- Automation & Robotics

- Robotic Vision Market

Robotic Vision Market Size, Share, and Growth Forecast 2026 - 2033

Robotic Vision Market by Component (Hardware [Cameras, LED Lighting, Optics, Processors & Controllers, Frame Grabbers], Software), Technology (2D Vision, 3D Vision, Laser-based Vision, Structured Light Vision, Others [Time of Flight (ToF)]), Application (Welding & Soldering, Packaging & Palletizing, Material Handling, Assembling & Disassembling, Measurement and Inspection, Cutting, Pressing, and Deburring, Painting), Industry, and Regional Analysis for 2026 - 2033

Robotic Vision Market Size and Trend Analysis

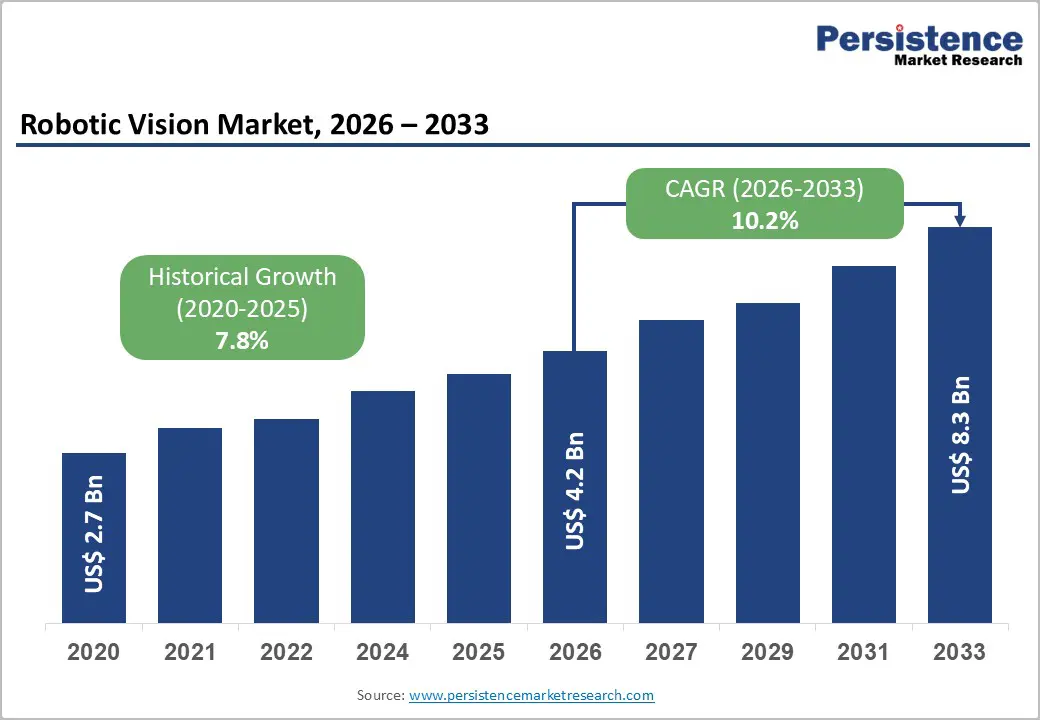

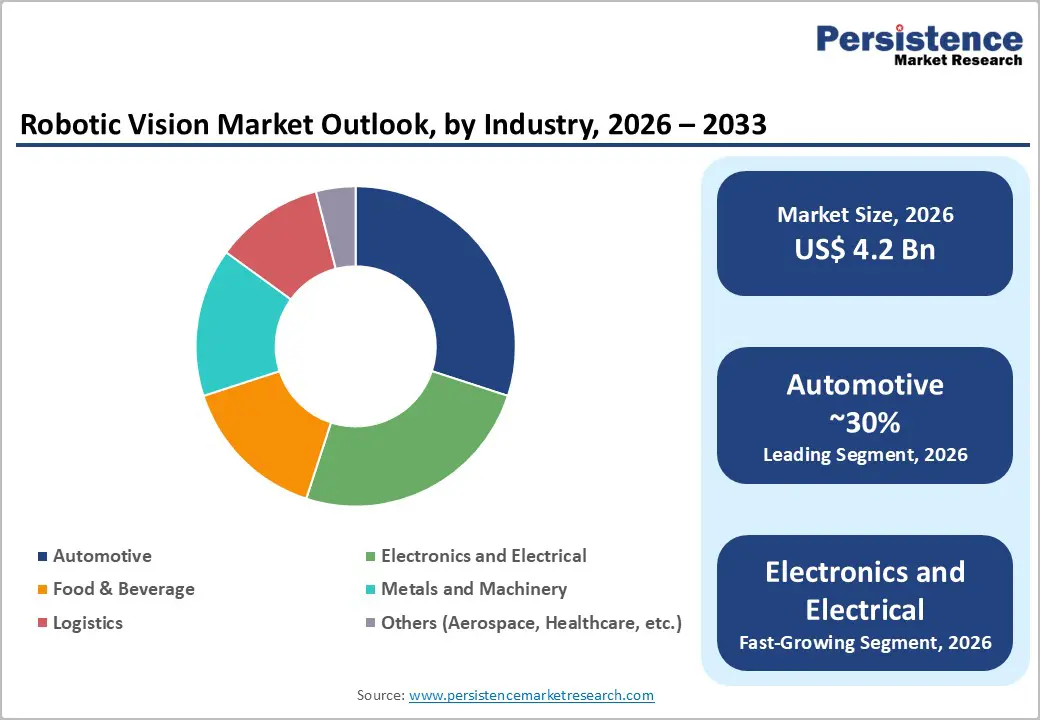

The global robotic vision market is valued at US$ 4.2 Bn in 2026 and is projected to reach US$ 8.3 Bn by 2033, growing at a CAGR of 10.2% between 2026 and 2033.

The robust expansion of this market is primarily propelled by the accelerating adoption of industrial automation frameworks, particularly Industry 4.0, across the automotive, electronics, and logistics sectors, which are increasingly integrating AI-powered vision systems to enhance production quality and operational throughput. Rising labor costs in developed economies, growing demand for zero-defect manufacturing, and widespread government-funded smart factory initiatives across North America, Europe, and the Asia Pacific are further reinforcing the structural shift toward vision-guided robotics at scale.

Key Industry Highlights:

- Leading Region - North America, led by the United States, is the dominant robotic vision region, supported by a mature industrial base, strong R&D ecosystems, and leadership from global companies such as Cognex Corporation, with the U.S. CHIPS and Science Act further stimulating manufacturing automation investment.

