- Oil & Gas

- Turboexpander Market

Turboexpander Market Size, Share, and Growth Forecast 2026 - 2033

Turboexpander Market by Product Type (Radial Flow, Axial Flow), Loading Device (Compressor-loaded, Generator-loaded), Application (LNG Processing, Air Separation), End-user (Oil and Gas, Industrial Gases), and Regional Analysis, 2026 - 2033

Turboexpander Market Size and Trends Analysis

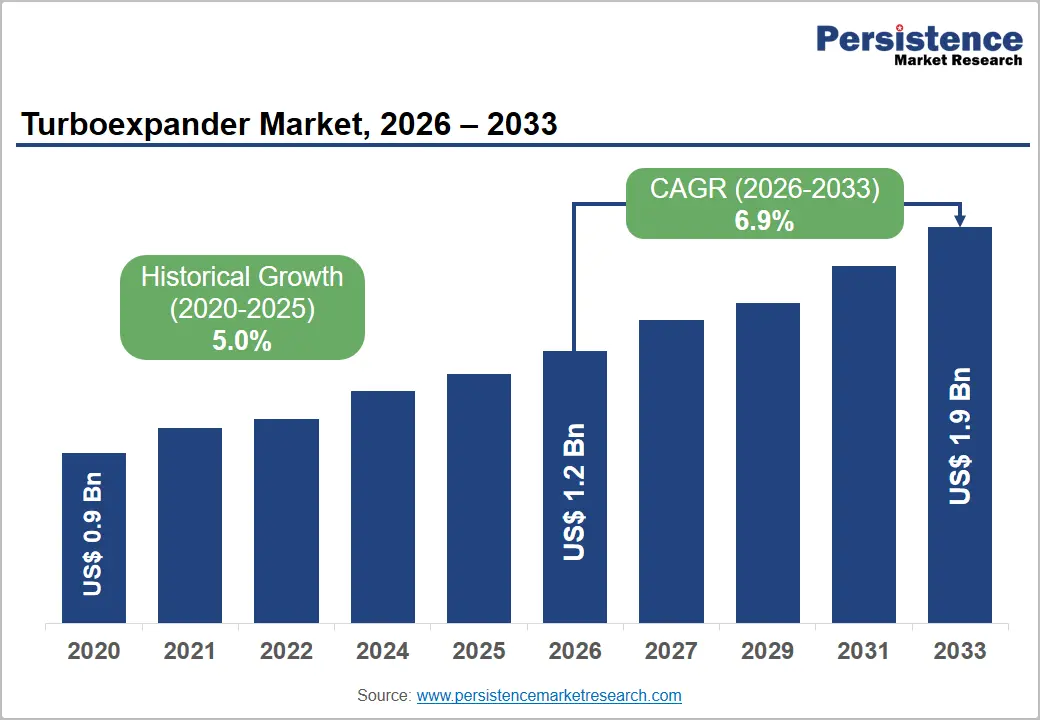

The global turboexpander market size is likely to be valued at US$1.2 billion in 2026 and is estimated to reach US$1.9 billion by 2033, growing at a CAGR of 6.9% during the forecast period from 2026 to 2033, driven by the ongoing expansion of LNG liquefaction capacity and rising deployment of pressure energy recovery systems across natural gas transmission networks. Surging adoption of high-efficiency radial turboexpanders and generator-loaded systems is further supporting market growth by improving energy efficiency.

Key Industry Highlights:

