- Construction & Engineering

- Hydraulic Elevators Market

Hydraulic Elevators Market Size, Share, and Growth Forecast, 2026 - 2033

Hydraulic Elevators Market by Product Type (Hole-less, Roped, Others), Capacity (1000-2000 kg, 4000-8000 kg, Others), Application, Speed, and Regional Analysis for 2026 - 2033

Hydraulic Elevators Market Size and Trends Analysis

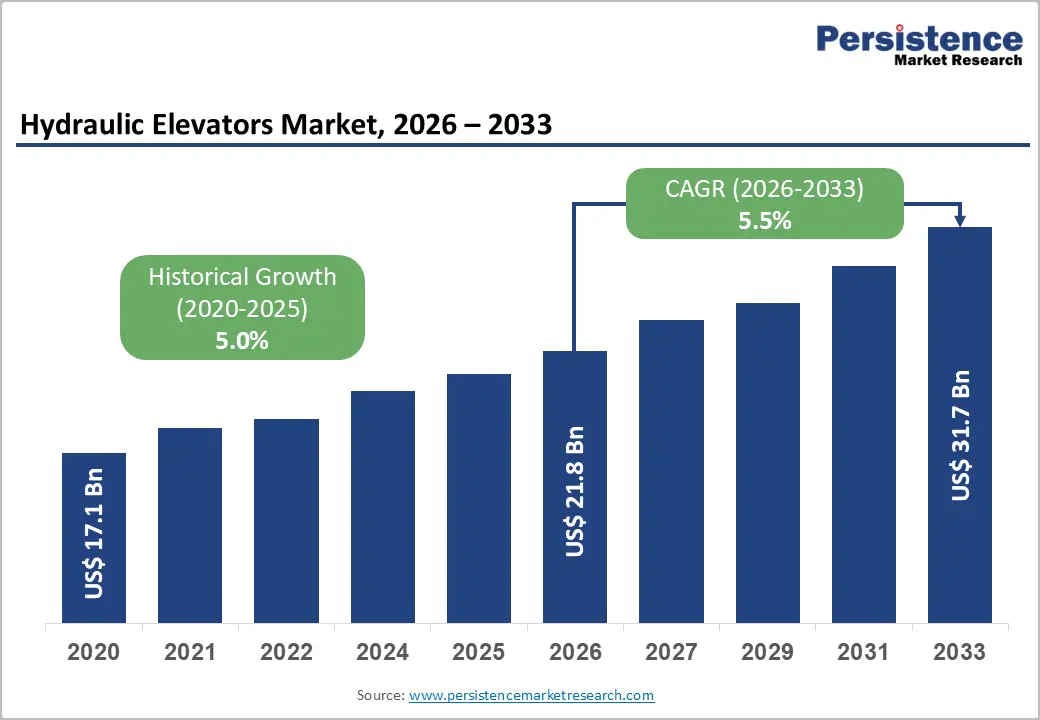

The global hydraulic elevators market size is likely to be valued at US$21.8 billion in 2026 and is expected to reach US$31.7 billion by 2033, growing at a CAGR of 5.5% between 2026 and 2033, driven by steady demand in low- and mid-rise construction, increasing retrofit activity across aging building infrastructure, and tightening accessibility and safety regulations.

Demographic shifts, particularly the rising aging population, are reinforcing demand for barrier-free vertical mobility solutions across residential and institutional settings. Hydraulic elevators are primarily deployed in low-rise and select mid-rise buildings, where cost efficiency, installation flexibility, and moderate speed requirements outweigh the need for high-speed vertical transport. These systems remain widely used across residential buildings, healthcare facilities, and retrofit projects due to their relatively simple design and adaptability to constrained building layouts.

Key Industry Highlights:

