- Executive Summary

- Global Regenerated Catalyst Market Snapshot, 2025 and 2033

- Market Opportunity Assessment, 2025 - 2033, US$ Bn

- Key Market Trends

- Future Market Projections

- Premium Market Insights

- Industry Developments and Key Market Events

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definition

- Market Dynamics

- Drivers

- Restraints

- Opportunity

- Key Trends

- Macro-economic Factors

- Global Sectoral Outlook

- Global GDP Growth Outlook

- COVID-19 Impact Analysis

- Forecast Factors - Relevance and Impact

- Value Added Insights

- Tool Adoption Analysis

- Regulatory Landscape

- Value Chain Analysis

- PESTLE Analysis

- Porter’s Five Force Analysis

- Price Analysis, 2025A

- Key Highlights

- Key Factors Impacting Deployment Costs

- Pricing Analysis, By Catalyst Type

- Global Regenerated Catalyst Market Outlook

- Key Highlights

- Market Volume (Units) Projections

- Market Size (US$ Bn) and Y-o-Y Growth

- Absolute $ Opportunity

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast

- Historical Market Size (US$ Bn) Analysis, 2025-2025

- Market Size (US$ Bn) Analysis and Forecast, 2025 - 2033

- Global Regenerated Catalyst Market Outlook: Catalyst Type

- Introduction / Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis, By Catalyst Type, 2025 - 2025

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Catalyst Type, 2025 - 2033

- Hydroprocessing

- Fluid Catalytic Cracking (FCC)

- Reforming

- Isomerization

- Alkylation

- Environmental Catalysts

- Market Attractiveness Analysis: Catalyst Type

- Global Regenerated Catalyst Market Outlook: Method

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By Method, 2025 - 2025

- Market Size (US$ Bn) Analysis and Forecast, By Method, 2025 - 2033

- Ex-situ

- In-situ

- Continuous Catalyst Regeneration (CCR)

- Advanced Methods

- Market Attractiveness Analysis: Method

- Global Regenerated Catalyst Market Outlook: Application

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By Application, 2025 - 2025

- Market Size (US$ Bn) Analysis and Forecast, By Application, 2025 - 2033

- Petroleum Refining

- Petrochemicals

- Chemical Processing

- Environmental

- Circular Economy

- Market Attractiveness Analysis: Application

- Key Highlights

- Global Regenerated Catalyst Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) and Volume (Units) Analysis, By Region, 2025 - 2025

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Region, 2025 - 2033

- North America

- Europe

- East Asia

- South Asia and Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Regenerated Catalyst Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2025 - 2025

- By Country

- By Catalyst Type

- By Method

- By Application

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 - 2033

- U.S.

- Canada

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Catalyst Type, 2025 - 2033

- Hydroprocessing

- Fluid Catalytic Cracking (FCC)

- Reforming

- Isomerization

- Alkylation

- Environmental Catalysts

- Market Size (US$ Bn) Analysis and Forecast, By Method, 2025 - 2033

- Ex-situ

- In-situ

- Continuous Catalyst Regeneration (CCR)

- Advanced Methods

- Market Size (US$ Bn) Analysis and Forecast, By Application, 2025-2033

- Petroleum Refining

- Petrochemicals

- Chemical Processing

- Environmental

- Circular Economy

- Market Attractiveness Analysis

- Europe Regenerated Catalyst Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2025 - 2025

- By Country

- By Catalyst Type

- By Method

- Application

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 - 2033

- Germany

- France

- U.K.

