- Construction & Engineering

- India Roofing Materials Market

India Roofing Materials Market Size, Share, and Growth Forecast, 2026 - 2033

India Roofing Materials Market by Material Type (Asphalt / Bituminous Shingles, Concrete & Clay Tiles (Concrete Tiles, Clay Tiles), Metal Roofing (Steel, Aluminum, Copper), Plastics / Synthetic Roofing (Polymer-based, composite), Elastomeric Roofing, Misc.), End-user (Residential, Commercial, Industrial), and Regional Analysis for 2026 - 2033

India Roofing Materials Market Size and Trends Analysis

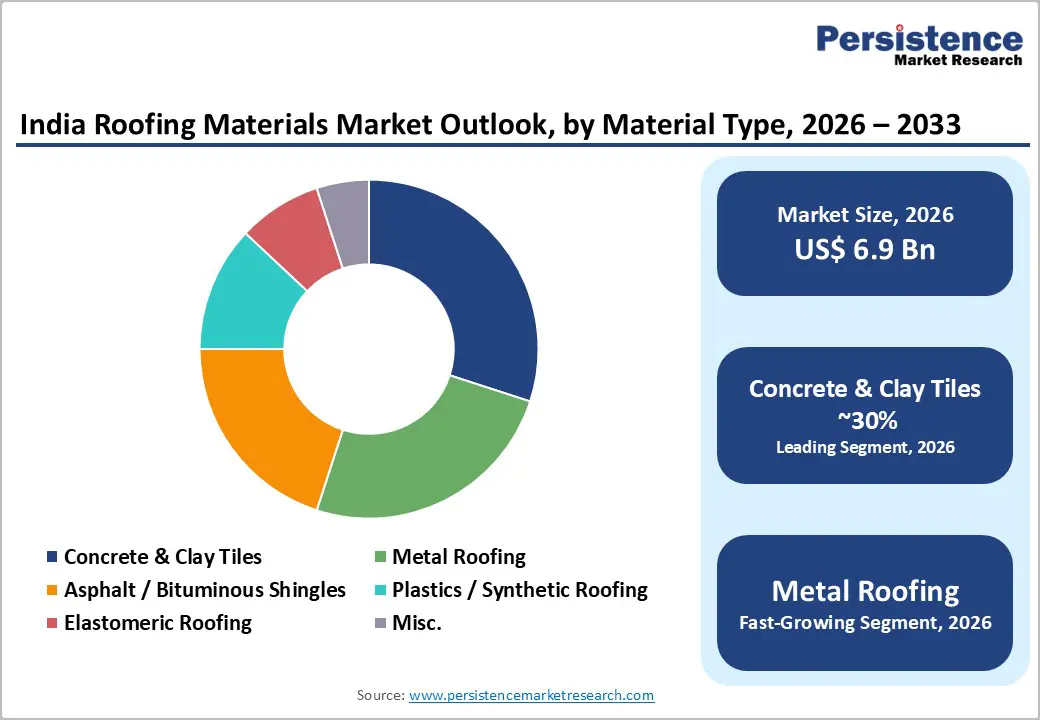

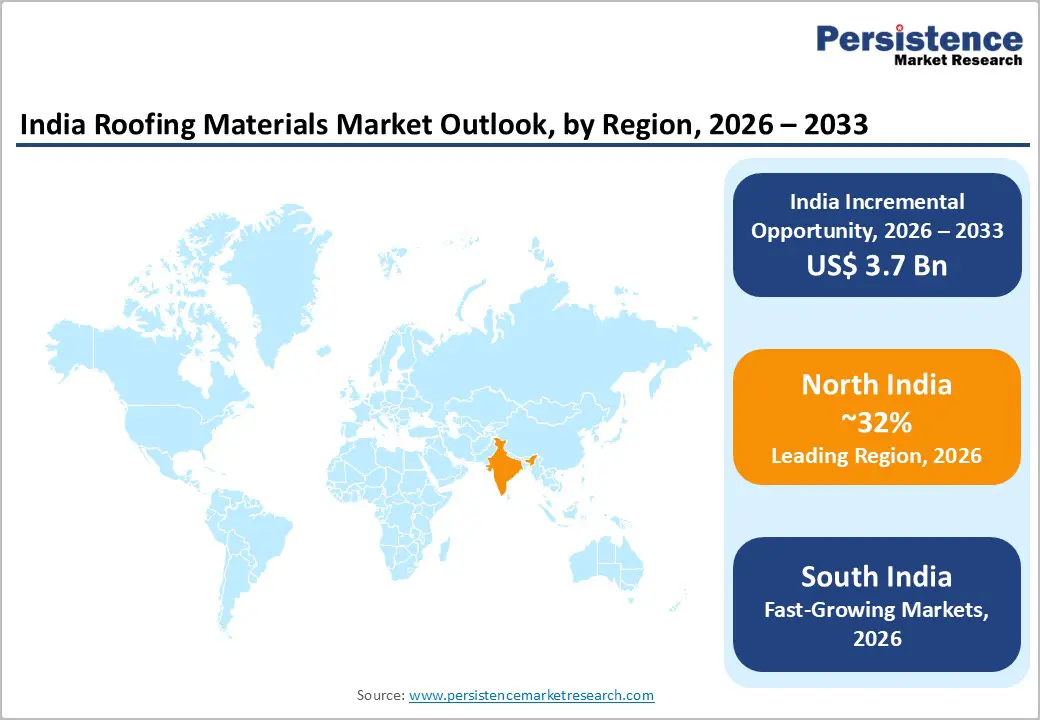

India roofing materials market size was valued at US$ 6.9 Bn in 2026 and is projected to reach US$ 10.6 Bn by 2033, growing at a CAGR of 6.3% between 2026 and 2033.

The market established a strong historical foundation driven by structured demand from India's construction, infrastructure, and real estate sectors. Government-backed affordable housing programs, accelerating commercial real estate activity, and a decisive shift toward energy-efficient and durable roofing technologies have reinforced demand across all material categories. Rapid urbanisation, rising disposable incomes, and policy-driven construction spending sustain the market's trajectory through the forecast period.

Key Industry Highlights:

- Concrete and Clay Tiles Lead the Market: Concrete and clay tiles account for 30% of market revenue in 2026, with strong adoption in southern and coastal regions due to thermal insulation, ventilation, and aesthetic appeal.

- Metal Roofing Fastest-Growing Segment: Driven by industrial, commercial, and large-span civic projects, metal roofing systems, including steel and aluminium, are expanding rapidly due to durability, solar integration, and ease of installation.

- Residential Sector Dominates End-Use: Residential construction represents 45% of market revenue, fueled by government housing schemes like PMAY and urbanisation trends in Tier 2 and Tier 3 cities.

