Size (US$ Bn) Analysis, By Market, 2020-2025

- By Country

- By Product Type

- By Application

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026-2033

- India

- Indonesia

- Thailand

- Singapore

- ANZ

- Rest of South Asia & Oceania

- Market Size (US$ Bn) Analysis and Forecast, By Product Type, 2026-2033

- Zinc Oxide

- Zinc Sulfate

- EDTA Chelated Zinc

- Sulphur Zinc Bentonite

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Application, 2026-2033

- Animal Feed

- Chemical Fertilizers

- Others

- Market Attractiveness Analysis

- Historical Market Size (US$ Bn) Analysis, By Market, 2020-2025

- Latin America Agricultural Grade Zinc Chemicals Market Outlook

- Historical Market Size (US$ Bn) Analysis, By Market, 2020-2025

- By Country

- By Product Type

- By Application

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026-2033

- Brazil

- Mexico

- Rest of Latin America

- Market Size (US$ Bn) Analysis and Forecast, By Product Type, 2026-2033

- Zinc Oxide

- Zinc Sulfate

- EDTA Chelated Zinc

- Sulphur Zinc Bentonite

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Application, 2026-2033

- Animal Feed

- Chemical Fertilizers

- Others

- Market Attractiveness Analysis

- Historical Market Size (US$ Bn) Analysis, By Market, 2020-2025

- Middle East & Africa Agricultural Grade Zinc Chemicals Market Outlook

- Historical Market Size (US$ Bn) Analysis, By Market, 2020-2025

- By Country

- By Product Type

- By Application

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026-2033

- GCC Countries

- Egypt

- South Africa

- Northern Africa

- Rest of Middle East & Africa

- Market Size (US$ Bn) Analysis and Forecast, By Product Type, 2026-2033

- Zinc Oxide

- Zinc Sulfate

- EDTA Chelated Zinc

- Sulphur Zinc Bentonite

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Application, 2026-2033

- Animal Feed

- Chemical Fertilizers

- Others

- Market Attractiveness Analysis

- Historical Market Size (US$ Bn) Analysis, By Market, 2020-2025

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping By Market

- Competition Dashboard

- Company Profiles (Details - Overview, Financials, Strategy, Recent Developments)

- UPL Limited

- Overview

- Segments and Product Type

- Key Financials

- Market Developments

- Market Strategy

- Syngenta

- Indian Farmers Fertiliser Cooperative

- Yara International

- Zochem

- EverZinc

- Rubamin

- Sulphur Mills

- Aries Agro

- Prabhat Fertilizer

- UPL Limited

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Agrochemicals

- Agricultural Grade Zinc Chemicals Market

Agricultural Grade Zinc Chemicals Market Size, Share, and Growth Forecast, 2026 - 2033

Agricultural Grade Zinc Chemicals Market by Product Type (Zinc Oxide, Zinc Sulfate, EDTA Chelated Zinc, Sulphur Zinc Bentonite, Others), Application (Animal Feed, Chemical Fertilizers, Others), and Regional Analysis for 2026 - 2033

