- Retail

- Point-of-Purchase (POP) Displays Market

Point-of-Purchase (POP) Displays Market Size, Share, and Growth Forecast, 2026-2033

Point-of-Purchase (POP) Displays Market by Display Format (Countertop Displays, Floor Standees, End-of-Aisle Displays, Digital Signage, Interactive Kiosks, AR-Enabled Displays), Material & Technology (Paper & Corrugated Board, Plastic, Metal, LED Panels, Sensor-Enabled Displays), End-User (Grocery & Supermarkets, Beauty & Personal Care, Consumer Electronics, Apparel & Fashion, QSRs), and Regional Analysis for 2026-2033

Point-of-Purchase (POP) Displays Market Share and Trends Analysis

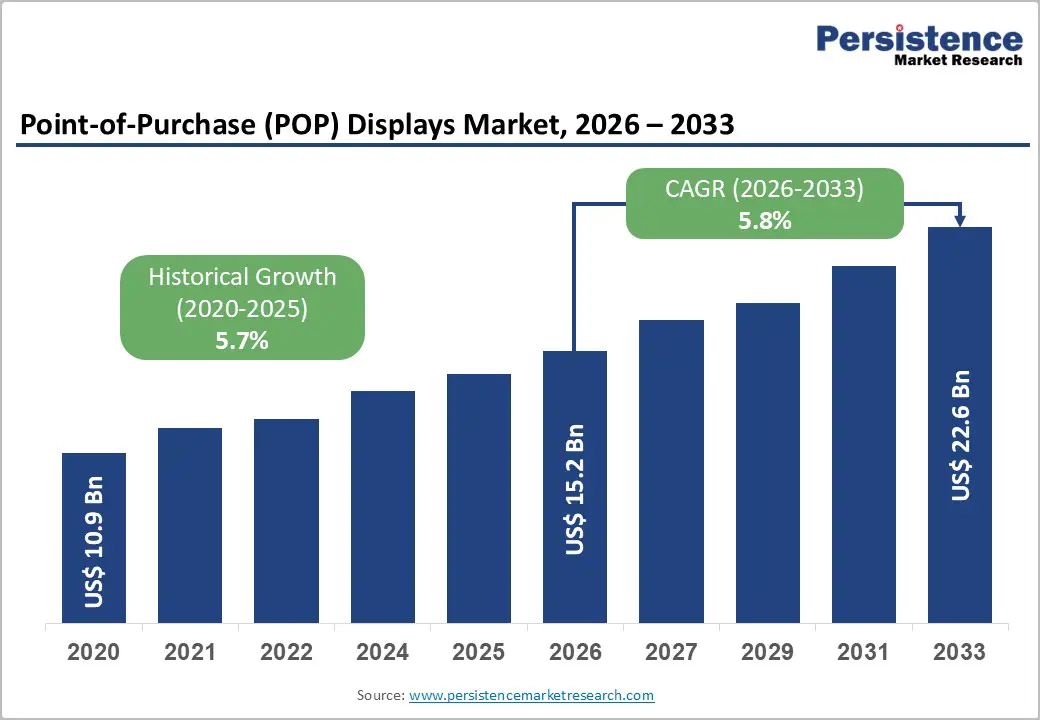

The global point-of-purchase (POP) displays market size is likely to be valued at US$15.2 billion in 2026, and is projected to reach US$ 22.6 billion by 2033, growing at a CAGR of 5.8% during the forecast period 2026–2033. This growth is fueled by rising in store marketing investments as retailers aim to capture consumer attention at critical decision points. Shoppers increasingly respond to visually engaging POP displays, prompting brands in grocery, beauty, consumer electronics, and fashion sectors to deploy innovative formats that drive impulse purchases and elevate product visibility. The integration of digital signage, interactive kiosks, and AR enabled displays enables real-time consumer engagement and personalized messaging, enhancing conversion rates. Retailers are adopting sustainable and recyclable materials and optimizing supply chains to reduce costs, improve operational efficiency, and meet evolving regulatory and environment, social, & governance (ESG) requirements, further shaping material and technology choices in the market.