- Fastest Growing Region - Asia Pacific is the fastest-growing regional market for robotic vision, driven by China’s record industrial robot installations exceeding 290,000 units in 2022, Japan’s technological leadership, and India’s expanding manufacturing sector under the Production Linked Incentive (PLI) scheme.

- Dominant Segment - Hardware dominates the Component category with approximately 72% market share, driven by robust demand for industrial cameras, optics, LED lighting, and processor units across high-volume automotive and electronics manufacturing applications globally.

- Fastest Growing Segment - 3D Vision is the fastest-growing technology segment, outpacing the mature 2D Vision category as demand surges for advanced bin-picking, flexible assembly guidance, and complex volumetric inspection capabilities in logistics automation and precision manufacturing.

- Opportunity - Integration of robotic vision with surgical robotics and pharmaceutical automation represents a high-margin opportunity, with regulatory approvals via the U.S. FDA and European CE pathways expanding the addressable market for precision vision components in healthcare applications.

| Key Insights | Details |

|---|---|

| Robotic Vision Market Size (2026E) | US$ 4.2 Bn |

| Market Value Forecast (2033F) | US$ 8.3 Bn |

| Projected Growth CAGR (2026 - 2033) | 10.2% |

| Historical Market Growth (2020 - 2025) | 7.8% |

DRO Analysis

Market Growth Drivers

Accelerating Industrial Automation and Industry 4.0 Deployment

The global push toward smart manufacturing stands as the primary structural engine driving robotic vision adoption. According to the International Federation of Robotics (IFR), global industrial robot installations reached a record 553,052 units in 2022, with subsequent years maintaining upward momentum.