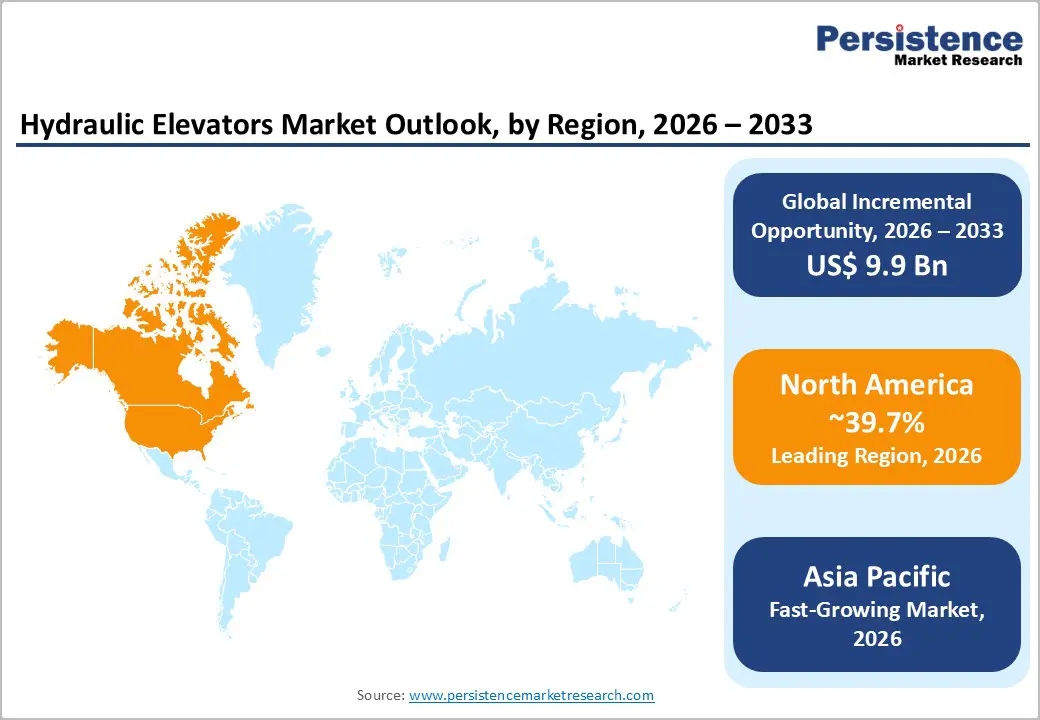

- Leading Region: North America is projected to lead the market with approximately 39.7% share, supported by strong retrofit demand, stringent accessibility regulations, and a well-established service ecosystem.

- Fastest-growing Region: Asia Pacific is the fastest-growing region, driven by rapid urbanization, expanding low- and mid-rise construction, and increasing adoption of cost-effective hydraulic systems.

- Investment Plans: Industry investments are increasingly focused on modernization, digital monitoring systems, and energy-efficient upgrades, particularly in North America and Europe, where aging infrastructure is creating sustained demand for phased elevator upgrades.

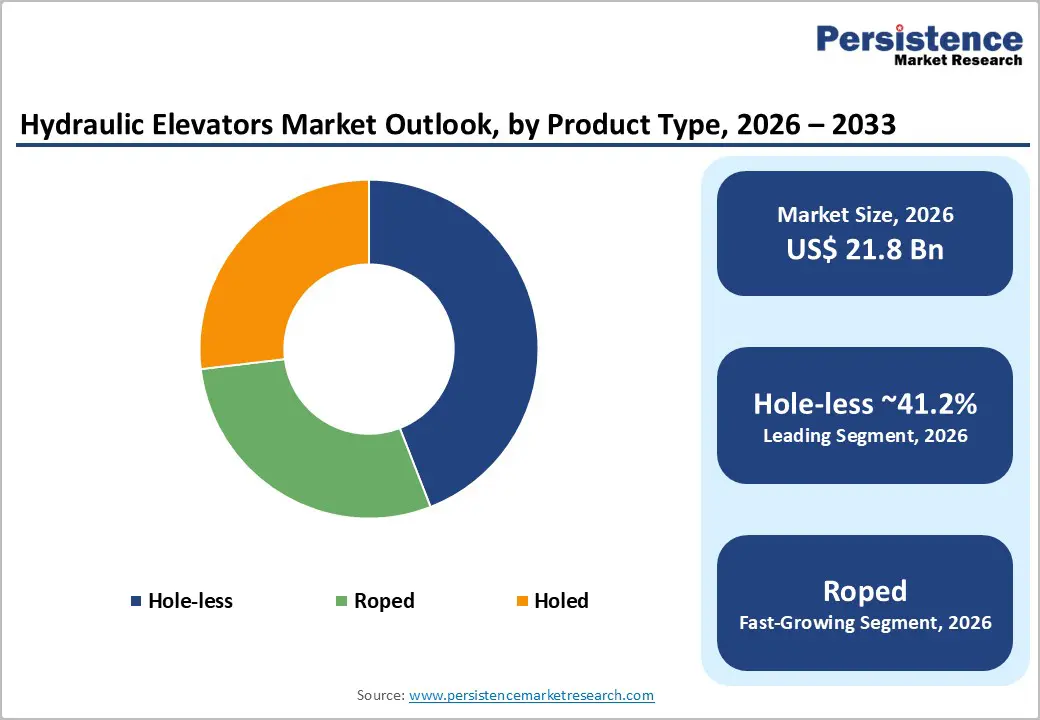

- Dominant Product Type: Hole-less hydraulic elevators dominate with an anticipated share of nearly 41.2%, owing to their ease of installation, reduced civil work requirements, and suitability for urban and retrofit applications.

