- Aerospace & Defense

- Aerial Imaging Market

Aerial Imaging Market Size, Share, and Growth Forecast 2026 - 2033

Aerial Imaging Market by Platform Type (Fixed Wing Aircraft, Helicopter, UAV, Others), Application (Geospatial Mapping, Disaster Management, Energy and Resource Management, Surveillance and Monitoring, Urban Planning, Others), End-user (Government, Military and Defense, Energy, Agriculture and Forestry, Civil Engineering, Media and Entertainment, Commercial, Others), and Regional Analysis for 2026 - 2033

Aerial Imaging Market Size and Trend Analysis

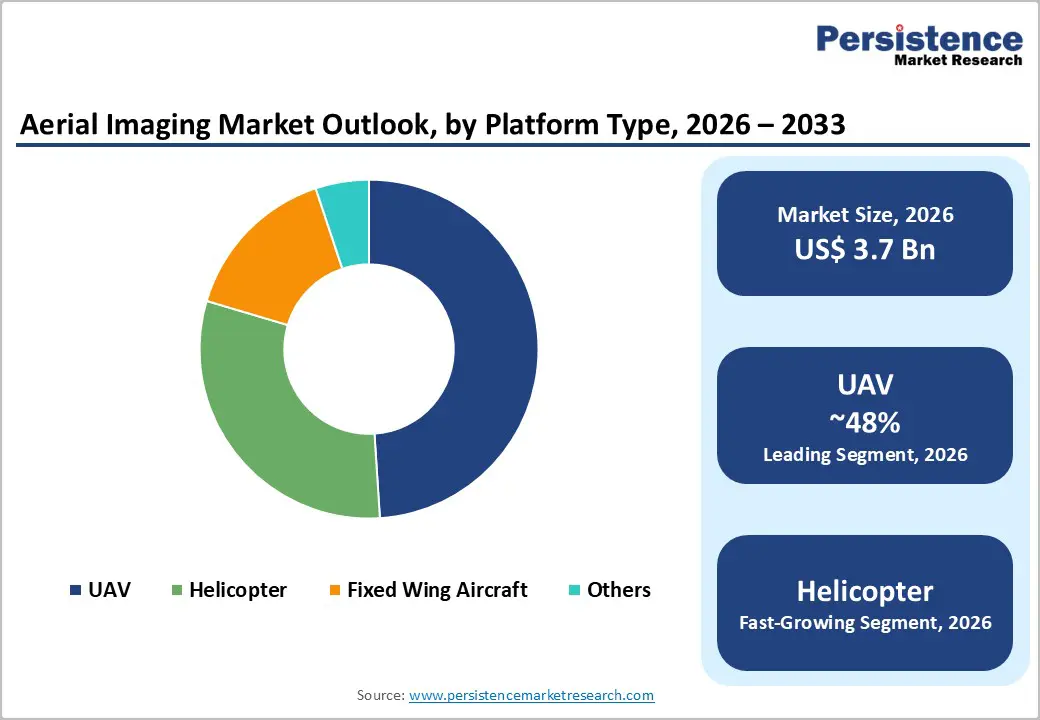

The global aerial imaging market size is estimated to be valued at US$ 3.7 Bn in 2026 and is projected to reach US$ 12.2 Bn by 2033, growing at a CAGR of 18.4% between 2026 and 2033.

This exceptional growth trajectory is driven by the rapid proliferation of UAV and drone technologies, accelerating adoption of AI-integrated geospatial analytics, and expanding demand across critical verticals, including government, defense, agriculture, and disaster management. The Federal Aviation Administration (FAA) had registered over 855,860 drones in the United States alone as of 2024, with commercial applications expanding steadily across industries.