- Italy

- Spain

- Russia

- Türkiye

- Rest of Europe

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Catalyst Type, 2025 - 2033

- Hydroprocessing

- Fluid Catalytic Cracking (FCC)

- Reforming

- Isomerization

- Alkylation

- Environmental Catalysts

- Market Size (US$ Bn) Analysis and Forecast, By Method, 2025 - 2033

- Ex-situ

- In-situ

- Continuous Catalyst Regeneration (CCR)

- Advanced Methods

- Market Size (US$ Bn) Analysis and Forecast, By Application, 2025-2033

- Petroleum Refining

- Petrochemicals

- Chemical Processing

- Environmental

- Circular Economy

- Market Attractiveness Analysis

- East Asia Regenerated Catalyst Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2025 - 2025

- By Country

- By Catalyst Type

- By Method

- By Application

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 - 2033

- China

- Japan

- South Korea

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Catalyst Type, 2025 - 2033

- Complete Dentures

- Partial Dentures

- Overdentures

- Market Size (US$ Bn) Analysis and Forecast, By Method, 2025 - 2033

- Ex-situ

- In-situ

- Continuous Catalyst Regeneration (CCR)

- Advanced Methods

- Market Size (US$ Bn) Analysis and Forecast, By Application, 2025-2033

- Petroleum Refining

- Petrochemicals

- Chemical Processing

- Environmental

- Circular Economy

- Market Attractiveness Analysis

- South Asia & Oceania Regenerated Catalyst Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2025 - 2025

- By Country

- By Catalyst Type

- By Method

- By Application

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 - 2033

- India

- Southeast Asia

- ANZ

- Rest of South Asia & Oceania

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Catalyst Type, 2025 - 2033

- Hydroprocessing

- Fluid Catalytic Cracking (FCC)

- Reforming

- Isomerization

- Alkylation

- Environmental Catalysts

- Market Size (US$ Bn) Analysis and Forecast, By Method, 2025 - 2033

- Ex-situ

- In-situ

- Continuous Catalyst Regeneration (CCR)

- Advanced Methods

- Market Size (US$ Bn) Analysis and Forecast, By Application, 2025-2033

- Petroleum Refining

- Petrochemicals

- Chemical Processing

- Environmental

- Circular Economy

- Market Attractiveness Analysis

- Latin America Regenerated Catalyst Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2025 - 2025

- By Country

- By Catalyst Type

- By Method

- By Application

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 - 2033

- Brazil

- Mexico

- Rest of Latin America

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Catalyst Type, 2025 - 2033

- Hydroprocessing

- Fluid Catalytic Cracking (FCC)

- Reforming

- Isomerization

- Alkylation

- Environmental Catalysts

- Market Size (US$ Bn) Analysis and Forecast, By Method, 2025 - 2033

- Ex-situ

- In-situ

- Continuous Catalyst Regeneration (CCR)

- Advanced Methods

- Market Size (US$ Bn) Analysis and Forecast, By Application, 2025-2033

- Petroleum Refining

- Petrochemicals

- Chemical Processing

- Environmental

- Circular Economy

- Market Attractiveness Analysis

- Middle East & Africa Regenerated Catalyst Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2025 - 2025

- By Country

- By Catalyst Type

- By Method

- By Application

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 - 2033

- GCC Countries

- Egypt

- South Africa

- Northern Africa

- Rest of Middle East & Africa

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Catalyst Type, 2025 - 2033

- Hydroprocessing

- Fluid Catalytic Cracking (FCC)

- Reforming

- Isomerization

- Alkylation

- Environmental Catalysts

- Market Size (US$ Bn) Analysis and Forecast, By Method, 2025 - 2033

- Ex-situ

- In-situ

- Continuous Catalyst Regeneration (CCR)

- Advanced Methods

- Market Size (US$ Bn) Analysis and Forecast, By Application, 2025-2033

- Petroleum Refining

- Petrochemicals

- Chemical Processing

- Environmental

- Circular Economy

- Market Attractiveness Analysis

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping By Market

- Competition Dashboard

- Company Profiles (Details - Overview, Financials, Strategy, Recent Developments)

- BASF SE

- Overview

- Segments and Deployments

- Key Financials

- Market Developments

- Market Strategy

- Albemarle Corporation

- Honeywell UOP

- W.R. Grace & Co.

- Johnson Matthey

- Axens

- Clariant AG

- Haldor Topsoe

- Veolia

- Eurecat

- Porocel

- JGC C&C

- Sinopec Catalyst Co.

