- Plastics, Polymers & Resins

- Recycled HDPE Market

Recycled HDPE Market Size, Share, and Growth Forecast 2026 - 2033

Recycled HDPE Market by Product Type (Non-Food-Grade, Food-Grade), End-use Industry (Packaging, Construction, Consumer Goods), and Regional Analysis, 2026 - 2033

Recycled HDPE Market Size and Trends Analysis

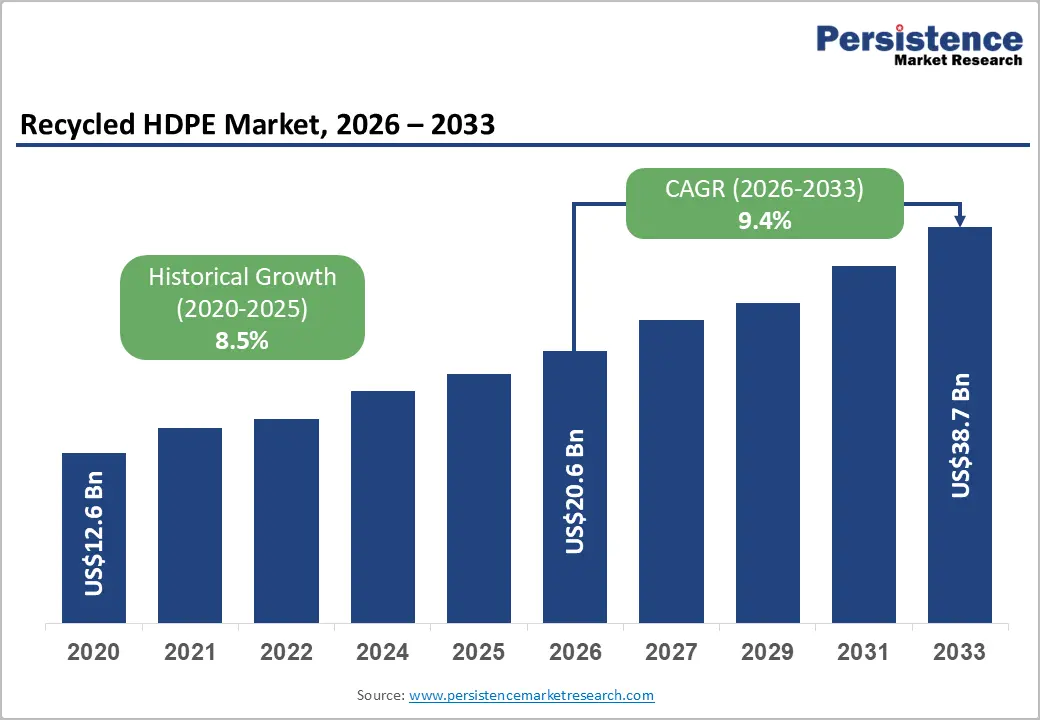

The global recycled HDPE market size is likely to be valued at US$20.6 billion in 2026 and is expected to reach US$38.7 billion by 2033, growing at a CAGR of 9.4% during the forecast period from 2026 to 2033, driven by rising regulatory pressure to increase recycled content in packaging across regions such as Europe and North America.

It is further supported by superior sustainability commitments from FMCG and packaging companies that are shifting from virgin plastics to recycled alternatives.

Key Industry Highlights:

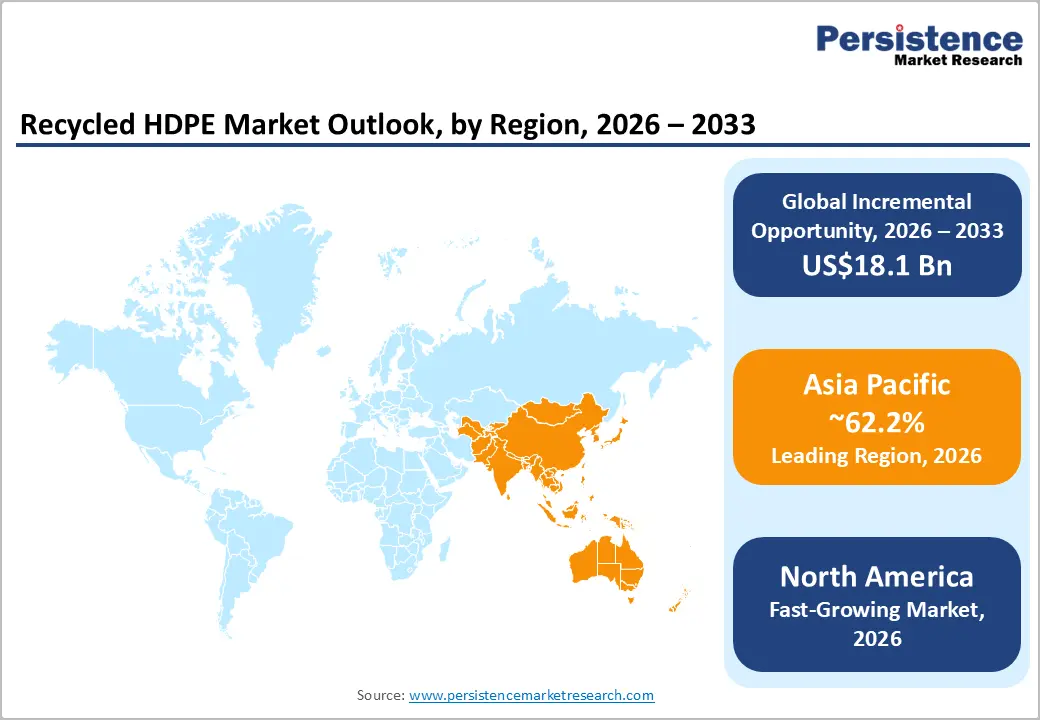

- Leading Region: Asia Pacific, with about a 62.2% share in 2026, owing to high plastic consumption and well-established waste collection networks.

- Fast-growing Region: North America, backed by strict recycled-content regulations and rising investments in high-quality recycling infrastructure.

- Leading Product Type: Non-food-grade recycled HDPE, approximately 79.5% share in 2026, as it avoids strict regulatory requirements.

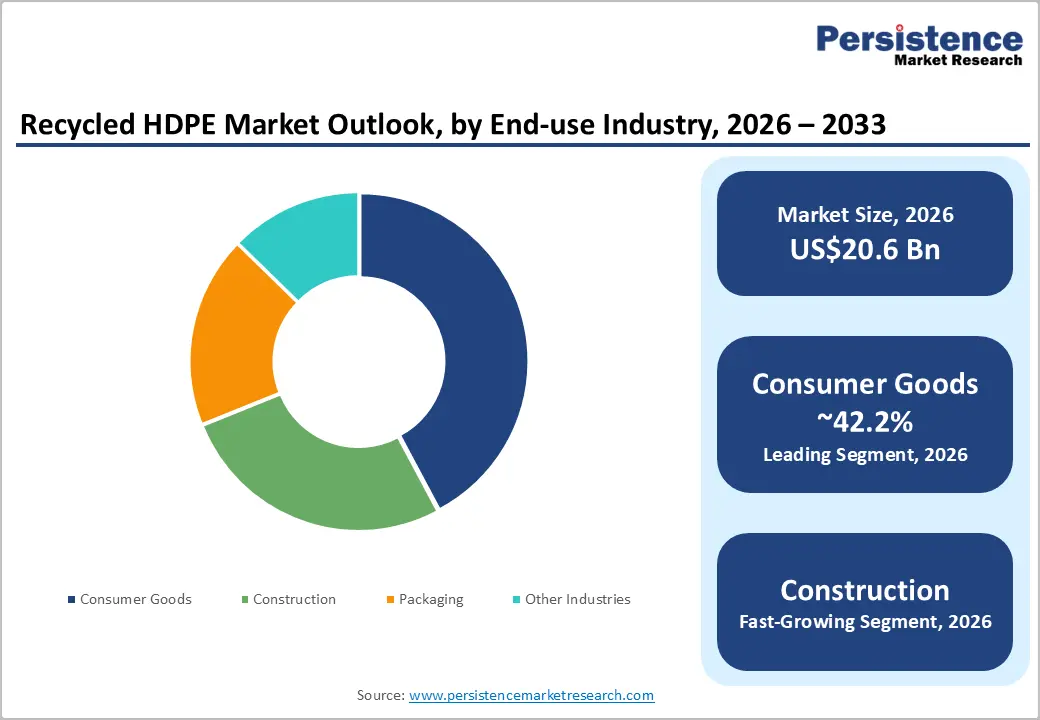

- Dominant End-use Industry: Consumer goods, nearly 42.2% in 2026, because brands are actively increasing recycled content in packaging to meet sustainability commitments.

