- Automotive

- Skid Steer Loaders Market

Skid Steer Loaders Market Size, Share, and Growth Forecast 2026 - 2033

Skid Steer Loaders Market by Rated Operating Capacity (Up to 1,250 lbs, 1,251 to 2,200 lbs, More than 2,200 lbs), Application (Construction & Mining, Landscaping & Ground Maintenance, Agriculture, Others), Sales Channel (Direct Sales, Dealer Networks, Rental Companies, Online Sales), and Regional Analysis for 2026 - 2033

Skid Steer Loaders Market Size and Trend Analysis

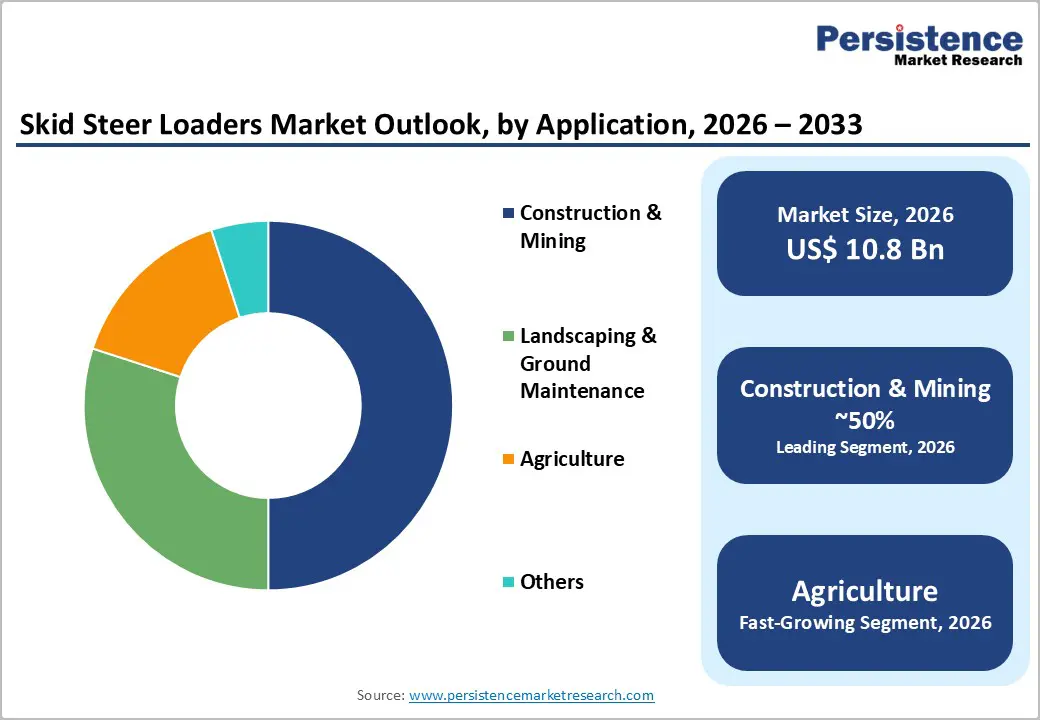

The global Skid Steer Loaders market is valued at approximately US$ 10.8 billion in 2026 and is projected to reach US$ 14.7 billion by 2033, growing at a CAGR of 4.6% between 2026 and 2033.

This steady expansion is anchored by the ongoing global construction boom, rapid urbanization in emerging economies, and the indispensable role of compact, multi-attachment loaders in infrastructure, agriculture, and landscaping applications. The U.S. Infrastructure Investment and Jobs Act (IIJA) has allocated US$ 1.2 trillion to infrastructure modernization, with US$ 568 billion disbursed to over 68,000 projects by November 2024, according to the White House, directly stimulating construction equipment procurement.