The IFR’s World Robotics 2023 report highlights that Asia, Europe, and the Americas collectively accounted for most new installations. Robotic vision systems are integral to enabling robots to execute precision tasks, including quality inspection, bin-picking, and precision assembly with minimal human intervention. Active government investment programs in Germany, South Korea, Japan, and the United States are continuously pushing manufacturers to deploy vision-guided automation at an industrial scale, creating sustained long-term demand across diverse end-use sectors.

Integration of Artificial Intelligence and Deep Learning in Machine Vision

AI-powered machine vision is fundamentally transforming the performance ceiling of robotic systems. Deep learning algorithms now enable vision systems to detect complex surface defects, identify objects in unstructured environments, and adapt to new product variants without manual reprogramming. NVIDIA Corporation’s Jetson edge AI platforms and similar embedded computing innovations have brought GPU-accelerated inference directly to factory floors, significantly improving real-time processing speed and detection accuracy.

The convergence of AI with 3D vision and structured light technologies is unlocking new high-value applications in flexible manufacturing and logistics. The European Machine Vision Association (EMVA) has documented accelerating AI-enabled deployments in electronics inspection and pharmaceutical packaging, confirming a decisive shift from rule-based to learning-based vision architectures that drives both adoption velocity and average selling price appreciation across the market.

Restraints - High Capital Investment and Complex System Integration

Despite strong demand fundamentals, the high upfront cost of robotic vision systems remains a significant barrier to adoption, particularly for small and medium-sized enterprises (SMEs). A fully configured machine vision deployment encompassing cameras, optics, LED lighting, frame grabbers, processors, and integration services can range from tens of thousands to several hundred thousand dollars per line.

According to the European Commission’s SME Performance Review, a substantial proportion of European manufacturers cite capital expenditure constraints as a primary obstacle to automation investment. Complex integration with legacy manufacturing infrastructure, the need for custom calibration, and reliance on high-cost specialized integrators further inflate the total cost of ownership, slowing penetration in price-sensitive industries and geographies.

Shortage of Skilled Vision System Engineers and Technicians

The deployment and maintenance of advanced robotic vision systems demand expertise spanning optics, software engineering, robotics, and artificial intelligence, a multidisciplinary skill set that remains in critically short supply globally. The World Economic Forum’s Future of Jobs Report 2023 identifies automation-related technical roles among the hardest to fill across major manufacturing economies.

This talent gap results in extended deployment timelines, heightened dependence on expensive external integrators, and the risk of systematic underutilization of deployed systems. In rapidly industrializing economies with fast-expanding manufacturing bases, the skills deficit is especially acute, materially constraining the pace at which robotic vision technology can be effectively absorbed into production operations.

Opportunities - Rapid Expansion of 3D Vision in Logistics and E-commerce Fulfillment

The explosive growth of e-commerce globally has created urgent and sustained demand for flexible, high-speed robotic vision in warehouse and fulfillment operations. 3D vision systems capable of managing unstructured bin-picking, multi-SKU sortation, and variable packaging formats are emerging as critical enablers of automated logistics. Amazon Robotics, Ocado Group, and major third-party logistics providers are actively investing in AI-guided robotic vision for order fulfillment.

The International Warehouse Logistics Association (IWLA) has documented sharp growth in fulfillment automation investments since 2020, driven by acute labor shortages and escalating consumer expectations for same-day and next-day delivery. The integration of Time-of-Flight (ToF) and structured light 3D vision with collaborative robots (cobots) creates a significant product differentiation opportunity for vision system vendors targeting the rapidly scaling logistics automation segment worldwide.

Healthcare Robotics and Surgical Vision Systems

The intersection of robotic vision and healthcare robotics represents one of the fastest-emerging application frontiers. Surgical robots, laboratory automation platforms, and pharmaceutical dispensing systems all rely on high-precision vision for task execution and patient safety. The global surgical robotics market was valued at approximately US$ 6.0 Bn in 2023, according to Intuitive Surgical’s annual report, and this growth trajectory is driving substantial demand for miniaturized, high-resolution vision components.

Intuitive Surgical’s da Vinci system and Stryker Corporation’s Mako robotic platform exemplify the critical role of vision in surgical navigation and orthopedic precision. Regulatory approvals for AI-assisted robotic surgery via the U.S. Food and Drug Administration (FDA) and European CE pathways are systematically expanding the addressable markets, offering vision hardware and software vendors a compelling, high-margin vertical opportunity.

