- Industrial Machinery

- Wine Processing Equipment Market

Wine Processing Equipment Market Size, Share, and Growth Forecast 2026 - 2033

Wine Processing Equipment Market by Wine Type (Red, White, Sparkling, Fortified), Equipment Type (Crushing & Pressing Equipment, Fermentation Equipment, Filtration Equipment, Bottling Equipment, Temperature Control Equipment, Storage Tanks, Others), Automation Level (Manual, Semi-automatic, Automatic), and Regional Analysis for 2026 - 2033

Wine Processing Equipment Market Size and Trend Analysis

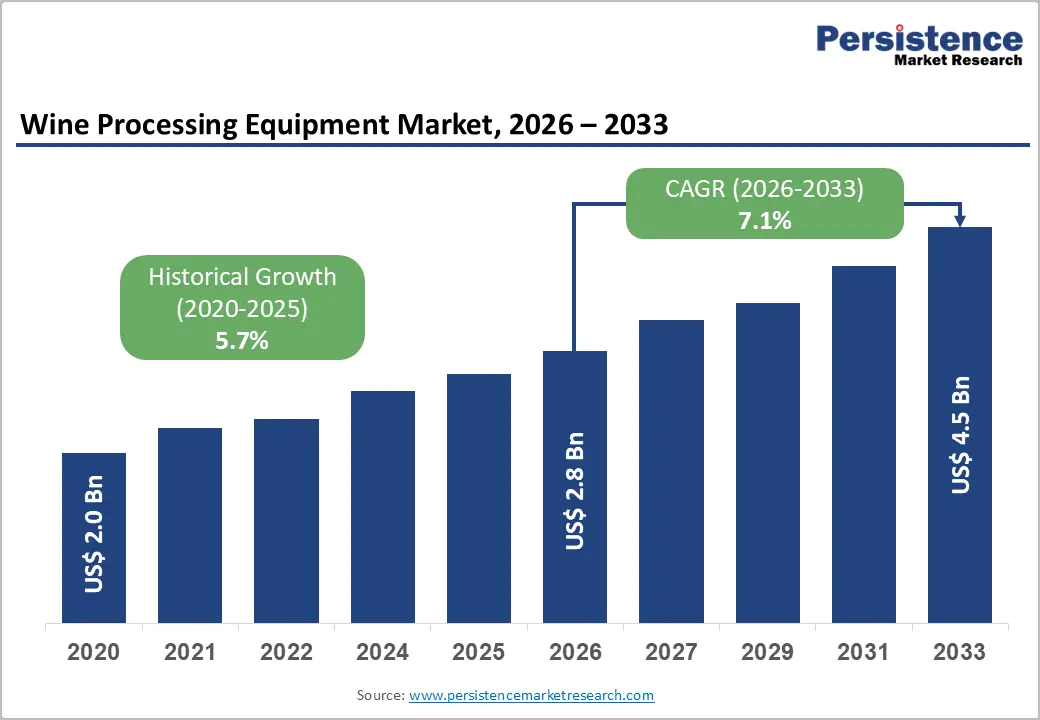

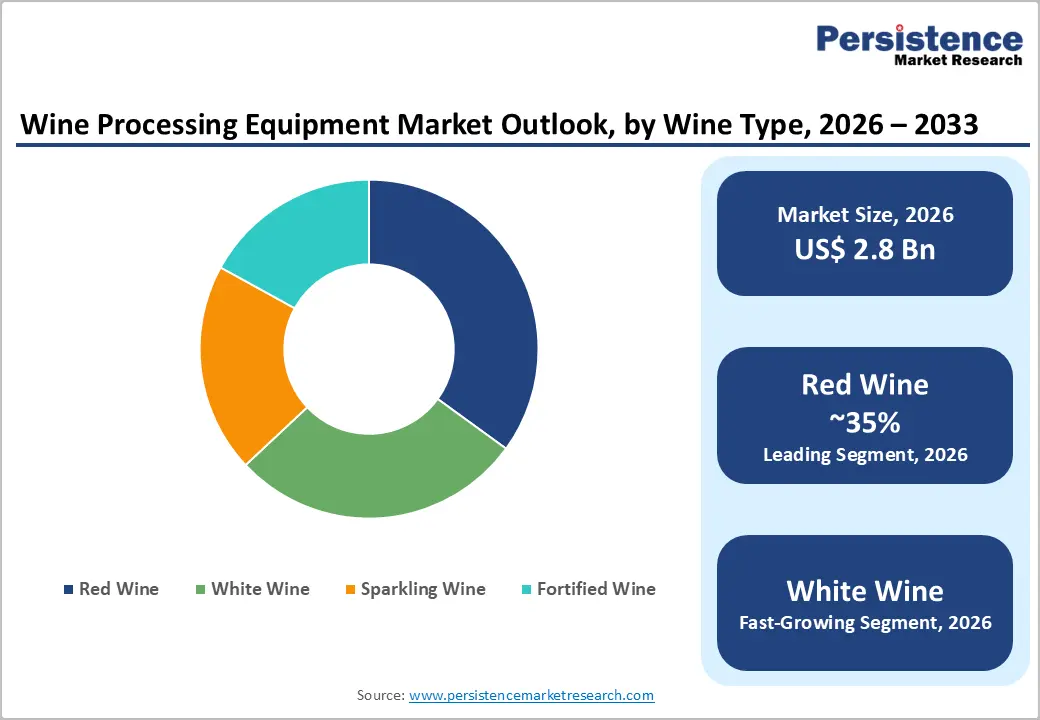

The global wine processing equipment market size is valued at US$ 2.8 Bn in 2026 and is projected to reach US$ 4.5 Bn by 2033, growing at a CAGR of 7.1% between 2026 and 2033.