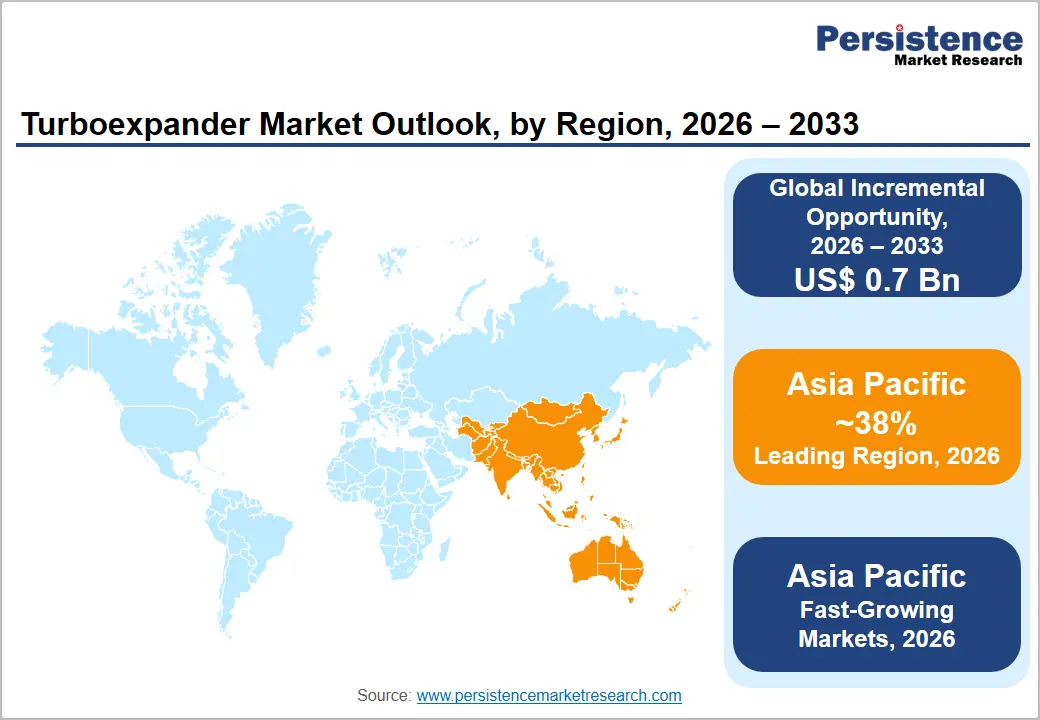

- Leading Region: Asia Pacific, with about a 37.2% share in 2026, fueled by ongoing expansion of LNG infrastructure and industrial gas production.

- Fast-growing Region: Europe, backed by investments in LNG infrastructure and hydrogen projects.

- New Product: Cryostar recently expanded its hydrogen-focused turbomachinery portfolio by introducing H2 turboexpanders designed for liquid hydrogen production. The new systems incorporate magnetic bearing technology for oil-free operation, improving reliability and efficiency in cryogenic hydrogen liquefaction while supporting emerging hydrogen infrastructure projects.

