- Metalworking & Fabrication

- Metal Fabrication Equipment Market

Metal Fabrication Equipment Market Size, Share, and Growth Forecast 2026 - 2033

Metal Fabrication Equipment Market by Equipment Type/Process (Machining, Cutting, Welding and Joining Equipment), by Material Type (Steel, Aluminum, Copper), by End-user Industry (Automotive, Construction), and Regional Analysis, 2026 - 2033

Metal Fabrication Equipment Market Size and Trends Analysis

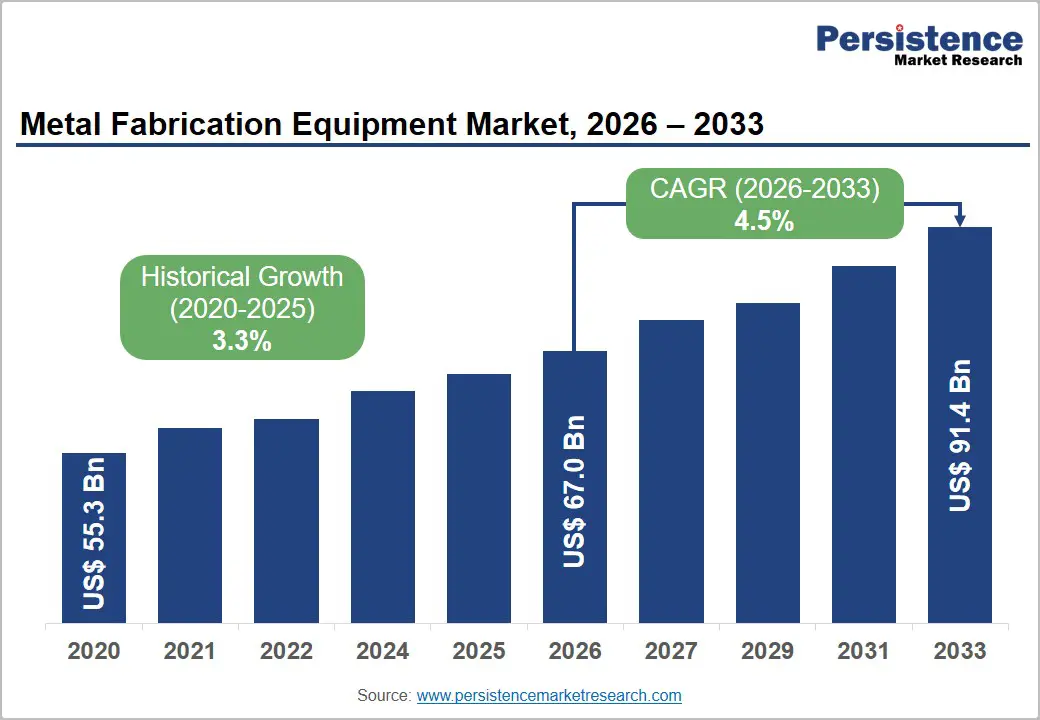

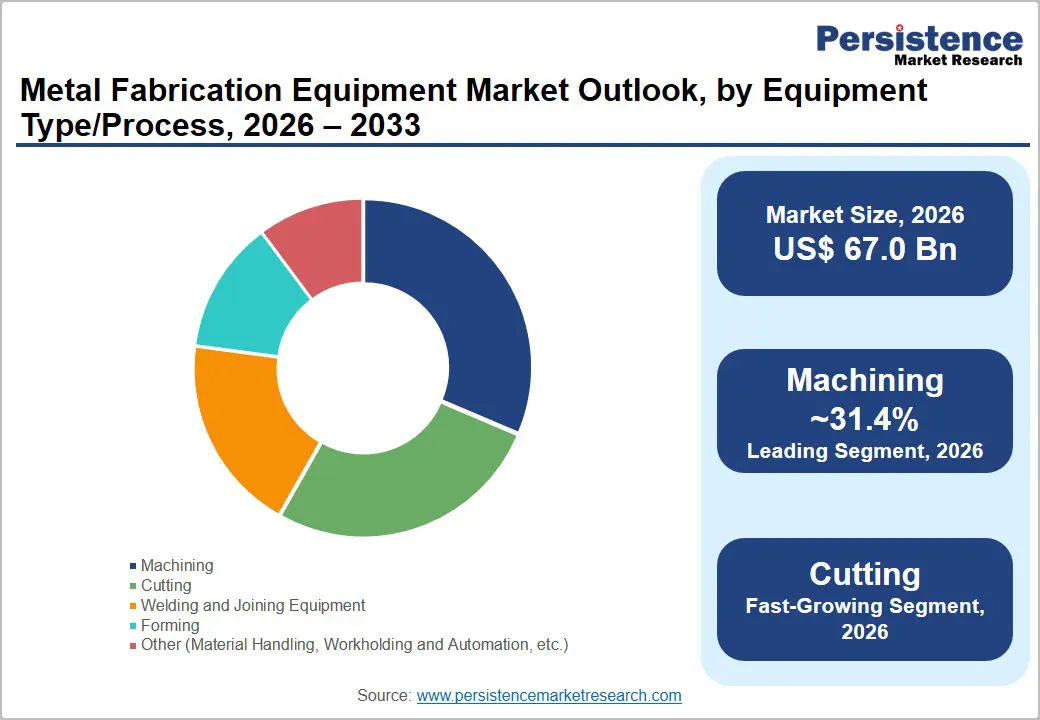

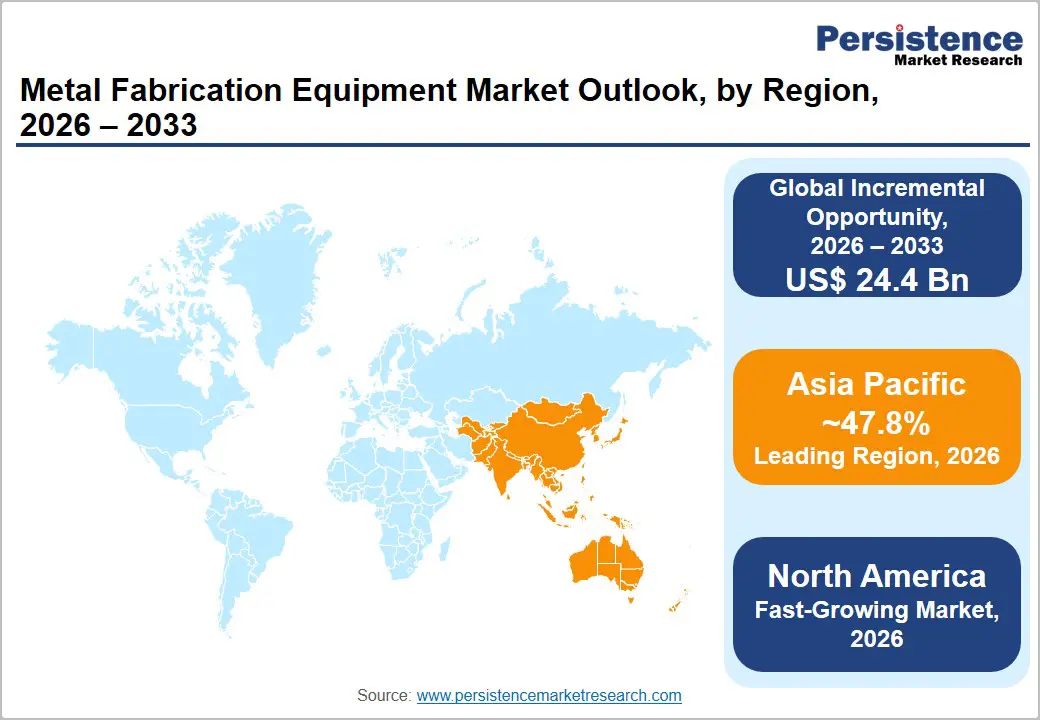

The global metal fabrication equipment market size is likely to be valued at US$67.0 billion in 2026 and is estimated to reach US$91.4 billion by 2033, growing at a CAGR of 4.5% during the forecast period from 2026 to 2033, driven by the rising demand for precision components in electric vehicles and aerospace manufacturing. Increasing adoption of automation and CNC-based smart factories is also improving production efficiency and reducing labor dependency.

Key Industry Highlights:

- Latest Integration: In October 2025, Bystronic announced plans to integrate the acquired Rofin laser technologies into its product portfolio. The company stated that the move would broaden its offerings across metal, glass, ceramic, polymer, and semiconductor processing applications.

- Leading Region: Asia Pacific, with about a 47.8% share in 2026, owing to its large manufacturing base and government-backed industrial policies.

- Fastest-growing Region: North America, backed by surging reshoring initiatives and rising automation adoption.