The market is primarily driven by the global acceleration of wine premiumization, compelling wineries to invest in precision processing equipment to meet quality benchmarks. According to the International Organization of Vine and Wine (OIV), global wine production reached 225.8 million hectolitres in 2024, with producers increasingly investing in advanced crushing, fermentation, and filtration systems to extract maximum quality from constrained volumes.

Key Market Highlights

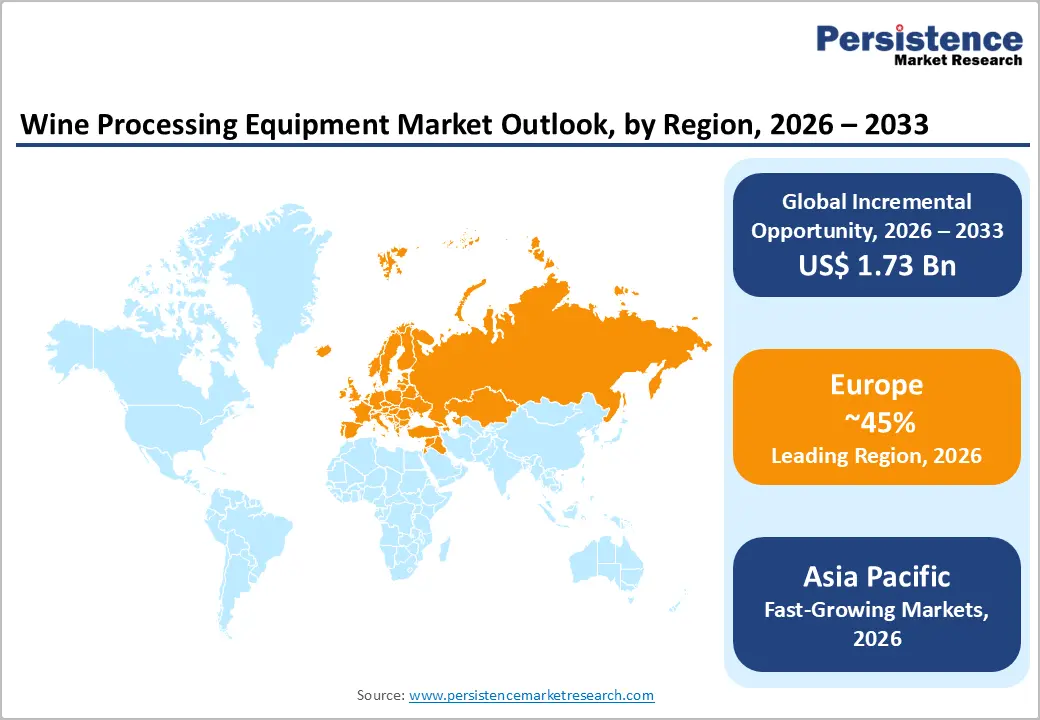

- Leading Region: Europe dominates the global wine processing equipment market with ~45% revenue share in 2024, driven by France, Italy, and Spain's concentrated wine production infrastructure and EU sustainability regulations mandating equipment modernization.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, led by India's vineyard expansion at 4.5% CAGR and major winery investments by Treasury Wine Estates and Penfolds in China, driving strong equipment procurement activity.