- Latest Acquisition: In January 2025, ALPLArecycling acquired a majority stake in Clean Bottle, a Brazil-based HDPE recycling company, forming a joint venture. The plant has an annual output capacity of 15,000 tons of rHDPE. This move marked ALPLA's entry into the South America recycling market and supported its goal of increasing the post-consumer recycled content in its HDPE packaging produced in the region.

DRO Analysis

Driver - Recent Spikes in Virgin Plastic Prices

Virgin HDPE pricing is notoriously sensitive to feedstock and geopolitical shocks. According to industry price monitoring data, U.S. HDPE injection molding grade prices recorded a sharp increase of 36.57% in early March 2025, while Europe-based polyethylene suppliers implemented successive hikes starting at EUR 200 (approximately US$215) per ton, which quickly escalated to EUR 400 to 600 (approximately US$430 to 645) per ton depending on the grade. These sudden spikes push buyers to look at Recycled High-Density Polyethylene (rHDPE) as a cost buffer.

Recycled HDPE pellet prices have been rising entering Q1 2025, augmented by increased demand from the packaging sector, with natural post-consumer pellets up by 6 cents per pound. When virgin resin prices shoot up unpredictably, rHDPE delivers manufacturers a more stable and often cheaper sourcing option, making price volatility itself a recurring tailwind for the recycled segment.

Stringent Corporate Sustainability Pledges

Leading brands are no longer treating recycled content as optional. SC Johnson has met its 2025 goals by cutting virgin plastic use by 33% and increasing post-consumer recycled content to 25% across plastic packaging, with a 2030 target of 55% PCR and a 55% reduction in virgin plastic use from 2018 levels. Industry-wide, the push is rising.

The U.S. Plastics Pact set a standardized goal for signatories to achieve an average of 30% post-consumer recycled content across all plastic packaging, with strategies in place to hit 25% PCR inclusion in HDPE beverage bottles by 2026 and 60% by 2030. These binding corporate targets create a sustained and predictable pull on rHDPE supply, moving demand well beyond goodwill gestures into contractual procurement commitments.

Restraint - Structural Weakening during Reprocessing May Limit rHDPE Usage

Every time HDPE is melted and reprocessed, its polymer chains take a hit. Repeated extrusion and thermo-mechanical processing promote chain scission and oxidative degradation, resulting in reductions in molecular weight and crystallinity, and marked changes in melt flow index and rheological behavior. These modifications can compromise stiffness and strength.

A study published in ScienceDirect (2023) confirms this directly. Increasing the number of thermal reprocessing cycles decreased tensile strength, elastic modulus, impact strength, and storage modulus in rHDPE. This rules rHDPE out of load-bearing or high-stress applications where mechanical specs are non-negotiable. Blending with virgin HDPE partially compensates, but adds cost and dilutes the recycled content claim. It further creates an ongoing tension between performance and sustainability goals for manufacturers.

Opportunity - Emergence of Food-Grade rHDPE in Global Markets

Until recently, rHDPE was barred from food-contact use due to contamination risks. That is changing fast. Borealis received two Food and Drug Administration (FDA) Letters of No Objection (LNOs) effective January 2024 for its Borcycle M mechanically recycled HDPE, allowing it to be used up to 100% in certain dry food contact applications and up to 10% in packaging for dry foods with surface oil and moist bakery products.

It is not an isolated case. In 2024 alone, the FDA approved food-contact post-consumer recycled materials including HDPE, LDPE, PP, and PET, with companies such as Blue Polymers and JB Ecotex receiving LNOs for HDPE in contact with produce, dairy, and fatty foods. As solvent-based purification and chemical recycling mature, rHDPE is edging into one of the highest-volume and highest-value packaging segments previously closed to it.

New Techniques to Reduce Discoloration for Visual Aesthetics

Mixed-color post-consumer HDPE carries gray or green tints that disqualify it from use in products requiring a clean and white finish. New solvent-based purification approaches are tackling this directly. A U.S. Patent and Trademark Office (USPTO)-registered patent describes a pressurized solvent method that produces essentially contaminant-free, pigment-free, odor-free, and homogeneous rHDPE with natural-like optical properties. It is similar in appearance to natural virgin HDPE.

On the research side, a 2024 paper published in Green Chemistry (RSC) demonstrated that natural terpene solvents such as limonene, α-pinene, and p-cymene show good capability for dissolving and purifying HDPE in a more sustainable dissolution-precipitation process. Better color control means brands can raise their recycled content percentage without the white or unpigmented products turning visually unacceptable. It is a direct path to extending rHDPE use in consumer-facing categories, including dairy packaging.