Category-wise Analysis

Component Insights

Hardware is the dominant segment within the component category, accounting for approximately 72% of total robotic vision market revenue. This commanding leadership reflects the fundamentally hardware-intensive architecture of robotic vision deployments, wherein cameras, optics, LED lighting modules, frame grabbers, and processors & controllers collectively represent the bulk of system cost and functional capability.

The proliferation of high-resolution industrial cameras manufactured by Basler AG, Teledyne DALSA, and Sony Semiconductor Solutions Corporation underscores robust demand for high-fidelity image acquisition hardware. The European Machine Vision Association (EMVA) has consistently documented that global machine vision camera revenues outpace software revenues in aggregate value. As sensor resolution, frame rates, and multi-spectral imaging capabilities advance, hardware’s per-deployment value contribution is expected to remain the dominant revenue driver throughout the forecast period.

Technology Insights

2D Vision retains the leading position in the Technology category, commanding approximately 45% of total market share. Its dominance is rooted in proven cost-effectiveness, technological maturity, and suitability for a wide range of industrial tasks including barcode reading, label verification, surface defect detection, and dimensional gauging across automotive, electronics, and food & beverage sectors.

Cognex Corporation, the global market leader in 2D machine vision, reported revenues exceeding US$ 900 Mn in recent fiscal years, underscoring the scale of installed 2D vision infrastructure worldwide. However, 3D Vision is the fastest-growing technology segment, driven by rising demand in robotic bin-picking, flexible assembly guidance, and volumetric inspection applications where three-dimensional spatial data is indispensable for system accuracy and reliability.

Application Insights

Measurement and inspection is the leading application segment, representing approximately 30% of total robotic vision market revenue. This primacy is anchored in the non-negotiable quality assurance requirements of automotive, semiconductor, and electronics manufacturing, where component tolerances are measured in microns. Vision-based inspection eliminates subjectivity and fatigue inherent in manual quality control, delivering consistent, high-speed defect detection at scale.

The semiconductor industry’s transition to advanced node fabrication below 5nm and the automotive sector’s commitment to zero-defect manufacturing under ISO/TS 16949 quality standards have been particularly powerful demand drivers. Regulatory requirements for end-to-end traceability in the pharmaceutical and food & beverage sectors further amplify demand for automated inspection, reinforcing this segment’s market-leading position through the forecast horizon.

Industry Insights

The automotive sector is the dominant industry vertical, accounting for approximately 28% of the global robotic vision market revenue. Automakers and their Tier 1 and Tier 2 suppliers deploy machine vision comprehensively across the vehicle production lifecycle, from body-in-white welding verification and powertrain assembly inspection to final surface quality audits and paint defect detection.

The accelerating transition to electric vehicles (EVs) has introduced new vision-intensive processes, including battery cell inspection, electrode alignment verification, and EV module assembly validation. According to the IFR, the automotive industry remains the largest single global end-user of industrial robots, with China, Germany, Japan, South Korea, and the United States representing the top automotive robot markets, all of which simultaneously serve as major robotic vision deployment hubs.

Regional Analysis

North America

The United States leads North American robotic vision adoption, underpinned by a mature manufacturing ecosystem, robust venture capital investment in automation startups, and a strong regulatory framework that actively supports industrial innovation. The U.S. National Institute of Standards and Technology (NIST) has played a pivotal role in establishing machine vision performance standards, while programs under the U.S. Department of Commerce’s Advanced Manufacturing National Program Office fund domestic vision technology research and development.

Canada contributes meaningfully through advanced robotics research at institutions such as the University of Waterloo and the University of Toronto, which have yielded several machine vision technology spin-offs. The Automate 2024 trade exhibition in Detroit, Michigan, highlighted intensifying North American demand for AI-enabled robotic vision across automotive, logistics, and food processing verticals.

Asia Pacific

Asia Pacific is the fastest-growing region for robotic vision globally, with China, Japan, and South Korea representing its dominant markets. China’s “Made in China 2025” initiative and subsequent industrial policy frameworks have catalysed massive government-backed investment in automation and smart manufacturing, propelling machine vision demand across electronics, EV battery, and consumer goods production sectors.