Agricultural Grade Zinc Chemicals Market Size and Trends Analysis

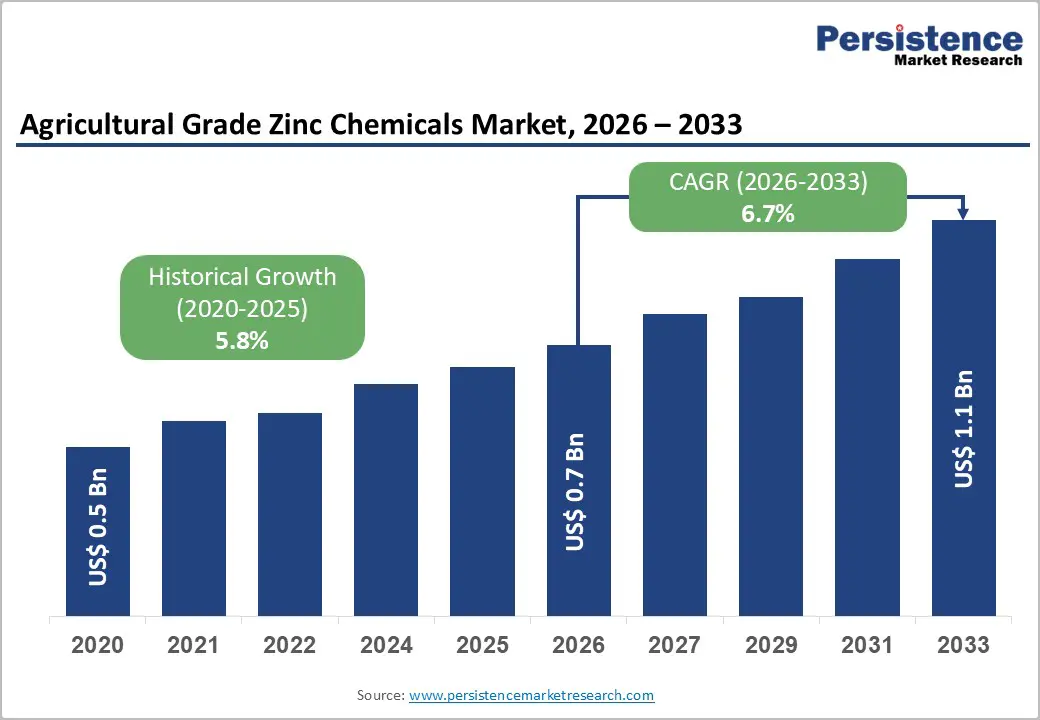

The global agricultural grade zinc chemicals market size is likely to be valued at US$0.7 billion in 2026, and is expected to reach US$1.1 billion by 2033, growing at a CAGR of 6.7% during the forecast period from 2026 to 2033, driven by the increasing prevalence of zinc deficiency in soils across major agricultural regions, rising demand for high-yield crop nutrition, and growing adoption of zinc-based micronutrient fertilizers and animal feed supplements to improve crop quality and livestock health.

Growing demand for zinc sulfate and EDTA chelated zinc, especially in chemical fertilizers for staple crops, is accelerating adoption across agribusinesses and farmers. Advances in granular formulations, chelated stability, and slow-release technologies are further boosting uptake by offering better nutrient availability and reduced leaching losses. Increasing recognition of agricultural-grade zinc chemicals as critical for correcting soil zinc deficiency, enhancing crop yield and quality, and supporting sustainable agriculture in emerging zinc-deficient markets remains a major driver of market growth.

Key Industry Highlights:

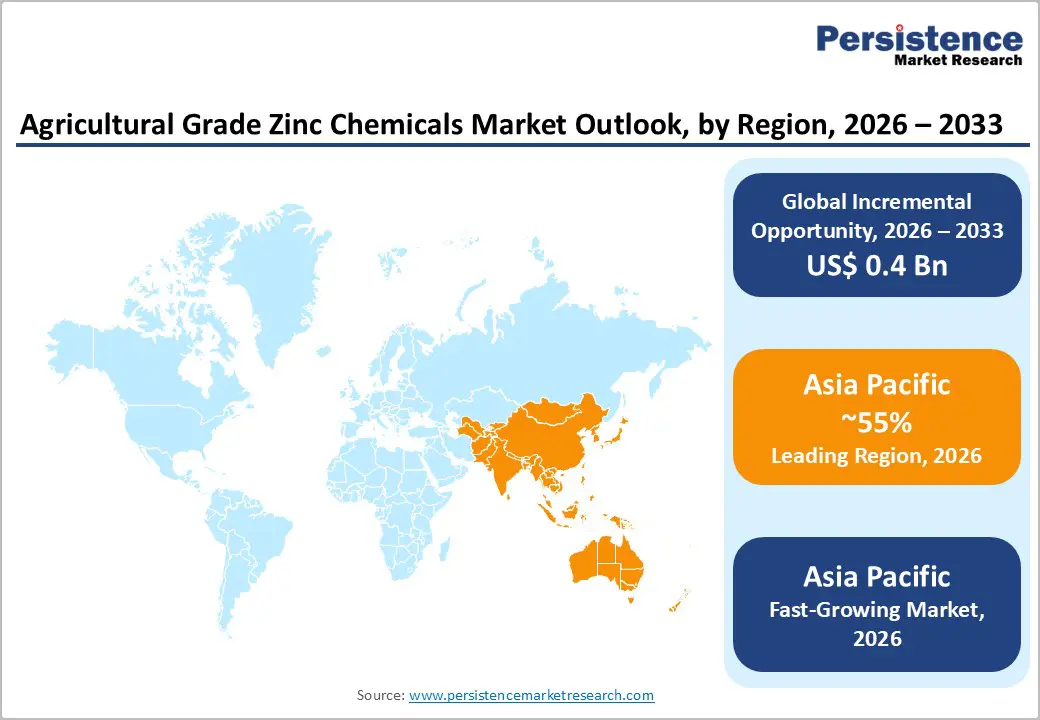

- Leading Region: Asia Pacific, anticipated to account for a 55% market share in 2026, driven by the largest arable land area, severe zinc deficiency in soils, and strong fertilizer consumption in India and China.

- Fastest-growing Region: Asia Pacific, fueled by the rapid expansion of zinc fertilizer programs, increasing awareness of micronutrient management, and the growing animal feed sector in India and Southeast Asia.

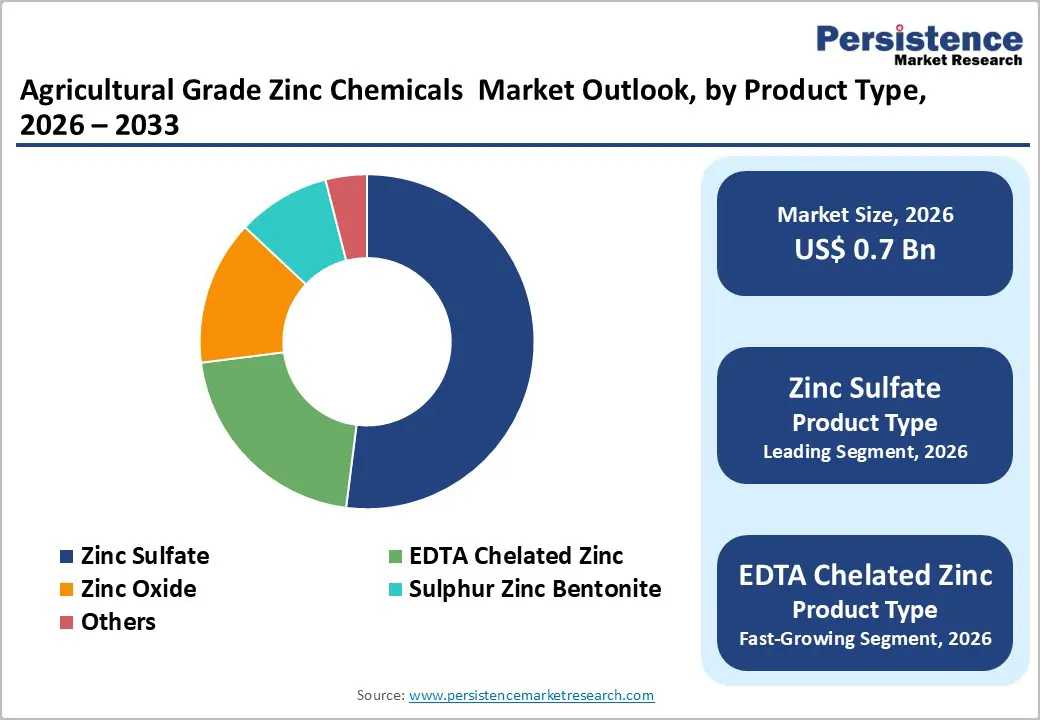

- Dominant Product Type: Zinc sulfate, to hold approximately 52% of the market share, as it remains the most cost-effective and widely used zinc source.