- BASF SE

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Specialty & Fine Chemicals

- Regenerated Catalyst Market

Regenerated Catalyst Market Size, Share, and Growth Forecast, 2026 - 2033

Regenerated Catalyst Market by Catalyst Type (Hydroprocessing, FCC, Reforming, Isomerization, Alkylation, Environmental), Method (Ex-situ, In-situ, CCR, Advanced Methods), Application (Petroleum Refining, Petrochemicals, Chemical Processing, Environmental, Circular Economy), and Regional Analysis for 2026 - 2033

Key Industry Highlights

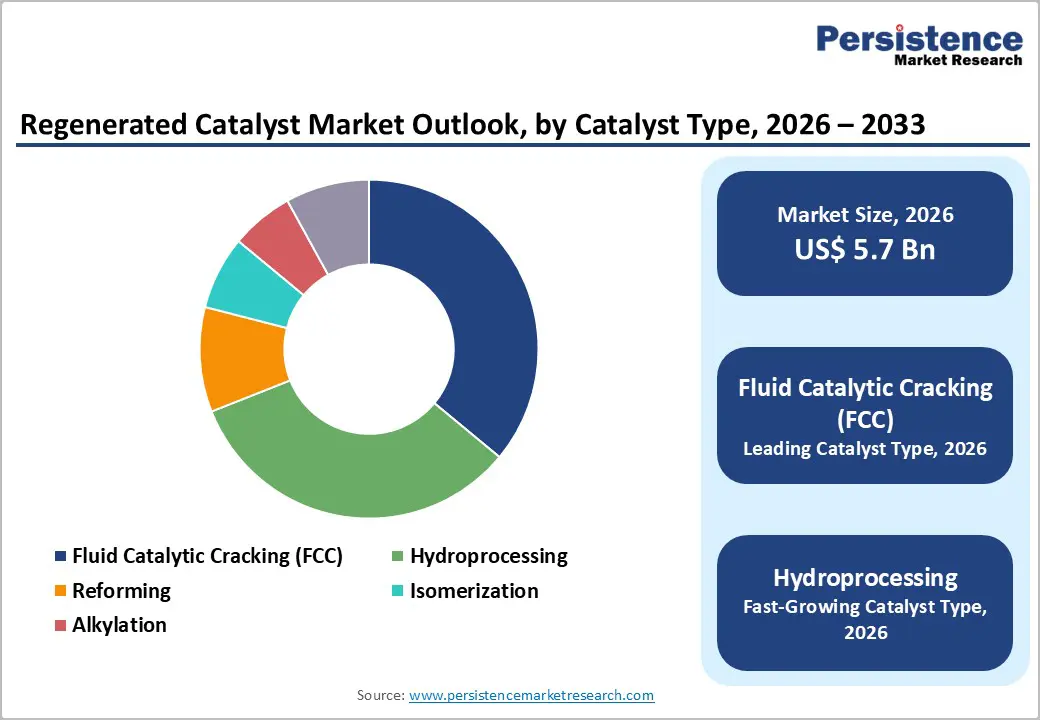

- Dominant Catalyst Types: Fluid catalytic cracking (FCC) catalysts are set to command around 36% revenue share in 2026, while hydroprocessing catalysts are likely to be the fastest-growing at 5.8% CAGR through 2033, driven by tightening low-sulfur fuel regulations.

- Leading Regeneration Methods: Ex-situ regeneration is expected to lead with an estimated 45% share in 2026, while CCR is projected to be the fastest-growing method, supported by its ability to enhance operational efficiency and reduce downtime.

- Dominant Applications: Petroleum refining is anticipated to dominate with over 50% share in 2026, while environmental applications are projected to be the fastest-growing through 2033, driven by emission control mandates and sustainability initiatives.