Key Industry Highlights

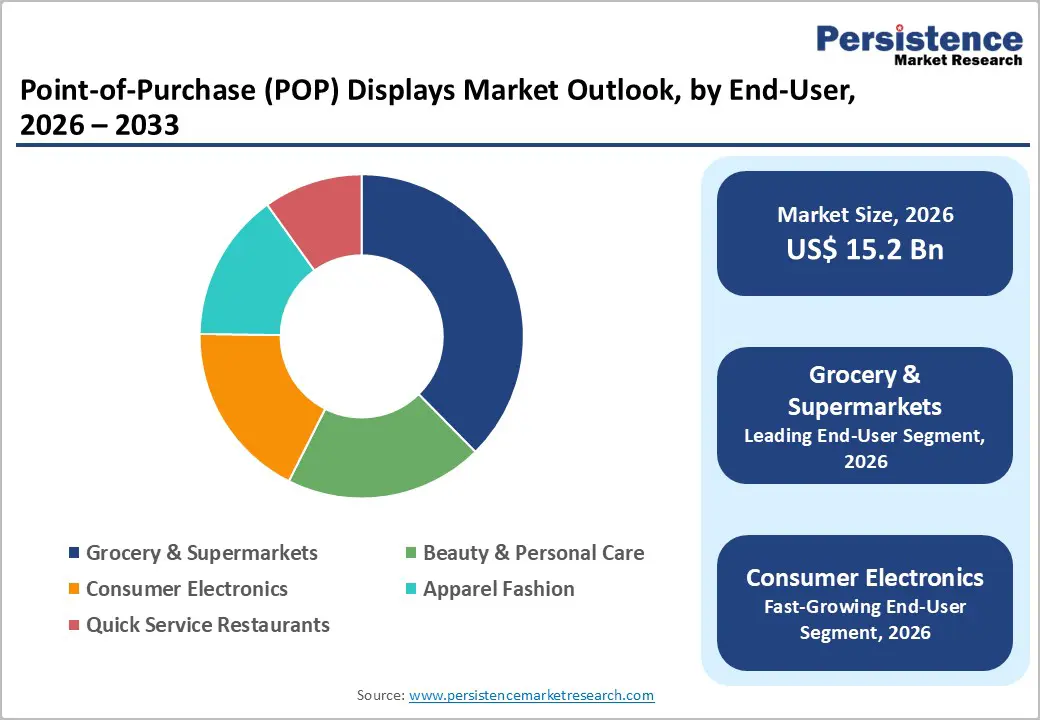

- Dominant End-User: Grocery and supermarkets are set to hold around 38% market share in 2026, leveraging high-traffic placements and frequent promotions.

- Fastest-Growing End-User: Consumer electronics is likely to grow the fastest at roughly 10.8% CAGR through 2033, fueled by experiential merchandising and interactive installations.

- Leading Display Format: Floor standees are set to command around 40% revenue share in 2026, reflecting high visibility and strategic placement in retail aisles.

- Fastest-Growing Display Format: Digital POP displays are likely to grow the fastest from 2026 to 2033, driven by interactive and immersive shopper engagement.