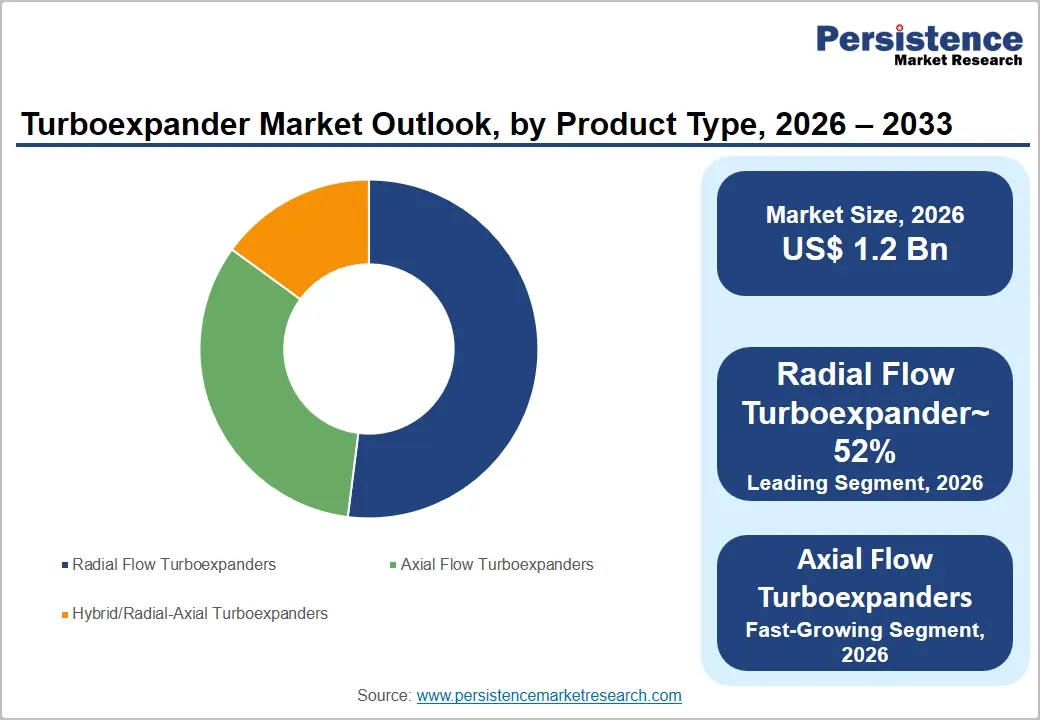

- Leading Product Type: Radial flow turboexpanders, with approximately 52.1% share in 2026, as they provide high efficiency across a wide operating range while maintaining a compact and reliable design.

- Dominant Loading Device: Compressor-loaded turboexpanders, with nearly 42.4% share in 2026, as they recover expansion energy to drive process compressors, significantly improving plant energy efficiency.

DRO Analysis

Driver - Expansion of LNG Capacity Globally

Every Liquefied Natural Gas (LNG) liquefaction train requires turboexpanders to achieve the cryogenic temperatures needed to convert gas into liquid form. These machines expand high-pressure gas to produce extremely cold temperatures, typically below -160°C, thereby driving the liquefaction process. The current wave of LNG construction is the largest in history. According to the International Energy Agency's (IEA) Global LNG Capacity Tracker, between 2025 and 2030, approximately 345 billion cubic meters per year (bcm/yr) of new LNG export capacity is set to come online from projects that have already reached Final Investment Decision (FID) and are under construction.

Annual capacity additions are projected to peak at approximately 95 bcm/yr in 2028, creating substantial demand for turboexpanders across new liquefaction facilities. This translates into turboexpander procurement. In January 2026, Chart Industries acquired a small-scale turboexpander technology company specifically to extend its cryogenic processing solutions portfolio. IHI Corporation also announced compact turboexpander systems customized for small- to mid-scale LNG facilities. Both moves showcase that manufacturers are extending supply in line with the construction pipeline.

Operators to Demand Turboexpanders for Energy-Recovery Projects

Natural gas must be pressurized to move efficiently through long-distance transmission pipelines, then stepped down in pressure at distribution stations before it can be delivered safely to end-users. This pressure drop has historically been performed using throttling valves that dissipate energy as heat. Turboexpander-generators replace these valves or run in parallel with them, converting the pressure differential into electricity instead. Sapphire Technologies' FreeSpin In-line Turboexpander systems are designed specifically for this application, with the company noting that assets in the energy sector often contain ready-to-develop pressure resources. These include natural gas wells that must be choked prior to processing and transmission pipelines that must be let down before interconnecting with local distribution pipelines.

The commercial momentum behind this category is confirmed by investment activity. In September 2025, for instance, Sapphire Technologies closed a US$18 million Series C financing round. It included Mitsubishi Heavy Industries as a strategic investor, with capital allocated specifically to expand manufacturing capacity and surge its installed base in Japan and other key geographies. This confirmed that pressure-letdown energy recovery is transitioning from niche to mainstream deployment.

Restraint - Volatile Oil and Gas Investments to Create Uncertain Order Pipelines

The majority of turboexpander applications sit within oil and gas Exploration and Production (E&P) operations, making procurement decisions dependent on capital spending cycles. When oil prices fall, E&P companies cut budgets, defer projects, and delay equipment purchases. The current cycle illustrates this scenario. According to RBN Energy's April 2026 analysis of 36 leading U.S. E&P companies, 2026 capital investment is set at US$59.1 billion, down 5% from US$62.5 billion in 2025 and continuing a moderation from the recent peak in 2023. This is because low oil prices are eroding returns and companies are prioritizing cash generation over growth.