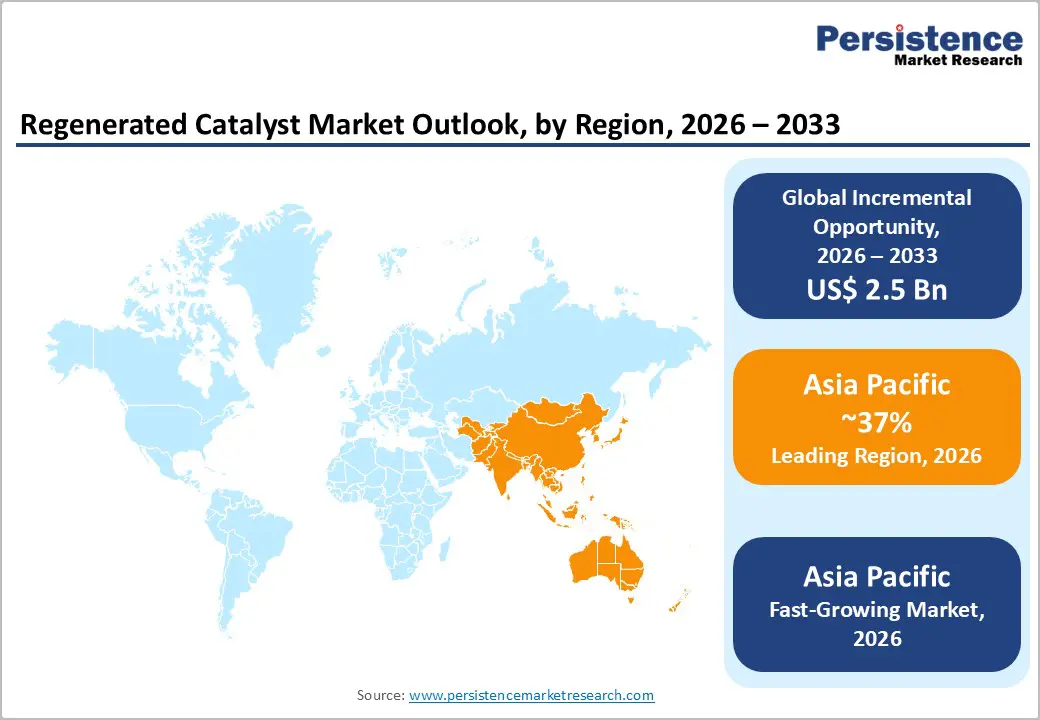

- Regional Leadership: Asia Pacific is poised to dominate with an estimated 37% share in 2026, driven by refining capacity expansions and industrial growth in China, India, and ASEAN.

- Prospective Opportunities: Technological advancements, including CCR and advanced regeneration methods, along with growing circular economy initiatives, are expected to shape long-term market opportunities and drive innovation across the value chain.