Key Industry Highlights:

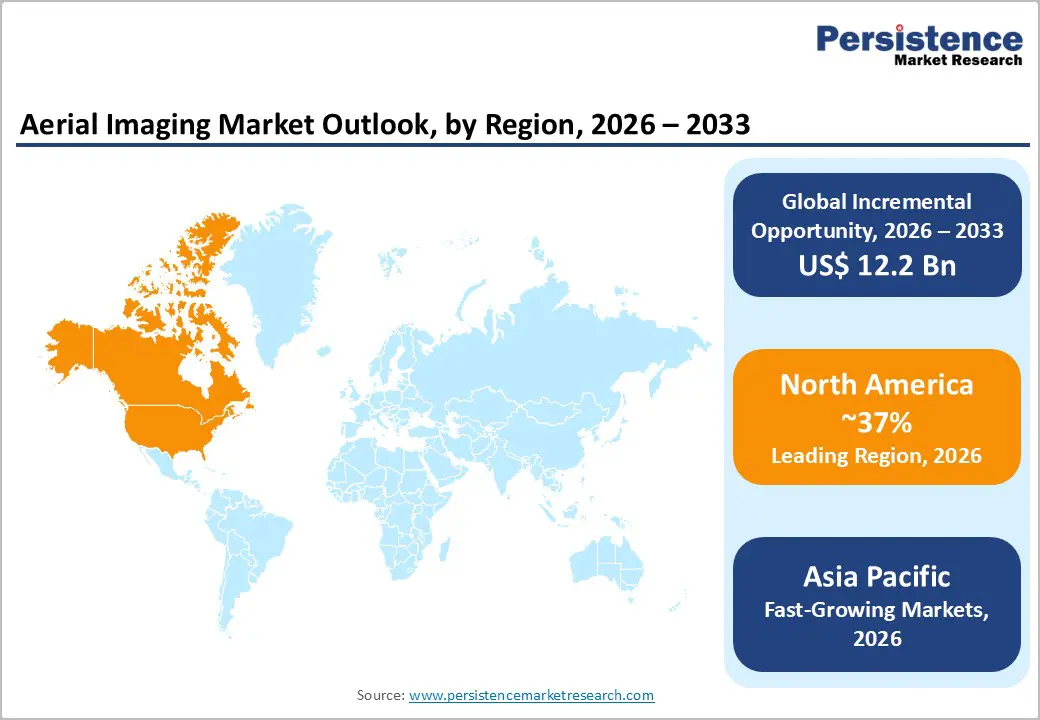

- Leading Region - North America holds approximately 37% of global Aerial Imaging revenue, driven by the U.S. government's substantial defense and surveillance UAV investments, a mature commercial drone ecosystem, and the FAA's BVLOS regulatory progression.

- Fastest Growing Region - Asia Pacific is the fastest-growing region at a 17.0% CAGR, led by China's 70% share of global commercial drone production, India's PLI-backed UAV manufacturing expansion, and South Korea's smart-city and 5G-enabled aerial imaging programs.

- Dominant Segment - UAVs command approximately 48% market share by platform type, driven by cost efficiency, imaging flexibility, AI payload integration, and government adoption with VTOL hybrid drones emerging as the fastest-growing UAV sub-category at 21.1% CAGR.

- Fastest Growing Segment - The Disaster Management application segment is forecast to grow at 18.4% CAGR through 2030, fueled by escalating climate-related events, real-time UAV situational awareness capabilities, and federal infrastructure renewal mandates for post-event aerial assessments.

- Key Market Opportunity - The FAA and TSA's August 2025 BVLOS NPRM marks a transformative regulatory milestone, creating a scalable pathway for long-range aerial surveying, agricultural monitoring, and infrastructure inspection fundamentally expanding the commercial aerial imaging addressable market.

| Key Insights | Details |

|---|---|

| Aerial Imaging Market Size (2026E) | US$ 3.7 Billion |

| Market Value Forecast (2033F) | US$ 12.2 Billion |

| Projected Growth CAGR (2026 - 2033) | 18.4% |

| Historical Market Growth (2020 - 2025) | 15.4% |

DRO Analysis

Drivers - Rapid Advancement of UAV and Drone Technologies with AI Integration

The accelerating technological sophistication of UAV encompassing higher resolution imaging sensors, extended flight endurance, autonomous navigation systems, and AI-driven analytics stands as the primary growth engine for the Aerial Imaging market. According to the FAA, commercial drone flights grew 25% in 2024 as 5G coverage and IoT gateways enabled real-time, low-latency data streaming for enterprise users. The integration of LiDAR payloads with AI algorithms now enables feature extraction converting raw point clouds into classified geospatial assets in hours rather than days.