Key Industry Highlights:

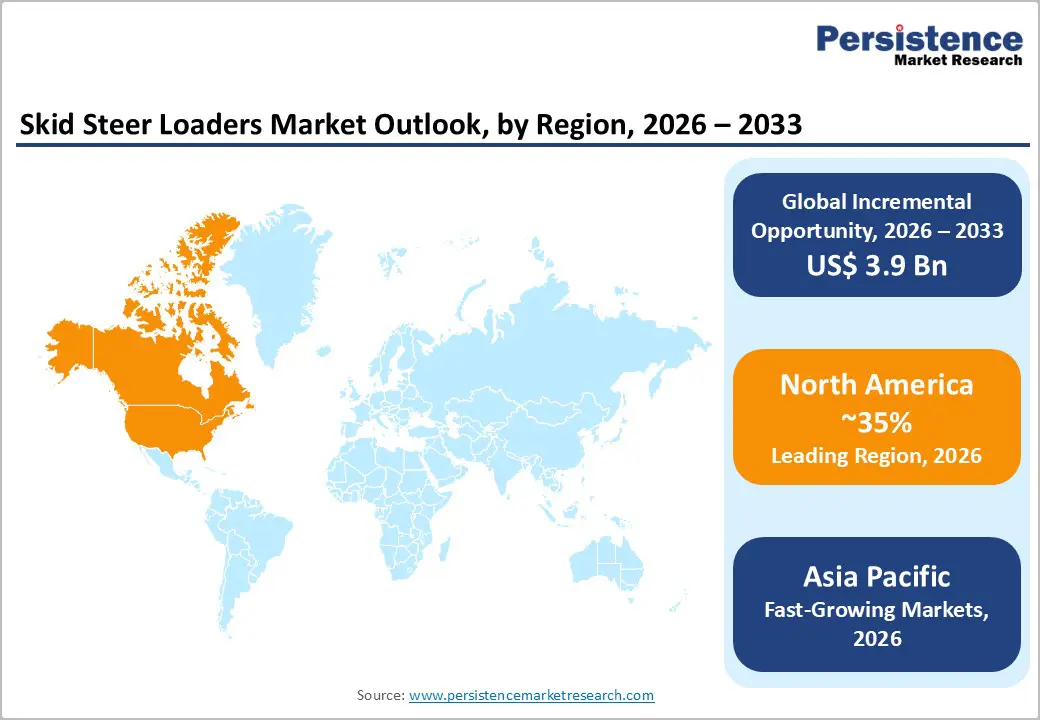

- Leading Region – North America leads the global Skid Steer Loaders market with approximately 85% revenue share, anchored by the U.S. IIJA's US$ 1.2 trillion infrastructure program, a large construction economy, and industry-leading OEMs including Bobcat, Caterpillar, and Deere & Company.

- Fastest-Growing Region – Asia Pacific is the fastest-growing region, driven by urbanization mega-projects in China and India, farm mechanization across Southeast Asia, and rising domestic manufacturing exemplified by CASE India's launch of its first made-in-India skid steer loader in June 2024.

- Dominant Rated Operating Capacity – The high-capacity segment leads with approximately 55% of revenue share, driven by demand from large-scale infrastructure, road-building, and mining projects that require maximum payload, breakout force, and hydraulic performance.

- Fastest-Growing Segment – Electric skid steer loaders are the fastest-growing technology segment, with Bobcat's S7X, Yuchai's S150, and GIANT's GS900E/GS950TE (launched January 2025) reflecting accelerating global OEM investment in zero-emission compact loaders for urban and emission-restricted applications.

- Key Opportunity – Rental companies are projected to command a rapidly growing share of skid steer procurement, with national operators such as Sunbelt Rentals deploying electric fleets and OEMs offering connected telematics for utilization-based rental models, unlocking recurring revenue streams.

| Key Insights | Details |

|---|---|

|

Skid Steer Loaders Market Size (2026E) |

US$ 10.8 Billion |

|

Market Value Forecast (2033F) |

US$ 14.7 Billion |

|

Projected Growth CAGR (2026–2033) |

4.6% |

|

Historical Market Growth (2020–2025) |

3.4% CAGR |

DRO Analysis

Drivers - Large-Scale Infrastructure Investment and Urban Construction Activity

A primary growth catalyst for the global Skid Steer Loaders market is the sustained surge in public and private infrastructure investment worldwide. In the United States, the Infrastructure Investment and Jobs Act (IIJA), a US$ 1.2 trillion bipartisan legislation, has funded over 68,000 infrastructure projects as of November 2024, covering roads, bridges, rail, ports, and urban redevelopment programs.