- Leading Capacity: The 1000-2000 kg capacity segment leads with an anticipated share of approximately 36.8%, as it aligns with the requirements of most residential and small commercial buildings.

| Key Insights | Details |

|---|---|

| Hydraulic Elevators Market Size (2026E) | US$21.8 Bn |

| Market Value Forecast (2033F) | US$31.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.0% |

DRO Analysis

Driver Analysis - Aging Population and Accessibility-Driven Demand

The global population aged 60 years and above is increasing rapidly, creating sustained demand for accessible infrastructure. A significant proportion of existing residential buildings lack features such as step-free access and vertical mobility systems, particularly in multi-story homes. This structural gap is driving the adoption of hydraulic elevators in residential retrofit projects, assisted living facilities, and healthcare environments. The ability of hydraulic systems to be installed with minimal structural modification makes them particularly suitable for aging-in-place solutions, thereby strengthening long-term demand.

Regulatory Expansion and Compliance Requirements

Governments and regulatory bodies across major economies are enforcing stricter accessibility and safety standards for buildings. Regulations mandate the inclusion of elevators in public and commercial infrastructure, particularly in healthcare, education, and retail facilities. These compliance requirements often trigger new installations or upgrades of existing systems. Hydraulic elevators benefit in low-rise environments where meeting regulatory thresholds efficiently is critical. Standardization frameworks also enhance product reliability and safety, supporting broader adoption across regulated sectors.

Modernization of Aging Building Infrastructure

A substantial share of the global elevator installed base is over two decades old, particularly in North America and Europe. Building owners are increasingly opting for modernization rather than complete replacement to manage costs and minimize operational disruption. Hydraulic elevators play a key role in these upgrades due to their compatibility with existing building structures. Modernization programs typically include upgrades to control systems, safety features, and energy efficiency components, creating recurring revenue streams for manufacturers and service providers.

Restraint Analysis - Competition from Traction and Machine-Room-Less Systems

Hydraulic elevators face increasing competition from traction and machine-room-less (MRL) systems, which offer advantages such as higher energy efficiency, reduced space requirements, and broader application across building types. These alternatives are increasingly preferred in mid-rise developments and new construction projects. As a result, hydraulic systems are gradually being confined to specific use cases, limiting their penetration in newer, design-optimized buildings.

Energy Efficiency and Lifecycle Cost Concerns

Hydraulic elevators generally consume more energy compared to newer traction-based systems, particularly in high-usage environments. This results in higher operating costs over the lifecycle of the equipment. As building owners place greater emphasis on sustainability and energy efficiency, hydraulic systems face challenges in premium and environmentally certified projects. While modernization can improve efficiency, the perception of higher lifecycle costs remains a constraint on broader adoption.

Opportunity Analysis - Retrofit and Modernization in Mature Markets

Developed regions with aging infrastructure present a significant opportunity for hydraulic elevator providers. Retrofitting older buildings with modern elevator systems is often more cost-effective than full replacement. Hydraulic elevators are particularly suited for these projects due to their installation flexibility and lower structural requirements. This creates opportunities not only for equipment sales but also for long-term service contracts, maintenance, and component upgrades.

Residential Mobility and Home Elevator Adoption

The residential segment offers strong growth potential, driven by increasing demand for home elevators in multi-story houses and luxury residences. Consumers are prioritizing convenience, accessibility, and property value enhancement. Innovations such as compact designs, pitless installations, and customizable cabins are expanding the addressable market. This trend is particularly pronounced in urban and suburban areas with aging populations and rising disposable incomes.

Urbanization and Low-Rise Construction in Emerging Markets

Rapid urbanization in Asia Pacific and other emerging regions is driving demand for cost-effective vertical mobility solutions. A large proportion of new construction in these regions consists of low- to mid-rise buildings, where hydraulic elevators are a practical and economical choice. Their ease of installation and lower upfront cost make them attractive for residential complexes, small commercial buildings, and institutional facilities, supporting faster market expansion.