- Dominant Segment: Crushing & Pressing Equipment commands the largest equipment type share at approximately 34%, reflecting its indispensable role across all winery scales and the ongoing shift toward pneumatic membrane pressing solutions for premium wine production.

- Fastest Growing Segment: The Automatic equipment segment is the fastest-growing automation tier as commercial wineries globally prioritize fully automated fermentation, bottling, and quality-control systems to reduce labor costs and improve batch consistency.

- Key Market Opportunity: Sustainability-driven equipment upgrade programs supported by the EU's Common Agricultural Policy (CAP) and rising demand for energy-efficient filtration and fermentation systems offer significant long-term revenue opportunities for eco-focused equipment manufacturers.

| Key Insights | Details |

|---|---|

|

Wine Processing Equipment Market Size (2026E) |

US$ 2.8 Bn |

|

Market Value Forecast (2033F) |

US$ 4.5 Bn |

|

Projected Growth CAGR (2026–2033) |

7.1% |

|

Historical Market Growth (2020–2025) |

5.7% CAGR |

DRO Analysis

Market Growth Drivers

Rising Premiumization and Craft Wine Production Boosting Equipment Demand

The global shift toward premium and craft wines represents one of the strongest tailwinds for wine processing equipment manufacturers. According to the OIV, while global wine consumption declined to 214.2 million hectolitres in 2024, the lowest since 1961, the average export price of wine peaked at EUR 3.60 per liter, reflecting robust premiumization.

Consumers are increasingly seeking artisanal, organic, and limited-edition wines, compelling wineries to invest in precise fermentation tanks, gentle pressing systems, and advanced filtration equipment that preserve varietal integrity. The growing number of boutique and micro-wineries worldwide further fuels demand for compact, flexible, and customizable processing lines capable of handling small batches of high-value wine at scale.

Technological Integration of IoT, AI, and Automation in Winery Operations

The rapid adoption of Internet of Things (IoT)-enabled systems and artificial intelligence in winery operations is significantly reshaping equipment procurement cycles. Modern processing equipment, equipped with real-time sensors, continuously monitors fermentation temperature, pressure, pH, and sugar levels, enabling data-driven adjustments that improve wine consistency and reduce batch losses.

According to Wine Industry Advisor, advanced crossflow filtration systems integrated with IoT platforms can reduce energy and water consumption by up to 60% compared to conventional systems. The commercial adoption of automated bottling lines, smart fermentation tanks, and AI-driven quality control systems further accelerates equipment replacement cycles globally, particularly in North America and Europe, where labor costs are high, and winery modernization programs are actively underway.

Market Restraints

High Capital Investment Requirements Limiting SME Adoption

A key challenge confronting the wine processing equipment market is the substantial upfront capital cost associated with advanced automated processing lines. Small and medium-sized wineries, which comprise most producers in regions such as Europe and the Asia Pacific, often find it difficult to justify investments in state-of-the-art stainless steel fermentation systems, automated bottling equipment, or IoT-integrated filtration units.

The U.S. Bureau of Labor Statistics recorded over 5,024 wineries in the United States alone as of 2020, many of which are small-scale producers operating on thin margins. High installation, maintenance, and operator training costs continue to suppress adoption among these operators, limiting overall market expansion.

Declining Global Wine Consumption Creating Capex Uncertainty

Structural decline in global wine consumption is prompting hesitancy among winery operators to invest. The OIV confirmed that global wine consumption fell 3.3% in 2024, marking the third consecutive year of decline and the lowest level since 1961. China's consumption alone contracted by 19.3% in 2024, averaging a loss of 2 million hectolitres annually since 2018.

This persistent demand softness discourages large-scale capacity expansions and delays capital equipment procurement, particularly in mature markets where wineries are already operating under overcapacity conditions.

Market Opportunities

Rapid Wine Industry Expansion in the Asia Pacific is Opening New Equipment Markets

The Asia Pacific region presents significant untapped demand for wine processing equipment, driven by expanding domestic wine production infrastructure. India's vineyard area reached 185,000 hectares in 2024, registering an annual growth rate of 4.5% since 2019, according to the OIV. In August 2024, Penfolds confirmed plans to build new vineyard and winery facilities in China, while Treasury Wine Estates acquired a 75% stake in Ningxia Stone & Moon Winery in December 2024.

These large-scale investments necessitate the procurement of complete winery processing lines from crushing and destemming equipment to automated bottling systems. Rapid urbanization, rising disposable incomes, and growing wine culture in emerging Southeast Asian economies such as Vietnam and Thailand further support long-term equipment demand in the region.

