- Medical Devices

- Synoptophore Market

Synoptophore Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Synoptophore Market by Product (Manual Synoptophore and Automated Synoptophore), by Application (Diagnostic and Therapeutic) End-user (Hospitals, Ophthalmic Clinics, Trauma Centers, and Others), and Regional Analysis from 2026 - 2033

Key Industry Highlights

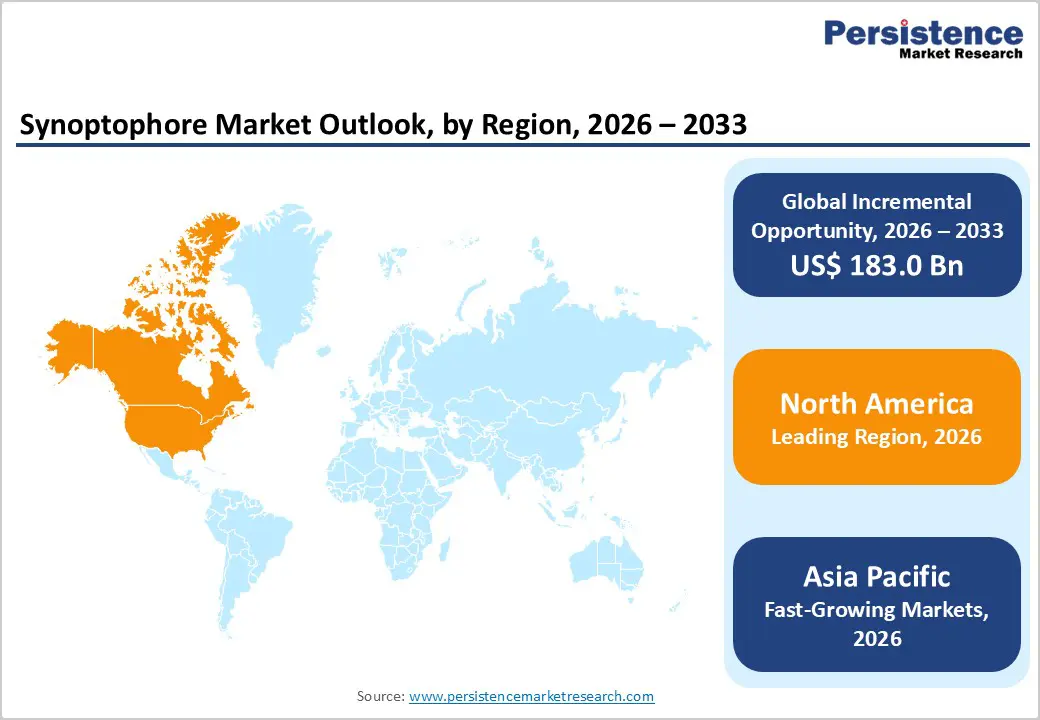

- Leading Region: North America holds 46.7% of the global market, supported by advanced healthcare systems, a strong presence of specialized eye care facilities, and continuous technological adoption in ophthalmology.

- Fastest-Growing Region: Asia Pacific is witnessing the fastest growth due to improving access to eye care services, rising awareness of early diagnosis, and expanding healthcare infrastructure.