- Leading Application: Chemical fertilizers, to contribute nearly 62% of the market revenue, due to the highest volume usage in soil application.

| Key Insights | Details |

|---|---|

| Agricultural Grade Zinc Chemicals Market Size (2026E) | US$0.7 Bn |

| Market Value Forecast (2033F) | US$1.1 Bn |

| Projected Growth CAGR (2026 - 2033) | 6.7% |

| Historical Market Growth (2020 - 2025) | 5.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Widespread Soil Zinc Deficiency and Micronutrient Fertilizer Programs

Soil zinc deficiency is increasingly recognized as a critical constraint on agricultural productivity and drives demand for agricultural-grade zinc chemicals. Recent government-linked soil surveys indicate that a substantial proportion of agricultural soils, including those in major farming regions, are low in available zinc; for example, roughly 37% of Indian soil samples were found to be zinc-deficient according to assessments linked to national soil health data, limiting crop growth and yield potential. Globally, micronutrient mapping shows that more than 50% of the world’s agricultural soils exhibit zinc deficiency, underscoring the scale of the issue and the necessity of targeted micronutrient inputs. Such deficiencies occur due to repeated cropping and the use of NPK fertilizers that do not supply micronutrients, resulting in nutrient depletion over time.

To address these shortfalls, governments have instituted soil testing and micronutrient fertilization programs that explicitly recommend zinc application where soil analysis indicates deficiency. In India, schemes such as the Soil Health Card initiative integrate micronutrient recommendations, encouraging balanced nutrient use tailored to local soil conditions, which stimulates the adoption of zinc-containing fertilizers. Policy-backed fertilizer subsidy structures and customized nutrient programs further catalyze market uptake of agricultural zinc chemicals, as producers and farmers prioritize inputs that correct deficiencies and improve crop health, productivity, and quality across zinc-depleted regions.

Rising Animal Feed Zinc Supplementation and Regulatory Push

The agricultural-grade zinc chemicals market is increasingly supported by structured animal nutrition strategies and evolving regulatory frameworks. Zinc is a critical trace element in livestock diets, essential for growth, immune function, reproductive performance, and enzymatic processes; diets for various species commonly require supplementation in the range of 30-250 ppm to meet physiological needs and avoid deficiency-related conditions such as impaired growth and weakened immunity. Government and food safety authorities set maximum permissible zinc levels in animal feed to ensure both animal health and environmental protection, with regulatory bodies such as the European Union adjusting allowable zinc contents to balance nutritional requirements against environmental runoff concerns.

Regulatory attention to feed additive quality and environmental impact drives demand for standardized, compliant zinc supplements in animal feed formulations. Authorized zinc compounds (e.g., zinc oxide, zinc sulfate) are prescribed up to defined legal limits, and compliance with these regulations compels feed manufacturers to source quality-certified zinc chemicals tailored for animal nutrition. Following bans or limits on therapeutic use (e.g., high-dose zinc oxide in piglet feeds in some jurisdictions) and the alignment of national standards with international guidelines, zinc supplementation practices have shifted towards optimized, regulated inclusion rates.

Barrier Analysis - Price Volatility of Zinc Raw Materials

The agricultural-grade zinc chemicals market faces notable cost and planning challenges due to zinc raw material price volatility. Industrial zinc prices, which serve as the base for many zinc chemical derivatives, have shown wide fluctuations on benchmark platforms such as the London Metal Exchange; zinc prices have been both up and down significantly year-on-year as market supply, inventory levels, and global demand dynamics change. For example, average monthly LME cash zinc prices in early 2025 ranged around US$2,824.82/ton, but exhibited meaningful month-to-month variation, including a 7% drop from the previous month. Government-linked data also show LME stocks of zinc shifting by over 20% in recent reporting periods, movements that directly influence spot pricing.

For producers of agricultural zinc chemicals, this volatility translates into input cost uncertainty and margin pressure. Zinc concentrates and refined metal are key feedstocks for products such as zinc sulfate and zinc oxide used in micronutrient fertilizers and supplements; unpredictable price swings make it difficult for manufacturers to commit to long-term procurement contracts, set stable pricing for customers, or hedge against cost escalations.