| Key Insights | Details |

|---|---|

|

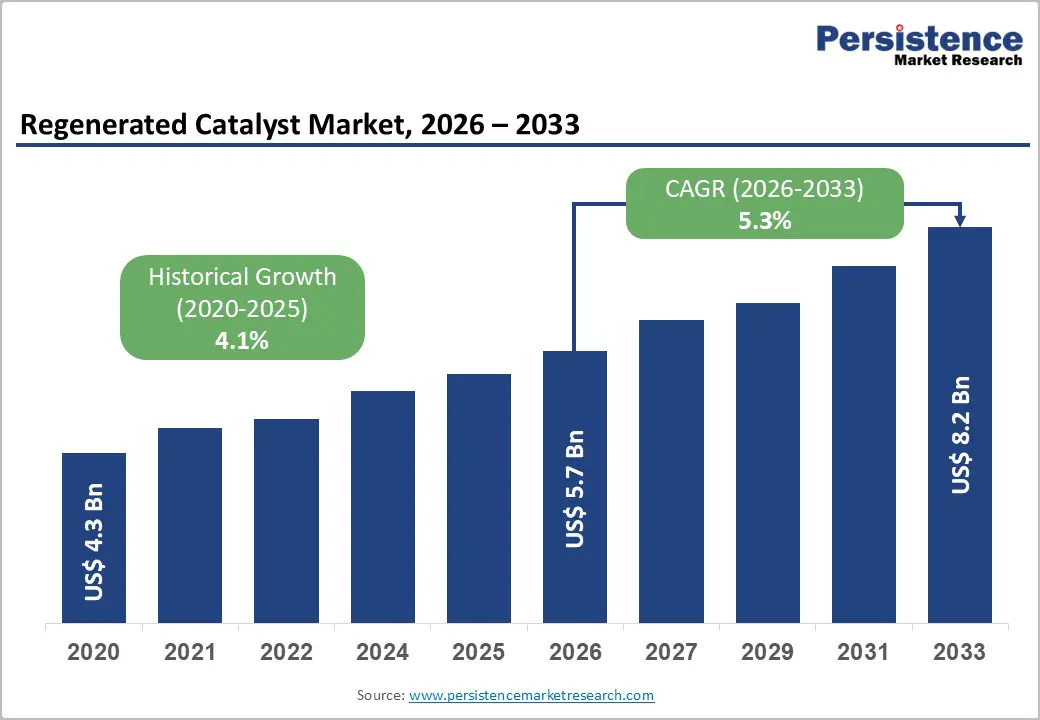

Regenerated Catalyst Market Size (2026E) |

US$ 5.7 Bn |

|

Market Value Forecast (2033F) |

US$ 8.2 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.1% |

DRO Analysis

Rising Global Refining Capacity and Throughput Expansion

According to the International Energy Agency (IEA), global refinery throughput is projected to exceed 85 million barrels per day by 2026, driven by demand growth in Asia and the Middle East. This increase directly impacts catalyst consumption and regeneration demand. Refineries are under pressure to maximize operational efficiency and reduce downtime, making regenerated catalysts a cost-effective solution compared to fresh catalysts, which can be 30–50% more expensive. In line with this trend, large-scale refinery expansions such as Indonesia’s Balikpapan refinery upgrade (2026) are significantly increasing processing capacity and output efficiency.

The market impact is significant as regeneration reduces raw material dependency and enhances catalyst lifecycle utilization. As refining complexity increases due to heavier crude processing, the need for efficient catalyst reuse solutions is accelerating. Recent geopolitical disruptions and supply constraints have also pushed refiners to operate at higher utilization rates to stabilize fuel supply, as seen in increased production adjustments across global facilities in 2026. This trend is reinforcing sustained demand for regeneration services globally, particularly in regions investing heavily in refining infrastructure upgrades and operational resilience.

Stringent Environmental Regulations and Cost Efficiency through Circular Economy Integration

Environmental agencies such as the U.S. Environmental Protection Agency (EPA) and the European Chemicals Agency (ECHA) have intensified regulations on hazardous waste disposal and emissions. Spent catalysts are classified as hazardous due to heavy metal content, with disposal costs ranging between US$ 500–1,500 per ton depending on composition. Regeneration provides a compliant alternative by reducing landfill waste and minimizing environmental impact. At the same time, global energy security concerns and refinery disruptions, such as temporary shutdowns and restarts of major facilities such as Saudi Arabia’s Ras Tanura refinery in 2026, have highlighted the importance of resource efficiency and waste minimization.

The circular economy practices are gaining strong traction across industrial sectors. Regenerated catalysts offer cost savings of 40–60% compared to virgin catalysts, making them highly attractive in cost-sensitive sectors such as petrochemicals and refining. Companies are increasingly optimizing asset portfolios and reducing operational costs, as reflected in strategic refinery restructuring and cost-cutting initiatives undertaken by major energy firms in 2026. This dual benefit of regulatory compliance and cost efficiency is strengthening long-term market demand while encouraging innovation in regeneration technologies and sustainable industrial practices.

Performance Degradation and Limited Regeneration Cycles

While regeneration is cost-effective, catalysts typically experience performance loss of 5–15% after each cycle, depending on contamination levels and process conditions. This limits the number of regeneration cycles, particularly for high-precision applications such as reforming and isomerization. As catalysts are exposed to repeated regeneration, issues such as metal fouling, pore structure damage, and reduced activity become more pronounced. These technical limitations are critical in processes where consistent catalytic performance is essential for maintaining product quality and process stability.