- Commercial and Non-Residential Segment Grows Rapidly: Grade A office parks, data centres, logistics warehouses, and civic infrastructure are driving fast-paced growth in commercial roofing demand across major cities.

- Government Programs Driving Market Demand: Housing programs (PMAY-U, urban infrastructure) and public capital expenditure (US$ 133 Bn in FY24-25) act as strong demand catalysts for roofing materials nationwide.

- Sustainability and Green Building Policies: Energy efficiency regulations, cool-roof policies, and green building certifications are shifting preference toward polymer-based, reflective, and thermally efficient roofing solutions.

| Key Insights | Details |

|---|---|

| India Roofing Materials Market Size (2026E) | US$ 6.9 Bn |

| Market Value Forecast (2033F) | US$ 10.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.6% |

Market Dynamics

Drivers - Government Housing Programs and Public Capital Expenditure Accelerating Construction Demand

Government-led housing and infrastructure expenditure functions as one of the most direct and measurable demand catalysts for the India Roofing Materials Market, as every sanctioned housing unit and public building project creates a specific procurement need for roofing solutions across material types and geographies.

In FY 2024 to 2025, the Government of India raised its capital expenditure by 11.1% to US$ 133 Bn, equivalent to 3.4% of GDP, channelling funds into urban and rural infrastructure development. The Pradhan Mantri Awas Yojana-Urban (PMAY-U) has sanctioned 1.18 crore houses, with 86.6 lakh completed and 1.15 crore grounded for construction as of September 2024.

In August 2023, an additional 1 crore houses were sanctioned under PMAY for urban poor and middle-class families, directly generating large-scale roofing procurement requirements. The 2022 national budget allocated INR 50,000 crore to the Ministry of Housing and Urban Development alongside a US$ 3.5 billion fund to expedite stalled housing projects, reinforcing the policy commitment that sustains demand for the India Roofing Materials Market well into the 2033 forecast horizon.