Limited Farmer Awareness and Application Practices

Farmers’ limited understanding of micronutrient nutrition significantly constrains the uptake of agricultural-grade zinc chemicals. Government-collected data show that 70% of farmers apply micronutrients without conducting soil testing, leaving them unaware of actual soil zinc deficiency levels and appropriate application rates; this gap in soil diagnostics undermines efficient use of zinc products and can lead to suboptimal yields at the farm level. Without reliable soil test information, many growers default to traditional fertilizer practices focused on macronutrients such as nitrogen, phosphorus, and potassium, neglecting the value of micronutrients in crop health and quality.

In field surveys, only about 45% of farmers reported using zinc on any crop in the prior year, with many non-users citing lack of information on benefits and application methods as primary reasons. This limited awareness of zinc’s agronomic role restricts demand for agricultural-grade zinc chemicals and slows market expansion, particularly among smallholder farmers who depend on extension services for technical guidance.

Opportunity Analysis - Demand for Chelated Zinc and Custom Blends

Demand for chelated zinc and custom blend formulations presents a clear opportunity for the agricultural-grade zinc chemicals market by aligning product performance with real agronomic needs and regulatory soil health priorities. Zinc deficiency remains widespread: more than 50% of global agricultural soils are zinc-deficient, limiting crop productivity and making effective zinc nutrition a core fertilization priority for governments and extension agencies. Chelated zinc formulations (such as EDTA complexes) significantly improve zinc availability and uptake in crops, especially in alkaline or high-pH soils where conventional zinc sources often become unavailable, driving adoption among progressive growers seeking yield and quality gains. Custom blends that combine chelated zinc with other nutrients tailored to soil test results support precision agriculture approaches increasingly encouraged by national soil health programs and nutrient management guidelines, helping farmers maximize nutrient use efficiency and align with sustainable intensification policies.

Governments and agricultural bodies are promoting balanced micronutrient strategies as part of soil health initiatives and fertilizer recommendations, supporting wider use of advanced zinc supplements beyond traditional zinc sulfate products. Through customized nutrient packages, suppliers can meet evolving agronomic requirements while complying with extension service recommendations that stress soil diagnostic-based inputs. This enhances the value proposition for agricultural-grade zinc chemicals, positioning chelated zinc and tailored blends as performance-oriented, regulatory-aligned solutions that improve crop outcomes in zinc-limited production environments.

Developments in Zinc-Deficient Regions and Animal Nutrition

Expanding agricultural activity in zinc-deficient regions is creating tangible demand for agricultural-grade zinc chemicals. A significant portion of cultivated land worldwide exhibits low plant-available zinc, impacting crop growth, grain quality, and nutritional value. In response, national agricultural extension services in major producing countries are intensifying soil testing initiatives and recommending zinc supplementation as part of balanced fertilization programs. These efforts drive farmers to adopt zinc inputs that are agronomically effective and compliant with soil health guidelines. Improved access to soil diagnostics enables precise identification of deficiency hotspots, encouraging targeted use of zinc sulfate, chelated zinc, and blended micronutrient products. This shift from blanket fertilization practices to data-led nutrient management is increasing the uptake of zinc chemicals in both crop and horticultural sectors.

Developments in animal nutrition markets support the agricultural zinc chemicals sector. Zinc is essential in livestock diets for immune competence, growth performance, and reproductive health. Regulatory bodies and animal health authorities have established clear guidelines for zinc inclusion in feed, aiming to optimize animal productivity while minimizing environmental excretion. Feed formulators increasingly incorporate standardized zinc compounds to meet these specifications, driving consistent demand for high-quality zinc inputs. Growth in livestock production, especially in developing economies, further amplifies this trend, making zinc supplementation integral to modern feed strategies.

Category-wise Analysis

Product Type Insights

Zinc sulfate is anticipated to dominate the market, accounting for approximately 52% of the market share in 2026. Its dominance is driven by a strong balance of cost efficiency, agronomic performance, and broad regulatory acceptance. The compound offers high zinc content with reliable solubility, enabling fast correction of zinc deficiency in both soil and foliar applications. Compatibility with common fertilizer programs supports easy integration into existing nutrient management practices. Large-scale availability and established manufacturing capacity ensure a stable supply for fertilizers, blenders, and distributors. Yara International supplies zinc sulfate products (such as its YaraTera ZINC range) that are widely used in micronutrient fertilizers to address zinc deficiency in major crops such as corn and rice, helping improve crop health and yields through readily soluble zinc nutrition.