The Federal Reserve Bank of Dallas confirmed the structural nature of this risk in a March 2025 publication. It noted that the oil and gas markets are highly volatile, with prices subject to fluctuations, fueled by geopolitical events, supply-demand imbalances, natural disasters, and policy changes. In the past, downturns in oil and gas markets led to surges in bankruptcies, loan defaults, and impaired asset quality for banks with exposure to the industry. For turboexpander manufacturers serving E&P customers, this cyclicality creates unpredictable order books and complicates long-term capacity planning.

Opportunity - Strict Flaring Norms to Propel Adoption of Wellhead Micro-Turboexpanders

Oil and gas producing pads typically require electricity for pumps, compressors, lighting, and control systems. Until recently, many relied on grid power or diesel generators while flaring associated gas at the wellhead, burning energy that could have been converted into electricity on site. Micro-turboexpanders and wellhead generator systems are changing this model by converting wellhead gas pressure into electricity at the pad. Sapphire Technologies' FreeSpin platform is specifically designed for this application, operating without a gearbox or lubrication system in a hermetically sealed housing that can be installed in-line with existing wellhead piping.

The regulatory push is now backed by law. According to the U.S. Environmental Protection Agency (EPA), the Biden-Harris Administration's 2024 Clean Air Act rules (OOOOb/c) require routine flaring of associated gas to be phased out by May 7, 2026. The rules also provide limited flexibility in compliance for operators in the Williston Basin, including the Bakken Formation and the Permian Basin. As operators face hard flaring deadlines, on-site power generation from wellhead gas using micro-turboexpanders becomes a compliance-backed alternative to grid connection or diesel supply.

Expanding Waste Heat Recovery Projects to Create Avenues for ORC Turboexpanders

The Organic Rankine Cycle (ORC) converts low- to medium-temperature heat into electricity using an organic working fluid with a low boiling point. The turboexpander or expander-generator is the core power-generating component of every ORC system. According to a recent report compiling publicly documented ORC installations worldwide, the technology has surpassed 2.7 gigawatts (GW) of installed capacity across 698 identified power plants globally. Waste heat recovery was identified as one of the most important and fast-growing application areas for the technology.

A peer-reviewed study published in the Journal of Engineering for Gas Turbines and Power (ASME, March 2026) confirmed that partial evaporation ORC systems with wet-to-dry expansion show an increase in power production of approximately 25% compared to the best single-phase cycle. It makes expander design optimization the primary lever for improving the economics of waste heat recovery installations. As governments tighten industrial emissions standards and energy efficiency mandates, ORC expander-generator systems are becoming the default technology for monetizing stranded thermal energy.

Category-wise Analysis

Product Type Insights

Radial flow turboexpanders are predicted to lead with a share of approximately 52.1% in 2026 as they deliver high efficiency across a wide operating range while maintaining a compact design. They can handle large pressure drops in a single stage, making them suitable for natural gas processing, LNG plants, helium recovery, and air separation units. Compared with axial designs, radial machines are less sensitive to changes in flow conditions and can continue operating efficiently even when plant loads fluctuate. This flexibility reduces energy losses and improves plant reliability.

Axial flow turboexpanders are estimated to be the fastest-growing segment over the forecast period, as they are better suited for very large gas volumes in high-capacity industrial plants. Their straight-through gas flow minimizes pressure losses and allows them to process significantly higher flow rates than radial machines. This makes them attractive for large air separation units, petrochemical complexes, and integrated gas processing facilities where continuous high-volume operation is essential.

Loading Device Insights

Compressor-loaded turboexpanders are anticipated to dominate with a share of nearly 42.4% in 2026, as they recover expansion energy and immediately reuse it inside the same process plant. Instead of allowing the turbine's energy to go to waste, the turboexpander drives a compressor mounted on the same shaft. This eliminates the need for a separate electric motor and lowers overall energy consumption. This configuration is valuable in natural gas processing, LNG production, and petrochemical plants, where compressed gas is constantly required.