Urbanisation and Real Estate Structural Expansion Generating Sustained Roofing Demand

Urbanisation-led construction activity represents a structural, long-term demand driver for the India Roofing Materials Market, as the transition of rural population to urban centres necessitates new residential, commercial, and civic construction at scale, each requiring purpose-designed roofing systems.

India's urban population share is projected to surpass 40% by 2030, with Invest India estimating demand for an additional 25 million mid-range and affordable housing units to absorb this demographic shift. India's real estate sector is projected to reach US$ 5.8 Tn by 2047, contributing 15.5% to total economic output, while currently accounting for 6 to 7% of GDP with a trajectory toward 13% by 2025.

Metro rail networks expanded from 248 km to 993 km over the past decade, with daily ridership reaching over 1 crore, indicating the intensity of urban corridor construction that generates sustained roofing demand. The warehousing market alone is projected to generate demand for 159 Mn sq ft by 2047 at an annual CAGR of 4%, each facility unit requiring large-span, high-performance roofing, further reinforcing the aggregate procurement pipeline for India roofing materials market.

Sustainability Regulations and Green Building Certification Reshaping Material Specifications

Regulatory mandates, energy efficiency codes, and green building certification requirements are progressively reshaping material selection within the India Roofing Materials Market, compelling developers and contractors to adopt thermally efficient, low-carbon, and long-lasting roofing solutions in place of conventional alternatives

India's Bureau of Energy Efficiency building code framework and the National Action Plan on Climate Change have heightened the significance of cool-roof performance metrics, solar reflectance, and lifecycle carbon footprints in project procurement decisions. In April 2023, the Government of Telangana launched a state-level cool roof policy specifically targeting heat retention reduction and countering urban heat island effects in densely populated urban zones, setting a regulatory precedent now being referenced by other state administrations.

Construction of facilities under the Smart Cities Mission and HRIDAY program has institutionalised sustainability requirements in public procurement contracts, broadening the addressable market for polymer-based composites, elastomeric membranes, and reflective-coated metal roofing products. India's construction sector is also experiencing rapid premiumization driven by evolving consumer preferences and environmental regulations that collectively support higher-value roofing product adoption.

Restraint - Raw Material Price Volatility and Cost Sensitivity Constraining Market Penetration

The India Roofing Materials Market faces significant structural pressure from price sensitivity, particularly in affordable housing and rural construction segments. Fluctuations in steel, aluminium, and petroleum-derived input prices directly impact the cost structures of metal and synthetic roofing products, creating budgetary constraints for contractors and project developers.

Low-income and semi-urban buyers default toward unbranded or minimum-cost options when premium material prices spike, limiting manufacturers' ability to pass on input cost escalations. This dynamic constrains margin expansion for organised players and slows technology adoption in price-sensitive market tiers, reducing overall premiumization momentum.

Opportunity - Commercial Real Estate and Logistics Infrastructure Building New Demand Corridors

The rapid expansion of commercial construction across Tier 1, 2, and 3 cities is generating significant untapped demand for specialised, high-performance roofing within the India Roofing Materials Market, particularly as large-span industrial and office buildings require roofing solutions that meet institutional durability, thermal, and compliance standards.

India's Commercial Real Estate market, estimated at USD 40.71 billion in 2024, is projected to reach USD 106.05 billion by 2029. Industrial and warehousing space leasing surged by 17% year-on-year in 2024, reaching 20.2 million sq ft across the top five cities, with e-commerce, logistics, and third-party logistics operators as the primary demand generators.

The PM Gati Shakti National Master Plan has assessed over 208 major infrastructure projects worth INR 15.39 lakh crore, accelerating the construction of logistics parks, multimodal terminals, and industrial corridors that require extensive, large-span metal and synthetic roofing systems. Government programs, including Bharatmala Pariyojana and the National Logistics Policy, are further boosting industrial construction activity, creating a durable and expanding procurement pipeline for organised roofing product suppliers across the India Roofing Materials Market.

Smart Cities Mission and Urban Infrastructure Programs Unlocking High-Specification Demand

The Government of India's Smart Cities Mission and associated urban renewal initiatives are driving construction of civic facilities, airports, metro stations, and digital infrastructure, where modern, specification-grade roofing materials are a mandatory requirement, creating a policy-driven, predictable procurement environment.

Airport infrastructure expanded from 74 airports in 2014 to 157 airports in 2024, with the UDAN regional connectivity scheme connecting previously isolated communities and stimulating regional infrastructure construction that drives local roofing demand across previously underserved geographies.