EDTA chelated zinc represents the fastest-growing product type, due to its superior nutrient availability and efficiency in plant uptake. The chelation process stabilizes zinc ions, preventing them from binding with soil minerals that make zinc unavailable to crops, especially in high-pH or calcareous soils. This enhanced bioavailability leads to more consistent correction of zinc deficiency with lower application rates compared to inorganic sources. EDTA-chelates also integrate easily into foliar and fertigation programs, providing flexibility for modern crop nutrition strategies. Agrisia Agro Private Limited markets Agrisia Zinc 12 EDTA, a chelated zinc micronutrient fertilizer formulated with EDTA to enhance zinc availability and plant uptake, especially in soils where conventional zinc sources are less effective; this product is used for foliar and fertigation applications across diverse crops.

Application Insights

Chemical fertilizers are expected to dominate the market, contributing nearly 62% of revenue in 2026, fueled by their established role in commercial agriculture and large-scale crop production. Farmers prioritize predictable nutrient delivery, fast crop response, and compatibility with mechanized application systems, which chemical formulations provide at scale. Strong distribution networks and standardized quality specifications support consistent procurement by cooperatives, agri-retailers, and contract farming programs. Integration with existing NPK fertilizer regimes enables seamless micronutrient fortification without operational disruption. Indian Farmers Fertilizers Cooperative Limited (IFFCO), which produces widely used chemical fertilizers such as urea, NPK blends, and DAP that form the backbone of crop nutrient programs in India; its supply plans show large volumes of indigenous DAP and urea dispatched across states, reflecting extensive market penetration and institutional backing by government departments for staple crop nutrition.

Animal feed represents the fastest-growing application, propelled by expanding livestock production and stricter nutritional standards for animal health. Zinc plays a vital role in enzyme function, immune response, and growth performance in poultry, swine, and ruminants, prompting formulators to include consistent and bioavailable zinc sources in feeds and premixes. Regulatory guidance on maximum safe inclusion levels encourages the use of standardized zinc sulfate and chelated zinc products that meet feed safety criteria. EverZinc, which produces high-quality zinc oxide products such as Afox 72-75, is specifically designed as a zinc source in animal nutrition and is included in feed premixes to support livestock enzyme function and growth performance.

Regional Insights

North America Agricultural Grade Zinc Chemicals Market Trends

North America is fueled by the region’s advanced precision agriculture, strong soil testing programs, and high public awareness of micronutrient management benefits. Distribution systems in the U.S. and Canada provide extensive support for zinc chemicals programs, ensuring wide accessibility across zinc sulfate, chemical fertilizers, and large farm populations. Increasing demand for chelated, convenient, and easy-to-apply forms is further accelerating the adoption, as these formats improve nutrient efficiency and reduce barriers associated with soil fixation.

Innovation in zinc chemicals technology, including stable chelated, improved foliar delivery, and targeted animal feed enhancement, is attracting significant investment from both public and private sectors. Government initiatives and USDA campaigns continue to promote use against deficiency risks, yield concerns, and emerging sustainable threats, creating sustained market demand. The growing focus on EDTA chelated grades and specialty uses, particularly for chemical fertilizers and others, is expanding the target applications for agricultural-grade zinc chemicals.

Europe Agricultural Grade Zinc Chemicals Market Trends

The growth of Europe is increasing awareness of micronutrient deficiency benefits, strong regulatory systems, and government-led soil health programs. Countries such as Germany, France, the U.K., and Spain have well-established agricultural frameworks that support routine zinc chemical use and encourage adoption of innovative chelated delivery methods. These high-efficiency formulations are particularly appealing for chemical fertilizer populations, regulation-conscious farmers, and animal feed users, improving yield and coverage rates.

Technological advancements in zinc chemical development, such as enhanced chelation, application-targeted delivery, and improved foliar grades, are further boosting market potential. European authorities are increasingly supporting research and trials for zinc against both routine and specialized needs, strengthening market confidence. The growing emphasis on convenient, sustainable options is aligned with the region’s focus on preventive soil degradation and food quality. Public awareness campaigns and promotion drives are expanding reach in both fertilizer and feed segments, while suppliers are investing in chelated forms and novel variants to increase efficacy.