The U.S. Census Bureau reported a 14% year-on-year increase in total construction activity from December 2022 to December 2023, underscoring robust demand for compact construction equipment for on-site preparation, grading, and material-handling tasks. Skid steer loaders are preferred for their ability to navigate confined urban job sites and perform multiple functions with interchangeable attachments, reducing labor dependency and the need for multiple machines on a single project.

Rising Adoption of Electric and Autonomous Skid Steer Loaders

The rapid development and market entry of electric and autonomous skid steer loaders are reshaping the competitive and demand landscape, creating a powerful growth driver for OEMs and rental companies. Bobcat launched the world's first all-electric skid steer loader, the S7X, in January 2024, powered by a 60.5 kWh lithium-ion battery with up to 8 hours of run time per charge, featuring electric drive motors and ball screw actuators that replace hydraulic systems, reportedly reducing operating costs to approximately one-tenth of a comparable diesel machine.

Caterpillar released four next-generation skid steer models, the 250, 260, 270, and 270 XE in late 2024, featuring upgraded power, torque, enhanced hydraulics, and fully integrated Cat Smart Attachment compatibility. In March 2025, Bobcat launched nine new skid steer models at ConExpo, including updated Pro Series platforms with advanced camera- and radar-based object detection.

Restraints - High Initial Acquisition Costs and Budget Constraints for Small Contractors

The Skid Steer Loaders market faces a significant restraint in the high upfront cost of equipment, particularly for electric and hybrid models. While a conventional diesel skid steer can be purchased in the US$ 30,000–80,000 range, advanced all-electric models such as Bobcat's S7X are priced at approximately US$ 200,000, more than three times the cost of comparable diesel loaders, per Engineering News-Record.

Approximately 34% of small contractors delay new equipment purchases due to budget constraints, according to industry data. This cost barrier limits adoption among the large base of small and medium-sized contractors that constitute a substantial portion of end-use demand.

Stringent Emission Regulations and Diesel Engine Phase-Out Pressures

Tightening environmental regulations, particularly Stage V emission standards in the European Union and Tier 4 Final standards in the United States, are increasing compliance costs for diesel-powered skid steer loaders and constraining the operational flexibility of existing fleets. In Europe, Stage V regulations impose stringent particulate and NOx limits on off-road machinery below 56 kW, directly affecting mid-range skid steers.

While Bobcat's S650 Stage V-compliant model for European markets showcased at Hillhead 2024 demonstrates OEM responsiveness, the cost of compliance engineering raises prices and compresses margins, particularly for smaller manufacturers with limited R&D budgets.

Opportunities - Electric Skid Steer Loaders and Emission-Free Urban Job Site Applications

The electrification of skid steer loaders represents one of the most compelling growth opportunities in the global market, driven by tightening emissions mandates, expanding zero-emission zones in urban areas, and rapidly declining battery costs. The European Union's Stage V regulations and expanding Low Emission Zones (LEZs) in cities such as London, Amsterdam, Brussels, and Paris are creating a mandatory market for zero-emission compact construction equipment.

Bobcat's S7X, featuring zero on-site emissions, minimal vibration, and near-silent operation, is specifically positioned for indoor demolition, urban renovation, and environmentally sensitive job sites where diesel machines face operational restrictions. Yuchai Heavy Industry (China) launched several electric skid steer models in April 2024, including the S150, the largest-tonnage electric SSL available, demonstrating the breadth of manufacturer investment in this category.

Rental Market Expansion and Subscription-Based Equipment Access Models

The growth of the equipment rental sector represents a high-value opportunity for Skid Steer Loader market participants, driven by contractor preferences for flexible, cost-effective access to machinery without capital expenditure. Rental companies, including Sunbelt Rentals (the first national customer for Bobcat's T7X electric track loader) and United Rentals, are actively investing in skid steer fleets, particularly as new electric and connected models reduce maintenance liabilities.