- Leading Equipment Type/Process: Machining, approximately 31.4% share in 2026, as it delivers the precision required for high-performance industrial components.

- Dominant End-user Industry: Automotive, with a nearly 33.6% share in 2026, owing to its high-volume production and continuous demand for diverse fabrication processes.

DRO Analysis

Driver - Electric Vehicle Production to Demand Retooled Fabrication Lines

The shift to Electric Vehicles (EVs) is compelling automakers to retool entire fabrication lines, thereby propelling demand for new metal fabrication equipment. EV body structures require high-precision stamping and cutting of lightweight materials such as aluminum and Advanced High-Strength Steel (AHSS), which conventional Internal Combustion Engine (ICE) tooling cannot handle.

According to the International Organization of Motor Vehicle Manufacturers (OICA), global automotive production reached 92.5 million units in 2024, with EV platforms now accounting for a growing portion of that output. New EV model launches planned through 2025 to 2026 are triggering fresh equipment procurement cycles. Each new platform typically requires dedicated dies, press lines, and welding systems, meaning model refresh cycles translate into fabrication equipment orders across Original Equipment Manufacturers (OEMs) and Tier-1 suppliers.

Large-Scale Public Construction Spending to Create Sustained Demand

Government-backed infrastructure investment is a reliable and prolonged source of demand for fabricated metal products. According to the U.S. Conference of Mayors, public spending on capital construction grew 76% between 2012 and 2024, reaching US$492 billion, with annual growth accelerating to 9.5% in 2024 alone.

The U.S. Infrastructure Investment and Jobs Act of 2021, which allocated US$550 billion for infrastructure projects using steel, is projected to generate demand for approximately 50 million tons of steel products, according to Worthington Steel. This long pipeline of bridge, highway, and utility projects requires structural beams, trusses, reinforcements, and fasteners, each dependent on metal fabrication equipment. As public construction outlays continue to rise, fabrication capacity must expand alongside them.

Restraint - Metal Price Swings May Disrupt Fabrication Cost Planning

Unpredictable swings in raw material prices are one of the most persistent operational challenges for metal fabricators. According to S&P Global Ratings, steel and aluminum prices have consistently stayed 20% above their ten-year average since the COVID-19 pandemic. The situation escalated sharply in 2025. The U.S. government raised tariffs on imported steel and aluminum from 25% to 50% in June 2025.

It drove U.S. Midwest Premium aluminum prices to 60 cents per pound by mid-2025, a 190% jump from November 2024 levels, according to American Douglas Metals. Fabricators operating on fixed-price contracts faced immediate margin compression. A Federal Reserve Board of Governors study found that rising input costs from the earlier 2018 tariff round were associated with 75,000 fewer jobs in the domestic manufacturing sector. This underscores how input price volatility cascades into broad economic disruption for the entire fabrication industry.

Opportunity - Offshore Wind Tower Development to Require Specialized Heavy Fabrication

The construction of offshore wind turbine towers represents a distinct and technically demanding application for metal fabrication. Steel accounts for approximately 90% of the materials required per megawatt for offshore installations, far exceeding the proportion used in onshore projects, according to the Global Wind Energy Council's (GWEC) Global Offshore Wind Report 2025. This is due to the fact that offshore towers must withstand corrosive marine environments, wave loading, and strong winds.

They hence require thick steel plates, corrosion-resistant alloys, and precision welding that standard fabrication lines are not equipped for. A peer-reviewed study published in Renewable and Sustainable Energy Reviews estimated that global offshore wind development will require between 129 and 235 million tons of steel through 2040. As of 2024, 65 gigawatts (GW) of new offshore projects are in planning or active construction globally, creating a durable and high-specification pipeline for fabrication equipment suppliers.

Launch of Single-Setup Manufacturing Cells That Build and Finish in One Pass

Hybrid fabrication systems that combine additive and subtractive processes in a single machine are changing how complex metal parts are produced. Traditional workflows require multiple machines and setups, additive printing followed by transfer to a separate Computer Numerical Control (CNC) milling machine. Hybrid machines eliminate that transfer step. A 2024 paper published in CIRP Annals, a peer-reviewed journal for manufacturing engineering, described how these systems combine a laser or wire-feed deposition head alongside a multi-axis milling spindle, enabling parts to be built up and finished without repositioning.