Additionally, thermal and multispectral imaging capabilities are increasingly embedded in aerial platforms, elevating applications in border surveillance, environmental monitoring, precision agriculture, and infrastructure inspection. These technological strides are dramatically broadening the addressable use-case spectrum for aerial imaging service providers globally, sustaining strong demand momentum.

Expanding Government and Defense Procurement for Surveillance and Reconnaissance

Rising geopolitical tensions and increasing national security imperatives are fueling robust government and defense procurement of aerial imaging systems globally. In 2024, the U.S. Department of Defense allocated USD 50 million specifically to integrate advanced thermal imaging systems into drone platforms for border surveillance and tactical operations.

The U.S. government awarded Maxar Technologies a landmark USD 3.24 billion Enhanced View Optional Laydown (EOCL) contract, anchoring multi-year aerial and satellite imagery demand. Furthermore, India's Ministry of Defense allocated USD 600 million in 2024 to boost surveillance infrastructure with UAVs equipped with thermal and HD cameras. These investments across multiple nations confirm the government and defense segment as a reliable and high-value demand driver for the foreseeable future.

Restraints - Regulatory Complexity and Airspace Restrictions on Commercial Drone Operations

Fragmented and evolving regulatory frameworks governing commercial UAV operations represent a significant restraint on market scalability. While the FAA Reauthorization Act of 2024 mandated development of a BVLOS (Beyond Visual Line of Sight) rule, only 190 BVLOS waivers had been issued in the U.S. as of October 2024. This reflects on persistent approval bottlenecks.

Varying drone regulations across EU member states, Asia Pacific nations, and emerging markets create inconsistent operational environments, increasing compliance costs for aerial imaging service providers attempting to scale internationally and limiting their commercial deployment at scale.

Privacy Concerns and Legal Challenges to Aerial Data Collection

Growing public concern over privacy invasion from aerial surveillance is posing increasing legal and operational challenges. A U.S. Fifth Circuit ruling upheld Texas statutes that bar aerial image capture over private property without consent, narrowing commercial flight corridors. Furthermore, insurance carriers' growing drone use for property underwriting has triggered legal pushback, with 61% of risk managers citing privacy-liability concerns.

In Europe, GDPR (General Data Protection Regulation) compliance requirements restrict the collection and processing of identifiable imagery data, increasing legal complexity for commercial aerial imaging operators and constraining certain high-value application verticals.

Opportunities - Precision Agriculture and Environmental Monitoring: An Untapped High-Growth Vertical

The agriculture sector represents one of the most transformative growth opportunities for aerial imaging service providers, with multispectral and hyperspectral UAV payloads delivering measurable agronomic value. By mid-2024, over 500 million hectares had received drone-based treatment globally, resulting in savings of 210 million metric tons of water and a reduction of 47,000 metric tons of pesticides. Multispectral data elevates crop-stress detection, boosting yield forecasts by up to 20% when paired with AI analytics.

India's drone market is projected to expand at a CAGR of 16% through 2028, driven by government-backed crop insurance pilots and the Production-Linked Incentive (PLI) scheme for domestic UAV manufacturing. Eased drone-spraying regulations in the U.S., Brazil, and China widen operational footprints for aerial imaging players specializing in agri-tech solutions.

BVLOS Regulatory Normalization: Unlocking Large-Scale Commercial Applications

The regulatory normalization of Beyond Visual Line of Sight (BVLOS) drone operations is poised to unlock unprecedented commercial aerial imaging opportunities. On August 7, 2025, the FAA and TSA jointly published a landmark Notice of Proposed Rulemaking (NPRM) for BVLOS operations under the FAA Reauthorization Act of 2024, creating a structured pathway for large-scale aerial surveying, precision agriculture, infrastructure monitoring, and disaster response without the current case-by-case waiver system.