In 2025, several refinery operators reported reduced efficiency in multi-cycle regenerated catalysts, necessitating partial replacement with fresh catalysts. This performance limitation creates a trade-off between cost savings and operational efficiency, restricting adoption in certain high-performance applications. Additionally, ongoing refinery disruptions and closures, such as the shutdown of major facilities in the U.S. and Europe, have highlighted operational challenges and efficiency pressures within the sector. As a result, refiners are increasingly cautious about relying heavily on regenerated catalysts in critical processes, reinforcing limitations in widespread adoption.

High Capital Investment for Advanced Regeneration Technologies

Advanced regeneration methods, including CCR and plasma-based systems, require significant capital investments exceeding US$ 10–20 million per facility. Smaller refineries and chemical plants often face financial constraints in adopting these technologies. The high upfront cost is further compounded by the need for specialized infrastructure, skilled labor, and ongoing maintenance. For many operators, especially in cost-sensitive markets, these financial requirements create a substantial barrier to entry, slowing the transition toward advanced regeneration solutions.

Multiple mid-sized refiners in emerging markets delayed modernization projects due to rising capital costs and uncertain returns. This trend is further supported by broader industry movements, where energy companies have reduced capital expenditure and restructuring activities have intensified. For instance, major oil firms have cut investments and divested refining assets to control costs, reflecting tightening financial conditions across the sector. This financial environment continues to limit large-scale adoption of advanced regeneration technologies, particularly in developing regions where funding and return visibility remain key concerns.

Expansion in Emerging Markets and Global Refining Hubs

Emerging economies such as India, China, and Southeast Asia are expanding refining capacities. According to India’s Ministry of Petroleum and Natural Gas, refining capacity is expected to reach 310 MMTPA by 2026. This expansion is part of a broader global trend, with capacity additions also observed in the Middle East and Asia Pacific to meet rising fuel and petrochemical demand. For instance, new large-scale refinery and petrochemical projects in China and the Middle East became operational or progressed significantly during 2025–2026, increasing global processing capacity and utilization rates, as reported by international energy agencies and major news outlets.

This expansion creates a substantial opportunity for regeneration services. Localized regeneration facilities and strategic partnerships can capitalize on this growth, particularly in cost-sensitive markets. Additionally, global energy companies are increasing long-term supply agreements and downstream investments to secure fuel supply chains, which in turn sustains high refinery utilization. This consistent operational intensity strengthens the long-term demand for catalyst regeneration services across both emerging and established refining hubs.

Technological Advancements and Expansion into Environmental Applications

Innovations such as microwave-assisted regeneration and AI-driven process optimization are improving efficiency and reducing performance degradation. In 2025, several pilot projects demonstrated up to 20% improvement in catalyst recovery efficiency, highlighting the growing impact of advanced technologies. At the same time, governments in North America, Europe, and Asia have increased investments in cleaner refining and industrial decarbonization. For example, large-scale clean fuel and hydrogen-related refinery upgrades announced across the U.S., EU, and East Asia reflect a global shift toward more efficient and sustainable processing technologies, as covered by agencies and publications such as Reuters and government energy departments.

The increasing focus on sustainability is expanding catalyst regeneration beyond traditional refining applications into environmental and waste treatment sectors. Regulatory frameworks promoting carbon neutrality are driving adoption in emission control systems. In 2025–2026, multiple energy companies and industrial operators globally integrated emission reduction technologies and circular resource strategies into their operations. This reflects a broader transition toward low-carbon industrial systems, where regenerated catalysts play a key role in reducing waste and improving efficiency. These trends are expected to generate new revenue streams, with advanced methods and environmental applications, creating strong long-term growth potential.

Category-wise Analysis

Catalyst Type Insights

FCC catalysts are expected to hold the dominant position in 2026, accounting for approximately 36% of the regenerated catalyst market revenue share, primarily due to their widespread use in gasoline production within refining operations. These catalysts operate in high-throughput environments where deactivation occurs rapidly, making regeneration a necessary and recurring process. Their high replacement frequency and operational importance make them the most commercially viable segment for regeneration services. In January 2026, the U.S. Energy Information Administration (EIA) reported that refinery utilization rates in the United States exceeded 90%, with FCC units playing a central role in gasoline output. This sustained high utilization directly reinforces consistent demand for FCC catalyst regeneration services.