Asia Pacific Agricultural Grade Zinc Chemicals Market Trends

Asia Pacific is projected to dominate and is expected to be the fastest-growing, capturing 55% share in 2026, supported by rising soil deficiency awareness, increasing government initiatives, and expanding application programs across the region. Countries such as China, India, Pakistan, and Bangladesh are actively promoting zinc campaigns to address yield gaps and emerging nutrition needs. Zinc chemicals are particularly attractive in these regions due to their cost-effective administration, ease of adoption, and suitability for large-scale chemical fertilizers and animal feed drives in both irrigated and rainfed areas.

Technological advancements are supporting the development of stable, effective, and easy-to-apply zinc chemicals, which can withstand challenging soil conditions and minimize fixation dependence. These innovations are critical for reaching domestic farmers and improving overall crop coverage. Growing demand for zinc sulfate, chemical fertilizers, and animal feed applications is contributing to market expansion. Public-private partnerships, increased agricultural expenditure, and rising investments in zinc research and distribution capacity are further accelerating growth. The convenience of zinc delivery, combined with improved yield and reduced risk of deficiency disorders, positions it as a preferred choice.

Competitive Landscape

The global agricultural grade zinc chemicals market reflects active competition between large fertilizer producers and specialized micronutrient suppliers, with regional strategies shaping market positioning. In Asia Pacific, UPL Limited and Aries Agro leverage dense distributor networks, field agronomist programs, and cost-efficient portfolios built around zinc sulfate and chelated zinc to drive penetration across cereals, oilseeds, and horticulture. In North America and Europe, Yara International and Rubamin compete through premium-grade inputs, quality assurance, and customized nutrition programs that strengthen accessibility for commercial farms.

Zinc sulfate remains the volume driver due to reliable performance and affordability, supporting large-scale integration into standard fertilizer regimes and reducing deficiency risk at the field level. Strategic partnerships, collaborations, and targeted acquisitions consolidate technical expertise, broaden micronutrient portfolios, and accelerate route-to-market execution. Chelated zinc formulations address availability constraints in alkaline soils, improving nutrient use efficiency and strengthening adoption in high-pH growing regions.

Key Industry Developments

- In December 2023, Rallis India, a Tata enterprise, introduced NAYAZINC, a patented zinc fertilizer for soil application, positioning it as a high-efficiency alternative to zinc sulphate across diverse crops, soils, and agro-climatic conditions. The company delivered a formulation with 16% zinc that enabled optimal zinc nutrition at nearly one-tenth the application rate of zinc sulphate, improving input efficiency for farmers. The product also contained 9% magnesium, supporting balanced plant nutrition and stronger early-stage development.

- In August 2023, The Mosaic Company announced the formation of the Mosaic Biosciences platform, a global initiative that brought advanced science and innovation to the agriculture market. The company introduced technologies through Mosaic Biosciences that enhanced crop health and supported natural biology in plants and soil, strengthening productivity outcomes. These solutions helped maximize the yield potential of every field by improving nutrient efficiency, soil function, and crop resilience across diverse growing conditions.

Companies Covered in Agricultural Grade Zinc Chemicals Market

- UPL Limited

- Syngenta

- Indian Farmers Fertiliser Cooperative

- Yara International

- Zochem

- EverZinc

- Rubamin

- Sulphur Mills

- Aries Agro

- Prabhat Fertilizer

Frequently Asked Questions

The global agricultural grade zinc chemicals market is projected to reach US$0.7 billion in 2026.

Widespread soil zinc deficiency and micronutrient fertilizer programs are key drivers.

The agricultural grade zinc chemicals market is poised to witness a CAGR of 6.7% from 2026 to 2033.

Chelated zinc and custom blends and expansion in zinc-deficient regions and animal nutrition are key opportunities.

UPL Limited, Yara International, Indian Farmers Fertiliser Cooperative, Syngenta, and Rubamin are the key players.