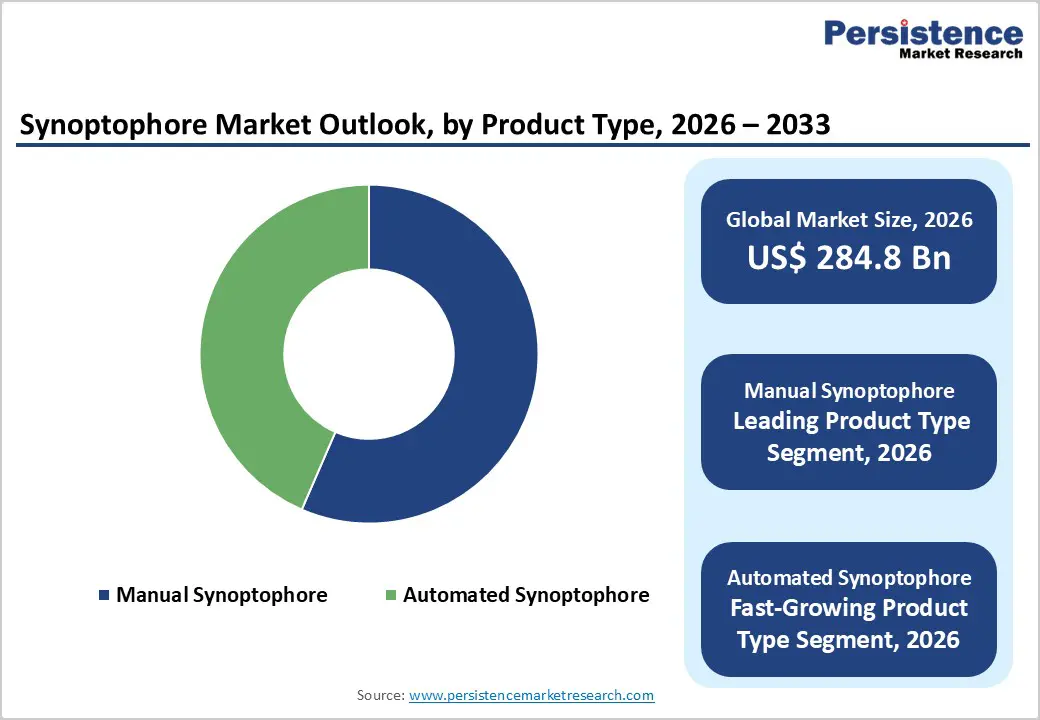

- Leading Product Segment: Manual synoptophore accounts for 42.6%, driven by their affordability, ease of operation, and widespread use in routine clinical evaluations.

- Fastest-Growing Product Segment: Automated synoptophores are gaining traction as healthcare providers shift toward digitally enhanced systems that improve diagnostic precision and workflow efficiency.

- Leading Application Segment: Diagnostic applications contribute 36.4% of the market, reflecting the high volume of clinical assessments for binocular vision disorders.

- Fastest-Growing Application Segment: Therapeutic applications are expanding steadily as vision therapy gains importance in managing ocular misalignment and improving binocular function.