Category-wise Analysis

Product Type Insights

Hole-less hydraulic elevators are expected to dominate the market with an anticipated share of 41.2% in 2026, primarily due to their installation advantages and adaptability to modern construction constraints. These systems eliminate the need for deep underground drilling, significantly reducing construction complexity, excavation risk, and overall project timelines. They are particularly well-suited for urban infill developments, retrofit projects, and space-constrained buildings, where traditional holed systems are not feasible. From a practical standpoint, hole-less systems are widely adopted in low-rise residential complexes, small office buildings, and healthcare facilities where minimal structural disruption is critical. For example, retrofitting older apartment buildings in dense cities or upgrading hospitals without interrupting operations often favors hole-less designs. Their compliance with safety standards, coupled with lower civil engineering costs, reinforces their position as the preferred solution across both developed and emerging markets.

Roped hydraulic elevators are emerging as the fastest-growing segment, driven by increasing demand for improved efficiency, flexibility, and modern design integration. These systems combine hydraulic drive mechanisms with roping technology, allowing for better space utilization and smoother performance compared to traditional configurations. Growth is particularly strong in premium residential developments, luxury villas, boutique hotels, and architecturally complex commercial buildings, where both aesthetics and performance are important. For instance, high-end homes and designer buildings increasingly require elevators that can be installed without large pits or machine rooms while still offering enhanced ride quality. This segment is also benefiting from the trend toward compact, customizable, and energy-optimized solutions, making it attractive for developers seeking differentiated building features without major structural modifications.

Capacity Insights

The 1000-2000 kg capacity segment is expected to lead with an anticipated share of approximately 36.8% in 2026, as it aligns closely with the operational requirements of most residential and small-to-medium commercial buildings. This capacity range offers an optimal balance between passenger handling, space utilization, and installation cost, making it the default choice for a wide range of applications. Typical use cases include apartment buildings, office spaces, retail outlets, and mid-sized healthcare facilities, where elevators need to accommodate moderate passenger volumes without requiring heavy-duty infrastructure. For example, residential complexes with four to eight floors or small office buildings often specify this capacity range to ensure efficiency without overdesigning the system. Its versatility and cost-effectiveness continue to reinforce its dominance across both new installations and modernization projects.

The 4000-8000 kg segment is expected to be the fastest-growing, supported by increasing demand in industrial, healthcare, and logistics environments where heavy load handling is essential. These elevators are designed to transport large equipment, hospital beds, pallets, and bulk goods, making them critical for operational efficiency in specialized facilities. Growth in this segment is closely linked to the expansion of warehousing, manufacturing plants, hospitals, and mixed-use developments. For instance, modern hospitals require elevators capable of moving patient beds and medical equipment seamlessly, while logistics hubs depend on high-capacity systems for material movement. As infrastructure investment continues to rise in these sectors, demand for higher-capacity hydraulic elevators is expected to accelerate, particularly in emerging economies and industrial corridors.

Regional Insights

North America Hydraulic Elevators Market Trends - Retrofit-Driven Market Led by Regulatory Compliance and Aging Infrastructure

North America is expected to lead the hydraulic elevators market with approximately 39.7% market share in 2026, supported by a highly structured regulatory environment and a significant base of aging infrastructure. The U.S. remains the dominant contributor, where accessibility mandates such as the Americans with Disabilities Act (ADA) and safety codes enforced through ASME standards continue to drive both new installations and modernization projects. A large portion of the installed elevator base in the U.S. and Canada is over two decades old, creating a sustained pipeline for upgrades, particularly in low- and mid-rise residential and institutional buildings.

Key growth drivers include strong retrofit demand, regulatory compliance requirements, and increasing adoption of home elevators. Major players such as Otis Worldwide Corporation and Schindler Group have expanded modernization offerings in North America, focusing on phased upgrades, smart monitoring systems, and energy-efficient components. For example, Otis has introduced modular modernization packages that allow building owners to upgrade controls and safety systems without full replacement, reducing downtime and capital expenditure. The presence of a mature service ecosystem further strengthens the region, with companies such as Savaria Corporation expanding their portfolio of home elevators and accessibility solutions. This is particularly relevant in Canada, where aging demographics and accessibility-focused housing policies are accelerating residential elevator adoption. Investment trends are increasingly centered on digitalization, predictive maintenance, and sustainability, positioning North America as a service-driven and innovation-focused market.

Europe Hydraulic Elevators Market Trends - Modernization-Focused Growth across Legacy Building Stock

Europe’s market growth is primarily driven by the modernization and refurbishment of existing infrastructure rather than new construction activities. A substantial share of the region’s building stock was developed several decades ago, and many of these structures continue to rely on outdated elevator systems. As a result, there is a growing need to upgrade these systems to comply with current safety standards, accessibility regulations, and energy efficiency requirements. This trend is significantly contributing to the demand for elevator modernization solutions across the region.