Hydroprocessing catalysts are likely to represent the fastest-growing segment, with an estimated CAGR of 5.8%, driven by increasing regulatory pressure to produce low-sulfur fuels. Refineries are upgrading their processing capabilities to comply with stringent emission standards such as Euro VI, leading to higher adoption of hydroprocessing units. In March 2025, Shell announced the expansion of its hydroprocessing capacity at the Rheinland refinery in Germany, aimed at producing cleaner fuels and reducing sulfur content, as reported by Reuters. These catalysts play a critical role in desulfurization and hydrogenation processes, and their increasing usage is directly contributing to higher regeneration demand, supporting strong segment growth.

Application Insights

Petroleum refining is projected to capture roughly 50% of the regenerated catalyst market share in 2026, owing to its intensive catalyst usage and continuous operational cycles. Refineries depend heavily on catalysts for core processes such as cracking, reforming, and hydrotreating, making regeneration an integral part of operational efficiency. In February 2026, Saudi Aramco restarted operations at its Ras Tanura refinery, one of the world’s largest, following maintenance activities, as reported by Reuters. The resumption of high-capacity operations in such large-scale facilities significantly increases catalyst usage cycles, thereby reinforcing the need for regeneration services within refining applications.

Environmental and circular economy applications are emerging as the fastest-growing segment, with a projected CAGR of 6%, supported by global sustainability initiatives and stricter emission control regulations. Industries are increasingly adopting regenerated catalysts in applications such as emission treatment, waste processing, and pollution control systems. In 2025, the European Commission advanced industrial decarbonization initiatives under the Green Deal Industrial Plan, encouraging the adoption of resource-efficient technologies, including catalyst reuse in emission control systems. This policy-driven shift toward sustainability is accelerating the integration of regenerated catalysts beyond refining, creating new growth opportunities across environmental applications.

Regional Insights

North America Regenerated Catalyst Market Trends

North America represents a strong and mature market for regenerated catalysts, supported by advanced refining infrastructure and high levels of technological adoption. While not the largest by volume, the region stands out for its leadership in innovation and process optimization, particularly in the United States. The presence of stringent environmental regulations, enforced by agencies such as the U.S. EPA, has made catalyst regeneration a standard practice for hazardous waste management. This regulatory environment ensures consistent demand for high-quality regeneration services across refining and petrochemical operations.

The region’s competitive strength lies in its early adoption of advanced regeneration technologies, including automation and AI-driven process monitoring. In 2025, leading refiners in the U.S. continued investing in digital refinery solutions to improve efficiency and reduce emissions, reinforcing the shift toward smarter catalyst lifecycle management. North America’s well-established service ecosystem further enables integrated offerings that combine regeneration with performance optimization. This positions the region as a technology benchmark, influencing global best practices in catalyst regeneration and sustainability.

Europe Regenerated Catalyst Market Trends

Europe holds a substantial position in the regenerated catalyst market, supported by strong contributions from Germany, the U.K., France, and Spain. The region’s growth is largely influenced by strict environmental regulations and circular economy initiatives under frameworks such as the European Green Deal. In 2025, the European Commission strengthened industrial emission reduction targets as part of its climate policy framework, increasing compliance requirements for refining and chemical industries. This regulatory push is accelerating the adoption of catalyst regeneration as a sustainable alternative to disposal.

Countries across Europe are investing heavily in sustainable refining processes and emission reduction technologies, further boosting market demand. In 2026, TotalEnergies advanced its strategy to convert traditional refining assets into low-carbon energy platforms, focusing on cleaner fuels and efficiency improvements. Regulatory harmonization across the European Union ensures consistent standards, enabling smoother adoption of advanced regeneration practices. The market remains moderately consolidated, with a strong emphasis on innovation, sustainability, and long-term environmental compliance.