| Key Insights | Details |

|---|---|

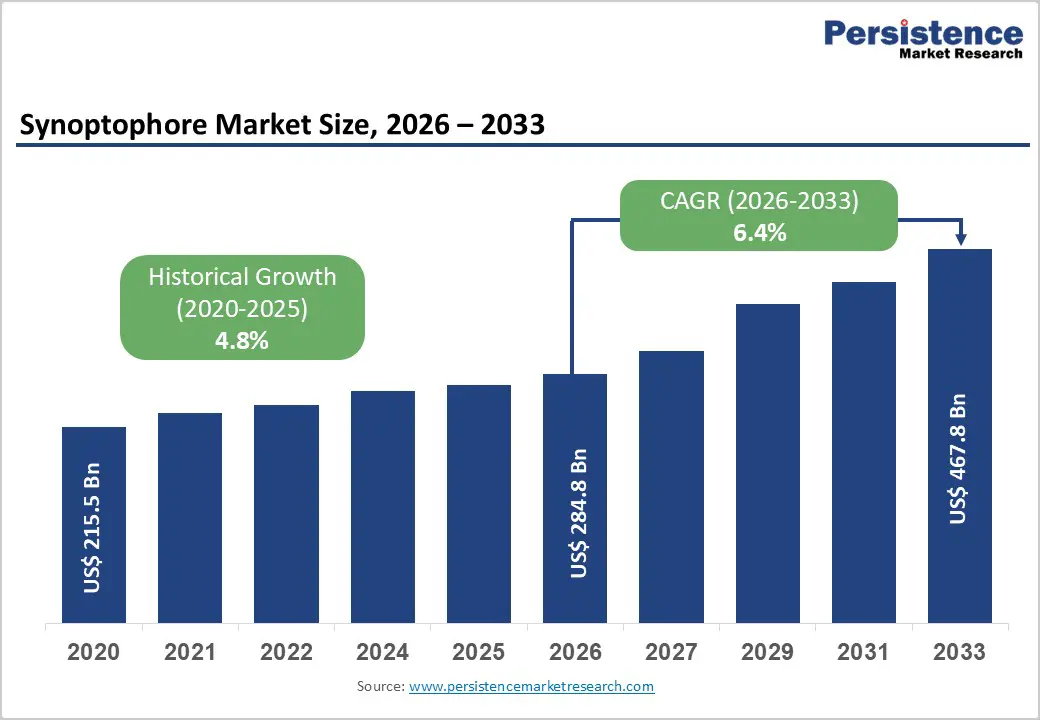

| Synoptophore Market Size (2026E) | US$ 284.8 Bn |

| Market Value Forecast (2033F) | US$ 467.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.8% |

DRO Analysis

Driver - Rising Prevalence of Strabismus and Increasing Focus on Early Vision Diagnosis

The growing incidence of binocular vision disorders, particularly strabismus and amblyopia, is significantly contributing to the demand for advanced ophthalmic diagnostic tools. These conditions are especially prevalent among pediatric populations, where early detection is critical to prevent long-term visual impairment. Synoptophores play a vital role in assessing ocular alignment, sensory fusion, and depth perception, making them indispensable in routine eye examinations. As awareness around childhood vision screening continues to increase, healthcare providers are placing greater emphasis on incorporating precise diagnostic instruments into clinical practice.

Additionally, the expansion of ophthalmology services globally is strengthening the adoption of such devices. Hospitals and specialized eye care centers are witnessing a steady rise in patient visits related to vision disorders, leading to increased utilization of diagnostic equipment. Technological improvements in synoptophores, including digital displays and enhanced measurement accuracy, are further improving clinical outcomes and workflow efficiency. Government-led initiatives promoting school-based vision screening programs and early intervention strategies are also accelerating demand. Furthermore, the increasing availability of trained ophthalmologists and optometrists, combined with rising healthcare expenditure, is supporting the integration of advanced diagnostic tools across both developed and emerging healthcare systems, reinforcing sustained market growth.

Restraints - High Equipment Costs and Availability of Alternative Diagnostic Methods\

One of the primary challenges limiting broader adoption is the relatively high cost associated with advanced and automated synoptophore systems. Smaller clinics, independent practitioners, and healthcare facilities in cost-sensitive regions often face budget constraints, which may restrict their ability to invest in sophisticated diagnostic equipment. In such cases, practitioners may rely on basic vision assessment tools or manual techniques that offer limited functionality compared to synoptophores. Additionally, maintenance requirements and periodic calibration needs can add to the overall operational expenses, further influencing purchasing decisions.

Moreover, the presence of alternative diagnostic technologies are restraining the market growth. Devices such as prism cover tests, autorefractors, and digital vision screening systems are widely used for preliminary assessment of ocular alignment and refractive errors. These alternatives, while not as comprehensive, can sometimes reduce reliance on synoptophores in routine clinical settings. Moreover, effective use of synoptophores requires trained professionals capable of interpreting results accurately and conducting detailed binocular vision assessments. In regions with limited access to skilled ophthalmic personnel, utilization rates may remain suboptimal. The combination of financial limitations, competing diagnostic approaches, and operational complexities may therefore moderate the pace of adoption across certain healthcare environments.

Opportunity - Expansion of Eye Care Infrastructure and Technological Advancements in Vision Therapy Devices

The continuous expansion of global eye care infrastructure presents significant growth opportunities for manufacturers of ophthalmic diagnostic equipment. Increasing investments by governments and private healthcare providers in establishing specialized eye hospitals, vision centers, and pediatric ophthalmology units are creating a strong foundation for market expansion. These facilities require advanced diagnostic tools capable of delivering precise and reliable assessments, positioning synoptophores as essential components of modern ophthalmic practice.