Programs such as AMRUT and Jal Jeevan Mission have catalyzed construction of community water infrastructure, urban amenities, and civic facilities across peri-urban areas, broadening the addressable geography for roofing material suppliers in the India Roofing Materials Market. By October 2024, the Gati Shakti platform had integrated 1,614 data layers across 44 central ministries and 36 states and union territories, enabling coordinated, multi-sector infrastructure execution that accelerates roofing material demand across project categories.

Solar Roofing Integration and Cool-Roof Technologies as High-Value Product Levers

The convergence of renewable energy policy and construction sector sustainability regulations is unlocking a high-value product opportunity in solar-integrated and thermally reflective roofing solutions within the India Roofing Materials Market, as developers and industrial operators seek roofing that serves dual functions of weather protection and energy generation or thermal conservation.

India's commitment to achieving 500 GW of renewable energy capacity by 2030 under the National Solar Mission has catalysed commercial and industrial interest in building-integrated photovoltaic roofing systems, particularly for large-roof-area industrial and warehousing facilities. TPO membranes, which offer solar reflectivity above 0.70 and strong recyclability credentials, are gaining traction with ESG-focused commercial building owners and developers seeking materials that satisfy both performance and sustainability reporting requirements.

Leading manufacturers are investing in patented clip-lock seam systems, factory-attached insulation layers, and high Solar Reflectance Index coatings that deliver measurable lifecycle cost advantages, positioning quality-differentiated products as compelling alternatives to commoditised, price-driven offerings in the India Roofing Materials Market.

Category-wise Analysis

Material Type Insights

Concrete and clay tiles represent the leading material segment of the India Roofing Materials Market, commanding approximately 30% of total market revenue in 2026. This dominance reflects deeply entrenched consumer preference, particularly in southern and coastal regions where clay tiles deliver proven thermal insulation, natural ventilation, and aesthetic compatibility with regional architectural traditions. Concrete tiles have gained parallel traction as a cost-effective, BIS-compliant alternative for large-scale residential and institutional construction under PMAY, offering fire resistance, durability, and structural compatibility with affordable housing specifications.

Mechanised production technologies and the development of lightweight, interlocking clay tile designs have progressively expanded the applicability of both clay and concrete variants beyond traditional residential use into institutional, semi-commercial, and mid-tier construction segments. Tamil Nadu's post-2023 cyclone rebuild programs, however, highlighted a structural vulnerability of traditional concrete tiles against high wind-uplift conditions, driving specification shifts toward composite and metal alternatives in climate-vulnerable geographies and indicating the competitive pressure that could moderate the segment's dominance over the forecast period.

Metal Roofing is the fastest-growing material segment within the Indian Roofing Materials Market, propelled by demand from industrial facilities, warehousing complexes, commercial buildings, and large-span civic infrastructure projects. Metal systems, including galvanised steel, aluminium, and colour-coated sheets, offer superior strength-to-weight ratios, modern galvanising upgrades that extend product warranties to 25 years, solar panel integration compatibility, and patented installation systems that reduce onsite labour requirements by approximately 50% compared to conventional roofing methods.

Application Insights

The residential segment is the dominant end-use category of the India Roofing Materials Market, holding approximately 45% of total market revenue in 2026. India's residential real estate sector recorded sales of approximately 3.65 lakh units across the top seven cities in 2022, surpassing previous highs, with affordable housing under PMAY continuing to lead demand, particularly in Tier 2 and Tier 3 cities and rural townships. Rising homeownership aspirations, government subsidies for pucca housing construction, and strong sales momentum across NCR, Mumbai, Bengaluru, Pune, and Hyderabad have collectively broadened the residential roofing demand base well beyond metro areas

Low home loan rates in preceding cycles and increasing branded developer activity have contributed to record-breaking residential sales volumes, with the real estate sector's contribution to India's GDP projected to nearly double from 6 to 7% currently to 13% by 2025. This sustained housing sector expansion ensures that the Residential segment retains its dominant position within the India Roofing Materials Market over the forecast period, anchored by both policy-driven affordable housing and aspirational mid-income residential construction.

The commercial and non-residential segment is the fastest-growing end-use category within the India Roofing Materials Market, underpinned by large-scale investment in Grade A office parks, data centres, logistics warehouses, airport terminals, retail malls, and public civic infrastructure. Grade A office space demand across the top seven Indian cities reached a cumulative 264 million sq ft between 2019 and 2024, with average office rentals surpassing pre-pandemic levels in 2024, reflecting robust occupier demand from IT/BPO, BFSI, and flexible workspace operators.