Sustainability-Driven Equipment Upgrades Creating Long-Term Revenue Pools

Increasing regulatory and consumer pressure on environmental sustainability is generating a new wave of equipment upgrade projects at wineries globally. The European Union's Common Agricultural Policy (CAP) actively supports sustainable winemaking practices, incentivizing wineries to replace energy-intensive conventional systems with eco-friendly alternatives. Advanced filtration systems with membrane technology can substantially reduce water and chemical consumption, aligning with environmental targets.

Equipment manufacturers offering modular, low-emission, and water-efficient processing solutions are well-positioned to capitalize on this trend. The global sparkling wine segment, growing fastest among wine categories, demands specialized secondary fermentation equipment and precise temperature-control systems, creating additional revenue opportunities for equipment suppliers serving premium producers.

Category-wise Analysis

Wine Type Insights

The Red Wine segment leads the wine processing equipment market by wine type, with approximately 34% market share. Red wine's dominance is sustained by its deep-rooted cultural acceptance across the world's largest wine-consuming regions, including France, Italy, the United States, and China. Red wine production requires specialized maceration tanks, extended fermentation systems, and temperature-controlled aging infrastructure, resulting in higher per-unit equipment costs than for other wine types.

According to the OIV, red wine accounted for 42% of total global wine production as recently as 2021, maintaining its status as the most widely produced category globally. While the share has modestly declined from its 48% peak at the start of the century due to the white and sparkling surge, red wine remains the primary driver of mid- to large-capacity winery equipment investments worldwide.

Equipment Type Insights

The Crushing & Pressing Equipment segment leads the wine processing equipment market by equipment type, commanding approximately 34% of the total market share, consistent with data from Market Research, which pegged the crushing, destemming and pressing segment at 34.3% revenue share in 2024. This dominance reflects the indispensable nature of primary processing machinery at every scale of wine production.

Wineries of all sizes require destemmers, grape crushers, and pneumatic presses regardless of their automation level or wine style. Technological advances such as membrane presses, gravity-fed systems, and stainless-steel distemper-crusher units have raised the average selling price of this equipment category. Compact and versatile pneumatic pressing solutions are especially sought after by premium and craft producers who prioritize gentle extraction to preserve polyphenols and aromatics.

Automation Level Insights

The Automatic equipment segment is the dominant automation tier in the wine processing equipment market, accounting for an estimated 45% share. Fully automated systems command this lead due to their proven ability to reduce labor overhead, accelerate processing throughput, and deliver batch-consistent quality that manual and semi-automatic alternatives cannot replicate at commercial scale.

Automated grape sorting tables, programmable logic controller (PLC)-driven fermentation tanks, and robotic bottling lines are now considered standard at mid-to-large commercial wineries. According to industry sources, automated machines are estimated to hold a major market share in the coming years, as automation reduces manual labor and accelerates production processes across sorting, crushing, pressing, and bottling operations. Major equipment manufacturers, including Criveller Group and Paul Mueller Company, continue to expand their automated product portfolios to serve this growing segment.

Regional Analysis

Europe

Europe dominates the global wine processing equipment market, holding the largest regional revenue share of approximately 45% in 2026, according to Market Research. The region's pre-eminence is anchored by its unrivalled concentration of wine production in France, Italy, Spain, and Germany. Italy remained the world's largest wine producer in 2024 at 44.1 million hectoliters, while Spain recorded a 9.3% production increase to 31 million hectoliters in 2024, as confirmed by the OIV. European wineries are at the forefront of adopting precision fermentation and membrane filtration technologies to maximize quality from smaller harvests driven by climate variability.

The European Union's Common Agricultural Policy (CAP) and sustainability mandates are major catalysts for equipment modernization across the region. Germany and the U.K. both major wine importers are investing in local bottling and packaging infrastructure to meet domestic labelling and food safety requirements. The U.K. wine market is increasingly focused on English sparkling wine production, creating new demand for specialized secondary fermentation and disgorging equipment.

Asia Pacific

Asia Pacific is the fastest-growing regional market for wine processing equipment, driven by large-scale winery investments and rapidly expanding domestic production infrastructure across China, India, and Australia. India's vineyard area grew at a 4.5% annual rate to reach 185,000 hectares by 2024, according to the OIV, supporting consistent demand for primary and secondary processing equipment. In October 2024, Omnia Technologies announced a strategic joint venture with Economy Process Solutions in India to supply processing and packaging equipment to the growing Indian beverage sector, reflecting the opportunity in this emerging market.