Emerging economies are particularly attractive markets due to improving healthcare accessibility and rising awareness regarding early diagnosis of vision disorders. Countries across Asia Pacific, Latin America, and the Middle East are actively strengthening their healthcare systems, leading to increased procurement of diagnostic instruments. In parallel, technological advancements are transforming traditional synoptophores into more sophisticated devices with digital interfaces, automated measurements, and enhanced patient interaction features. Integration with vision therapy programs and customized treatment protocols is further expanding their clinical applications beyond diagnosis. Additionally, the growing adoption of preventive healthcare practices and routine eye examinations is increasing the volume of patients requiring binocular vision assessment. These evolving trends, combined with continuous innovation in ophthalmic technologies, are expected to create substantial long-term opportunities for market participants.

Category-wise Analysis

By Product Insights

Manual synoptophore are projected to account for 56.5% of the global synoptophore market in 2026, positioning them as the dominant product category. Their strong adoption is primarily supported by affordability and ease of use across hospitals and eye care centers, particularly in developing regions. These devices enable clinicians to evaluate binocular vision, fusion, and ocular alignment with dependable accuracy. In addition, their simple mechanical design reduces maintenance requirements and ensures long-term usability. Despite the emergence of automated systems, manual synoptophores remain preferred in routine ophthalmic assessments due to their accessibility and clinical familiarity.

By Application Insights

Diagnostic applications are expected to hold 74.8% of the global synoptophore market in 2026, making them the largest segment. The widespread need for early detection of strabismus, amblyopia, and other binocular vision anomalies continues to drive demand. Synoptophores are extensively used in clinical examinations to assess ocular deviation angles, sensory fusion, and retinal correspondence. Increasing awareness regarding early eye disorder diagnosis, especially among pediatric populations, further strengthens this segment. As ophthalmic evaluations become more standardized globally, diagnostic usage remains the core application area.

By End-user Insights

Hospitals are anticipated to capture 52.6% of the global synoptophore market in 2026, establishing them as the leading end-user segment. Large patient inflow, availability of specialized ophthalmology departments, and access to trained professionals contribute to this dominance. Hospitals routinely handle complex vision disorders requiring detailed binocular assessment and therapeutic planning. Moreover, integration of advanced diagnostic equipment and growing investment in eye care services further support adoption. Increasing surgical procedures for strabismus correction and comprehensive eye examinations also reinforce the demand within hospital settings.

Regional Insights

North America Synoptophore Market Trends

North America is forecast to account for 46.7% of the global synoptophore market in 2026, maintaining its leadership position. The region benefits from a highly developed ophthalmic care ecosystem supported by advanced healthcare infrastructure and early adoption of innovative diagnostic technologies. Eye care facilities across the United States and Canada routinely utilize synoptophores for detailed binocular vision assessment, particularly in pediatric ophthalmology and strabismus management.

A strong presence of specialized eye hospitals, academic medical centers, and vision therapy clinics has significantly contributed to sustained demand. Additionally, increasing awareness regarding early diagnosis of visual disorders and routine eye screening programs has expanded the patient base requiring binocular vision evaluation. Favorable reimbursement policies and access to skilled ophthalmologists further encourage the use of advanced diagnostic tools. Continuous investments in healthcare technology and rising emphasis on precision diagnostics are also supporting the integration of digital and automated synoptophore systems. These combined factors continue to reinforce North America’s dominance in the global synoptophore market.

Europe Synoptophore Market Trends

Europe represents a mature yet steadily evolving synoptophore market, driven by strong healthcare systems and a well-established ophthalmology research landscape. Countries such as Germany, the United Kingdom, France, and Italy play a key role in supporting demand through advanced eye care services and widespread clinical adoption of diagnostic technologies. Synoptophores are commonly utilized in hospitals and specialized vision centers for evaluating binocular vision disorders and supporting treatment planning.