Generator-loaded turboexpanders are expected to remain in the second position in 2026, as industries want to convert wasted pressure energy into electricity. Instead of driving a compressor, these systems are connected to an electrical generator, allowing excess expansion energy to produce power that can be used on-site or exported to the grid. Rising electricity prices and increasing sustainability targets are making this approach more attractive.

Regional Insights

Asia Pacific Turboexpander Market Trends

Asia Pacific is anticipated to be the leading region globally in 2026 with a share of nearly 37.2%, as it is building more LNG, industrial gas, and petrochemical facilities than any other region. China, India, South Korea, and Japan continue to invest heavily in natural gas infrastructure to improve energy security and support industrial growth. Turboexpanders are widely used in LNG liquefaction, natural gas processing, and air separation units, making them essential equipment for these projects.

The region also has the world's largest manufacturing base. Industries such as steel, chemicals, semiconductors, and electronics require large volumes of oxygen, nitrogen, and argon, all of which are produced using cryogenic air separation plants equipped with turboexpanders.

China Turboexpander Market Trends

China is projected to lead Asia Pacific in 2026, with a regional share of around 35.3%, as it expands both its LNG infrastructure and industrial gas production at an unprecedented pace. The country continues to build LNG receiving terminals, gas processing facilities, and large air separation plants to support chemical, steel, and semiconductor manufacturing, as well as clean energy projects. China is also investing heavily in hydrogen. According to the National Development and Reform Commission (NDRC) and the National Energy Administration (NEA), the country's Hydrogen Industry Development Plan (2021 to 2035) aims to establish a complete hydrogen supply chain.

India Turboexpander Market Trends

In 2026, India is projected to account for approximately 27.4% of the Asia Pacific market, as the country expands its natural gas network and industrial manufacturing base. The government is increasing city gas distribution coverage, constructing new LNG import terminals, and extending pipeline infrastructure to raise the share of natural gas in the country's energy mix.

These projects require turboexpanders for gas processing and cryogenic applications. India's industrial gas demand is also rising. New steel plants, semiconductor manufacturing projects, and electronics production facilities require oxygen and nitrogen supplied by air separation units.

Europe Turboexpander Market Trends

Europe is predicted to exhibit the fastest growth globally over the forecast period, with a share of nearly 30.1% in 2026, as the region continues to diversify its energy supply while improving industrial energy efficiency. Following the energy crisis, countries in the region have accelerated investments in LNG import terminals, gas infrastructure, and industrial decarbonization projects. These developments are creating new opportunities for turboexpanders in LNG regasification, gas processing, and automotive energy recovery systems.

Germany Turboexpander Market Trends

Germany will likely register an approximately 38.5% share in Europe in 2026, as it combines industrial strength with strict energy transition policies. The country has expanded LNG import infrastructure since 2022 to improve energy security. New LNG terminals and gas handling facilities require cryogenic equipment, including turboexpanders. Germany is also investing heavily in hydrogen. The German Federal Ministry for Economic Affairs and Energy (BMWK) continues to support hydrogen production, import terminals, and industrial decarbonization under its National Hydrogen Strategy.

U.K. Turboexpander Market Trends

The U.K. is projected to account for approximately 28.2% of the Europe turboexpander market in 2026, driven by continued investments in low-carbon energy projects and the modernization of industrial infrastructure. Carbon capture, hydrogen production, and energy recovery projects are creating new opportunities for turboexpander suppliers. The government's long-term decarbonization strategy is encouraging industries to adopt technologies that improve energy efficiency and reduce emissions.

The U.K. Government's Hydrogen Strategy supports large-scale hydrogen production and infrastructure development. Projects such as the HyNet North West and the East Coast Cluster are augmenting investments in hydrogen and carbon capture. These are propelling demand for cryogenic processing equipment.

North America Turboexpander Market Trends

North America is predicted to see steady growth in 2026, with a global share of approximately 22.4%, owing to continued investments in LNG exports, natural gas processing, and energy recovery technologies. The U.S. and Canada possess abundant natural gas resources, leading to ongoing construction and expansion of LNG export terminals and gas processing plants. Turboexpanders remain key equipment for these facilities. The region is also witnessing increasing adoption of pressure energy recovery systems. Instead of wasting pressure through conventional valves, utilities are installing generator-loaded turboexpanders to produce electricity.