Japan remains a global centre of technological excellence in robotic vision, with FANUC Corporation, Keyence Corporation, and Omron Corporation holding significant worldwide market positions. India is rapidly emerging as a high-growth market, supported by the government’s Production Linked Incentive (PLI) scheme and expanding electronics and automotive manufacturing sectors. ASEAN nations, particularly Vietnam, Thailand, and Malaysia, are attracting substantial foreign direct investment in electronics contract manufacturing, generating greenfield opportunities for robotic vision system integration at scale.

Europe

Germany remains the cornerstone of European robotic vision demand, underpinned by its globally dominant automotive OEM and industrial machinery manufacturing base. Companies such as Sick AG (headquartered in Waldkirch, Germany) and Basler AG (Ahrensburg, Germany) serve as global leaders in industrial vision hardware, anchoring European technology innovation. Germany’s “Platform Industrie 4.0” initiative a flagship government-industry collaboration continues to accelerate smart factory deployments, directly stimulating vision system investments.

The United Kingdom and France are expanding robotic vision deployments in aerospace manufacturing and pharmaceutical production, supported by national AI investment strategies and EU Horizon Europe research funding. Spain is witnessing growing machine vision adoption in automotive assembly plants operated by Stellantis and Volkswagen Group. Compliance requirements under the EU AI Act for automated decision-making systems in manufacturing are expected to further standardize and accelerate vision system deployments across the European bloc, presenting regulatory-driven growth tailwinds for established suppliers.

Competitive Landscape

The global robotic vision market is moderately consolidated at the technology and hardware component level but remains fragmented in system integration and application-specific solutions.

Key players, including Cognex Corporation, Keyence Corporation, FANUC Corporation, ABB Group, and Sick AG, command significant revenue shares through sustained R&D investment, proprietary algorithm libraries, and extensive global distribution networks. Strategic M&A activity, such as Teledyne Technologies’ acquisition of FLIR Systems in 2021 for approximately US$ 8.0 Bn, illustrates an industry trend toward portfolio expansion through consolidation.

Key Market Developments

- In March 2025, Keyence Corporation announced the launch of a vision sensor with built-in AI. It automates part detection, position verification, and counting under challenging conditions, surpassing the capabilities of traditional vision sensors.

- In January 2025, Cognex Corporation launched its In-Sight L38 line-scan vision system, targeting high-speed web inspection and continuous material processing in the electronics and packaging sectors, offering enhanced defect-detection speeds for demanding production environments.

Companies Covered in Robotic Vision Market

- Cognex Corporation

- Keyence Corporation

- FANUC Corporation

- ABB Group

- Sick AG

- Teledyne DALSA

- Omron Corporation

- Basler AG

- Hexagon AB

- Qualcomm Technologies, Inc.

- Yaskawa Electric Corporation

Frequently Asked Questions

The global Robotic Vision market is valued at US$ 4.2 Bn in 2026 and is projected to reach US$ 8.3 Bn by 2033, expanding at a compound annual growth rate (CAGR) of 10.2% during the forecast period 2026 - 2033.

The primary demand drivers include the rapid global adoption of Industry 4.0 and smart manufacturing practices, the integration of AI and deep learning algorithms into machine vision platforms, rising deployment in automotive and electronics manufacturing, and acute labor cost pressures compelling manufacturers in developed economies to accelerate automation investments.

2D Vision is the dominant technology segment, commanding approximately 45% of total market share. Its leadership is attributable to proven cost-effectiveness, broad industrial applicability in inspection and identification tasks, and a large installed base across automotive, electronics, and food & beverage manufacturing sectors worldwide.

North America, and specifically the United States, leads the global robotic vision market, supported by advanced manufacturing infrastructure, a strong innovation ecosystem underpinned by institutions such as the U.S. National Institute of Standards and Technology (NIST), and the presence of global market leaders including Cognex Corporation.

The leading companies in the global Robotic Vision market include Cognex Corporation, Keyence Corporation, FANUC Corporation, ABB Group, Sick AG, Teledyne DALSA, Omron Corporation, Basler AG, Hexagon AB, Qualcomm Technologies, Inc., and Yaskawa Electric Corporation, among other prominent regional and niche players.