A separate 2025 study in Applied Sciences confirmed that hybrid additive-subtractive systems can achieve 97% material utilization efficiency. These can also produce geometrically complex parts that would be impossible to manufacture using either process alone. As aerospace, energy, and defense sectors demand tight tolerances and short lead times, hybrid fabrication cells are predicted to become a feasible production-floor investment.

Category-wise Analysis

Equipment Type/Process Insights

The machining segment is predicted to lead with a share of approximately 31.4% in 2026, as it is the final step that defines precision and tolerances. Almost every fabricated metal part still needs CNC machining to meet exact dimensions. Processes such as cutting or welding shape the part, but machining ensures it fits and functions. This makes it unavoidable across industries. Another factor is the shift toward high-precision components in aerospace, EVs, and medical devices. For example, NASA highlights in its manufacturing guidelines that critical aerospace parts often require tolerances within microns, which only advanced CNC machining can deliver.

Cutting systems are estimated to be the fastest-growing segment over the forecast period, owing to the ongoing shift toward fiber laser technology. Fiber lasers are faster and more energy efficient than CO2 lasers. They also reduce material waste. This makes them attractive in industries where margins are tight. A key driver is sheet metal demand in EVs and electronics. EV battery enclosures and lightweight frames require precise and clean cuts. Companies such as TRUMPF reported that demand for fiber laser cutting machines has increased due to EV and renewable energy projects. These machines can cut reflective materials, including aluminum and copper, which are widely used in EVs.

End-user Industry Insights

Automotive is anticipated to dominate with a share of nearly 33.6% in 2026, as it uses every type of metal fabrication process. A single vehicle involves cutting, stamping, welding, machining, and finishing. This creates continuous demand for a wide range of equipment. The shift to EVs is increasing complexity. EVs require new components such as battery trays, motor housings, and lightweight structures. According to the International Energy Agency (IEA), EV production continues to surge globally, which is increasing demand for fabrication equipment.

Energy and oil & gas are expected to remain in the second position in 2026 owing to large-scale infrastructure expansion and replacement cycles. Pipelines, offshore rigs, wind towers, and hydrogen plants all require heavy metal fabrication. These projects use thick metals, which require advanced cutting, welding, and machining tools. In oil & gas, there is rising investment in maintenance and safety upgrades. Aging pipelines and refineries need replacement parts and retrofitting. According to the IEA, upstream investments are recovering, especially in LNG and deepwater projects. These require high-strength fabricated components, which boost demand for machining and cutting systems.

Regional Insights

Asia Pacific Metal Fabrication Equipment Market Trends

Asia Pacific is anticipated to lead in 2026 with a share of nearly 47.8%, as it has the largest manufacturing base in the world. China, Japan, South Korea, and India produce high volumes of automobiles, electronics, and industrial goods. This creates continuous demand for fabrication equipment. Another driver is government-led industrial expansion. For example, the Asian Development Bank has highlighted that Asia accounts for the majority of global manufacturing output. Policies such as China’s Made in China 2025 and India’s PLI schemes are pushing local production. This increases demand for machining, cutting, and welding systems.

China Metal Fabrication Equipment Market Trends

China will likely lead in Asia Pacific in 2026 with a share of around 48.5% as it is upgrading from low-cost manufacturing to high-tech production. The government is investing heavily in advanced machinery, robotics, and precision engineering. For example, the State Council of China, under its Made in China 2025 plan, has prioritized CNC machines and high-end equipment. This has increased domestic production of fabrication systems and reduced reliance on imports.

India Metal Fabrication Equipment Market Trends

In 2026, India is projected to account for a share of approximately 27.3%, owing to policy-driven manufacturing expansion and gradual industrial upgrades. The government is focusing on increasing domestic production across sectors. Schemes led by the Ministry of Heavy Industries and Make in India are encouraging companies to invest in local plants. This is increasing demand for basic and mid-range fabrication equipment, especially in automotive and infrastructure.

North America Metal Fabrication Equipment Market Trends

North America is predicted to be the fastest-growing market in 2026 with a share of approximately 28.3%, due to reshoring and supply chain shifts. Several companies are bringing manufacturing back from Asia Pacific to reduce risks and improve control. Policies from the U.S. Department of Commerce are supporting domestic production. Incentives for semiconductors, EVs, and clean energy are increasing demand for fabrication equipment.