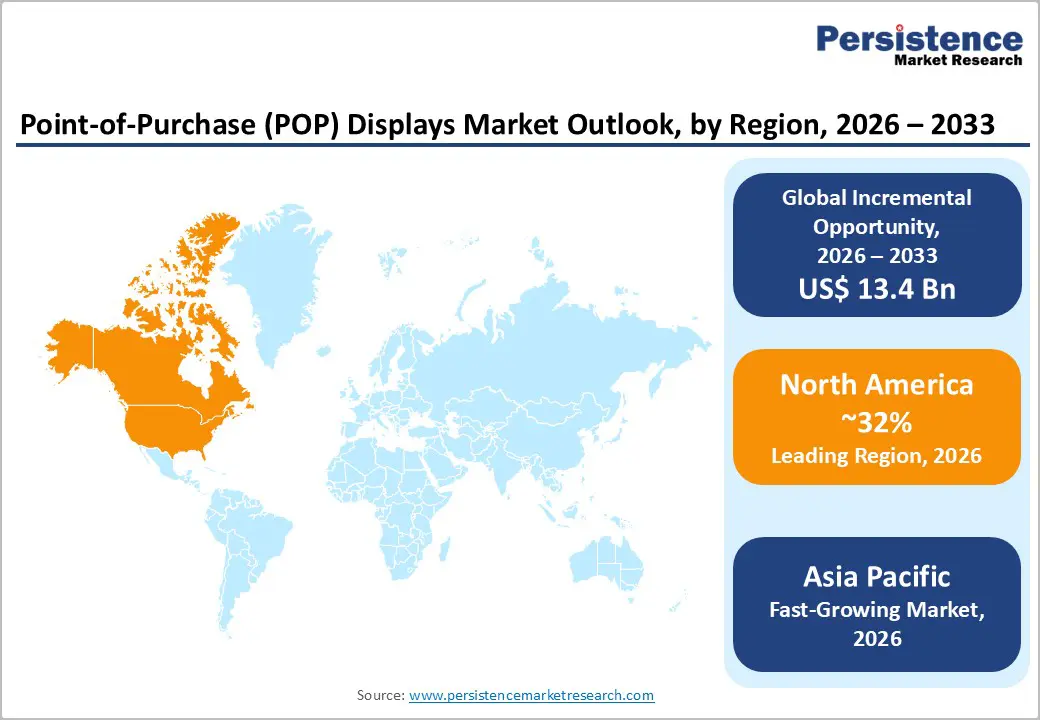

- Regional Leadership: North America is projected to lead with 32% market share in 2026, while Asia Pacific is expected to be the fastest-growing market at about 9.4% CAGR through 2033, supported by retail modernization.

- Strategic Trend: Sustainability adoption and digital integration continue to drive material innovation and interactive technology deployment across global markets.

| Key Insights | Details |

|---|---|

|

Point of Purchase (POP) Displays Market Size (2026E) |

US$ 15.2 Bn |

|

Market Value Forecast (2033F) |

US$ 22.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.8% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.7% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Retail Marketing Investments and Shopper Engagement Needs

Global retail environments are significantly increasing investments in in-store promotional strategies to enhance conversion rates at checkout counters and high-traffic zones. Over 60% of consumer purchases are influenced by in-store display interaction, highlighting the critical role of point-of-purchase displays in shaping buying decisions. Floor standees and end-of-aisle units are particularly effective, capturing shopper attention and improving brand recall across multiple product categories. Retailers are also focusing on strategic placement of promotional displays to maximize visibility in seasonal campaigns and high-demand areas.

Recent industry movements reinforce this trend. At NRF 2026, retailers showcased AI-driven, interactive in-store solutions designed to enhance shopper engagement and improve promotional effectiveness. Crave Retail unveiled smart fitting rooms and store-wide engagement platforms integrating radio frequency identification (RFID) and mobile insights, demonstrating how POP displays are increasingly part of data-driven, immersive retail experiences that directly impact conversion rates and basket size. These innovations are driving measurable improvements in store performance metrics, emphasizing the strategic value of POP technologies in modern retail operations.

Digital Integration and Sustainability Adoption

The evolution of digital signage, augmented reality (AR)-enabled displays, and interactive kiosks is transforming traditional POP deployments into data-driven, interactive customer touchpoints. Integration of technologies such as QR codes, near-field communication (NFC), and RFID allows brands to engage shoppers with personalized content, product storytelling, and targeted promotions, enhancing average basket size. These innovations complement omnichannel retail strategies, seamlessly connecting physical store experiences with digital engagement. Retailers are also leveraging real-time performance tracking to optimize in-store messaging and improve ROI across campaigns.

Sustainability has emerged as a key purchasing criterion, with over 30% of global POP installations now using recyclable or biodegradable materials, including corrugated board and plant-based polymers. Supporting this, SOLUM showcased e-paper and smart in-store solutions at NRF 2026 emphasizing eco-friendly, tech-enabled merchandising, while the digital signage market continues to expand globally with smart, energy-efficient displays. Together, these developments highlight how retailers are investing in both digital integration and sustainable material adoption to enhance shopper experience and brand reputation. This dual focus is reinforcing long-term operational efficiency and aligning with evolving ESG expectations.