Category-wise Analysis

Product Type Insights

Non-food-grade recycled HDPE is predicted to lead with a share of approximately 79.5% in 2026, as it can be used in a much wider range of applications without meeting strict food-contact regulations. Products such as detergent bottles, chemical containers, industrial drums, crates, pallets, buckets, outdoor furniture, pipes, and construction materials can utilize recycled HDPE with relatively simple processing. This creates a large and stable demand base across industries. Another key advantage is low production cost.

The food-grade recycled HDPE segment is estimated to be the fastest-growing segment in the forecast period, as governments and brand owners are under increasing pressure to reduce virgin plastic consumption in food packaging. Regulations in Europe and North America are encouraging the use of recycled content in packaging while maintaining food safety standards. This is pushing companies to invest in high-quality food-grade recycling technologies. Another important factor is technological improvement. Unique sorting systems, near-infrared identification technologies, and decontamination processes now allow recyclers to produce clean recycled HDPE suitable for food-contact applications.

End-use Industry Insights

Consumer goods are anticipated to dominate with a share of nearly 42.2% in 2026, as HDPE is already deeply integrated into everyday products. Household cleaners, shampoo bottles, laundry detergent containers, storage bins, toys, furniture, crates, and utility products all rely heavily on HDPE. Replacing virgin resin with recycled HDPE is often easier in these products than in highly regulated industries. Fast-moving consumer goods also generate continuous demand for plastic packaging and containers. Even a small increase in recycled content across thousands of product lines creates significant recycled HDPE consumption. This demand is more consistent than in several industrial sectors.

The construction segment is expected to remain in the second position in 2026, as recycled HDPE performs well in infrastructure applications. The material delivers corrosion resistance, flexibility, chemical resistance, and long service life. These properties make it suitable for drainage systems, sewage pipes, irrigation networks, cable conduits, and geomembranes. Governments and infrastructure developers are now prioritizing sustainable construction materials. Recycled HDPE helps reduce waste while lowering the environmental footprint of construction projects. This complies with circular economy initiatives being adopted in several countries.

Regional Insights

Asia Pacific Recycled HDPE Market Trends

Asia Pacific is anticipated to dominate in 2026 with a share of nearly 62.2%, as it has the largest base of plastic consumption and waste generation, which supports recycled HDPE supply. Countries such as China, India, Indonesia, and Vietnam generate massive volumes of post-consumer plastic, especially HDPE bottles and containers. This ensures continuous feedstock availability for recyclers. According to the United Nations Environment Program, Asia accounts for a key share of global plastic waste generation, creating superior recycling potential.

China Recycled HDPE Market Trends

China will likely lead Asia Pacific in 2026 with a share of around 41.5%, due to strong policy intervention and domestic recycling expansion. After the China National Sword Policy, the country stopped importing plastic waste and invested heavily in domestic recycling systems. This compelled local capacity expansion and improved sorting technologies. The government is also enforcing strict recycled content targets. China’s National Development and Reform Commission has mandated a reduction in single-use plastics and encouraged recycled alternatives in packaging. This is pushing demand for recycled HDPE in sectors such as e-commerce and food delivery.

India Recycled HDPE Market Trends

In 2026, India is projected to account for a share of approximately 24.1%, with a policy-driven recycling network, but it still depends heavily on informal players. The government’s Plastic Waste Management Rules and Extended Producer Responsibility (EPR) framework have made it mandatory for producers to use recycled content. This is increasing the demand for recycled HDPE in packaging and consumer goods. The Ministry of Environment, Forest and Climate Change has mandated that brand owners ensure proper plastic waste collection and recycling. Hence, FMCG companies are partnering with recyclers to secure recycled materials. For example, several local brands have started using recycled plastic in packaging to meet EPR targets.

North America Recycled HDPE Market Trends

North America is predicted to be the fastest-growing region in 2026 with a share of approximately 18.9%, owing to strict sustainability commitments and corporate demand for recycled content. Large companies are setting clear targets to increase recycled plastic usage in packaging. This is creating high demand for recycled HDPE, especially in food-grade and high-quality applications. Government support is also increasing. The U.S. Environmental Protection Agency (EPA) promotes recycling through initiatives such as the National Recycling Strategy. The U.S. recycling rate for plastics remains low at around 8 to 9%, which highlights a large untapped opportunity for growth.