Industry analysts note that rental companies are projected to command a significant share of the Skid Steer Loaders market over the forecast period, as small and mid-sized contractors in North America, Europe, and the Asia Pacific increasingly favour operating expense models over capital expenditure. The growing adoption of subscription-based and as-a-service equipment models enabled by connected telematics platforms such as Bobcat Machine IQ further supports utilization-based rental arrangements, creating new recurring revenue streams for OEMs and rental operators.

Category-wise Analysis

Rated Operating Capacity Insights

The More than 2,200 lbs rated operating capacity (ROC) segment leads the global Skid Steer Loaders market, accounting for approximately 55% of revenue in 2025. High-capacity skid steer loaders are essential for large-scale construction, road building, utility installation, and infrastructure excavation projects where handling heavy loads and operating in demanding terrain conditions is non-negotiable.

The global construction equipment market, valued at US$ 161.4 billion in 2024 per industry analysis, is driven by government and private sector infrastructure mega-projects that specifically require the payload and breakout force capabilities of high-ROC machines. Caterpillar's next-generation 270 and 270 XE offering, rated operating capacities exceeding 3,000 lbs and the highest hydraulic flow in their class at 40 gallons per minute, exemplify OEM investment in this dominant segment.

Application Insights

The Construction & Mining application segment is the undisputed leader in the global Skid Steer Loaders market, holding approximately 50% of revenue in 2025. Skid steer loaders are indispensable on construction sites for site preparation, grading, material handling, interior demolition, and utility trench work, thanks to their compact size, which allows effective operation in tight urban environments where full-size excavators and wheel loaders cannot access.

The U.S. Census Bureau confirmed a 14% year-on-year jump in total construction activity (December 2022 to December 2023), while the IIJA is funding over 68,000 projects through 2026, sustaining a robust construction equipment procurement pipeline. Landscaping & Ground Maintenance is the second-largest application, driven by the rapid expansion of smart-city greening programs and residential landscaping in North America and Europe.

Sales Channel Insights

The Dealer Networks sales channel leads the global Skid Steer Loaders market, accounting for approximately 52% of revenue in 2025. Authorized dealer networks provide buyers with access to pre-sales consultation, equipment demonstrations, financing options, after-sales service, and warranty support, all critical for high-value capital equipment purchases. Bobcat, Caterpillar, Deere & Company, and CNH Industrial all operate extensive global dealer networks that serve as the primary point of contact for end users, from large contractors to independent operators.

Caterpillar's dealer network spans over 160 countries, providing unmatched geographic reach for parts and service support. Rental Companies represent the second largest and fastest-growing channel, with national rental operators such as Sunbelt Rentals and United Rentals actively expanding their compact equipment fleets.

Regional Analysis

North America Skid Steer Loaders Market Share and Trends Analysis

North America leads the global Skid Steer Loaders market, commanding approximately 85% of global revenue in 2023 per industry data, underpinned by the United States' role as the world's largest construction economy and the birthplace of the skid steer loader itself. The Infrastructure Investment and Jobs Act (IIJA) has released US$ 568 billion to 68,000+ infrastructure projects by November 2024, covering highways, bridges, transit, water systems, and broadband all requiring compact equipment on site.

Canada contributes through steady residential and commercial building activity, particularly in major urban centers. The region's innovation ecosystem anchored by OEM R&D centers for Bobcat, Caterpillar, Deere & Company, and CNH Industrial, drives continuous technology advancement, including AI-based object detection, telematics platforms, and electrification.

Asia Pacific Skid Steer Loaders Market Share and Trends Analysis

Asia Pacific is the fastest-growing regional market for skid steer loaders, projected to expand at above-average CAGR through 2033, driven by large-scale urbanization, infrastructure mega-projects, and rapid farm mechanization across China, India, and Southeast Asia. China dominates the region both as the world's largest construction market and as a growing manufacturer of skid steer loaders, with domestic OEMs such as Yuchai Heavy Industry launching electric models, including the S150 in April 2024 the largest-tonnage electric SSL globally.