Barrier Analysis - High Production and Customization Costs

While digital and interactive POP displays offer enhanced consumer engagement, customized high-impact units can cost 30–35% more than traditional static signage, limiting adoption among smaller brands and emerging retailers. Additional costs arise from specialized materials, complex fabrication, and integration of interactive components, creating financial barriers for deploying advanced POP solutions across retail categories. Retailers must carefully balance design impact with operational feasibility to maintain profitability. High-end designs also often require ongoing maintenance, adding to the total cost of ownership.

Moreover, production lead times can extend due to customization demands, requiring specialized labor and equipment for unique design specifications. Reports in 2025–2026 highlight that material cost pressures and rising labor expenses in manufacturing further increase upfront investment for high-end POP solutions. Retailers aiming for seasonal or short-term campaigns may face constraints, affecting time-to-market and campaign effectiveness, emphasizing the need for selective deployment and budget optimization. Strategic planning is critical to avoid campaign delays and ensure ROI is maximized.

Supply Chain Complexities and Material Volatility

The POP display value chain is highly sensitive to fluctuations in raw material prices, including corrugated board, plastics, and metals. Nearly 25% of manufacturers report rising material costs as a key challenge affecting profitability and delivery schedules. These cost pressures can influence design choices, encourage the use of lower-cost alternatives, and affect the quality and durability of displays deployed in high-traffic retail environments. Differences in regional sourcing and local production capacity can further complicate consistency and standardization.

Industry developments in past years reinforce these challenges. Maersk surveys report that 78% of supply chain professionals expect ongoing disruptions due to geopolitical tensions and shifting trade policies, while global shipping and carrier rates have increased sharply, adding to logistics expenses. Furthermore, the World Trade Organization forecasts slowing trade growth in 2026, which may exacerbate supplier lead-time unpredictability and inventory mismatches. Retailers must adopt robust sourcing strategies and flexible supply chain planning to mitigate operational bottlenecks and ensure timely POP deployment. Advanced forecasting and buffer stock strategies are becoming increasingly essential.

Expansion in Fledgling Retail Markets

Emerging economies in Asia Pacific, particularly China and India, are witnessing rapid retail modernization, organized store expansion, and increasing disposable incomes. These markets are experiencing a growing demand for sophisticated in-store merchandising solutions, creating fertile ground for POP display adoption. Retailers are increasingly investing in interactive, high-visibility displays to capture consumer attention and encourage impulse purchases across grocery, fashion, electronics, and beauty segments. Retail modernization is also supported by urban retail hubs and increasing mall penetration, enhancing visibility for promotional displays.

Supporting this, Hikvision India launched energy-saving active LED display modules in late 2025, demonstrating how advanced retail technology is diffusing into key emerging markets. Additionally, government initiatives promoting modern retail infrastructure and digital payment integration schemes enhance store efficiency and shopper convenience. As organized retail networks expand, brands entering early can secure long-term partnerships and preferential placement opportunities, leveraging rising consumer spending through 2033. Strategic local partnerships also facilitate faster adoption and logistical efficiency, maximizing ROI for new POP deployments.

Innovation in Smart and Sustainable POP Technologies

Interactive POP solutions equipped with sensors, AR, and IoT-enabled capabilities are demonstrating up to 29% higher ROI compared with conventional displays. Retailers investing in smart, data-driven displays can monitor shopper interactions in real time, optimize product placements, and enhance engagement metrics. These solutions support personalized promotions and immersive experiences, enabling brands to differentiate offerings and increase repeat purchases across diverse retail sectors. Adoption is particularly strong in high-traffic, premium retail environments where customer engagement directly impacts sales velocity.

At ISE 2025–2026, Samsung and LG showcased AI-driven, sustainable, and ultra-efficient signage technologies, highlighting a shift toward eco-friendly, interactive, and connected retail displays. Combined with the phygital retail trend, which blends physical stores with AR and sensor-based interactivity, these innovations allow brands to integrate sustainability with digital engagement. Manufacturers developing biodegradable materials, modular assemblies, and reusable unit designs are positioned to capture premium market share while meeting ESG and lifecycle cost priorities. Growing consumer demand for environmentally responsible experiences further strengthens this opportunity.