U.S. Turboexpander Market Trends

The U.S. is projected to account for approximately 73.2% of the North American turboexpander market in 2026, supported by its position as one of the world's largest producers and exporters of natural gas, which is driving sustained investments in LNG production and gas processing infrastructure. New LNG export terminals, gas processing plants, and petrochemical facilities continue to create demand for turboexpanders. The country is also investing in helium recovery, hydrogen, and carbon capture projects, which require advanced cryogenic expansion technology.

The U.S. is also becoming a leading market for pressure energy recovery. Companies such as Sapphire Technologies are deploying in-line turboexpanders that convert natural gas pressure into electricity.

Competitive Landscape

The global turboexpander market is moderately consolidated with a limited number of multinational turbomachinery manufacturers dominating large LNG, natural gas processing, and industrial gas projects. Regional engineering firms and niche cryogenic equipment suppliers compete in specialized applications such as helium liquefaction and small-scale energy recovery. High entry barriers, including proprietary aerodynamic design expertise, make it difficult for new companies to compete in large-capacity projects.

Competition is centered on technology differentiation rather than pricing. Leading companies are investing in magnetic bearing systems, oil-free designs, digital condition monitoring, predictive maintenance software, and high-efficiency turbine blades to improve operational efficiency and reduce maintenance intervals. Manufacturers are also supplying integrated turbomachinery packages that combine turboexpanders with compressors, generators, and control systems, enabling customers to simplify procurement for LNG terminals, air separation units, and petrochemical plants.

Key Industry Developments:

- In November 2025, Baker Hughes signed an agreement to supply its turbomachinery portfolio, including main refrigerant compressors and power generation equipment incorporating turboexpander technology, for the Alaska LNG project. The project is expected to strengthen large-scale LNG infrastructure in North America while expanding Baker Hughes' presence in integrated cryogenic processing solutions.

- In October 2025, Baker Hughes shareholders approved the company's proposed acquisition of Chart Industries in a transaction valued at approximately US$13.6 billion, with closing expected in 2026 following regulatory approvals. The acquisition is intended to combine Baker Hughes' turbomachinery portfolio with Chart's cryogenic processing technologies, creating a broad portfolio for LNG, hydrogen, carbon capture, and industrial gas projects.

- In September 2025, Baker Hughes secured a contract from Fervo Energy to supply turboexpanders and related Organic Rankine Cycle (ORC) power generation equipment for five geothermal power plants at the Cape Station project in Utah. The project represents one of the largest deployments of turboexpander technology in geothermal energy recovery applications and supports the commercialization of enhanced geothermal systems.

Companies Covered in Turboexpander Market

- Atlas Copco AB

- Air Products Inc. (ROTOFLOW)

- Air Liquide (formerly Nikkiso Cryogenic Industries)

- Honeywell International Inc.

- Baker Hughes Company

- Chart Industries (L.A. Turbine)

- Linde Plc (Cryostar)

- R&D Dynamics Corporation

- Elliott Group (EBARA Corporation)

- Siemens Energy (Siemens AG)

- Man Energy

- PBS Group, a. s.

- Turbogaz

- Others

Frequently Asked Questions

The global turboexpander market is projected to be valued at US$1.2 billion in 2026.

The turboexpander market is expected to reach US$1.9 billion by 2033.

Key market trends include the development of hydrogen liquefaction turboexpanders and the adoption of magnetic bearing technology.

Radial flow turboexpanders are expected to be the leading product type with a share of nearly 52.1% in 2026, as they can efficiently handle large pressure drops in cryogenic applications.

The turboexpander market is expected to grow at a CAGR of 6.9% from 2026 to 2033.

Atlas Copco AB, Air Products Inc. (ROTOFLOW), and Air Liquide (formerly Nikkiso Cryogenic Industries) are a few key market players.