Asia Pacific Regenerated Catalyst Market Trends

Asia Pacific is expected to dominate by holding a significant 37% of the regenerated catalyst market value in 2026, and is also projected to be the fastest-growing region with an estimated CAGR of 5.8% through 2033. This leadership is driven by rapid industrialization, expanding refining capacities, and increasing energy demand across key economies such as China, India, and ASEAN countries. In 2025, Zhejiang Petrochemical continued expansion of its large-scale integrated refining and petrochemical complex in China, increasing overall throughput capacity and strengthening the region’s refining base.

The regional market’s growth is supported by cost sensitivity, government-backed industrial policies, and rising fuel consumption, which collectively drive high refinery utilization rates. In 2026, Petronas progressed downstream investments in Southeast Asia, focusing on refining and petrochemical integration to enhance supply chain efficiency. These developments highlight increasing capital allocation toward refining infrastructure across Asia Pacific. Competitive dynamics are evolving rapidly, with both global and regional players expanding their presence, positioning the region as the central growth engine for the regenerated catalyst market.

Competitive Landscape

The global regenerated catalyst market structure is moderately fragmented, with leading players such as BASF SE, Albemarle Corporation, Honeywell UOP, W.R. Grace & Co., and Johnson Matthey collectively accounting for a significant share of total revenues. These companies leverage their strong relationships with refineries and petrochemical operators, along with deep technical expertise in catalyst manufacturing and lifecycle management. Their competitive advantage lies in offering integrated solutions that combine fresh catalyst supply with regeneration services, supported by continuous investments in R&D to enhance catalyst recovery efficiency and process performance.

Specialized service providers such as Veolia, Eurecat, Porocel, and regional catalyst service firms are strengthening their presence by focusing on cost-efficient regeneration services and localized operations. High entry barriers, including technical complexity, environmental compliance requirements, and capital-intensive infrastructure, limit the entry of new players. However, advancements in process optimization, digital monitoring, and circular economy models are creating opportunities for niche participants. The market is expected to witness gradual consolidation, driven by strategic partnerships, service integration, and selective acquisitions aimed at expanding technological capabilities and geographic reach.

Key Industry Developments

- In February 2026, Honeywell revised its acquisition of Johnson Matthey’s Catalyst Technologies business to £ 1.3 billion (about US$ 1.7 billion), reflecting changing market conditions and segment performance. The deal, expected to close in 2026, will strengthen Honeywell’s integrated catalyst and process technology portfolio.

- In October 2025, Ketjen and Axens expanded their collaboration with Eurecat to enhance catalyst regeneration technologies and global service capabilities. While financial terms were not disclosed, the partnership focuses on scaling efficient regeneration solutions and supporting sustainable catalyst lifecycle management.

- In September 2025, Valero’s Tennessee refinery underwent a major overhaul involving shutdown and replacement of FCC and hydroprocessing catalysts, with investments typically in the range of US$ 200–500 million. This development highlights the ongoing need for catalyst regeneration and replacement to maintain refinery efficiency.

Companies Covered in Regenerated Catalyst Market

- BASF SE

- Albemarle Corporation

- Honeywell UOP

- W.R. Grace & Co.

- Johnson Matthey

- Axens

- Clariant AG

- Haldor Topsoe

- Veolia

- Eurecat

- Porocel

- JGC C&C

- Sinopec Catalyst Co.

Frequently Asked Questions

The global regenerated catalyst market is projected to reach US$ 5.7 billion in 2026.

Rising refining throughput, strict environmental regulations, and increasing adoption of cost-efficient and sustainable catalyst lifecycle solutions are driving the market.

The market is poised to witness a CAGR of 5.3% from 2026 to 2033.

Expansion of refining capacity in emerging regions and advancements in regeneration technologies aligned with circular economy goals present key opportunities.

BASF SE, Albemarle Corporation, Honeywell UOP, W.R. Grace & Co., and Johnson Matthey are some of the key players in the market.