U.S. Recycled HDPE Market Trends

A share of nearly 63.8% is expected to be held by the U.S. in 2026, backed by strong corporate action and infrastructure investments. Leading companies are committing to using recycled plastics. For example, brands such as Procter & Gamble and Unilever have announced targets to increase recycled content in packaging. The American Chemistry Council reports that billions of dollars have been committed to recycling and recovery projects in recent years. These investments focus on improving collection, sorting, and processing capabilities.

Europe Recycled HDPE Market Trends

Europe will likely see decent growth over the forecast period, with a share of nearly 12.6% in 2026, spurred by favorable regulatory frameworks and circular economy policies. The European Commission has introduced strict rules under the Circular Economy Action Plan. These include targets for recycled content and restrictions on single-use plastics. The European Environment Agency reports that Europe has one of the highest plastic recycling rates globally, supported by well-developed collection and sorting systems. This ensures a stable supply of recycled HDPE.

Germany Recycled HDPE Market Trends

Germany will likely register a substantial share of approximately 33.7% in 2026, as it has a highly efficient waste management and recycling system. The country’s dual system for packaging waste ensures high collection rates. According to the Federal Environment Agency, Germany achieves some of the highest recycling rates in Europe. The government also enforces strict regulations. The Packaging Act requires companies to register and ensure recycling of their packaging materials. This creates consistent demand for recycled HDPE.

U.K. Recycled HDPE Market Trends

A share of around 18.9% is predicted to be held by the U.K. in 2026. The government has introduced a Plastic Packaging Tax, which applies to packaging with less than 30% recycled content. This is pushing companies to increase the use of recycled HDPE. According to the U.K. Environment Agency, the country is strengthening its recycling infrastructure and compliance mechanisms. Extended Producer Responsibility reforms are also being implemented to improve collection and recycling rates.

Competitive Landscape

The global recycled HDPE market is moderately fragmented, with no single company exercising dominant control over global supply. The industry comprises a mix of large waste-management companies, specialized plastic recyclers, and integrated packaging manufacturers, while hundreds of regional recyclers compete in local markets. Companies such as Veolia, Biffa, KW Plastics, Plastipak Holdings, Envision Plastics, and ALPLA Group are focusing on securing long-term waste collection networks and post-consumer plastic streams to ensure stable production.

Technology is becoming another important battleground. Companies are investing in advanced washing, sorting, decontamination, and food-grade recycling technologies to meet stringent regulatory requirements. Recyclers capable of producing FDA- and EFSA-compliant recycled HDPE are gaining a competitive edge, especially in packaging, personal care, and household product applications where quality standards are high.

Key Industry Developments:

- In May 2026, Recove Ventures signed a 10-year Memorandum of Understanding with the Maharashtra government, committing to an investment of INR 500 crore (approximately US$52.4 million) to develop a large-scale plastic recycling and circular manufacturing ecosystem across the state. The first project under the agreement is an advanced HDPE and PP recycling facility at Additional Jalgaon MIDC in the Jalgaon district.

- In October 2025, LyondellBasell announced at K 2025 that it is building a chemical recycling plant in Wesseling, Germany, using its proprietary MoReTec technology, with an annual processing capacity of 50,000 metric tons. The plant forms part of LyondellBasell's broader effort to extend its Circulen portfolio of circular polymer products, including recycled HDPE grades.

- In December 2025, ALPLA Group announced the establishment of a new recycling company in partnership with the National Test Center for Circular Plastics (NTCP) to develop a food-grade HDPE recycling process. The initiative was supported by a grant from the Dutch Ministry of Climate Policy and Green Growth.

Companies Covered in Recycled HDPE Market

- Veolia Environnement SA

- Biffa Group

- KW Plastics

- Plastipak Holdings, Inc.

- Altium Packaging (Envision Plastics)

- ALPLA Werke Alwin Lehner GmbH & Co. KG

- Cirplus GmbH

- KAMAL POLYPLAST

- Reprocessed Plastics, Inc.

- Reclaim Plastics

- Others

Frequently Asked Questions

The global recycled HDPE market is projected to be valued at US$20.6 billion in 2026.

The recycled HDPE market is expected to reach US$38.7 billion by 2033.

Key market trends include rising recycled-content mandates and brand-led sustainability targets.

Non-food-grade recycled HDPE is expected to be the leading product type with a share of nearly 79.5% in 2026, due to the high volume of HDPE-based packaging used in everyday products.

The recycled HDPE market is expected to grow at a CAGR of 9.4% from 2026 to 2033.

Veolia Environnement SA, Biffa Group, KW Plastics, and Plastipak Holdings, Inc. are a few key market players.