CASE India, a brand of CNH Industrial, launched its first indigenously manufactured SR130B Skid Steer Loader from its Pithampur, Madhya Pradesh facility in June 2024, marking a milestone in domestic production for the Indian market. Japan contributes approximately 6% of global skid steer loader revenue, supported by compact construction requirements in its densely built urban environment.

Europe Skid Steer Loaders Market Share and Trends Analysis

Europe is a mature but technologically progressive market for skid steer loaders, driven by stringent EU Stage V emission regulations, expanding Low Emission Zones (LEZs), and a construction sector focused on urban renewal and sustainable building. Germany's federal government is committed to building hundreds of thousands of new homes by 2025 under its Housing Construction Program, generating sustained demand for compact equipment on residential construction sites.

European OEMs and construction operators are particularly focused on electrification, with the EU's expanding zero-emission zones in cities driving procurement of electric and hybrid loaders. Wacker Neuson Group headquartered in Munich, Germany operates a fully electric compact equipment portfolio tailored for European markets. GIANT (Tobroco-Giant) of the Netherlands launched two fully electric skid steer models in January 2025, the GS900E and GS950TE, further demonstrating the region's early-adopter leadership in zero-emission construction equipment.

Competitive Landscape

The global Skid Steer Loaders market is moderately consolidated, with a handful of dominant OEMs, Bobcat, Caterpillar, and Deere & Company collectively holding the largest market share, particularly in North America. These leaders differentiate through comprehensive product portfolios spanning multiple ROC classes, proprietary attachment ecosystems, extensive dealer service networks, and integrated telematics platforms such as Bobcat Machine IQ and Cat App. Emerging business model trends include the shift toward rental and as-a-service fleet arrangements, cloud-connected machine health monitoring, and the commercialization of electric and autonomous platforms.

Key Developments:

- In March 2025, Bobcat launched nine new skid steer loader models at ConExpo 2025, including Pro Series platforms with camera- and radar-based object detection, 115 hp engines, and 12-foot lift height, setting a new performance benchmark in the compact loader segment.

- In April 2024, Bobcat unveiled its innovative electric telehandler concept at the INTERMAT 2024, showcasing a significant step towards sustainable machinery in the construction industry. The electric telehandler is designed to meet the growing demand for environmentally responsible equipment, such as the skid steer loader, without compromising power or efficiency.

Companies Covered in Skid Steer Loaders Market

- Bobcat

- Caterpillar Inc.

- Deere & Company

- CNH Industrial N.V.

- Komatsu Ltd.

- JCB Inc.

- Kubota Corporation

- Yanmar Co., Ltd.

- Volvo Construction Equipment

- Wacker Neuson Group

Frequently Asked Questions

The global Skid Steer Loaders market is estimated to be valued at US$ 10.8 Billion in 2026 and is projected to reach US$14.7 billion by 2033, registering a CAGR of 4.6% during the forecast period 2026-2033.

The primary demand drivers include the U.S. Infrastructure Investment and Jobs Act (IIJA) funding over 68,000 infrastructure projects worth US$ 568 billion by November 2024, rising urban construction activity confirmed by the U.S. Census Bureau's reported 14% YoY construction jump, expanding farm mechanization in Asia Pacific and Latin America, and rapid product innovation, particularly electric and autonomous loaders.

The More than 2,200 lbs rated operating capacity (ROC) segment leads the global Skid Steer Loaders market with approximately 55% revenue share in 2025. This segment's dominance is driven by large-scale infrastructure, road building, mining, and utility projects that require maximum payload capacity, superior breakout force, and high-flow hydraulics.

North America leads the global Skid Steer Loaders market with approximately 85% revenue share, anchored by the United States' role as the world's most active construction economy and largest skid steer market.

The leading companies in the global Skid Steer Loaders market include Bobcat (Doosan Bobcat), Caterpillar Inc., Deere & Company, CNH Industrial N.V. (CASE CE / New Holland), Komatsu Ltd., JCB Inc., Kubota Corporation, Yanmar Co., Ltd., Volvo Construction Equipment, and Wacker Neuson Group.