Canada's 2025 RPAS rules also formalized BVLOS approvals, easing cross-province pipeline-inspection workflows. Once BVLOS is normalized, service providers will be able to conduct long-range, high-frequency aerial imaging missions at significantly reduced operational costs, creating a step-change in market addressability particularly for energy infrastructure inspection, corridor mapping, and emergency response verticals.

Category-wise Analysis

Platform Type Insights

The UAV (Unmanned Aerial Vehicle) segment is the undisputed leader in the Aerial Imaging market by platform type, commanding approximately 48% of overall revenue share in 2026. UAVs have fundamentally disrupted traditional aerial imaging paradigms by offering a cost-effective, highly flexible, and rapidly deployable alternative to manned fixed-wing aircraft and helicopters.

Their ability to operate at low altitudes with high-resolution cameras, multispectral sensors, LiDAR, and thermal imaging payloads makes them ideally suited for precision agriculture, infrastructure inspection, and real-time disaster response. The FAA registered over 855,860 drones in the U.S. by 2024, reflecting the scale of adoption. Furthermore, the hybrid VTOL (Vertical Take-Off and Landing) platforms sub-category within UAVs is accelerating at a 21.1% CAGR through 2030, reinforcing the UAV segment's long-term dominance across diverse commercial and government applications globally.

Application Insights

Geospatial mapping is the leading application segment in the global Aerial Imaging market, accounting for approximately 33% of total revenue share in 2026. This leadership is grounded in persistent government, infrastructure, and resource management demand for accurate, up-to-date cadastral and topographic data. Geospatial mapping underpins critical activities including land use planning, utility corridor management, construction progress monitoring, and environmental impact assessment.

The U.S. and EU governments are major buyers of geospatial mapping services, funding large-scale initiatives through infrastructure renewal budgets. Advancements in LiDAR and AI-enhanced photogrammetry have further elevated precision and turnaround speed. Notably, the Disaster Management segment is forecast to grow at the fastest CAGR of 18.4% through 2030, as escalating climate-related events drive demand for real-time aerial situational awareness and rapid damage assessment.

End-user Insights

The government segment is the leading end-use category in the global Aerial Imaging market, holding approximately 27% of total revenue share in 2026. Governments worldwide deploy aerial imaging for a wide spectrum of applications, from border surveillance and urban planning to national disaster response and environmental regulation enforcement.

Major government contracts anchor revenue visibility for aerial imaging service providers: the U.S. government's USD 3.24 billion EOCL contract with Maxar Technologies and India's USD 600 million defense UAV allocation in 2024 exemplify the scale of public-sector demand. Near map Ltd. signed an agreement with U.S. federal agencies to provide aerial mapping tools and imagery covering over 80% of the U.S. population, supporting homeland security, infrastructure management, and FEMA resilience missions, underscoring government dominance in this market.

Regional Insights

North America Aerial Imaging Market Trends

North America is the leading region in the global aerial imaging market, contributing approximately 37% of total revenue in 2026. The United States drives regional dominance, supported by the world's largest defense and intelligence spending budget, a mature commercial drone ecosystem, and progressive regulatory frameworks. The FAA had issued 190 BVLOS waivers by October 2024, up from just 6 in 2020, reflecting accelerating regulatory openness. Key sectors driving demand include agriculture, construction, insurance, government, and energy infrastructure.

The innovation ecosystem in North America remains the global benchmark for aerial imaging technology development. In June 2025, President Trump signed the 'Unleashing American Drone Dominance' executive order, aimed at reducing regulatory barriers for BVLOS operations, a landmark policy signal for the commercial aerial imaging sector.

Asia Pacific Aerial Imaging Market Trends

Asia Pacific is the fastest-growing region in the global Aerial Imaging market, forecast to expand at a CAGR of 17.0% through 2033. China dominates the regional landscape, producing approximately 70% of global commercial drones, with domestic policy support channelled toward dual-use platforms valued at over 600 billion yuan by 2029. India is a rapidly emerging aerial imaging market, with the country's drone sector projected to grow at a CAGR of 16% through 2028.