The region benefits from extensive collaboration between research institutions, healthcare providers, and medical device manufacturers, which contributes to continuous improvements in ophthalmic diagnostics. Additionally, a growing elderly population and increasing prevalence of vision-related conditions are driving the need for routine eye examinations. Regulatory frameworks focusing on clinical accuracy and patient safety further promote the use of reliable diagnostic equipment. Rising awareness about pediatric eye health and early intervention strategies is also expanding the application base. Collectively, these factors ensure consistent demand for synoptophores across Europe’s healthcare ecosystem.

Asia Pacific Synoptophore Market Trends

Asia Pacific is projected to be the fastest-growing regional market, expanding at a CAGR of approximately 7.4% between 2026 and 2033. Rapid improvements in healthcare infrastructure, combined with increasing access to ophthalmic services, are significantly driving demand for synoptophores across countries such as China, India, Japan, and South Korea. Growing population size and rising incidence of vision disorders, particularly among children, are creating substantial demand for early diagnostic tools.

Governments in the region are actively investing in healthcare modernization and expanding eye care programs, including school-based vision screening initiatives. This has led to increased adoption of diagnostic devices in both urban hospitals and emerging eye care centers. In addition, the expansion of private ophthalmology clinics and vision therapy centers is contributing to broader market penetration. Medical tourism, especially in countries like India and Thailand, is further supporting the demand for advanced ophthalmic diagnostics. The increasing availability of trained professionals and gradual shift toward technologically advanced equipment are positioning Asia Pacific as a rapidly expanding market for synoptophores.

Competitive Landscape

The global synoptophore market is highly competitive, with strong participation from Takagi Seiko Co., Ltd., Haag-Streit AG, Prakamya Visions Private Limited, 66 Vision Tech Co., Ltd., and Shanghai Link Instrument Co., Ltd.. These companies leverage extensive distribution networks, clinical training programs, and continuous innovation in binocular vision assessment systems and digital synoptophores to strengthen their market presence.

Growing demand for accurate diagnosis of strabismus and binocular vision disorders, increasing pediatric eye care focus, and expanding ophthalmology infrastructure are encouraging manufacturers to develop advanced synoptophores with improved ergonomics, digital interfaces, and enhanced diagnostic precision, supporting efficient vision assessment and therapy across hospitals and eye care centers worldwide.

Key Industry Developments:

- In December 2025, researchers from Massachusetts Institute of Technology demonstrated a new strategy for treating amblyopia in adults, highlighting the potential to expand treatment beyond early childhood and increasing the need for advanced diagnostic tools such as synoptophores to evaluate visual function and monitor therapeutic outcomes.

- In April 2025, Luminopia, Inc. received clearance from the U.S. Food & Drug Administration for its amblyopia treatment for children aged 8-12, expanding its indication and increasing the number of patients requiring diagnosis and monitoring of binocular vision disorders, thereby supporting demand for synoptophores in clinical assessment and treatment planning.

Companies Covered in Synoptophore Market

- Takagi Seiko Co., Ltd.

- Haag-Streit AG

- Prakamya Visions Private Limited

- 66 Vision Tech Co., Ltd.

- Shanghai Link Instrument Co., Ltd.

- Nanjing Redsun Optical Co., Ltd.

- Gem Optical Instruments Industries

- Appasamy Associates Private Limited

- Dahlgren Medicare Systems Private Limited

- Matronix India Corporation

- Sussex Vision International Ltd.

- Mei Medical Private Limited

- Unitech Vision

- Hesh Opto Lab Private Limited

- Others

Frequently Asked Questions

The global synoptophore market is projected to be valued at US$ 284.8 Bn in 2026.

Rising prevalence of strabismus & vision disorders, increasing pediatric eye care focus, and technological advancements in automated/digital synoptophores driving early diagnosis demand.

The global Synoptophore Market is poised to witness a CAGR of 6.4% between 2026 and 2033.

Growth opportunities lie in AI-integrated devices, portable/telehealth-enabled synoptophores, and expanding eye care infrastructure in emerging markets.

Takagi Seiko Co., Ltd., Haag-Streit AG, Prakamya Visions Private Limited, 66 Vision Tech Co., Ltd., and Shanghai Link Instrument Co., Ltd. are some of the key players in the synoptophore market.