Category-wise Analysis

Display Format Insights

Floor standees are poised to dominate in 2026 by commanding around 40% of the point-of-purchase displays market revenue share, owing to their ability to attract shopper attention in high traffic aisles and showcase featured SKUs with prominent visuals. These freestanding units drive impulse purchases, reinforce branding, and optimize aisle layouts across grocery, convenience, and lifestyle stores. Retailers increasingly combine traditional standees with digital elements and signage to extend dwell time and engagement. Supporting this trend, Iceland supermarkets rolled out oversized 3D hanging signs and thousands of digital screens in 2025, demonstrating the strategic value of high impact visual fixtures that blend static and dynamic communication, enhance shopper attention, and complement promotional activity.

Digital signage formats are likely to grow the fastest 2026 to 2033, driven by consumers’ demand for immersive, interactive in-store experiences. These solutions integrate motion sensors, screens, and AR features to deliver real-time product storytelling, personalized promotions, and alignment with omnichannel retail strategies. Adoption is particularly strong in consumer electronics and beauty sectors, where engagement directly influences sales. Supporting this growth, new advanced digital signage models launched in late 2025 feature ultra-wide formats, cloud-enabled content management, and wireless connectivity, enabling flexible placement across shelves and kiosks and reinforcing the transition from static to dynamic POP communication.

End-User Insights

Grocery and supermarket channels are anticpated to capture nearly 38% of the POP displays market revenue in 2026, leveraging floor and end-of-aisle units to enhance visibility for promotions, new product launches, and seasonal campaigns. High footfall in these stores ensures maximum exposure, increasing impulse purchases in core categories such as packaged foods and beverages. POP solutions also integrate with shelf-edge signage to guide shopper navigation and reinforce value messaging. Supporting this trend, Asda rolled out electronic pricing labels with QR codes across 250 stores in 2025, demonstrating adoption of flexible, digital display technologies that improve information clarity, operational efficiency, and in-store shopper engagement.

Consumer electronics segments is projected to grow at an estimated 10.8% CAGR through 2033, driven by experiential retail initiatives and competitive merchandising strategies. Large-format displays, interactive kiosks, and AR touchpoints enable immersive product demonstrations, style visualization, and personalized promotions, enhancing shopper engagement and conversion. Real-world momentum comes from 2025–2026 retail tech trends adopting phygital experiences and interactive displays, enabling brands to blend digital richness with physical browsing, differentiate in-store experiences, and capture higher average transaction values across high-margin categories.

Regional Insights

North America Point-of-Purchase (POP) Displays Market Trends

North America is projected to lead in 2026, accounting for around 32% of the POP displays market value in 2026, supported by high retail density, large supermarket and hypermarket networks, and advanced adoption of digital merchandising solutions. The United States is projected to lead revenue contribution, with widespread deployment of digital signage and sensor-enabled displays enhancing shopper engagement across consumer electronics, cosmetics, and grocery sectors. Retailers are expected to leverage data-driven displays to optimize in-store promotions, integrate with mobile loyalty programs, and support omnichannel strategies, improving conversion rates and campaign effectiveness.

Market trends suggest continued growth driven by sustainability and operational efficiency priorities. In 2025, cloud-based digital signage management systems were increasingly adopted across multi-location retailers, enabling centralized content control and consistent messaging deployment. This is estimated to reduce operational costs and enhance campaign impact across chains. North America’s competitive landscape is likely to remain consolidated, with leading display providers investing in automation, customized content, and interactive solutions to maintain market leadership and meet evolving retailer demands.

Europe Point-of-Purchase (POP) Displays Market Trends

Europe is forecasted to hold a significant portion of the point-of-purchase displays market share in 2026, with Germany, the U.K., and France as primary contributors due to high organized retail penetration and regulatory emphasis on sustainability. Retailers are expected to adopt recyclable and modular POP designs, integrating digital and interactive elements to enhance omnichannel engagement. Grocery, health & beauty, and QSR segments are likely to sustain demand for both traditional and tech-enabled displays. Estimated growth is supported by strong urban retail infrastructure and compliance with energy efficiency and environmental standards.