Japan is advancing smart-city aerial imaging programs, with drone integration into urban management systems led by government-backed initiatives. South Korea is forecast to expand at a CAGR of 18.4% between 2026 and 2033, supported by 5G infrastructure, government-backed smart city programs, and Ministry of Land, Infrastructure and Transport (MOLIT)-enforced drone certification frameworks.

Europe Aerial Imaging Market Trends

Europe is the second-largest regional market for Aerial Imaging, with key contributors including Germany, the U.K., France, and Spain. The region benefits from well-established geospatial mapping traditions, strong investment in sustainable smart-city infrastructure, and a harmonized regulatory environment under the European Union Aviation Safety Agency (EASA) drone framework, which standardized UAV operational categories (Open, Specific, Certified) across EU member states.

Germany's engineering capabilities and France's investment in urban digital twins and precision agriculture imaging are driving high-value aerial data demand. The EU's Green Deal and Copernicus Earth Observation Program continue to fund large-scale aerial and satellite monitoring initiatives. Regulatory harmonization under EASA is enabling cross-border service delivery particularly beneficial for pan-European infrastructure corridor mapping.

Competitive Landscape

The global Aerial Imaging market exhibits a moderately fragmented competitive structure, characterized by a mix of large vertically integrated geospatial data companies, specialized aerial survey firms, and emerging drone-native tech platforms. The top five players collectively hold less than 40% of global revenue, leaving substantial space for regional specialists and disruptors. Market leaders including Eagle View Technologies, Near map, and Fugro are differentiating through AI-powered analytics platforms, frequent-capture imagery subscription models, and deep vertical integration.

Key Developments:

- In May 2025, John Deere completed the acquisition of Sentera, integrating drone-management software into Operations Centre for real-time agronomic insights.

- In April 2025, BRINC Drones raised USD 75 million Series C to scale solutions for first responders.

- In March 2025, Sikorsky demonstrated rotor-blown-wing UAS achieving 86-knot cruise and 40 VTOL transitions.

Companies Covered in Aerial Imaging Market

- Google Inc.

- Cooper Aerial Surveys Co.

- Digital Aerial Solutions (DAS), LLC

- EagleView Technologies, Inc. and Pictometry International Corp.

- Fugro

- Global UAV Technologies Ltd.

- Kucera International

- Nearmap

- Landiscor

- Greenman-Pedersen, Inc.

Frequently Asked Questions

The global Aerial Imaging market is projected to reach US$ 12.2 Billion by 2033, growing from an estimated US$ 3.7 Billion in 2026, at a CAGR of 18.4% during the forecast period. The market recorded a historical CAGR of 15.4% between 2020 and 2025, reflecting the rapid and sustained adoption of aerial imaging technologies across both government and commercial end-use sectors.

Core demand drivers include the rapid technological advancement of UAVs and AI-integrated geospatial analytics supported by the FAA's registration of over 855,860 drones in the U.S. by 2024 and 25% growth in commercial drone flights in 2024.

The UAV segment leads by platform type, holding approximately 48% of total revenue share in 2024. UAVs' competitive advantage lies in their operational flexibility, cost efficiency, and compatibility with advanced payloads including LiDAR, thermal imaging, and multispectral sensors.

North America is the leading regional market, accounting for approximately 37-38% of global revenue in 2024. U.S. leadership is reinforced by substantial government defense and intelligence procurement, strong FAA regulatory support (including 190 BVLOS waivers issued by October 2024), and the presence of market leaders including EagleView Technologies, Nearmap, and Google Inc.

Leading companies in the global Aerial Imaging market include EagleView Technologies, Inc., Fugro N.V., Nearmap Ltd., Google Inc., Maxar Technologies, DroneDeploy, Inc., Vexcel Imaging GmbH, Digital Aerial Solutions (DAS), LLC, Teledyne FLIR LLC, and Pix4D SA, among others.