Key markets such as Germany, the U.K., France, and Spain demonstrate steady demand across both residential and commercial sectors. Leading companies such as KONE Corporation, TK Elevator, and Schindler Group are actively investing in modernization and digital service platforms. For instance, KONE has expanded its digital connectivity solutions in Europe, enabling real-time monitoring and predictive maintenance, which improves uptime and reduces lifecycle costs for building owners. TK Elevator has also strengthened its presence in Southern Europe through modernization contracts targeting residential complexes and public infrastructure. These developments highlight a shift toward lifecycle cost optimization, energy-efficient upgrades, and smart elevator ecosystems. Investment activity remains concentrated in retrofit projects, particularly in dense urban areas such as Paris, London, and Madrid, where upgrading existing buildings is more feasible than new construction.

Asia Pacific Hydraulic Elevators Market Trends - Rapid Urbanization Fueling Cost-Effective Hydraulic Elevator Adoption

Asia Pacific is the fastest-growing region, driven by rapid urbanization, population expansion, and rising middle-class income levels. The region’s construction landscape is dominated by low- and mid-rise buildings, especially in emerging economies, making hydraulic elevators a cost-effective and practical solution. Governments across the region are investing heavily in urban infrastructure and housing development, further supporting market growth. China, Japan, and India are the primary contributors, each offering distinct advantages. Japan remains a technological hub with companies such as Mitsubishi Electric Corporation and Hitachi Ltd. focusing on advanced elevator systems and reliability. Meanwhile, India is emerging as a key growth market, with domestic players such as Elite Elevators and BRIO Elevators introducing compact and customized hydraulic home elevators tailored to urban residential needs.

In South Korea, Hyundai Elevator has invested in smart factory infrastructure and R&D capabilities, enhancing production efficiency and innovation in elevator systems. Across Southeast Asia, increasing investments in affordable housing and mixed-use developments are driving demand for cost-efficient vertical mobility solutions. Local manufacturing and supply chain localization are key factors shaping the region, as they reduce costs and improve delivery timelines. As a result, Asia Pacific is evolving into both a high-growth consumption market and a global manufacturing hub, with strong long-term potential supported by infrastructure expansion and urban development initiatives.

Competitive Landscape

The global hydraulic elevators market is moderately consolidated at the global level but remains fragmented in regional segments. Large multinational companies dominate through strong brand presence, advanced technology, and extensive service networks. At the same time, regional and local players compete effectively by offering cost-competitive, customized solutions tailored to local building requirements.

Key strategies include product innovation, service-led revenue models, and geographic expansion. Companies are prioritizing modernization services, digital monitoring, and energy-efficient solutions while expanding their presence in emerging markets. Differentiation is increasingly based on lifecycle value, customization, and installation efficiency.

Key Industry Developments:

- In February 2026, Otis Worldwide Corporation launched its Arise MOD Prime and Arise MOD Plus modernization solutions in North America, enabling building owners to upgrade low- and mid-rise elevators in phases, improving safety, energy efficiency, and operational flexibility.

- In November 2025, Otis Worldwide Corporation expanded its Gen3 Core™ elevator platform, offering larger cabins and higher lifting capacity specifically designed for low- to mid-rise residential and commercial buildings, strengthening its position in the hydraulic-compatible segment.

Companies Covered in Hydraulic Elevators Market

- Otis Worldwide Corporation

- Schindler Group

- KONE Corporation

- TK Elevator

- Mitsubishi Electric Corporation

- Hitachi Ltd.

- Hyundai Elevator

- Fujitec Co., Ltd.

- Toshiba Elevator and Building Systems Corporation

- Savaria Corporation

- KLEEMANN Group

- Sigma Elevators

- Elite Elevators

- BRIO Elevators

- Wittur Group

- Escon Elevators Pvt Ltd

Frequently Asked Questions

The hydraulic elevators market is expected to be valued at US$21.8 billion in 2026.

The hydraulic elevators market is projected to reach US$31.7 billion by 2033, driven by steady demand in low- and mid-rise construction and modernization projects.

Key trends include increasing retrofit and modernization activities, rising demand for home elevators and aging-in-place solutions, and growing adoption of digital monitoring and energy-efficient systems.

The hole-less hydraulic elevator segment leads the market, accounting for nearly 41.2% share, due to its ease of installation and suitability for urban and retrofit applications.

The hydraulic elevators market is expected to grow at a CAGR of 5.5% from 2026 to 2033.

Some of the major players include Otis Worldwide Corporation, Schindler Group, KONE Corporation, TK Elevator, and Mitsubishi Electric Corporation.