Competitive Landscape

The India roofing materials market is moderately fragmented, with a mix of large national players and numerous regional manufacturers competing across metal roofing, tiles, polymer sheets, and speciality membranes. Leading companies such as Tata BlueScope Steel, JSW Steel Coated Products Ltd., Hindalco Industries Ltd., Everest Industries Ltd., Bansal Roofing Products Ltd., and Visaka Industries Ltd. dominate the organised segment, leveraging strong brand recognition, pan-India distribution, and integrated manufacturing capabilities.

These major players control a significant portion of the market, particularly in industrial and commercial applications, giving the sector pockets of oligopolistic characteristics. At the same time, numerous smaller and regional manufacturers cater to residential and rural demand, reflecting the fragmented nature at the lower end of the market. Niche players like Monier Roofing and BirlaNu Limited focus on lightweight polymer sheets, UPVC roofing, and customised solutions, adding to market diversity.

Key Industry Developments:

- In May 2025, JSWSCPL continued to strengthen its position in the roofing and value-added steel products market by expanding capacity and operationalising new facilities, including a colour coating plant in Jammu & Kashmir. The company reported a sales volume of 4.11 mtpa in FY24, generating INR 34,137 crore in revenue, with strong operating profitability of INR 3,710 per tonne. Increased domestic demand for coated steel products, which are widely used in roofing applications, helped stabilise performance despite a decline in average steel prices, supporting the growth of the Indian roofing materials market.

- In February 2025 Praana Group, an India-based holding company, acquired Owens Corning’s glass reinforcements business, which supports composites and building materials, including products relevant to roofing. This strategic acquisition expands Praana Group’s footprint in advanced materials for the industrial and construction sectors in India. The move is expected to strengthen the company’s capabilities in glass fiber reinforcements for roofing and building applications, improve operational efficiency, and support the growing demand for high-performance, durable roofing materials in India’s residential and commercial construction markets.

- In April 2025, Metecno India, a subsidiary of Metecno Holding Asia B.V., Netherlands, advanced its position in the Indian roofing materials market by innovating in insulated sandwich panels for industrial, commercial, and cold storage applications. The company’s panels incorporate Polyurethane Foam (PUF), Polyisocyanurate Foam (PIR), and Mineral Wool (Rockwool), offering superior thermal insulation, fire resistance, and acoustic performance. Metecno India’s focus on sustainability, energy efficiency, and precision-engineered interlocking systems enhances the durability and insulation performance of roofs, addressing the rising demand for high-performance, eco-friendly roofing solutions in India.

Companies Covered in India Roofing Materials Market

- BlueScope Steel

- Hindalco Industries Ltd

- JSW Steel Coated Products

- CK Birla Group (HIL Ltd)

- Everest Industries Ltd

- Owens-Corning

- Compagnie de Saint-Gobain S.A.

- Bansal Roofing Products Ltd

- Metecno India Pvt Ltd

- Indian Roofing Industries Pvt Ltd

- Visaka Industries Ltd

- Ramco Industries Ltd

- Onduline India

- Interarch Building Products

- Saint-Gobain India Pvt Ltd

- Bhushan Power & Steel Ltd

- JSW Everglow (JSW Steel)

- LYSAGHT® Roofing Solutions

Frequently Asked Questions

The India Roofing Materials Market is projected to be valued at US$ 6.9 Bn in 2026.

The Concrete & Clay Tiles segment is expected to account for approximately 62% of the India Roofing Materials Market by Material Type in 2026.

India Roofing Materials market is expected to witness a CAGR of 6.3% from 2026 to 2033.

India Roofing Materials Market growth is primarily driven by government housing programs and public capital expenditure boosting construction demand, rapid urbanization and real estate expansion creating sustained roofing needs, and evolving sustainability regulations and green building mandates shaping the adoption of energy-efficient and high-performance roofing materials.

Key market opportunities in the India Roofing Materials Market lie in commercial real estate and logistics infrastructure expansion, Smart Cities and urban infrastructure programs driving high-specification demand, and adoption of solar-integrated and cool-roof technologies offering high-value, sustainable roofing solutions.

Key players in the Roofing Materials Market include Tata BlueScope Steel, JSW Steel Coated Products Ltd., Hindalco Industries Ltd., Everest Industries Ltd., Bansal Roofing Products Ltd., and Visaka Industries Ltd.