U.S. Metal Fabrication Equipment Market Trends

A share of nearly 51.4% is expected to be held by the U.S. in 2026, backed by investment in advanced manufacturing and infrastructure. The Infrastructure Investment and Jobs Act is funding large projects in transport, energy, and utilities. These projects require fabricated metal components. The U.S. is also leading in aerospace and defense manufacturing. Organizations such as NASA and defense contractors require high-precision machining. This supports demand for advanced CNC and hybrid systems.

Europe Metal Fabrication Equipment Market Trends

Europe will likely see decent growth over the forecast period, with a share of nearly 19.6% in 2026, as it has a well-established industrial base. Germany, Italy, and Switzerland already have advanced fabrication industries. Growth is stable rather than rapid. A key driver is the shift toward sustainable and energy-efficient manufacturing. The European Commission is promoting green industrial policies. This encourages companies to replace aging machines with energy-efficient ones such as fiber lasers.

Germany Metal Fabrication Equipment Market Trends

Germany will likely register a substantial share of approximately 39.7% in 2026, fostered by its position as a global leader in industrial machinery and precision engineering. Companies such as TRUMPF and DMG MORI continue to innovate in automation and smart manufacturing. The country is investing in Industry 4.0 technologies. According to initiatives supported by the Federal Ministry for Economic Affairs and Climate Action, local factories are integrating IoT and AI into production. This increases demand for advanced fabrication equipment.

U.K. Metal Fabrication Equipment Market Trends

A share of around 25.2% is predicted to be held by the U.K. in 2026, fueled by aerospace, defense, and energy projects rather than mass manufacturing. The government, through the Department for Business and Trade, is supporting advanced manufacturing and clean energy. Offshore wind projects in the North Sea are increasing demand for heavy fabrication. The U.K. also has superior capabilities in precision engineering and research-driven manufacturing. However, limited large-scale manufacturing compared to Germany or China keeps growth moderate. Investments are more focused on high-value and specialized fabrication rather than volume-driven demand.

Competitive Landscape

The global metal fabrication equipment market is moderately fragmented, with a handful of multinational leaders dominating the premium and automated equipment segments. The top four companies, namely, TRUMPF, Amada, DMG MORI, and Yamazaki Mazak, account for around 42% of global revenue, while the remaining share is distributed among various regional and niche players. Competition is constantly shifting from machine performance alone to integrated manufacturing networks.

TRUMPF, Amada, Bystronic, and DMG MORI are differentiating themselves through software platforms, automation, robotics integration, predictive maintenance, and smart factory connectivity. China-based manufacturers, including Han's Laser and Shenyang Machine Tool, are narrowing the technology gap with Western and Japan-based competitors while using large-scale domestic production to deliver significantly lower pricing.

Key Industry Developments:

- In February 2026, Bystronic completed the acquisition of Coherent Corp.’s Tools for Materials Processing business unit. The company noted that the transaction expanded its technology portfolio and established the new Bystronic Rofin business unit, strengthening its position in advanced laser processing applications.

- In October 2025, TRUMPF launched the new generation of the TruLaser Weld 5000 automated laser welding machine. The company reported that the system consumes 20% less energy than its predecessor, as well as delivers fast setup and programming capabilities for small-batch production environments.

- In May 2025, the State of Connecticut awarded TRUMPF a US$2.5 million grant through its Strategic Supply Chain Initiative. The funding will support expansion of the company’s manufacturing operations across North America, including a new press-brake production line scheduled for 2026.

Companies Covered in Metal Fabrication Equipment Market

- Trumpf

- Amada

- DMG MORI

- Yamazaki Mazak

- Bystronic

- Shenyang Machine Tool

- Okuma

- FANUC

- Lincoln Electric

- ESAB Corp.

- Hypertherm

- Doosan Machine Tools

- Haas Automation

- Atlas Copco

- Colfax (Howden)

- Koike Aronson

- Mitsubishi Electric (MC Machinery)

- Prima Industrie

- Salvagnini

- Sandvik

- Others

Frequently Asked Questions

The global metal fabrication equipment market is projected to be valued at US$67.0 billion in 2026.

The metal fabrication equipment market is expected to reach US$91.4 billion by 2033.

Key market trends include increasing adoption of automation and rising use of fiber laser cutting systems.

Machining is expected to be the leading equipment type/process with a share of nearly 31.4% in 2026, as it is a mandatory finishing step in most fabrication processes.

The metal fabrication equipment market is expected to grow at a CAGR of 4.5% from 2026 to 2033.

Trumpf, Amada, and DMG MORI are a few key market players.