China remains the largest wine market in the region by revenue. Penfolds' confirmed plans to build winery facilities in China in August 2024, alongside Treasury Wine Estates' acquisition of a 75% stake in Ningxia Stone & Moon Winery in December 2024, signal strong investment conviction in Chinese domestic wine production. Following the removal of tariffs on Australian wine imports in March 2025, shipments rebounded to AUD 1.03 billion within a year, further boosting winery modernization activity in Australia.

North America

North America holds a leading position in the global wine processing equipment market, accounting for approximately 35% of total revenue share. The United States is the region's primary growth engine, home to over 5,024 registered wineries, more than four times the count recorded in 2001, as documented by the U.S. Bureau of Labor Statistics.

The U.S. wine market is estimated at approximately USD 45 billion, according to the Wine Institute, with wine regions such as California's Napa Valley and Sonoma County continually upgrading processing infrastructure to maintain premium-quality standards. The emphasis on artisanal and reserve wine tiers compels North American wineries to invest in state-of-the-art fermentation and filtration technologies.

The region's innovation ecosystem is robust, with equipment manufacturers such as G.W. Kent Inc. and Criveller Group actively expanding their North American service infrastructure. Regulatory frameworks under the U.S. Alcohol and Tobacco Tax and Trade Bureau (TTB) continue to enforce stringent quality and safety standards for winery operations, supporting sustained demand for compliant, modern equipment solutions.

Competitive Landscape

The global wine processing equipment market is moderately fragmented, characterized by a mix of established European and North American manufacturers and emerging regional players. No single company holds a commanding share, reflecting the specialized nature of equipment requirements across different winery scales and geographies. Market leaders differentiate through full-line solution capabilities covering crushing, fermentation, filtration, and bottling supported by regional service networks.

Key strategies include partnerships with research institutions to develop next-generation pressing and filtration technology, geographic expansion into Asia Pacific, and the integration of IoT and smart automation into conventional product lines. Emerging business models focus on modular, scalable systems that serve micro-wineries and artisanal producers, while established players target large commercial wineries with high-capacity automated lines and ERP-compatible equipment.

Key Market Developments

- In April 2024, Agrovin launched Ultrawine Perseo, a unique winery harvesting and processing solution that expands the company's portfolio for wineries requiring versatile, high-throughput equipment for modern production demands.

- In October 2024, Omnia Technologies announced a strategic joint venture with Economy Process Solutions in India to establish a leading supplier of processing and packaging equipment for the Indian beverage and pharmaceutical industries.

Companies Covered in Wine Processing Equipment Market

- Adamark Air Knife Systems

- Agrovin

- Criveller Group

- DT Pacific Pty. Ltd.

- G.W. Kent Inc.

- Love Brewing Limited

- Northern Brewer

- Paul Mueller Company

- Grapeworks Pty Ltd.

- Vitikit Ltd.

- SRAML

- Della Toffola Group

- Omnia Technologies Group

- ZAMBELLI Enotech s.r.l.

- Bucher Industries AG

- GEA Group AG

Frequently Asked Questions

The global Wine Processing Equipment Market is valued at US$ 2.8 Bn in 2026 and is projected to reach US$ 4.5 Bn by 2033, expanding at a CAGR of 7.1% during the forecast period.

The market is primarily driven by the premiumization of wine globally compelling wineries to invest in advanced crushing, fermentation, filtration, and bottling systems alongside rapid adoption of IoT-enabled automation and energy-efficient technologies.

The Crushing & Pressing Equipment segment leads the market, accounting for approximately 34% of total revenue share. Its dominance stems from the universal requirement for primary processing machinery at every winery scale, combined with technological advancements in pneumatic membrane pressing and stainless steel destemmer-crusher systems that improve quality extraction.

Europe leads the global market with approximately 45% revenue share, driven by the world's highest concentration of wine production in Italy, France, and Spain. The region's deep-rooted wine heritage, EU sustainability regulations, and strong winery modernization programs maintain its market leadership position.

Key players operating in the global wine processing equipment market include Paul Mueller Company, Criveller Group, Agrovin, G.W. Kent Inc., Grapeworks Pty Ltd., Vitikit Ltd., DT Pacific Pty. Ltd., Northern Brewer, Love Brewing Limited, Adamark Air Knife Systems, SRAML, Omnia Technologies Group, and Della Toffola Group, among others.