Industry movements indicate steady adoption of sensor-based tracking technology across European supermarkets, allowing real-time measurement of shopper exposure and improving in-store promotional accountability. This trend is expected to enhance POP effectiveness while maintaining compliance with data privacy regulations. European retailers are likely to continue investing in smart display networks and data-driven content solutions, supporting operational efficiency, campaign agility, and long-term growth in the region.

Asia Pacific Point-of-Purchase (POP) Displays Market Trends

Asia Pacific is estimated to be the fastest-growing market for POP displays, likely to showcase an approximate 2026-2033 CAGR of 9.4%, driven by rapid urbanization, rising disposable incomes, and expansion of organized retail in China, India, and Japan. Adoption of interactive, sensor-enabled, and AR-integrated POP solutions is expected to accelerate across grocery, electronics, apparel, and lifestyle sectors. Local manufacturing advantages, including lower production costs and proximity to supply chains, are estimated to enable high-volume deployments, while retailers integrate POP with digital loyalty and mobile engagement initiatives to improve shopper experience and conversion rates.

Verified developments indicate that smart city and digital signage initiatives expanded significantly in 2025–2026, with government-backed programs installing thousands of digital screens for retail and urban wayfinding. These efforts are estimated to further accelerate POP adoption and support retail digital transformation. Coupled with rising consumer expectations for immersive experiences, Asia Pacific is expected to continue serving as a dynamic growth engine for interactive POP technologies, driving both domestic and international supplier opportunities.

Competitive Landscape

The global point-of-purchase displays market structure is moderately consolidated, with leading players such as Pro Mach, Axyz Printing, WestRock, DS Smith, and ITAB Shop Concept collectively accounting for over 50% of the market revenue in 2026. These companies leverage extensive relationships with retailers and brands, strong supply chain networks, and integrated design-manufacturing capabilities. They continue to invest in R&D and digital integration, focusing on smart, interactive, and sensor-enabled displays, augmented reality solutions, and sustainable material innovations to maintain a competitive edge.

Regional and niche players, including DisplayCraft, Sealed Air, and Vivid Displays, focus on specialized formats, vertical markets, or localized distribution channels. Barriers to entry such as high production costs, material sourcing complexity, and retailer certification requirements limit new entrants. However, trends in digitalization, modular design, and cloud-enabled content management are enabling software and tech-focused firms to participate, offering smart signage, interactive kiosks, and data-driven shopper analytics. Market consolidation is expected to increase gradually as global leaders pursue strategic acquisitions and integration partnerships to expand geographic reach, enhance technology portfolios, and meet growing demand for immersive, ROI-focused POP solutions.

Key Industry Developments

- In November 2025, Bauer Media Outdoors finalized a seven-year agreement with Morrisons to deploy and operate digital Waferlite screens across 300 U.K. stores, creating long-term revenue streams and enhancing in-store shopper engagement through advanced digital signage.

- In November 2025, Bed Bath & Beyond merged with the Brand House Collective, with the aim to convert 300 stores and expand in-store technology deployments, enabling experiential retail formats and supporting the company’s strategic modernization of its physical retail footprint.

- In June 2025, Albertsons Media Collective launched an in-store digital display network that installs large-format digital screens in high-traffic store areas such as entrances and produce sections to deliver targeted brand messaging at the point of purchase. Developed with STRATACACHE, the network enables advertisers to run campaigns with performance measurement tools that track engagement and sales impact during shoppers’ in-store journeys.

Companies Covered in Point-of-Purchase (POP) Displays Market

- International Paper Company

- DS Smith Plc

- Smurfit Kappa Group PLC

- Sonoco Products Company

- Menasha Packaging Company LLC

- Georgia Pacific LLC

- Pratt Industries Inc.

- FFR Merchandising Company

- Marketing Alliance Group

- LG Innotek

- Samsung Display Solutions

Frequently Asked Questions

The global point-of-purchase (POP) displays market is projected to reach US$ 15.2 billion in 2026.

Growth is driven by increasing in-store marketing investments, digital integration, and rising shopper engagement strategies.

The market is poised to witness a CAGR of 5.8% from 2026 to 2033.

Opportunities exist in emerging retail markets, interactive display technologies, and sustainable material adoption.

Some of the leading players in the market include Pro Mach, Axyz Printing, WestRock, DS Smith, and ITAB Shop Concept.